Update: Balloting Results are out! Check out the post here for the full results.

I loved Astrea IV. I loved it so much that when Astrea V was launched the past week, I even went down for their management presentation to hear them speak (see photo below). But is Astrea V as good as Astrea IV?

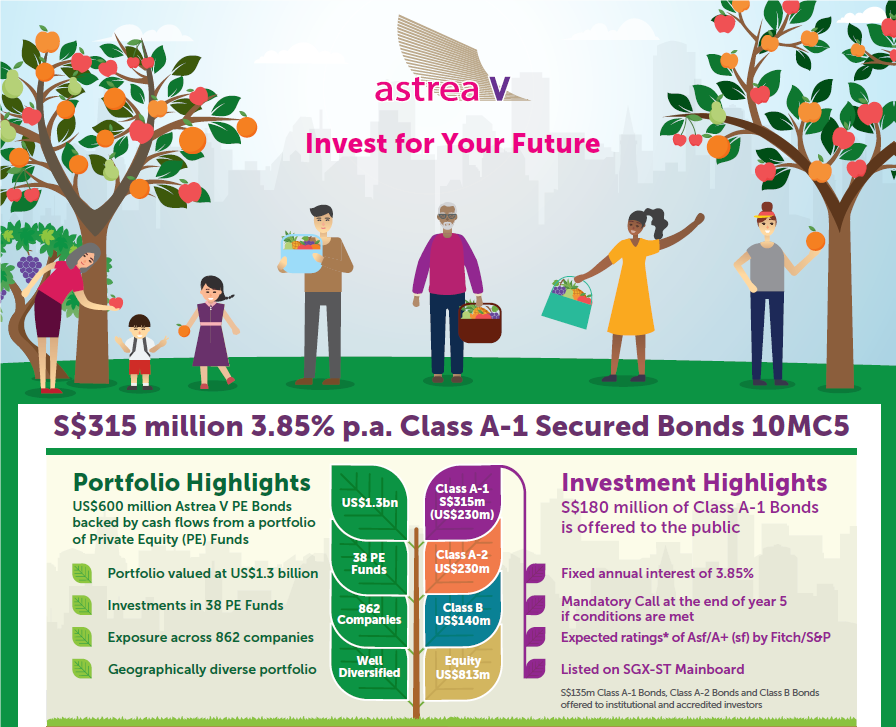

Basics: What is Astrea V?

Astrea V is a 10 year bond with a mandatory call at the 5 year mark. Think about it this way – the bond will pay you 3.85% per annum, semi annually for 5 years. At the end of 5 years, if Astrea has sufficient cash, they will redeem the bonds fully. If certain performance conditions are met, they will also pay a bonus of 0.5% on redemption. If there is insufficient cash after 5 years, the interest steps up to 4.85%, and they will redeem the bonds as soon as they have enough cash, even before the 10 year mark.

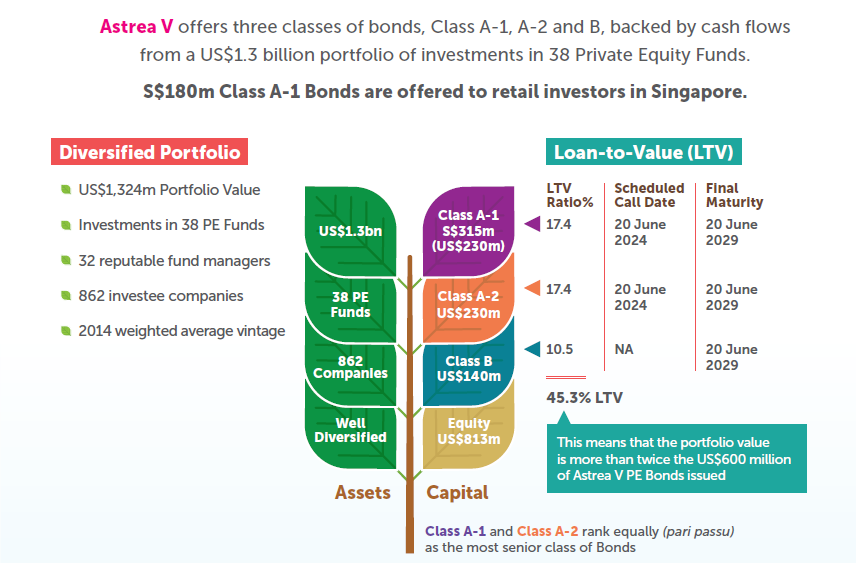

Astrea V is a structured finance product, backed by the cash flows from 38 underlying private equity funds.

To illustrate how this works very simply, imagine that Astrea owns 38 “houses” that is worth US$1.3 billion. It wants to borrow US$600 million. Within this US$600 million, it splits the borrowings into a Class A loan for US$460 million and a Class B loan for US$140 million. Bank A agrees to provide the Class A loan, secured with a mortgage over the 38 houses. Bank B provides the Class B loan. Because Bank A will get paid ahead of Bank B in an insolvency, Bank A’s investment is safer, and it receives a lower interest rate for its efforts. In this scenario, retail investors are the Bank A, and we get a chance to loan Astrea money if we wish.

It’s a bit of a simplistic explanation, but swap the “house” out for PE Funds, and you get the rough idea of how these bonds work.

Possibility of Default

To understand the risk of default of Astrea, we need to look at (1) the structural safeguards in place, and (2) the quality of the underlying assets.

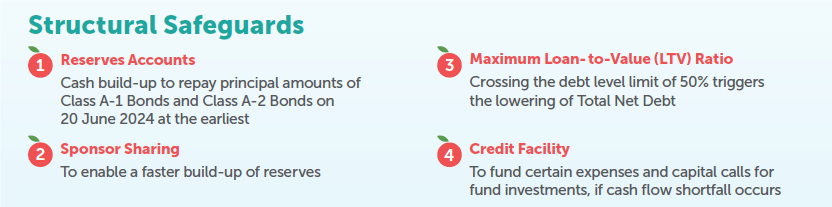

(1) Structural Safeguards

Astrea V has 4 main structural safeguards in place to prevent default. These are very similar to Astrea IV, but I’ll summarise them briefly.

Reserves Account

Back to the house example, imagine that the bank now requires that all rental income from the houses, or all proceeds from the sale of the houses, needs to be paid in a specific order.

That’s basically what this is. Astrea is required to pay all moneys in the following priority:

- Key expenses

- Interest on the bonds

- Into a reserve account every 6 months at a fixed rate, that will be used to redeem the bonds after 5 years.

- Remaining expenses

Only after these payments are made, will the “owner” of the houses (effectively Temasek, via the Sponsor Azalea), be entitled to receive any moneys from the equity tranche.

Sponsor Sharing

Any amount that is paid to the Sponsor in the equity tranche will also be split 50-50, with 50% of it going into the Reserves Account, which is then used to redeem the Class A-1 bonds after 5 years.

Maximum LTV Ratio

Astrea has a max LTV Ratio of 50%. Once the gearing of Astrea crosses 50%, this clause will kick in, and the Sponsor will not be entitled to any cashflows until the Reserve Account has been topped up to the amount to redeem the Class A-1 bonds.

Credit Facility

The credit facility is pretty interesting, and I’ve extracted the prospectus disclosure below:

In the event of cash flow shortfalls, the facility provided by DBS Bank Ltd. and Standard Chartered Bank to the Issuer can be used to fund certain expenses and other amounts payable (including unpaid accrued interest on the Class A-1 Bonds, the Class A-2 Bonds and the Class B Bonds) and Capital Calls.

However, to avoid any doubt, the Credit Facility cannot be used to repay any principal amount on the Bonds.

Essentially, DBS and Standard Chartered Bank have come together to give Astrea a loan, that can be drawn on at any time to provide emergency liquidity. This can be used to pay expenses, and interest on the bonds, but it cannot be used to redeem the bonds themselves.

The other interesting thing, is that the amount of the credit facility at launch, as a proportion of its total asset size is 15.4%, lower than Astrea IV’s 21.2%.

You can overread this and say that this means Astrea V has a higher default risk, but frankly speaking, because this loan can only be used for working expenses and not to redeem the bonds, I wouldn’t read too much into it. The US$200 million liquidity at launch is more than enough to cover any working expenses that may be required in the interim.

At the end of the day, the security of these bonds is tied to the underlying cash flows from the 38 PE Funds, and all this credit facility does is ensure that Astrea doesn’t go bust from liquidity issues before the underlying cash flows mature and kick in.

Ratings agency Fitch reached a similar conclusion, which said that the credit facility size is sufficient for its projected use and in line with other Fitch-rated PE CFOs. Under the rating agency’s most severe stress scenario, the maximum utilization of the facility was just USD96m, or about 41% of its total capacity.

Hedging

Because the underlying PE funds are heavily exposed to US and Europe, Astrea also hedges the Euro and USD against the SGD, to minimise currency risk.

(2) Underlying Assets

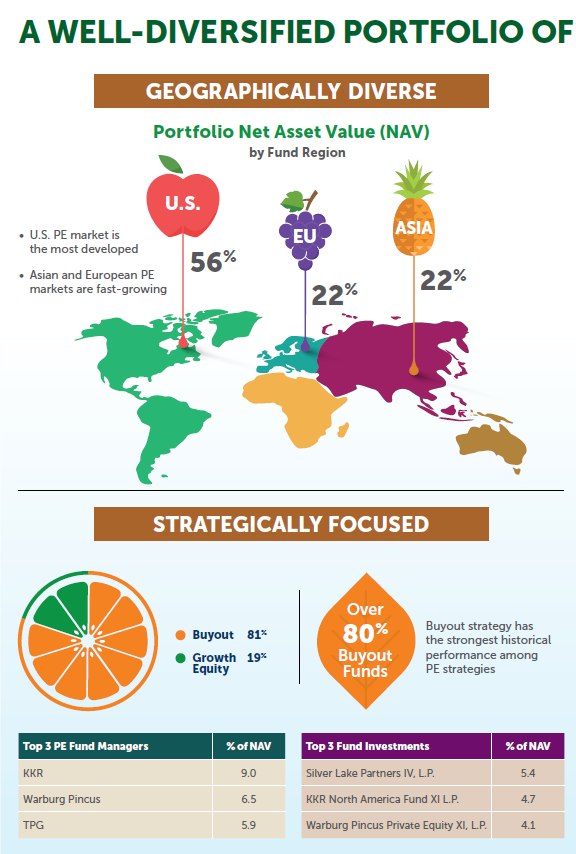

The underlying assets are 38 Private Equity Funds, with a total asset value of US1.3 billion.

They’re generally quite diversified across US, EU and Asia, with a heavy focus on buyout funds, but with no concentration in any one single fund manager or fund. So that’s good.

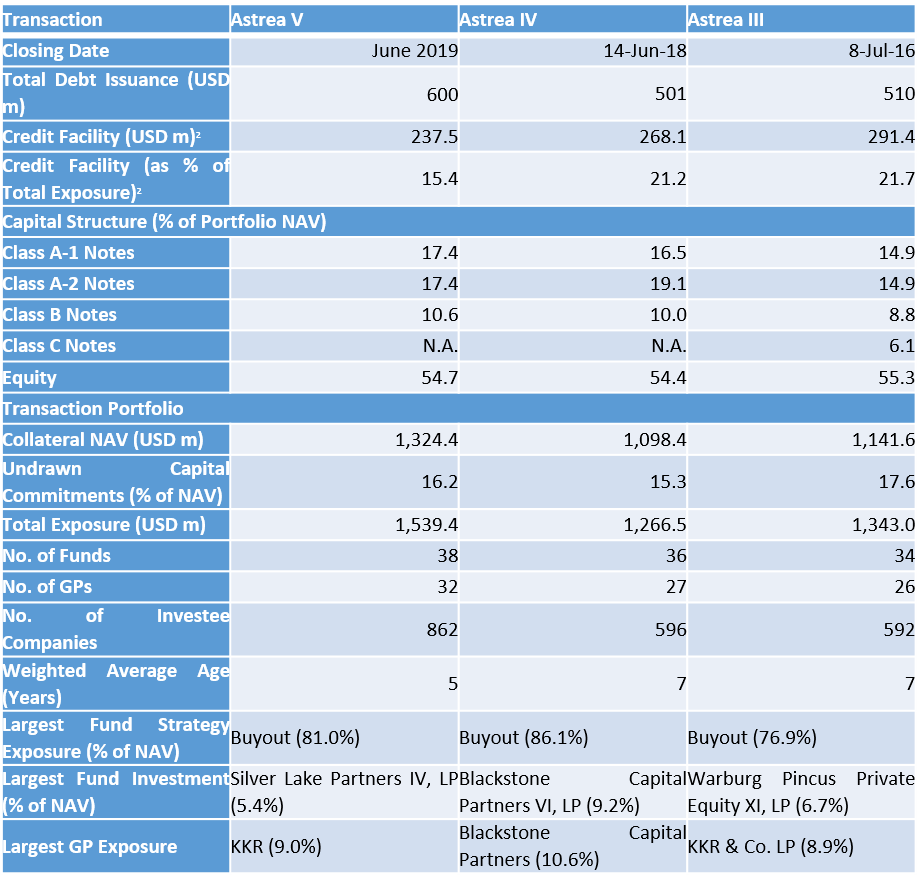

Bond Supermart has a great table below that compares Astrea V with Astrea IV and Astrea III. The thing that immediately jumps out, is that the average vintage of the funds used by Astrea V is younger than that of Astrea IV and Astrea III.Private Equity has this fancy J-Curve concept which really just means that in the early years of a PE fund, it’s cash flow negative, and in the later years, it becomes cash flow positive. Because of this, by packing Astrea V with younger dated funds, there is slightly higher chance the underlying funds don’t generate cash in time, which results in an inability to redeem the bonds after 5 years.

Couple this with how late we are in the credit cycle, how poorly the recent IPOs did for tech unicorns (IPOs are a key bellweather because they are the main exit strategy for PE Funds, and a poor IPO climate affects sentiment for private M&A), and we have a far more cautious macro environment, that could potentially impact the ability of these PE Funds to exit their investments in the near future. Because of this, I think we actually have a small argument that Astrea V may be slightly riskier than Astrea IV.

Hey Financial Horse, I just want to know if this is the next Hyflux

To be very clear, I am not saying that these bonds will default. The strength of these bonds come from the structural safeguards, and the diversification in place. When you take a $1.3 billion dollar portfolio and borrow $260 million, just about everything has to go wrong before there is a default of the most senior tranche retail investors are buying.

Don’t forget that during the 2008 sub-prime when mortgages were defaulting left and right, the top tier of the mortgages, those lawyers and bankers who owned houses, were still diligently paying their mortgages, and those CDOs never defaulted.

Don’t forget also that Astrea I was conceptualised in 2006 and went through the 2008 Financial Crisis unharmed.

So the way I see it, even if something does go wrong with the global economy the next few years, the most senior Class A-1 tranche that retail investors are holding, are still incredibly unlikely to default. I wouldn’t say the same about the Class B tranche though.

But my gut feel tells me that the chance of non-redemption after 5 years is slightly higher than it was for Astrea IV, because of the younger dated PE Funds, and the macro climate.

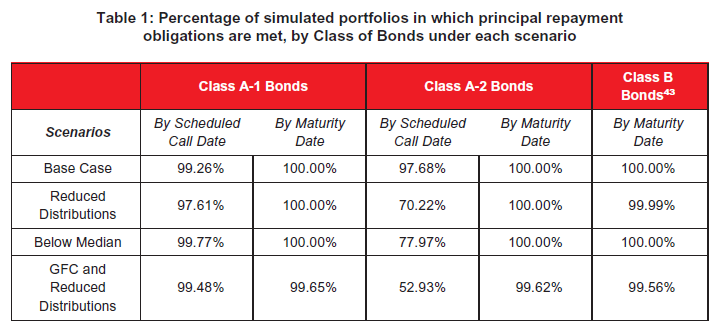

For the record, the independent research consultant also modelled the chances of default on these bonds.

It generally backs up what I just said, where the below median scenario for Astrea V has a 0.33% chance of failure to redeem by 5 years, slightly higher than Astrea IV’s 0.01% chance of failure.

But when you zoom out and look at the probability of default after 10 years, it’s still 0% chance in the below median scenario.

I actually really agree with this analysis – The chance of Astrea V not being redeemed after 5 years is higher than in Astrea IV’s case, because of the younger dated funds and the macro climate. But after 10 years, the chance of default for either of them, is as close to zero as it gets.

Astrea V

Astrea IV

Yield

This was what I wrote for Astrea IV last year:

“For reference only, the yield on a 10 year SSBs for June 2018 yield 2.63%. SSBs are a risk free investment, so the risk premium for these bonds is about 172 bps. A blue-chip REIT such as Mapletree Commercial Trust is yielding about 5.6%, but the risk of capital loss for a REIT is far higher.”

Fast forward 1 year, the 10 year SSB now yields 2.16%, and MCT yields 4.53%. So Astrea V’s 3.85% yield works out to a 169 bps yield spread against the risk free rate, and about 68 bps less than a REIT.

My take on this? Man, I wish the yield were higher…

I know the corporate spiel on how the global yield environment has deteriorated significantly since 2018 etc etc, but man, I really wish it were 4.35% instead of 3.85%. It’s hard to fault Astrea on this one though, because if you look at the yield spread against the 10 year SSB, it’s really the same premium it was back in 2018.

And for the record, Astrea IV that trades on the open market now? It yields a ridiculous 3.56% to maturity. So yeah, this is still better than Astrea IV on the open market.

Liquidity

This is what I wrote on Astrea IV:

The Astrea IV bonds will be listed on the SGX-ST post listing, so technically you can sell them on the SGX. However, my suspicion is that the trading volumes will be quite thin, and the bid-ask spreads are going to be quite high. This means that you cannot exit your investment easily without taking a loss (I could be wrong though).

That said, you probably shouldn’t buy this bond unless you are prepared to hold it to maturity. These are not equity instruments that are designed to be traded.

All that continues to hold true for Astrea V.

As it turns out, liquidity for Astrea IV is indeed a joke, with trading volume around 45 lots a day last I checked. So yes, don’t count on you being able to buy or sell these things on the open market without a large bid-ask spread. If you buy this, you should seriously plan to hold them until maturity in 5 years or more.

How much to apply for

Astrea IV allocated the bonds similar to how SSBs are allocated. In other words, everyone gets something, but everyone gets a little bit only. It’s quite a socialist way of doing things now that I think about it. It also led to ridiculous situations where guys who applied for 1 million only got an S$8000 allocation.

The key difference with Astrea V, is that if you apply for S$50,000 or more, there will be a balloting process to determine if you get any. The rationale for this is that if you actually win the ballot, at least you get a meaningful allocation, instead of a paltry S$8,000. What this also means, is that the chances of winning the ballot, are actually going to be low.

So if you’re a high roller and you wouldn’t know what to do with S$5000 worth of Astrea V Bonds, you should probably apply for S$50,000 or more.

If you’re a mere mortal like me, stick with below S$50,000, so that at least we get something, instead of being subject to the mercy of the ballot.

I’ve extracted Astrea IV’s balloting table below. Based off this, the sweet spot to apply for would have been S$11,000, as that got you S$5,000 worth of bonds. Unfortunately, this balloting table is unique to Astrea IV, and Astrea V’s allocation will depend on the bookbuild process, which we’ll only know once applications close. So yeah, the balloting table below isn’t all that helpful.

One thing to note though, is that the public tranche is slightly bigger this time, with S$180 million against Astrea IV’s $121 million. Coupled with the lower interest rate, perhaps less people are going to apply this time round, leading to better allocations for the rest of us? Either that or people are attracted by the success of Astrea IV, and they’re coming out in force this time round.

It’s hard to say what’s going to happen.

Closing Thoughts: Am I buying Astrea V?

To be honest, I like Astrea IV a lot more than I like Astrea V. But then again, I also wish I could go back to 2018 and buy more REITs.

There’s no denying that the global yield environment has come down significantly since June 2018, which is why the yield on these bonds have come down so significantly. Logically, I understand all those arguments, but deep down, the investor in me still wishes for a higher yield.

Credit to Azalea (the sponsor), I think this product retains a lot of the structural safeguards that made Astrea IV so safe to begin with. But with the slightly younger PE Funds, and the global macro where it is, I think the chances of a non-redemption after 5 years are slightly higher than Astrea IV. That said, the chance of a default after 10 years is still incredibly low.

Am I subscribing for Astrea V? Yeah, I probably will, because I quite like them as a diversifier to my current portfolio, and given the yield environment, they’re still really decent. Worst case if they don’t get redeemed after 5 years, I don’t need the liquidity, and 4.85% a year is pretty good as well.

I’ve giving this a 4 Financial Horse rating, to reflect that it’s not as great as Astrea IV, but objectively, still a very sound product.

Will you guys be applying as well? Do you like this as much as you did Astrea IV? Share your thoughts in the comments section below! I respond personally to all comments!

Financial Horse Rating – Astrea V Class A-1 Bonds

Financial Horse Rating Scale

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

[…] repeat the good work done by other bloggers: You can read Financial Horse’ piece of Astrea V here. You can also read about Bondsupermart research on Astrea V here. In addition, the Issuer has […]

There is a potential issue however: usually the issuer would like to satisfy everyone who applies, it ends up each subscriber getting a very small tranche of it, the selling commission becomes relatively a larger part.

Yes correct. I was invited for the placement tranche. Even for that, the allocation is quite pathetic in my opinion (only).

Yeah, agreed on this.

Thank you for the well written article. It summarizes everything I would like to know about Astrea V. I am new to Astrea and don’t have the knowledge to judge if it is a good buy. The prospectus is too technical and lacks relevance. You made it so much easier to understand. Keep it up!

Having enjoyed a decent 4.35% from Astrea IV, (oh yes just receive the second tranche of $108 in my Account), I am ruefully saddened to have only 3.85% this time for Astrea V that I’m hesitating to apply until I read your current comparison of SSB(2.16%) and MCT(4.35%). The horizon outlook for the next few years are not bright, meaning; the rates are likely to go lower further that I decide to hedge in at this dismal 3.85% for five years.

Haha, yeah I think it’s really about alternatives at this time. With SSBs yielding 2.16%, I don’t mind putting some money in here for the higher yield, in the event that we’re stuck in a low yield environment for an extended period, given how safe these are if held to maturity. Worst case if the market crashes, we’ll *probably* be able to exit these bonds to rotate into stocks.

I am a middle-aged retiree and I am new to this Astrea Bond and I also had never bought bonds from the open market before.

By the way, If I were to buy the Astrea IV 4.35% Bond from the open market at $1.07 and hold the bonds till year 2023 June, can someone calculate for me and tell what is the yield that I am getting if I buy the bonds at $1.07?

Hi! Welcome to Financial Horse!

At current prices, Astrea IV yields about 3.5% when held to maturity. Viewed in this light, Astrea V at 3.85% is pretty attractive.

Cheers.

Hi financial horse, could you share the calculation of the yield at 3.5%? Using 43.5/1070, the yield is 4.06%.

Hi Financial Horse, will you be able to share how you calculate the yield of 3.5% for Astrea IV bonds with the current price of 1.07? I calculated using $43.5 coupon for every 1000 shares. The yield is 43.5/1070 = 4.06%. Thank you.

I cheated I just used the yield to maturity numbers from the bondsupermart website haha:

https://www.bondsupermart.com/bsm/bond-factsheet/SGXF92571078

They’re usually fairly accurate, and it saves a lot of time.

Hi Financial Horse

What are your views of Astrea V in light of the covid 19 crisis? I hold a substantial amount and concerned about the possibility of a default

I can’t advise for your financial situation of course. If you’re worried do consult a financial advisor to decide on next steps.

With Astrea, the underlying securities are a bit of a black box, so it’s really hard to comment constructively. That said, the securitisation structure lends a lot of security to the instrument. So even in 2008 the highest tier of mortgages never defaulted.

For now I remain sanguine on Astrea (I’m holding on to mine – but I only have a small amount), subject to any material change in global macro.