For investors with cash to spare, 2022 has been like Christmas come early.

A sell-off in REITs, stocks and bonds.

And now Astrea 7, with 4.125% and 6% yields.

A ton of you have reached out to ask for my views on the Astrea 7 PE Bonds, and whether it’s worth buying.

Lots to cover today, so lets go!

What is the Astrea 7 PE Bond?

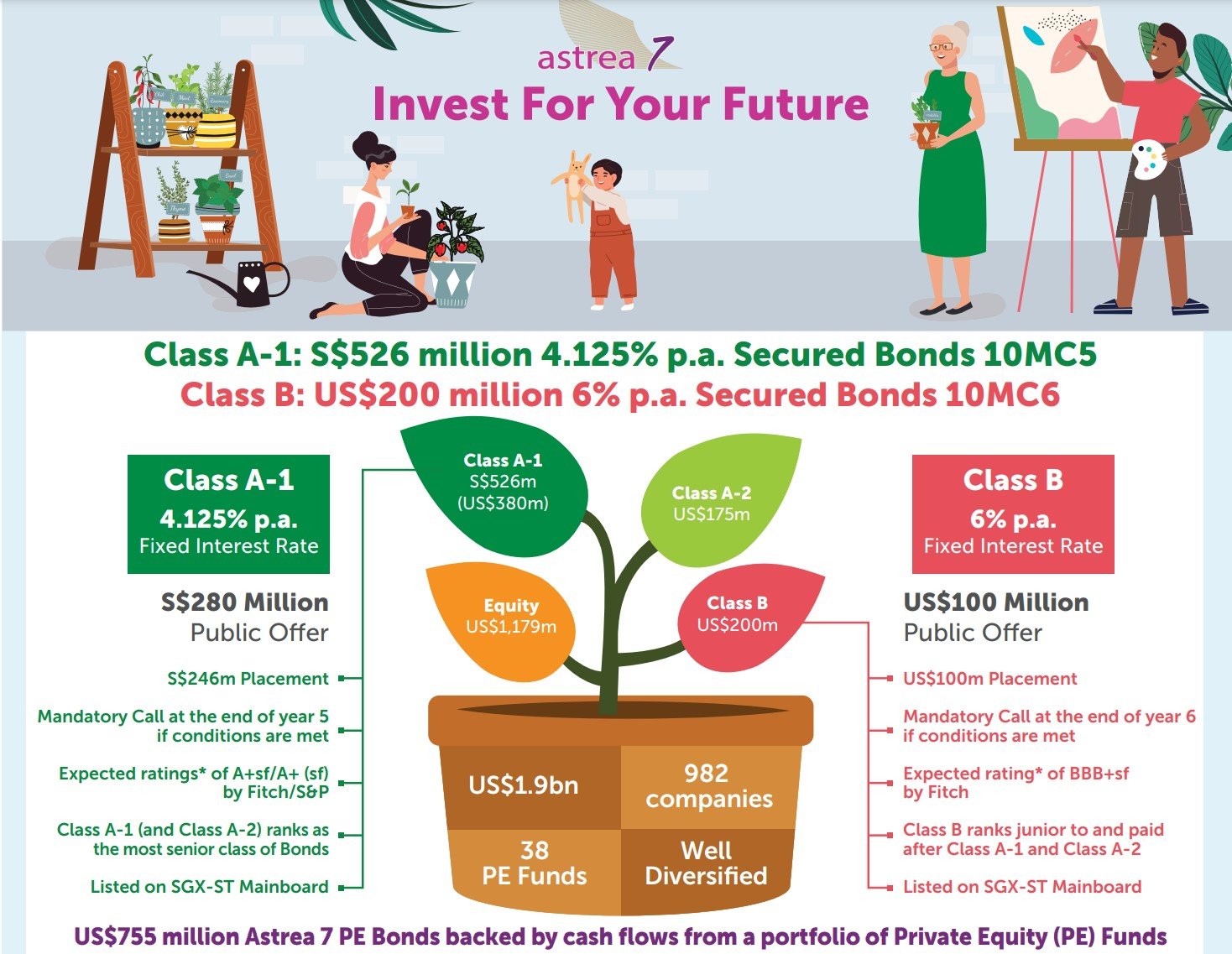

Astrea 7 PE Bond is basically a set of bonds secured by the cash flow from private equity (PE) Funds.

Think about it this way.

You take 38 different PE Funds.

You put them all together into a $1.9 billion portfolio.

And you borrow $755 million secured against this $1.9 billion portfolio.

And from the $755 million, you slice it up into Tranche A ($555 million) and Tranche B ($200 million).

Tranche A gets paid first, then Tranche B (which means Tranche A is less risky).

That’s really what the Astrea 7 bonds are.

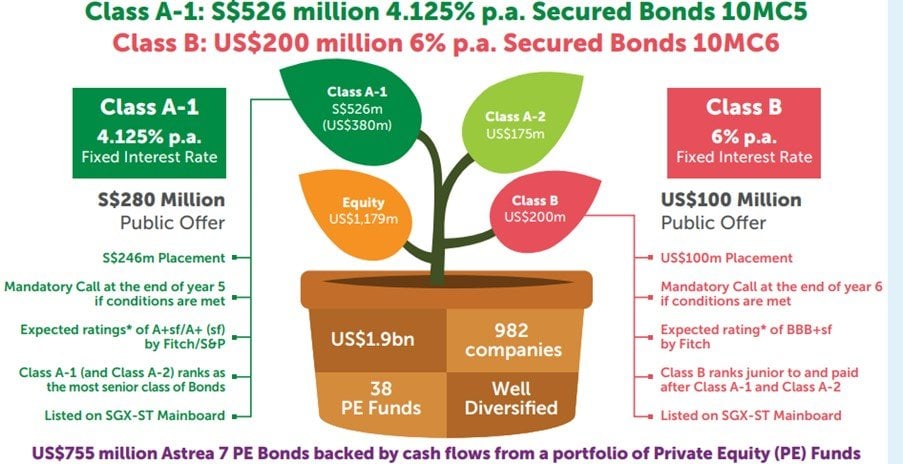

Class A-1 4.125% yield Astrea 7 Bonds

To summarise the key facts for Class A-1

- 4.125% yield

- 10 year maturity

- Mandatory call after 5 years – This means that if there is sufficient cash, the Class A-1 Bonds must be redeemed at the 5 year mark. If not, the interest rate will step up to 5.125%

- Must apply S$2,000 or higher (in multiples of S$1,000)

Class B 6% yield Astrea 7 Bonds

For the first time ever, retail investors will get access to the higher risk Class B Astrea 7 Bonds.

The main difference with Class B is the 6% yield, and the mandatory call is 6 years instead of 5 years for the Class A.

This means that if there is sufficient cash, the Class B must be redeemed at the 6 year mark (vs 5 years for Class A). If not, the interest rate will step up to 7%.

- 6% yield

- 10 year maturity

- Mandatory call after 6 years (if not called, 1% interest rate step up to 7%)

- Must apply US$2,000 or higher (in multiples of US$1,000)

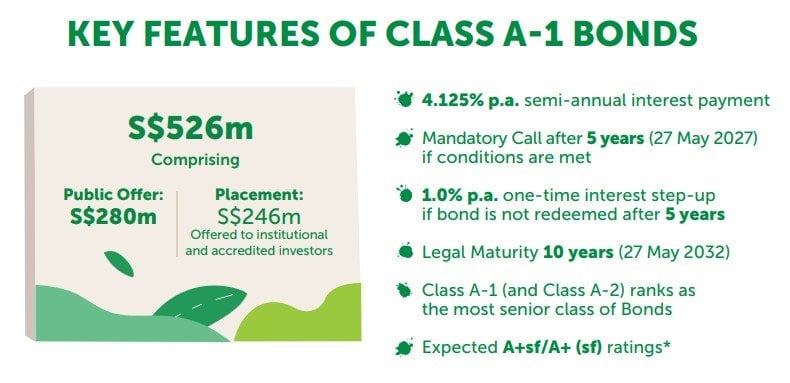

What are the safeguards in place for Astrea 7 Bonds?

The underlying structure of Astrea 7 is very similar to that of Astrea IV, V and VI.

To summarise briefly:

- Reserves Account – All cash generated (after expenses) will be paid into a Reserves Account which will then be used to repay the principal on Astrea 7. The Reserves Account for Class A will be filled up first, then Class B.

- Maximum LTV – If the gearing ratio crosses 50%, certain automatic procedures will kick in to reduce total net debt

- Credit Facility – there is a loan facility that can be drawn on in the event of emergency liquidity requirements

So FH… will Astrea 7 Bonds default?

Okay let’s cut to the chase.

Will Astrea 7 Bonds default?

Looking through the prospectus, the 3 key safeguards for Astrea 7 Bonds for me are:

- Overcollateralization

- Portfolio Vintage

- Diversification

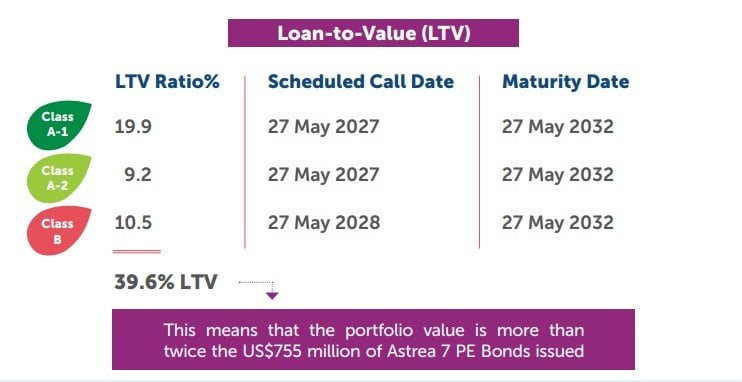

Overcollateralization for Astrea 7 Bonds

Think of it like a mortgage.

You buy a house worth $1.9 billion, and only take a $755 million loan.

This means that you paid $1145 million (60.4% of the value) in “home equity”.

Or in other words – the home can lose 60.4% of its value, and theoretically the bank is still safe because it can still sell the house to repay the debt fully.

So the loan is heavily overcollateralized, which is a very good to have if you’re the guy lending the money (which you are in this case).

But… PE Funds take on heavy leverage at the portfolio company level

The problem though, is that you’re not really buying a house.

You’re buying 38 different Private Equity Funds.

And the way private equity works is that they buy a company with a lot of debt, execute a turnaround plan, and hope to sell the company for a profit after 10 years.

Which means that at the portfolio company level, you’re probably looking at a lot more debt.

So don’t be fooled by the 39.6% LTV and think that’s the only leverage in play here.

It’s leverage, on top of leverage.

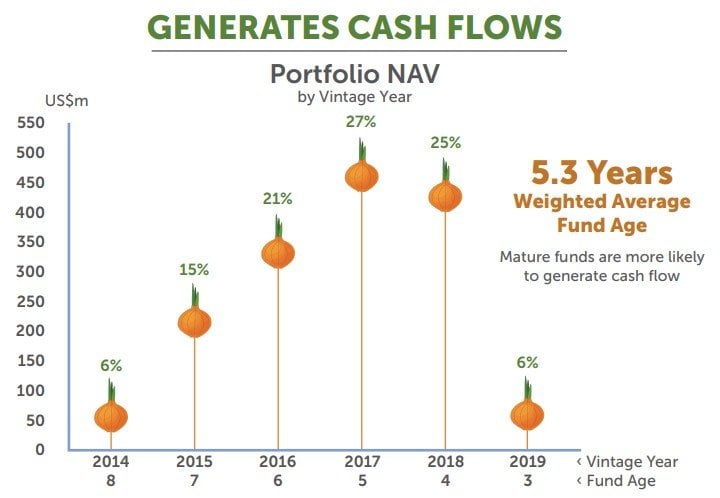

Portfolio Vintage of Astrea 7 Bonds

Which is where the next point comes in.

Portfolio Vintage is just a fancy way of saying how old the PE Funds are.

Longer is better, because the more time has passed, the more time there is for the company to stabilise its business and cash flows.

You can see the average PE Fund age is 5.3 years, which is good.

Most PE Funds are intended to wind up after 10 years, which means the bulk of the PE Funds are already halfway though their lifespan.

This is a very strong point in favour of Astrea 7.

Diversification across geography / sectors

The PE Funds are split amongst US, Europe and Asia.

And across multiple industries:

But don’t forget in a real crisis, correlation goes to 1

Of course, the counterargument is that in a real crisis, correlations go to one, and no diversification in the world is going to save you.

We saw this in March 2020, where even safe havens like Treasuries and Gold were selling off, as investors sold anything they could get their hands on to raise cash.

So yes the diversification helps of course, but don’t expect it to reduce risk to zero.

Astrea 7 Bonds are NOT CAPITAL GUARANTEED

I do want to caveat that Astrea 7 bonds are not capital guaranteed by Temasek or Azalea.

So Astrea 7 is 100% NOT RISK FREE.

If you want risk free you buy the Singapore Savings Bonds at 2.53% yield.

That’s not the question we are asking today.

The question we are asking, is whether the risk-reward for Astrea 7 is attractive, relative to the risk of default that we are taking on.

In plain English… will Astrea 7 Bonds default?

That said, I know many of you want a straight answer from me, so my personal opinion is this:

Class A-1 SGD 4.125% yield Astrea 7 Bonds

I think the risk of default of Class A-1 is low, but of course not zero.

With Class A you’re looking at 30% LTV on a very broadly diversified PE Fund portfolio.

I think that the kind of global scenario required for a PE Fund Portfolio like this to implode to the point where the Class A defaults, means that you’re already looking at a very extreme global economic event.

Think 2008, or 2020 (without Fed support).

In which case any other investment you’re making in stocks or REITs is also looking at 50%+ losses.

So personal view – Class A-1 is low risk, but definitely not zero.

If s**** hits the fan hard enough, and long enough, it can still default.

Class B USD 6% yield Astrea 7 Bonds

I wouldn’t say the same about Class B Astrea 7 though.

There’s no free lunch in this world.

With Class B’s 6% yield, I think you have to acknowledge that you are taking on real risk here.

Class B is the 30-40% tranche of the portfolio, so it is definitely more risky than Class A.

In fact I may go as far as to say you’re taking on equity level risk with Class B.

So the right comparison with Class B Astrea 7 Bonds should be something like Ascendas REIT or Mapletree Industrial Trust or Netlink Trust. These pay about a 5.5% yield at current prices.

Would Astrea 7 Class B be more attractive than that?

That’s probably the right question to be asking.

Long story short – Both Classes of Astrea 7 Bonds are NOT CAPITAL GUARANTEED, and Class B brings real risk with it.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Is the yield on Astrea 7 Bonds attractive?

I’ve compared Astrea 7’s Bond yields against the 10 year Singapore Savings Bond rate, and against the previous Astrea series below:

|

Series |

Date |

Yield |

10 year SSB at the time |

Yield spread vs 10 year SSB |

|

June 2018 |

4.35% |

2.43% |

1.92% |

|

|

June 2019 |

3.85% |

2.13% |

1.72% |

|

|

March 2021 |

3.0% |

1.15% |

1.85% |

|

|

Astrea 7 |

May 2022 |

4.125% |

2.53% |

1.595% |

Class A-1 Astrea 7 Bonds (4.125% yield)

Frankly speaking the yield is not amazing.

The 4.125% yield works out to just a 1.595% yield spread against the 10 year risk free, which is a fair bit lower than the previous Astrea bonds.

In fact the USD version of Class A-2 seems far more attractive.

Class A-2 ranks pari passu with Class A-1 in a default, but is USD denominated, pays a 5.35% yield.

With the 10 year treasury at 2.85%, that’s a 2.5% yield spread vs the risk free, which is almost an entire percentage point higher than Class A-1’s yield spread.

So if I had it my way, the tranche I want to buy is the Class A-2 USD bonds, but unfortunately it is not available to the public.

Class B Astrea 7 Bonds (6% yield)

Class B on the other hand at 6% yield is a 3.15% yield spread vs the risk free.

That’s quite a big spread, which again gives you an idea that market is pricing in real risk of default here.

Long story short – yields for Astrea 7 Bonds are not amazing, but to be fair to them it’s probably fairly priced in this market.

Liquidity will be an issue for Astrea 7 Bonds…

Astrea 7 Bonds will be freely traded on the SGX-ST.

But just take a look at the trading liquidity for the previous Astrea VI.

1 lot a day.

So don’t kid yourself on this, trading liquidity for Astrea 7 is likely to be very poor, and you may not be able to cash out quickly unless you’re prepared to sell at a discount.

Will rising interest rates result in capital loss for Astrea 7 Bonds?

Quite a few of you have expressed concerned that Astrea VI bonds trade below par.

With a rising interest rate environment, this is to be expected, especially as Astrea VI was issued at a low 3% yield.

Remember – bond prices trade inversely to yield, so when interest rates go up, bond prices go down.

Given that Astrea 7 is being issued at significantly higher yields, I *don’t expect* the same to happen to Astrea 7 unless interest rates get very extreme.

That being said, you never know how crazy Jerome Powell may get in his bid to fight inflation.

Whatever the case, you must understand that if interest rates go up significantly, Astrea 7 Bonds can trade at a loss.

In which case your options are to (1) sell into poor liquidity at a loss, or (2) hold to maturity (and hold there is no default).

Do note this point, it’s pretty important especially if you need the cash very soon, and don’t plan to hold Astrea 7 Bonds to maturity.

Will I be subscribing for the Astrea 7 PE Bonds?

As you would have guessed from the title, I will probably be subscribing for the Astrea 7 PE Bonds.

I have subscribed for every single series since Astrea IV because I think the risk-reward is attractive, and I don’t think this round is any different.

How much of Astrea 7 Bonds will I be subscribing? What Class?

What I haven’t decided though, is how much of Astrea 7 I will be subscribing, and how to split the allocation between Class A-1 and Class B.

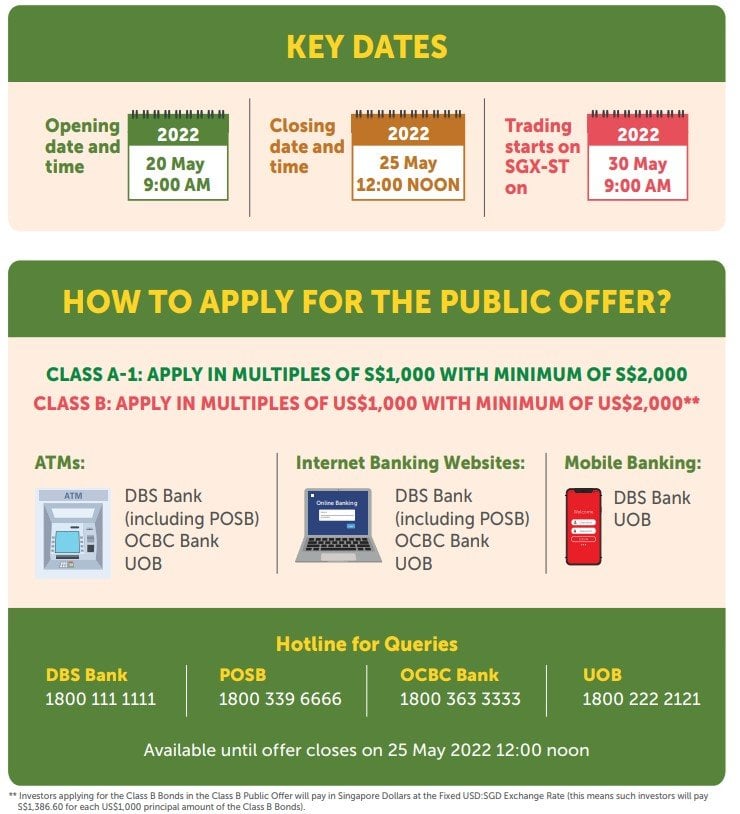

I have until 25 May to decide though, so I can mull on it the whole weekend.

In any case I’ll walk you through my preliminary thought process below, and you can let me know what you think.

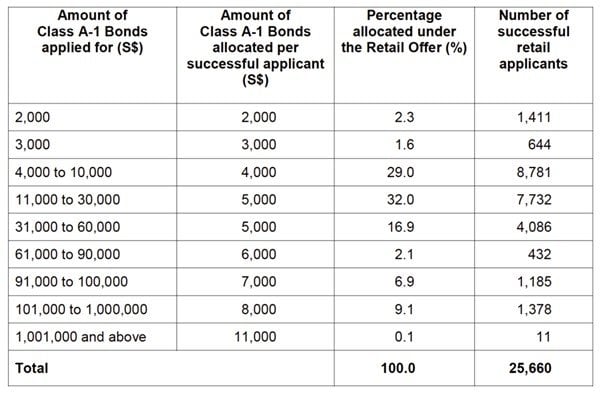

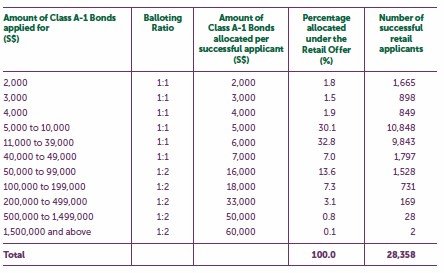

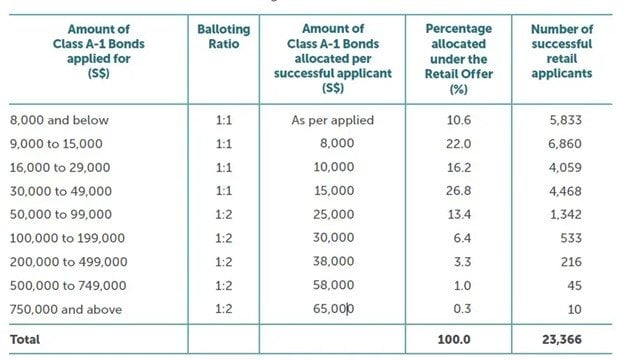

Balloting Results from past Astrea Bonds

I’ve set out the balloting results from the past Astrea Bonds below:

Astrea IV Bonds

Astrea V Bonds

Astrea VI Bonds

Astrea VI was the least popular because of the 3% yield, so we can leave it out for now.

Astrea 7 is probably going to be closer to Astrea IV and V in terms of popularity (because of the higher yield).

Looking at Astrea IV and V, the sweet spot is around $11,000, which gets you about a $5000 to $6000 allocation.

Which frankly is not very much.

Class B though has never been open to the public before, so it would be very interesting to see how the public responds. Would Class B be hotter than Class A-1? Or less?

What is the right allocation of Class A and Class B Astrea 7 Bonds?

I will probably be applying for both Class A and Class B Astrea 7 Bonds.

Off the top of my head, am thinking equal amounts each, but frankly haven’t decided.

I don’t think there’s much point applying for too much because the chances of getting a significant proportion is not high.

And in the slim chance that you get full allocation – frankly I don’t want too much of my cash tied up in Astrea 7 Bonds too, because I do want to save some dry powder to buy REITs and stocks as the year plays out. For those who are keen, you can view my full portfolio and my stock watch on the REITs/Stocks I am keen to buy on Patreon.

My risk appetite is high enough that I don’t mind having a 50-50 split for Class A and B, such that if I get allocated the same amount for both it’s about a 5% blended yield.

But investors will need to decide accordingly. If you don’t want to take on too much risk, might be best to skip the Class B Astrea 7 Bonds entirely.

I also received a bunch of great questions from readers, that I wanted to address below.

Class A-1 Astrea 7 (4.125%) – Isn’t buying REITS with 5% div a better deal? Can sell easily if you need cash too. So what’s your logic in buying Astrea 7?

I think the simple answer is that the risk associated with REITs is arguably much higher than Class A-1 Astrea.

So I don’t think it’s an apples to apples comparison here.

The more accurate comparison for Class A-1 Astrea 7 is probably an SGD denominated investment grade bond, which trades about 3-4% yield these days.

If you are looking at REITs, the better comparison would be with Class B Astrea 7 at 6% yield.

Class B Astrea 7 USD (6%) – What about USD FX Risk?

Agree that USD FX risk is a concern.

Over a 5 year horizon, there’s probably a real risk of USD depreciation against the SGD.

Of course on the flipside, if the USD strengthens you do benefit, so it’s a double edged sword.

The better question then, is does the additional yield compensate for the risk of USD depreciation?

Personally I dont mind the USD exposure, and I can hedge USD depreciation risk more holisitically via the rest of my portfolio (you can view my full portfolio on Patreon).

But really, each investor is different. Only you can answer this question for yourself.

IPO USD FX Rate

Btw sidenote that if you subscribe for the Class B at IPO stage, the USD-SGD exchange rate is fixed at 1:1.3866. This only gets triggered on the amount you get allocated, the rest will be refunded in SGD to you.

So if you apply for $50,000 and get $10,000, only $10,000 USD will be charged to you, the remaining will be refunded in SGD so you don’t incur the FX 2 ways.

USD Coupon is received in SGD

Another quirk is that if you buy the Class B Astrea 7 Bonds, unless you “opt out” from CDP, they will automatically convert the USD into SGD are prevailing market rate.

Which means you’ll receive the coupon (or interest payment) in SGD.

If you really want to get around this you need to transfer the Class B Astrea 7 Bonds into a brokerage/private bank that allows you to receive the interest in USD.

It’s a fair bit of hassle though (and will incur custody fees), so for most investors it probably wouldn’t make sense unless you’re investing really large sums and have a specific use for the USD.

How much more risky is Class B versus Class A-1?

Actually this is not an apples to apples comparison because you’re comparing Class B (USD) vs Class A-1 (SGD).

The better comparison would be Class B (USD) vs Class A-2 (SGD).

In which case the rates at 6.0% and 5.35% respectively.

Which means the market prices an additional 0.65% risk premium for the Class B, which is not really a lot.

If you look at the LTV, with Class A you’re taking on the safest 30% tranche, whereas with Class B it’s the 30-40% tranche.

So I guess what I’m trying to say is that the market is pricing in marginally higher risk for Class B, but not necessarily double the risk. If there is a GFC Part II that affects the NAV of this portfolio to the extent that Class B is affected, Class A is unlikely to be fully immune too.

And I mean frankly, I do agree with that.

PE Funds are very illiquid, there is real risk of a markdowns in the coming 12 months

Yes, agreed with this.

PE Funds are private market assets, so for now their valuations are unlikely to be affected.

But if you look at how public markets are imploding, global economy is slowing, I do agree there is a real risk that the assets are marked down in the coming 6 to 12 months.

The question then – for a portfolio as broadly diversified as this, with a 5.3 years average vintage (indicating fairly mature businesses), will it be marked down by more than 50%, to the extent where Class B Astrea 7 would be in danger of default.

Of course that’s not an easy question to answer, but that’s the risk you’re taking on here. And if you’re keen to buy Astrea 7 Bonds, you need to at least have a view on this.

How to subscribe for Astrea 7 PE Bonds?

In any case, we have until noon on Wed, 25 May to decide.

Application process is the same as any other IPO or Astrea Bonds – via the ATM, mobile banking, or internet banking for the 3 local banks (DBS, OCBC and UOB).

As always, this article is written on 21 May 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

hallmark of analysis should reflects deep thoughts and balanced perspectives, never loose your position as the pack is coming closer everyday

Haha wasn’t sure if you meant that this article lived up to / did not meet those standards. 😉

In any case – Absolutely hear you on this. Will strive to keep increasing the standard of each article I write.

Trying to understand the rationale of comparing this Astrea B (illiquid, risk and complex holdings) to REITS which is backed by assets. Wouldnt we not be backing up the truck soon for REITS?

I think both are quite different asset classes, with different pros and cons. It’s not an apples to apples comparison.

Main reason why I did the comparison in this article was because it was quite a frequent question I was getting from readers.

for the class B, if we wait for it to be avail for trade on SGX, instead of the IPO. do we buy it at USD ?

Yes, that’s exactly right.

Excellent article. You’re covered all the important points in a clear and concise manner. I’ll be sharing this with friends.

Thanks! Appreciate the kind words!

Hi FH thanks for the great post 🙂

Have never subscribed to any of the astrea bonds as I just didn’t have comfort with the “black box” structure. I.e there are high level metrics of how many companies / sector / geography. But there isn’t much information financial on the underlying companies and leverage employed by the funds. Am I thinking of it the right way and am I over estimating the risks?

Also was wondering how such PE deals are typically structure for institutions. Is the yield / risk / structure for retail compelling vs what instis get? Or is this like a “free lunch” or “national service” that temasek is doing for retail.

Hi Moomoo, thanks for the kind words – yes your way of thinking about it is correct.

It is similar to the mortgage backed securities from 2008, at a certain point you’re just making a leap of faith here.

That said, my personal view is that Astrea is *probably* leaving some money on the table here. If they really wanted to squeeze the yields, and if this were purely a commercial transaction, they might have gotten away with even lower yields, given the securitisation structure that they’re using. So my gut feel is that there is an element of “national service” here, where they are prepared to pay a slightly higher yield to throw a bone to retail investors (which is half of Class A and Class B).

Thanks FH. I felt this issue can forgo in lieu of Reits. The complex business of what Astrea does in this climate will make the B share too risky to take

And A share will he just lesser than what a reit with big local presence can give given SG stronger stability

Would you consider MIT to be such. Any more?

I think the problem is that if you really think about it – what does the world look like if the Class B with 40% LTV, on a broadly diversified PE Fund portfolio from the world top PE managers, defaults.

That’s probably an event that is worse than 2008, and equivalent to 2020 without the Feds stepping in.

In such a scenario – what are the losses on MIT going to be like? Probably 50% or more as well. So personally I dont really buy the argument that REITs like MIT is a safer play. Sure you hedge the micro level risk, but at a macro level the exposure is the same.

What about buying Astrea IV at a discount?

Sure if you get it at a discount. But at current market prices Astrea IV trades at a sub 3% yield to maturity.

Newbie to bond. Isn’t Astrea VI at current price has higher yield than the Astrea 7 4.125%?

No at current market prices Astrea IV trades at a sub 3% yield to maturity.

Oh so VI yield is not calculated by 103(3% yield)/988(current price)=4.25%?

Got it. My mistake in the calculation. Please ignore my comments.

No worries!