In my recent Astrea IV Bond article, I had a theory that MAS/Temasek was trying to expand the retail bond market in Singapore, with SSBs being the first limb and Astrea’s PE bonds being the second. Nikko AM’s latest corporate bond ETF, the “Nikko AM SGD Investment Grade Corporate Bond ETF”, sure looks like the third limb in this broader strategy.

A recent Business Times article seems to confirm this point as well:

The ETF manager, Nikko Asset Management Asia, has an AUM (assets under management) target of S$50 million for the fund. The Business Times understands that the Monetary Authority of Singapore (MAS) is a seed investor.

Nikko AM declined to confirm this, but Eleanor Seet, its president and head of Asia-ex-Japan, told BT last Friday: “This is very much in line with a lot of the strategic initiatives that the MAS has always had in terms of growing the bond market locally … Anything that broadens, deepens the liquidity and breadth of the local bond market is so important.”

Whatever the reason, I can’t say that I’m complaining, because anything that provides greater investment choices, especially in the infant retail bond market in Singapore, is a plus in my books.

Basics: Nikko AM SGD Investment Grade Corporate Bond ETF

The Nikko AM SGD Investment Grade Corporate Bond ETF invests in a broad based set of Singapore bonds. It pays an annual dividend, and will be listed on the SGX.

Do note that as an ETF, there is no “IPO” here. Rather, it’s an Initial Offer Period, where you can place an order through your broker for units in the ETF. You will get whatever you apply for, so don’t go crazy and press S$100,000 like a normal IPO thinking that you will only get a small allotment.

Portfolio constituents

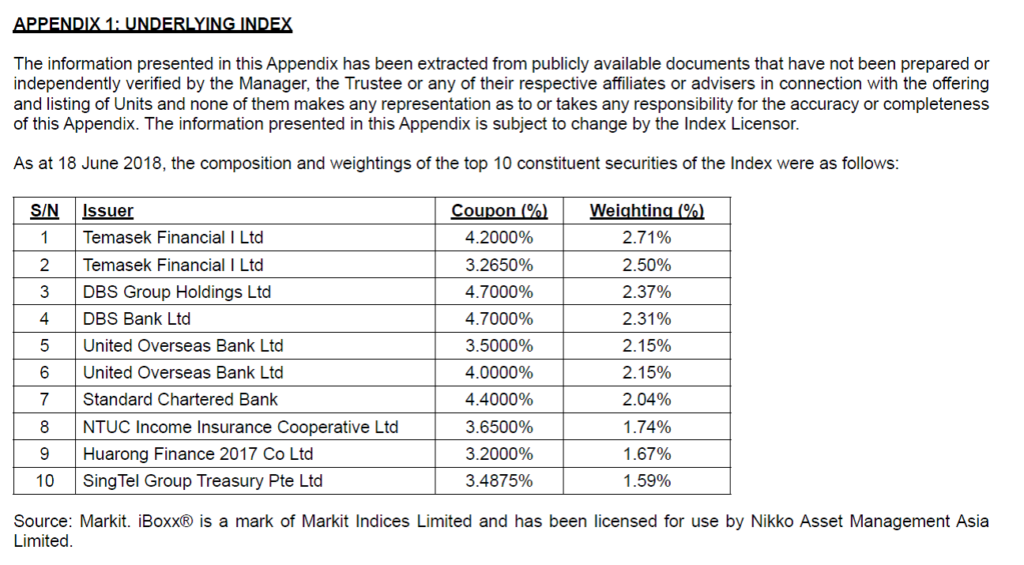

The Nikko AM SGD Investment Grade Corporate Bond ETF tracks the “iBoxx SGD Non-Sovereigns Large Cap Investment Grade Index”. Unfortunately the exact constituents of this Index is proprietary information that is not available to the public (also prevents frontrunning the ETF). Once the ETF is constituted, more details on its underlying holdings will be available, but as of now, all we know is what is disclosed in the Prospectus/Website:

Couple of points to note:

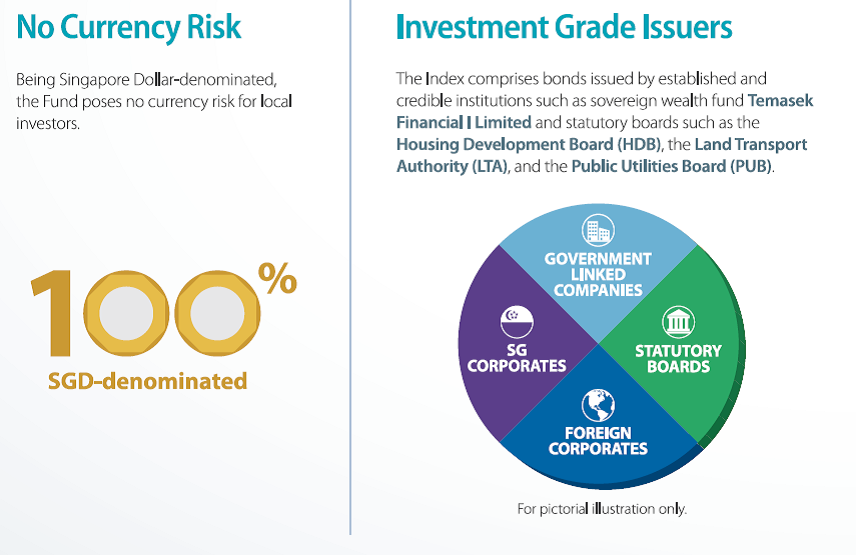

The bonds are 100% SGD denominated. This is definitely a plus, as I wouldn’t be comfortable with a Singapore bond ETF taking on forex exposure.

They adopt a fairly loose definition of “Corporate”. Despite being a “Corporate” bond ETF, the ETF clearly includes bonds from Temasek, HDB, LTA, PUB etc. Okay I get that if we exclude these quasi-government entities, the universe of SGD denominated bonds to choose from is greatly reduced. But then calling this a Corporate Bond ETF is not exactly the best name in the world.

In any case, I don’t view this as a negative, because these Temasek, HDB bonds have close to zero default risk to me, so I quite like that they are in the portfolio

They adopt a broad interpretation of “Investment Grade”. When I first heard of Investment Grade bonds, I assumed an Investment Grade rating by S&P or Moody’s. But it turns out that when Nikko AM means Investment Grade, they mean Investment Grade as per the iBoxx credit rating methodology, notwithstanding that the bonds are unrated. From the Business Times articles: In terms of weight, currently 22 per cent of the bonds in the index are not rated, including names like Singapore Airlines and the Land Transport Authority. Mr Sarmago explained: “iBoxx has an implied credit rating methodology based on current pricing. That determines whether an issuer is investment grade or not.”

Okay I get that a lot of great corporate bonds in Singapore are not rated (eg. SIA and LTA). I also get that credit ratings don’t really mean much these days, as evidenced in the previous financial crisis. But I would have appreciated that my Investment Grade Corporate Bond ETF actually bought IG Corporate Bonds. It seems strange to name it as such, when practically what this ETF buys is “high quality SGD denominated bonds that are not issued by the Singapore government”. It’s definitely less catchy, but it gives investors a better idea of what the ETF invests in.

And do note that while the ETF tracks the iBoxx index, the ETF has the discretion to invest 20% of their NAV in other types of bonds:

The Manager may invest in certain securities that are not included in the Index (“non-Index Securities”) but have aggregate characteristics (such as yield and duration) similar to those of the Index. The Fund can invest up to 20% of its total net asset value in such non-Index Securities, that should meet at least one of the following criteria: – SGD denominated bonds in which the bond or its issuer are rated as investment grade by S&P, Moody’s or Fitch, and have a minimum issuance size of SGD 100 million; – SGD denominated bonds by prevailing issuers of the Index with a minimum issuance size of SGD 100 million; or – Singapore Government Securities (SGS). The Fund will generally not hold all the securities that are included in the Index.

It’s a bit strange to me because that sort of destroys the whole point of an ETF, which is meant to be passive tracking and avoid the judgment call that comes with active management. I suppose their reasoning will be that the limited liquidity in the Singapore bond market may prevent them from taking up large positions in the certain bonds, so they need this flexibility to allocate it the money to an alternative bond

It’s quite hard to evaluate the quality of the underlying bond portfolio, because there simply isn’t enough information on its constituents. We’ll need to take a look at the full disclosures once the bond is constituted. But based on the information available, and leaving aside the naming issues, I do quite what this ETF is trying to do. As a retail investor, it’s incredibly hard to DIY a bond portfolio such as this, simply because the minimum subscription amounts for most of these bonds are S$250,000. Once listed, this ETF trades in lots of 100, with an initial listing price of S$1.00, so it’s easy to pop a few thousand on this ETF and gain exposure to a broad range of SGD bonds. It really gives a lot of added flexibility from a portfolio diversification perspective.

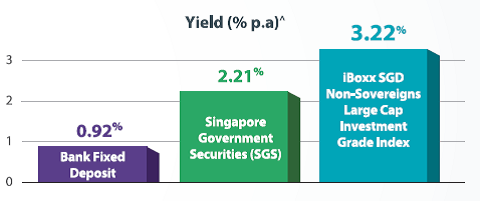

Yield

The indicative yield is about 3.22%.

This actually isn’t all that attractive, given that a risk-free SSB now yield 2.57% over 10 years. So that’s about a 0.65% risk premium for this ETF, but the SSB has zero risk and can be redeemed any time without worrying about market liquidity (you even get your yield up till the month of redemption).

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest, % | 1.78 | 2.16 | 2.37 | 2.54 | 2.67 | 2.76 | 2.81 | 2.86 | 2.95 | 3.11 |

| Average return per year, %* | 1.78 | 1.97 | 2.10 | 2.21 | 2.29 | 2.37 | 2.43 | 2.48 | 2.52 | 2.57 |

As comparison, the recent Astrea IV Bonds yielded 4.25% at IPO, and a blue chip REIT like Mapletree Commercial Trust yields about 5.5%. Personally I think the current yields on corporate bonds are a little low, and I would like to see it go up a little before opening a position.

Impact of Interest rate increase

At this point in the economic cycle, just about everyone knows that we are in a rising interest rate environment.

When interest rates go up, the market prices of bonds will fall. If you buy the bonds directly, you can always hold the bonds to maturity, where you get your principal and interest back (assuming no default). With a bond ETF, you don’t get this option. As bonds mature, the ETF will continually rollover and purchase new bonds. The net effect is that the market price of the bond ETF will be somewhat exposed to interest rate volatility. Of course, this isn’t necessarily a bad thing, because that’s exactly what a bond ETF is supposed to do.

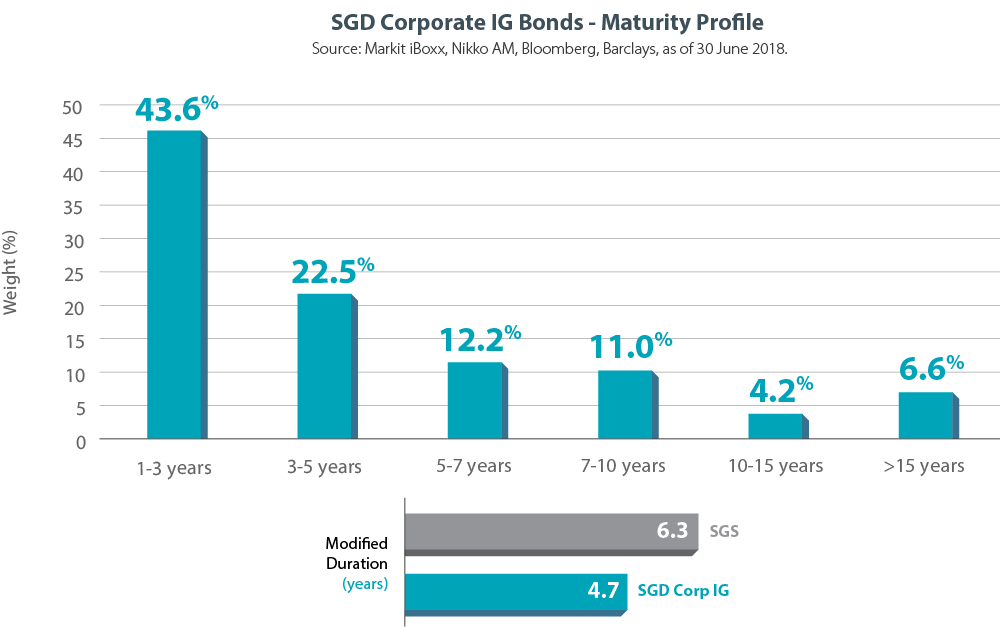

The maturity profile is tilted towards the short end as well, so there may be some volatility going forward.

Expense Ratio

The expense ratio is 0.3% per annum, locked in for the first 3 years. 0.3% isn’t exactly the lowest expense ratio around, but it’s hard to complain when it’s the only “corporate” bond ETF in Singapore. By contrast, the ABF Singapore Bond Index Fund (also by Nikko AM) has an expense ratio of 0.25%.

Liquidity

If past experience is anything to go by, I expect that there will be horrible liquidity for this ETF, with large bid-ask spreads (the difference between the price that sellers want, and what buyers are willing to pay).

Per the Business Times article:

The ETF manager, Nikko Asset Management Asia, has an AUM (assets under management) target of S$50 million for the fund.

The ABF Singapore Bond Index Fund, which invests in Singapore government bonds, has grown to an AUM of S$749 million since its listing in 2005.

The ABF Singapore Bond Index Fund with a S$749 million AUM has an average daily trading volume of 24,100. If we assume a linear correlation between AUM and trading liquidity (which is of course simplistic), we’re looking at about 2000 units daily trading volume for this ETF. That’s truly horrible.

Closing thoughts

It’s quite a straightforward decision for me for this one. There’s a bit of uncertainty over what exactly goes into the portfolio. There’s also a bit of uncertainty over what liquidity is going to look like. But that’s also okay, because I don’t see any need to subscribing for this “Corporate Bond ETF” during the initial offer period. It makes more sense to just wait until the ETF is listed, and have a look at what the liquidity, the AUM, and the underlying portfolio looks like, before reaching a decision on whether to invest. This isn’t like the Astrea Bonds where if you don’t buy at IPO, you may never get a chance to buy it at that price again.

But that said, I fully appreciate what Nikko AM is trying to do here. A corporate bond ETF is hugely useful when trying to build a diversified portfolio. As the first corporate bond ETF investing in SGD denominated bonds and targeted at Singapore retail investors, it is long overdue.

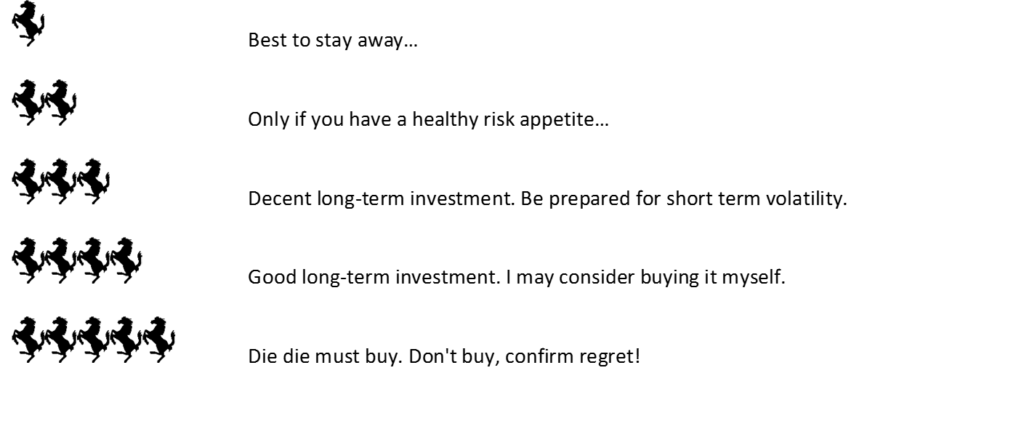

With that in mind, I’ll give this a 3 Financial Horse rating. From a longer term perspective, I expect that the risk of default is going to be low, given that they are picking companies like Temasek, HDB, SIA etc. But I also have concerns about liquidity. I’ll be keeping an eye on this one. If the liquidity is half decent, I may look to incorporate this into my portfolio in future.

Nikko AM SGD Investment Grade Corporate Bond ETF – Financial Horse Rating

Financial Horse Rating Scale

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!