So… the next T-Bills auction is on 26 Oct (Thursday).

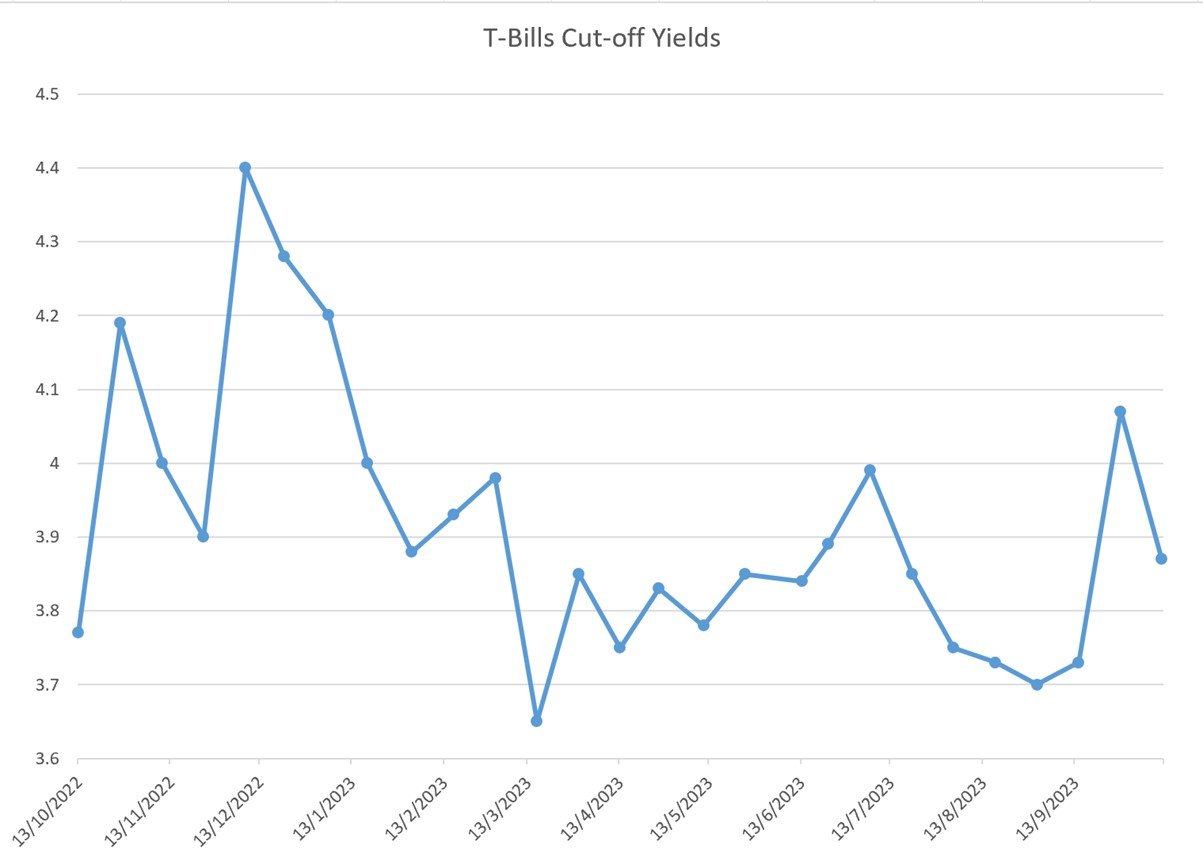

As you would recall – 2 auctions ago T-Bills went as high as 4.07%.

Then after that, demand for T-Bills soared, and yields dropped to 3.87%.

What will happen the next auction?

Will we see interest rates cross 4.0% again?

Are T-Bills still worth buying vs other options like Fixed Deposit or Singapore Savings Bonds?

Let’s dive in.

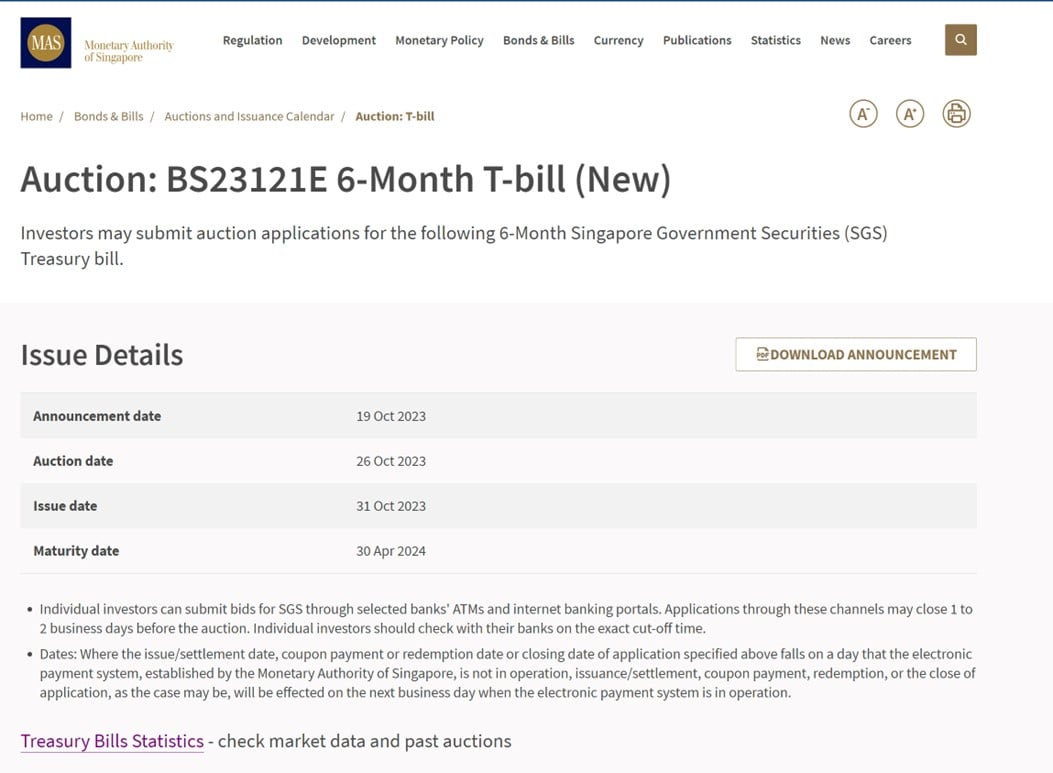

Next T-Bills auction is on 26 Oct (Thursday) – (BS23121E 6-Month T-bill)

First off – next 6 months T-Bills auction is on 26 Oct 2023 (Thurs).

If you’re applying in cash do apply by 9pm on 25 Oct 2023 (Wed)

For CPF-OA you’ll want to get it done by 24 Oct 2023 (Tues).

What is the estimated yield on the next 6-month T-Bills auction? (BS23121E 6-Month T-bill)

T-Bills trade at 3.85% on the open market

6-month T-Bills are pretty much unchanged.

Trading at 3.85% on the open market.

But… T-Bill trading liquidity is incredibly thin

But we’ve seen the past few auctions that trading liquidity on the T-Bills is so thin – that actually the market pricing is not indicative.

In fact you’ll find that the market pricing actually takes its cue from the latest T-Bills auction.

The past few auctions where the T-Bills auction yield diverged materially from market price.

It was actually market price that adjusted to the latest T-Bills auction yield, rather than the other way around.

So I would caution against placing too much reliance on market pricing on T-Bills – there just isn’t sufficient trading liquidity for true price discovery.

12-week MAS Bills flat at 4.05%

The institutional only 12-week MAS Bills have been flat the past month or two – at 4.05%.

Sharp moves in MAS Bills are a good indicator of the trend for T-Bills.

So as of now, MAS Bills are not showing any big changes in yields either way.

If you are submitting a competitive bid I do suggest taking a quick look at the latest MAS Bills pricing before you apply.

If there is a sharp move up or down – that could suggest a similar trend for T-Bills (can access it here).

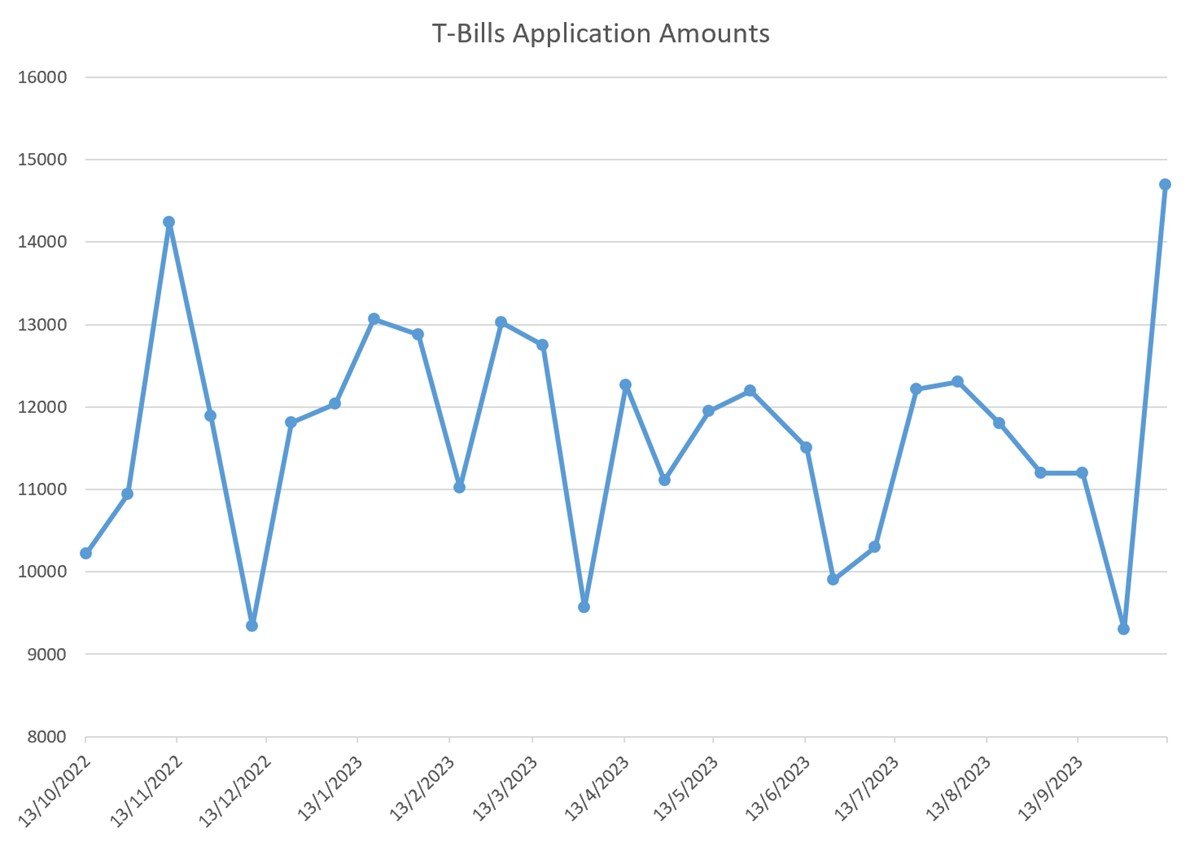

Demand for T-Bills soared the previous auction – causing yields to drop to 3.87%

After the previous round of T-Bills was issued at 4.07%.

Demand for T-Bills absolutely soared after that.

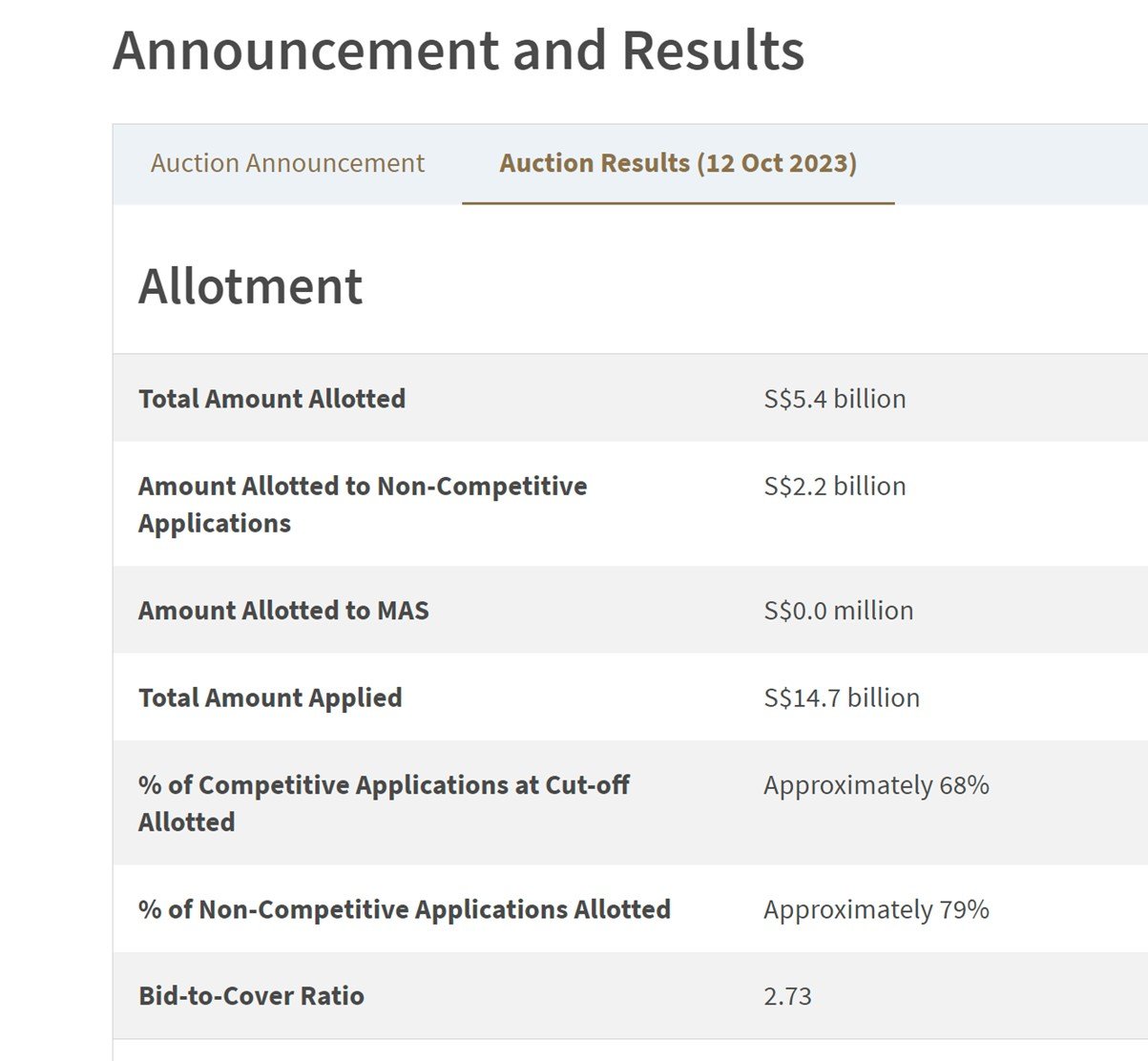

A huge 58% increase in T-Bills application amounts – from $9.3 billion to $14.7 billion.

This caused a sharp drop in T-Bills cut-off yields.

From 4.07% to 3.87%:

Will demand for T-Bills stay high?

Given that demand for T-Bills was so high.

To the point where non-competitive bids only saw 68% allotment.

It looks like we’ll see investors who didn’t get their allotment the previous auction try their hand for this auction.

So you may see demand stay elevated.

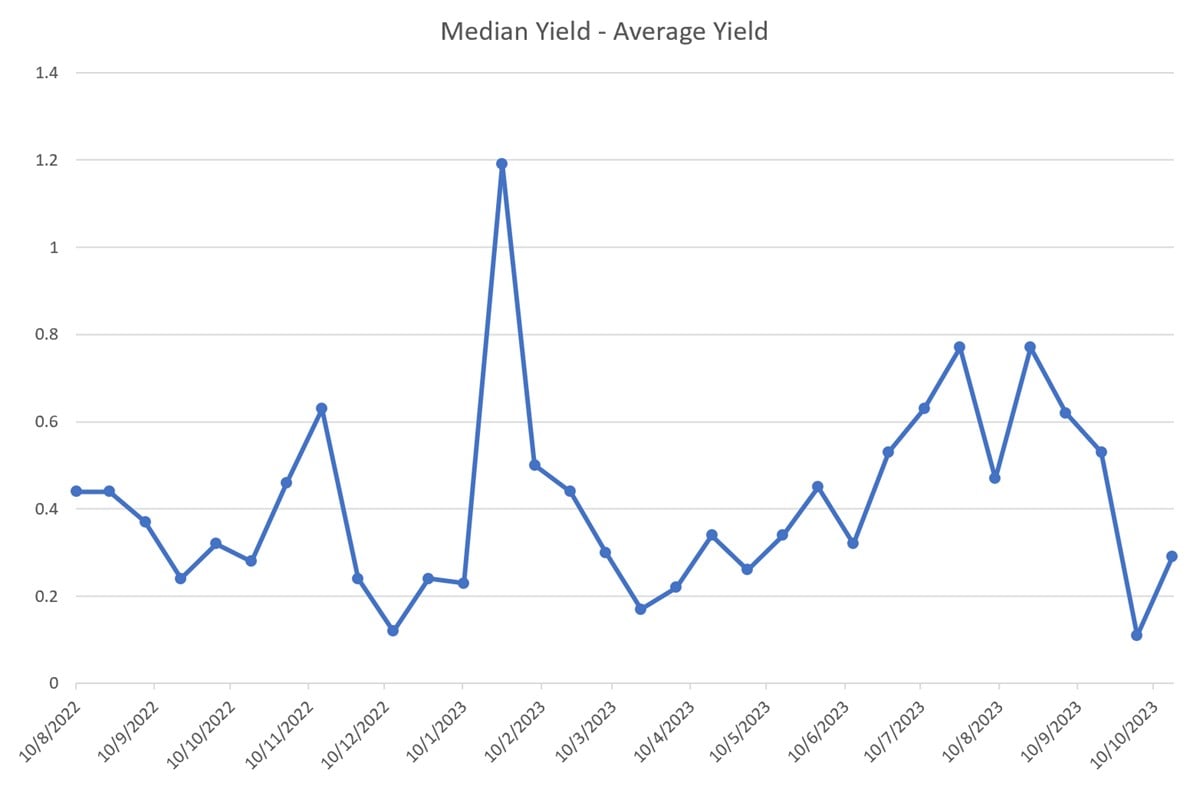

Median Yield – Average Yield narrowed – more “lowballers”?

To illustrate what this is:

Imagine you have 100 bids.

The median yield, is if you arrange all the bids from small to high, and take the yield of the 50th bid.

While average yield, is adding up the yields of all 100 bids and dividing by 100.

So average yields are skewed by lowball bids, while median yields are not.

To put it simply – the bigger the spread between the median yield and average yield, the more “low-ballers”.

And interestingly you can see how despite demand for T-Bills increased massively the last auction.

The median – average yield spread actually didn’t increase that significantly, indicating that bidding was still somewhat rational.

Given that the last auction only saw 68% allotment for non-competitive bids.

Will we see investors submit more low ball competitive bids just to get an allotment?

You know, the guys who submit a 1.0% competitive bid so that they will get an allotment no matter what?

I don’t know – but let’s hope not.

Estimated yield of 3.75% – 3.95% on the 6-month T-Bills auction? (BS23118S 6-Month T-bill)

Putting all this together.

The fact that demand may remain high, and you may get low-ball competitive bids.

While the overall interest rate climate remains supportive of higher yields.

I would probably go with a conservative estimated yield of 3.75% – 3.95% on the next T-Bills auction.

For obvious reasons though – there is significant uncertainty because you just can’t predict with certainty how investors will bid.

The other wildcard is the Israeli-Hamas conflict.

If we get a significant escalation in the conflict next week, then all bets are off.

As always, I encourage investors to submit a competitive bid (just in case there is a freak result and yields drop a lot).

And submit as close to the deadline as you can, so you can take a look at where market pricing is at that time before deciding on your bid.

Are T-Bills still worth buying vs Singapore Savings Bonds or Fixed Deposit or Savings Accounts?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

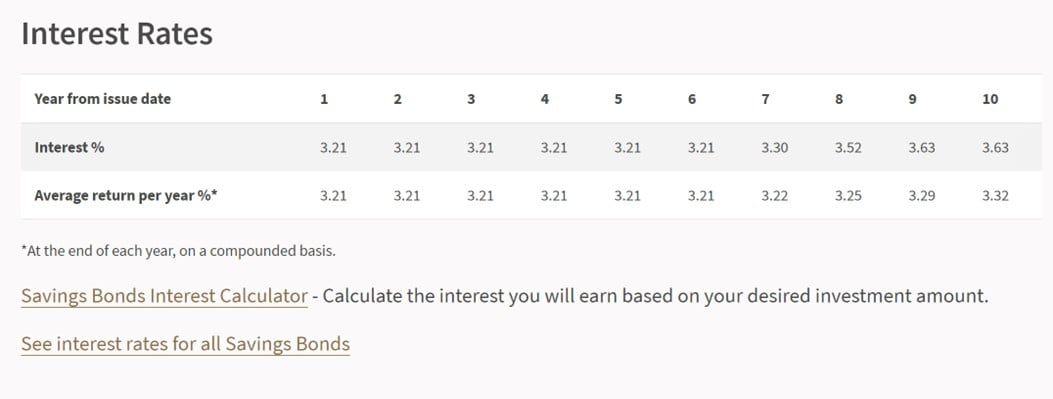

Singapore Savings Bonds are a decent buy – and will get better

I just want to put it out there that this month’s Singapore Savings Bonds are decently attractive.

You’re locking in 3.21% yield for the next 6 years, stepping up to 3.32% over 10 years.

That’s risk free yield locked in for 10 years, and you can get the money back anytime with no capital loss.

Considering CPF-OA pays 2.5%, to be able to get 3.32% risk free for 10 years is very attractive.

Next month’s SSBs will be even better

Singapore Savings Bonds yields track the average yield 10 year Singapore government security for the previous month.

The average yield on the 10 year SGS this month so far, is about 3.3 – 3.5%.

Put that together, and you might see next month’s Singapore Savings Bonds offer around:

- 3.4% for 10 years

- 3.3% for first 5 years or so

That’s likely even better than this month’s SSBs, and can be considered as an alternative to T-Bills.

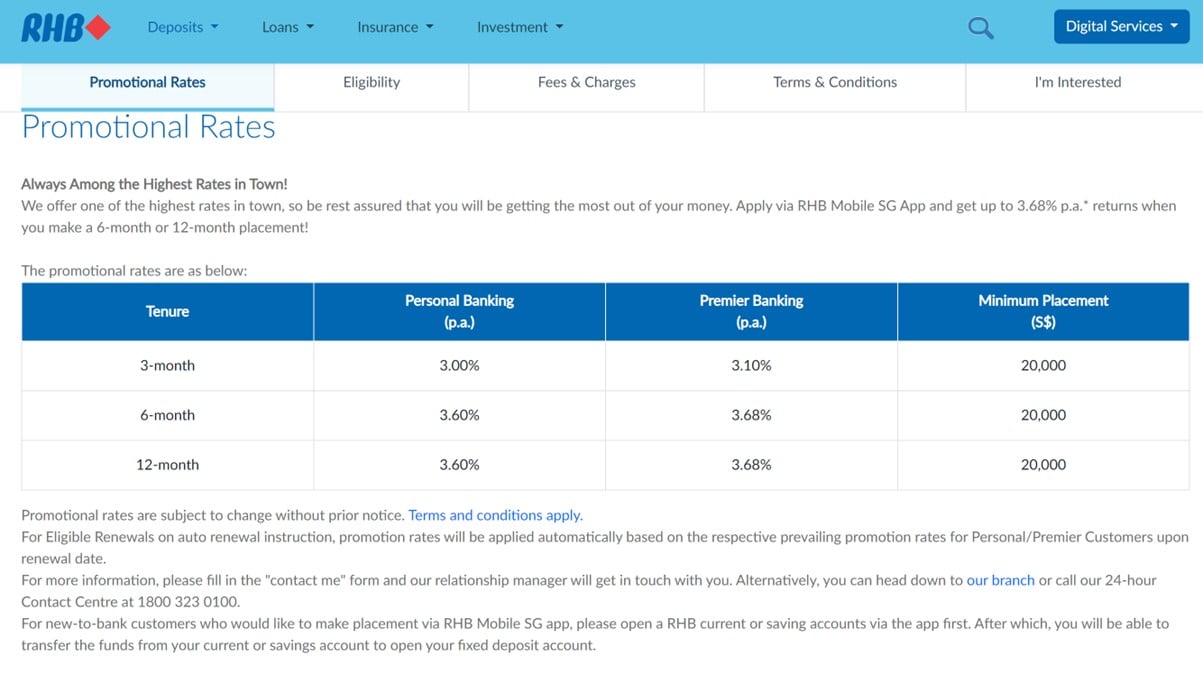

RHB Bank Fixed Deposit – 3.68%

The best Fixed Deposit option I could find today is RHB at 3.60% for 6 months.

Minimum of $20,000, that steps up to 3.68% if you are premier banking.

So if you don’t want to buy T-Bills, this is probably the next best thing.

Are T-Bills still worth buying vs Singapore Savings Bonds or Fixed Deposit?

Generally speaking I would say if you want the highest short term yield, T-Bills are better than Fixed Deposit.

But if you already have a lot of cash in short term instruments and want to lock in something for a longer duration, Singapore Savings Bonds (SSBs) are a great diversifier.

SSBs are likely to get even better next month though, so I leave it for individual investors to decide if you want to apply now and wait for the next month.

I shared further thoughts on this in yesterday’s article, so do check it out.

Where does my liquid cash go?

Given that T-Bills don’t offer good liquidity (cannot be easily sold before maturity).

I maintain a chunk of liquid cash in a mix of:

|

Instrument |

Approx Yield |

Maximum |

|

UOB One |

5% |

$100,000 |

|

Singapore Savings Bonds |

3%+ |

$200,000 |

|

MariBank Account |

2.88% – 3.5% |

$75,000 |

In the past I also tried GXS and Chocolate Finance (see my review on Chocolate Finance), but these days the bulk of spare cash goes into a mix of the 3 above.

MariBank Account (SDIC Insured, by Shopee)

I did a full review on MariBank Account recently, which is the bank by Shopee (Sea Ltd).

Long story short:

- SDIC Insured

- 2.88% yield

- Withdraw anytime, no lockup

- No minimum amount (maximum of $75,000)

It’s simple, fuss free, and SDIC insured, what’s not to like?

Am I applying for T-Bills?

I’ve been applying for almost every T-Bills auction this year (I roll whatever excess cash I have into T-Bills for the highest yield).

That said the recent REIT sell-off has been very interesting.

To the point where I might skip this T-Bills auction, and go into REITs instead.

Whatever the case, I would love to hear what you guys think.

Are you applying for the next T-Bills auction?

How are you allocating your cash these days?

WeBull Account – Get up to USD 2000 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 2000 free fractional shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The fundamentals still seem to strongly support an underlying upward trend in yields. My own gut feeling is that the 6-month Singapore T-bill yield will eventually top out around 4.25% to 4.50%, probably in Q1 or Q2 of 2024. My own strategy has been to average in and build my bond ladder. After recent events it is helping me sleep better.

Interesting. My personal view is that we are somewhat close to the top in rates here, but trying to call the exact top is not something I’ll have high confidence in. Let’s see.

Economic data is starting to come in weak – pointing towards weakness in Q4 / Q1. But of course the middle east conflict and 2024 elections are big wildcards.