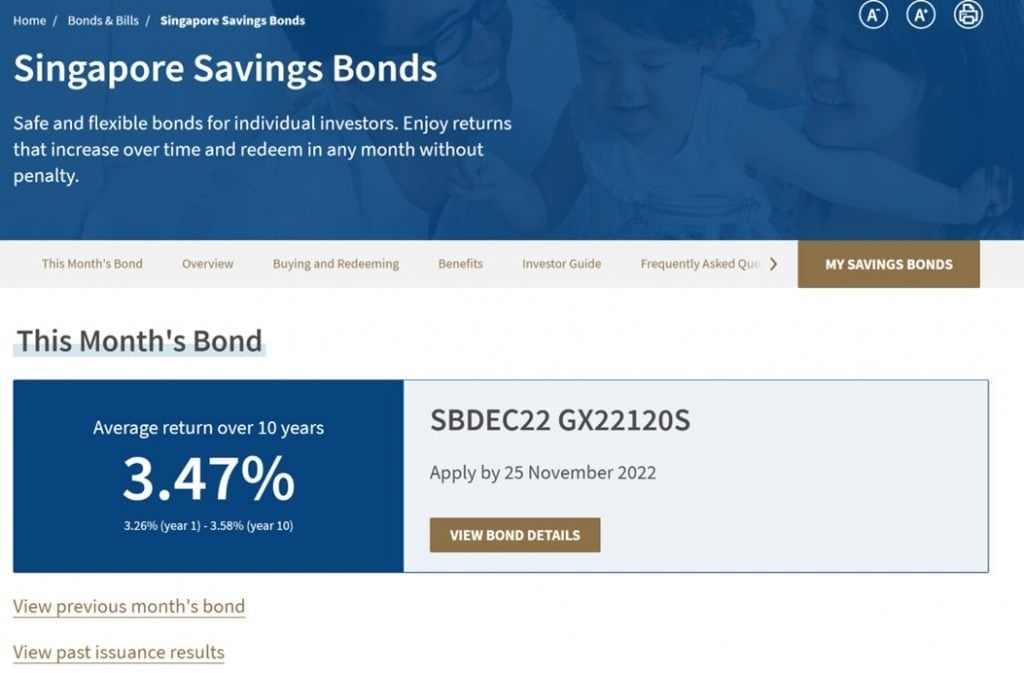

The latest Singapore Savings Bonds are out.

As expected – they are very attractive.

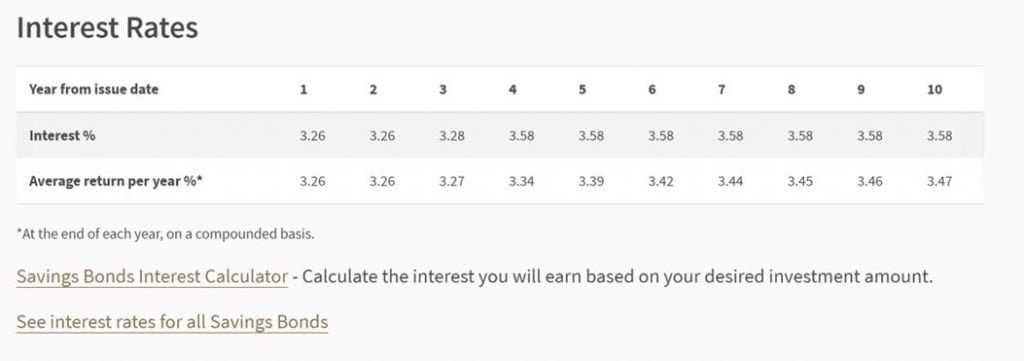

Starting at 3.26% in the first year, and going up to 3.58% in the tenth year.

For an average return of 3.47% if held over 10 years.

This is probably the most attractive Singapore Savings Bond in the history of Singapore Savings Bonds.

And they’re only going to get more attractive going forward.

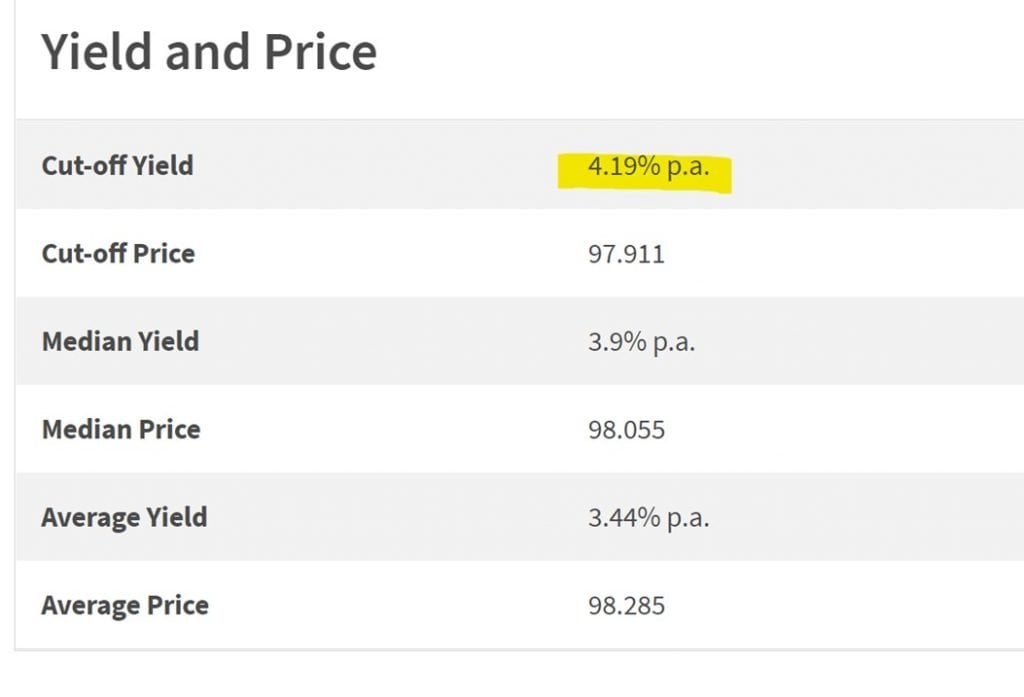

The only reason why they’re not even more popular, is because we are living in a time where you can get 4.19% yield risk free on T-Bills, and 3.9% on Fixed Deposit.

Man… it’s like Christmas come early.

Basics: Singapore Savings Bonds at 3.58% yield

To recap the key features of Singapore Savings Bonds, they are:

- Risk Free – Backed by the Singapore Government

- Can be redeemed any time with accrued interest – you get your money back the start of the following month

- Can be held up to 10 years, and interest rate changes each year:

But… $10,000 allotment is dismal…

Unfortunately, Singapore Savings Bonds are popular, and the whole market wants a slice of the action.

For the November Singapore Savings Bonds – Each person who applied has a chance of getting allotted either $10,500 or $10,000, with a 29.15% chance of getting $10,500.

That’s dismal.

At $10,000 it would take 20 months just to fill up the full $200,000 allocation per person, by which time the Feds are probably already cutting interest rates.

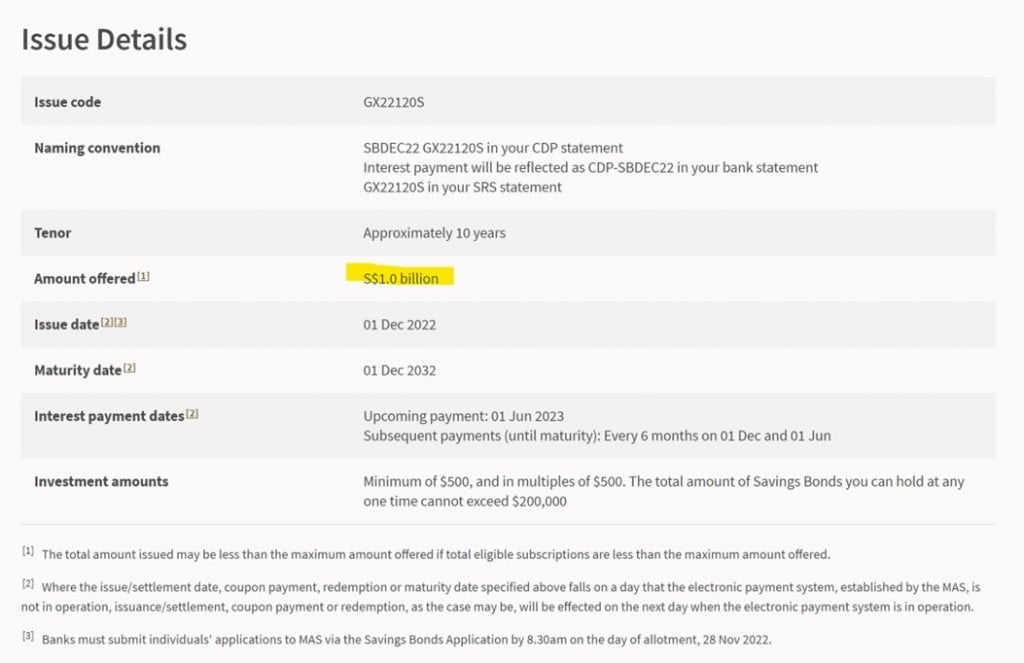

Issue size for Singapore Savings Bonds upped to S$1.0 billion

Interestingly, the issue size for the latest Singapore Savings Bonds is upped to S$1.0 billion (vs $900 million for last month’s).

That said, given the yields are a fair bit more attractive this time around (3.47% vs 3.21%), I frankly doubt if this will increase allotment level by much.

2 Big Questions on Singapore Savings Bonds

The 2 big questions I’ve been getting on Singapore Savings Bonds are:

- Should you buy Singapore Savings Bonds now or wait for higher interest rates?

- Should you buy T-Bills (4.19%) or Fixed Deposit (3.9%) instead of Singapore Savings Bonds?

Let’s discuss each.

Should you buy Singapore Savings Bonds now or wait for higher interest rates?

Jerome Powell’s press conference this week was a much watch for serious investors.

I did a piece for Patreons this week to share my thoughts, but the long and short can be summarised as Higher Interest Rates for longer.

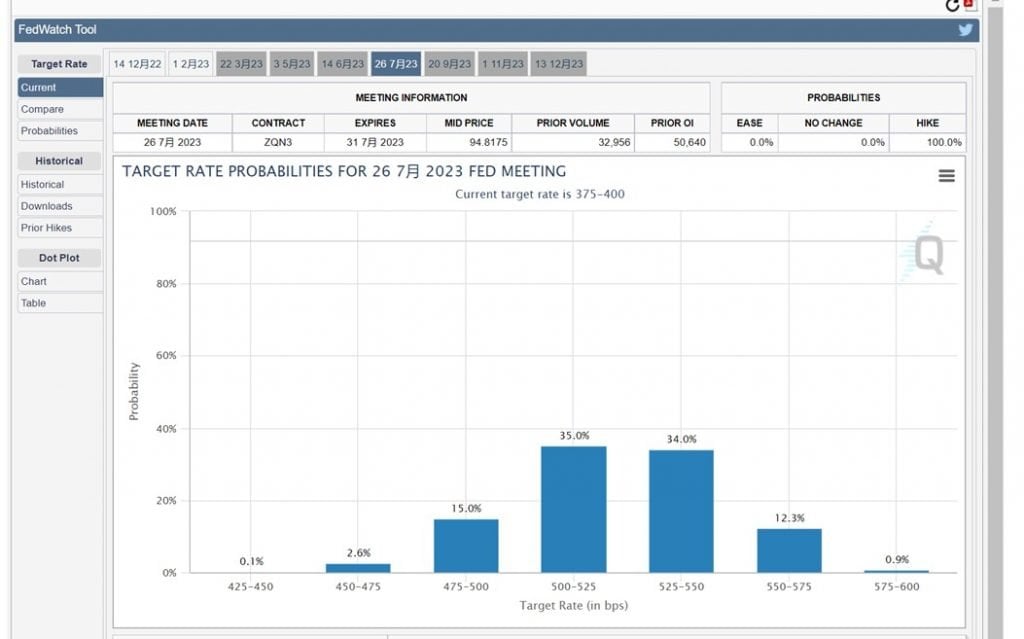

With this, the market is now looking at a terminal rate of 5 – 5.5% on the Fed Funds Rate:

I think realistically you’re looking at a peak 10 Year Treasury yield of around 4.5% (plus or minus 0.25%).

Working backwards we may see a peak 10 Year SGS yield of around 4.0% (plus or minus 0.25%).

In other words – a peak 10 year SGS yield of 3.75% – 4.25% is probably my base case this cycle.

Interest Rates for the Singapore Savings Bonds track the 10 year SGS quite closely, so we may see 10 year Singapore Savings Bonds peak at 3.75% – 4.25% this cycle.

At 3.47%, we’re getting pretty close to the end-game.

Short term instruments should yield higher (eg. T-Bills)

Now do note the discussion above is for 10 year interest rates.

Short term interest rates are significantly more volatile, and much more prone to overshoot.

That’s why you see so much excitement around T-Bills, because you can get higher and more flashy yields with short term instruments.

Assuming peak 5 – 5.5% Fed Funds Rate, my base case for the 6 month T-Bills is a peak of 4.5% – 5.0%.

With the latest T-Bills at 4.19%, we’re getting close.

We are approaching the interest rate end game? Rates bear market is over…

So for all those waiting for interest rates to go higher.

Your time has come.

Sure, I doubt if this is cycle peak for interest rates, and they probably continue to trend higher from here.

But I think the bulk of the interest rates increase is probably behind us.

As Powell put it this week, the question going forward is less about the pace of the rate hikes. And more about how high interest rates need to go (terminal rate), and how long they need to stay high?

So for fixed income investors who want to lock in the higher risk-free yields (via Singapore Savings Bonds or T-Bills etc), I think it would make sense to start doing so at these kind of yields.

BUT – not the start of a new bull market

BUT and this is important.

The end of the rates bear market, does not mean the start of a new bull market.

What I’m trying to say, is that while interest rates will not go up as quickly going forward, it doesn’t mean interest rates are going to drop just yet. They may stay high for a while.

So it’s a good time to buy stuff like Singapore Savings Bonds, T-Bills, or Fixed Deposit that you plan to hold to maturity for the higher yields.

But if you plan to trade bonds – for eg. To buy 10 year Treasuries or SGS for capital gains when interest rates go down, I don’t think we are there yet.

So FH… Should I buy Singapore Savings Bonds now or wait for higher interest rates?

Long story short – I think cycle peak for Singapore Savings Bonds is 3.75% – 4.25%, give or take.

At 3.47% we’re getting close, but not exactly there yet.

So yes, if you really wanted to wait for peak interest rates maybe you wait a few more months for higher rates.

But your bigger consideration might be allotment, as $10,000 a month is just dismal.

All things considered though, I think it’s a good time to be buying.

I’ve been buying Singapore Savings Bonds regularly for the past few months, and I will continue to do so going forward.

Remember – these Singapore Savings Bonds are backed by the Singapore Government (risk free), and can be redeemed any time with accrued interest (money comes back the 1st of the following month). And can be held for up to 10 years.

That’s as good as it gets in my books.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Should you buy T-Bills (4.19%) or Fixed Deposit (3.9%) instead of Singapore Savings Bonds?

Now probably the more tricky question.

Of the 3, which is the better buy:

- Singapore Savings Bonds at 3.47%

- T-Bills at 4.19%

- Fixed Deposit at 3.9%

Let’s talk briefly about each.

T-Bills yield 4.19% risk free (backed by Singapore Government)

The main advantage of the T-Bills is much higher interest rates.

The latest T-Bill auction saw 4.19% p.a. yields (6 month T-Bills), which is a fair bit higher than the 3.26% p.a. for the latest Singapore Savings Bonds (first year).

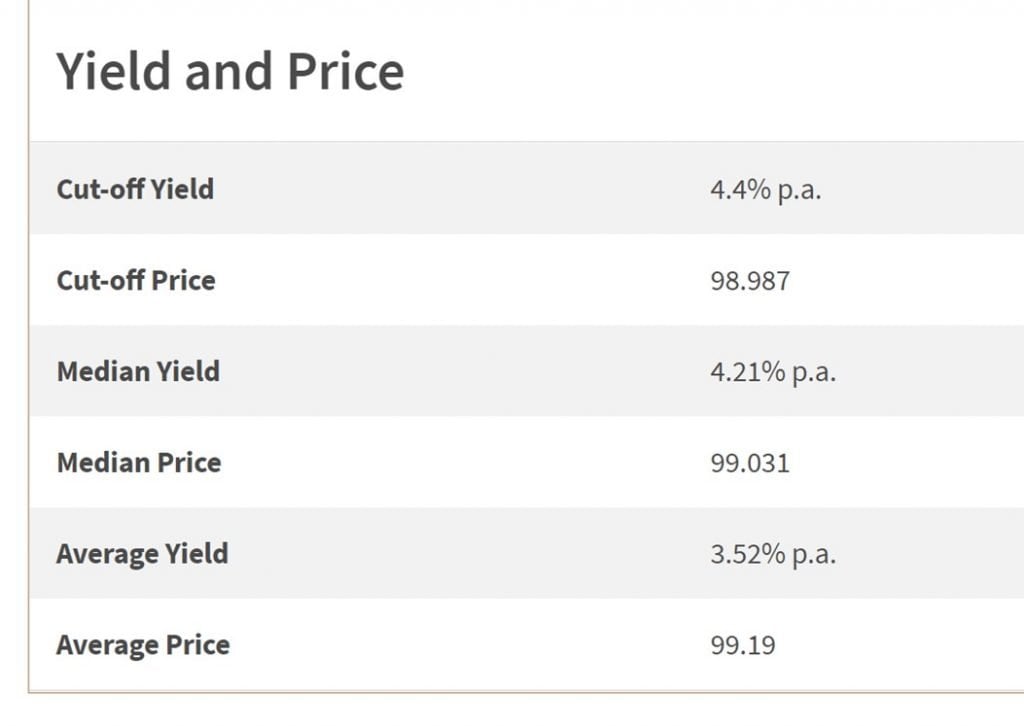

And if you look at the latest 12 Week MAS Bills, the auction closed at 4.4%.

Which means you’re probably looking at 4.2% – 4.3% yields on T-Bills for the next auction.

With T-Bills there are also no allotment limits.

So if you wanted to pop a couple hundred thousand away risk free, you can do that via T-Bills, but not via Singapore Savings Bonds.

For the record – technically there is a $1 million limit per auction for retail investors, but there are ways around this if you’re slinging around that kind of cash.

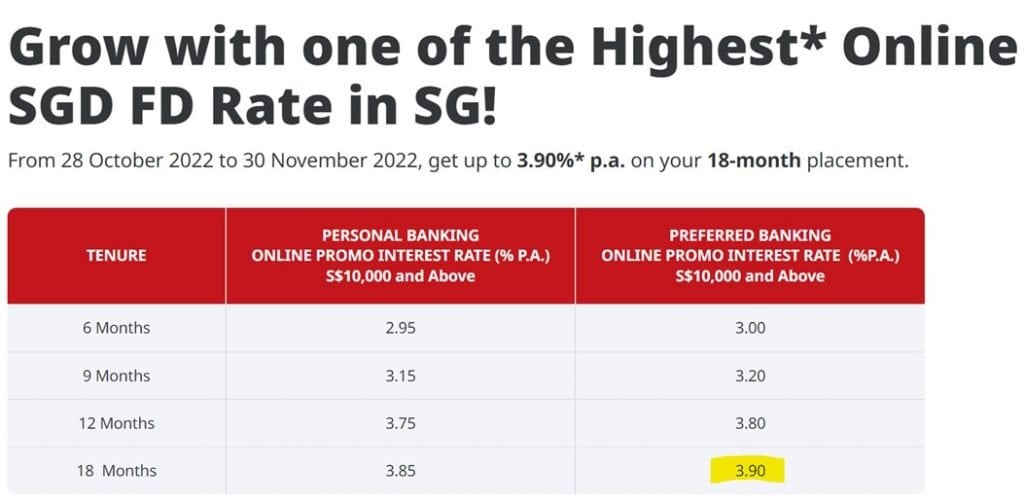

Fixed Deposit pays up to 3.9% (SDIC Insured)

I plan to do an updated article to round up the latest Fixed Deposit rates in Singapore.

But for now – you can get 3.9% for an 18 months tenure with CIMB.

Don’t forget that bank deposits are SDIC insured, so anything up to $75,000 is risk free.

Man… it’s like Christmas come early for investors who want to squirrel away their cash.

Which to Buy – Singapore Savings Bonds vs T-Bills vs Fixed Deposit?

What I would say, is that it doesn’t need to be mutually exclusive.

It doesn’t have to be one or the other.

The way I see it – The advantage of T-Bills is allowing you to benefit from the high short term interest rates, at the expense of liquidity (hard to exit before maturity).

The advantage of Singapore Savings Bonds is allowing you to lock in higher interest rates for up to 10 years (in case they are cut in future), with the added benefit of easy liquidity (can redeem any time). But interest rates are slightly lower than T-Bills.

The advantage of Fixed deposit is high short term interest rates (but not as high as T-Bills), with the possibility of getting your money back before maturity (with a small penalty).

So… each instrument has their own benefits and drawbacks, and it’s really up to each investor to decide what is the right combination of T-Bills, Singapore Savings Bonds, and Fixed deposit that fulfils their cash needs.

What am I doing?

I shared my general approach to cash management in a recent article:

Personally for me in this climate – I would prioritise liquidity.

I would optimise my cash positions for liquidity first, and yield second.

I think in this climate, the chances of a liquidity event in the next 12 – 18 months is quite high, and I want to have immediate cash on hand to buy if that happens.

So the priority for me is:

- Minimum amount of cash in savings account

- Max out Singapore Savings Bond allocation each month

- X amount in T-Bills / Fixed Deposit

- Rest in savings account (depending on liquidity needs)

The only change I would make to that, is that with T-Bills comfortably at the 4%+ range, it is getting close enough to the interest rate end game that I will start applying for T-Bills going forward as well.

But that will be in addition to my Singapore Savings Bonds.

If all the money is going into risk-free bonds… Are REITs still attractive?

Perhaps a logical next question.

A blue chip REIT like CapitaLand Integrated Commercial Trust yields 5.64% today.

When you can get 4.19% risk free from government T-Bills, why would anyone still put money into REITs at these prices?

Why would you want to take on all that equity risk, refinancing risk, liquidity risk, just for an additional 1.5% spread.

Capital gains you say?

Sure, but capital gains is a double-edged sword, and can easily turn into capital losses.

There’s a lot of uncertainty over what the next 12 months will look like, and with the Feds committing to higher for longer, equity risk premium needs to go up quite a bit to price in all these risks.

So yeah… like I’ve been saying all year, do not underestimate what rising risk free rates will do to global financial asset prices.

If interest rates stay higher for longer, more pain will come.

You can see my updated macro views and price targets for REITs on Patreon.

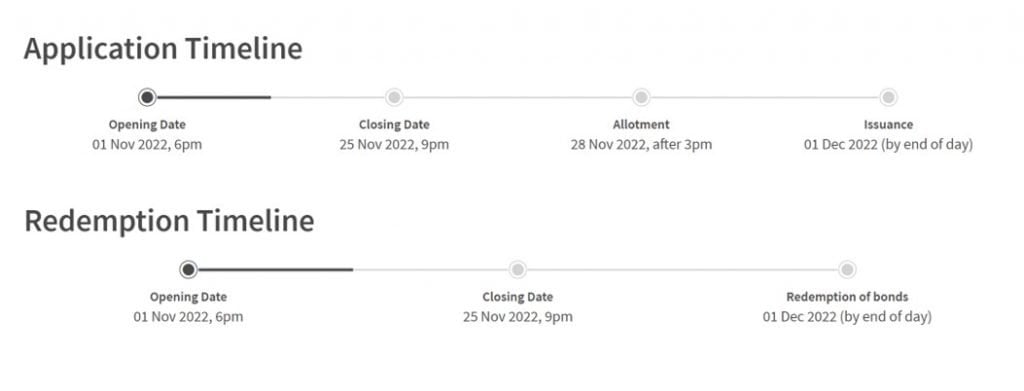

Application Timeline for December Singapore Savings Bonds

Application Timeline is below.

Don’t forget to apply by 25 Nov 2022 if you are keen to buy the December Singapore Savings Bonds!

Next T-Bills is coming up on 10 Nov

Shoutout also that the next T-Bills auction is on 10 Nov.

If you want to subscribe, you need to apply at least 1 business day before, so by 9 Nov.

You can apply via online banking for Cash and SRS, but you need to go down to a bank (OCBC, UOB and DBS) in person for CPF.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Off topic, but as a Meta investor, what are your thoughts on what’s happening there? Are you still fully invested? Are you adding to your position here?

I’m not a single stock guy but Meta’s price is starting to look interesting to me, though may have further to drop (along with the other tech megacaps). The negative sentiment on Meta is probably overdone in my view.

I think the problem is that there is a big sector rotation underway, away from the tech / FAANG and into real economy stocks.

Within that broader climate, individual names (like Meta) may be able to outperform.

But it might be easier to just buy into the sector that investors are buying (real economy stocks), instead of trying to play a rebound on individual names in the sector that investors are selling.

So it’s probably not a play for me, but that doesn’t necessarily mean you can’t make money from the stock. At the right support levels and with the right stop loss, could still be a good trade.

From a conservative investor standpoint, my strategy regarding Singapore Savings Bond (SSB) is to invest every month as a form of safeguarding cash which otherwise would have been placed in low-earning savings accounts. SSB ‘forces’ me to discipline myself with a regular savings plan. I divest/redeem the lower performing SSBs and purchase the new SSB if the new interest rates outperform the divested SSB’s latest paid or next to be paid interest amount. I also make sure that I only redeem the SBB that just posted the interest for the current month. I have been trying this strategy since 2019 and have redeemed older SSBs and then adding more funds to purchase the latest SSBs. I like the fact that I can plan and safeguard up to $200K and have a quick and easy redemption should I need it. SSBs are excellent additions to a basic savings account in my opinion for ease of providing liquidity.