Okay I have received quite a few requests for my views on Grab stock.

Since its high of $6.5 in October 2025, Grab stock has plunged 45% in 6 months.

Dropping to as low as $3.5 in March 2026 during the height of the Iran war.

Yet Grab remains South East Asia’s premier delivery and ride hailing app.

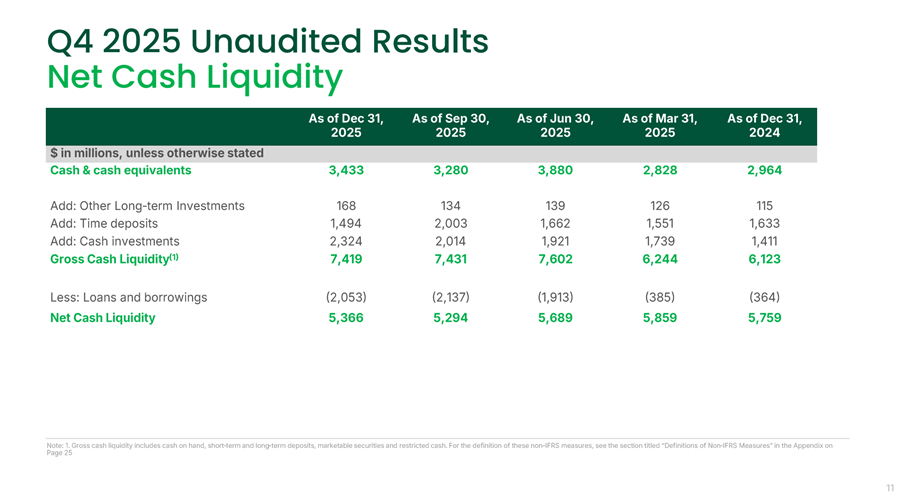

With $5 billion in cash on their balance sheet.

So… Will I buy Grab stock at this price?

Grab shares have dropped 45% in 6 months

Here’s the daily chart for your reference.

Since its high of $6.5 in October 2025, Grab stock has plunged 45% in 6 months.

Dropping to as low as $3.5 in March 2026 during the height of the Iran war.

Understanding the Grab business

Grab’s business today is split into 3 business lines:

- Deliveries

- Mobility

- Financial Services

Deliveries is Grab Delivery – delivers cooked meals, groceries, and parcels from local merchants directly to consumers.

Mobility is ride hailing – connects passengers with drivers for on-demand ride-hailing and transportation.

Financial Services is the newly created GXS bank – provides digital payments, micro-loans, insurance, and banking solutions for users and local businesses.

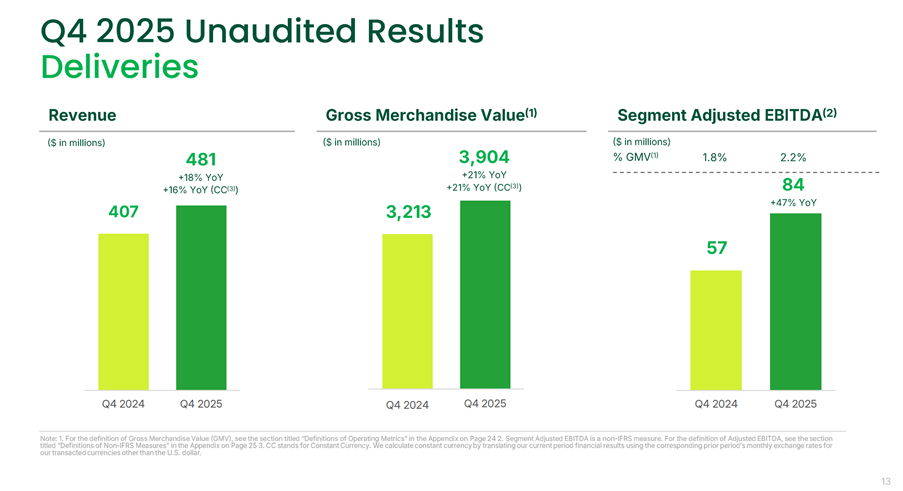

Delivery is the biggest business today

It may surprise many, but today the biggest revenue driver in Grab is actually not ride hailing but deliveries.

Grab delivery has surpassed the core Grab ride hailing business – and today sits at $481 million revenue vs $325 million for ride hailing.

Revenue growth is growing nicely at 18% year on year growth.

Business is also “profitable”, and adjusted EBITDA is up 47% year on year.

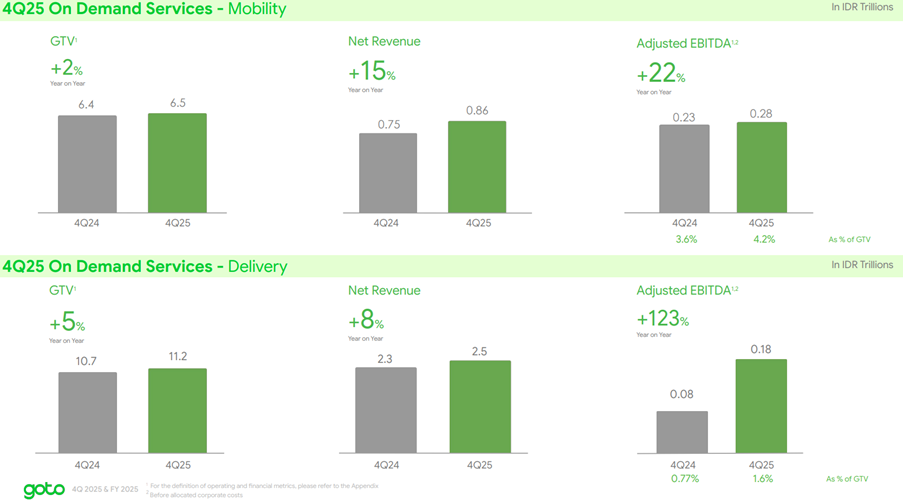

The most natural comparison for delivery and ride hailing is of course the direct competitor Gojek Tokopedia.

Here are their numbers.

Gojek’s delivery business is pulling in 647 million USD in gross merchandise value, which is way smaller than Grab’s 3.9 billion.

GMV growth is a miserable 8% compared to Grab’s 21%.

So Grab is the undisputed bigger player here – which is why you keep seeing talk about a potential Grab Gojek merger.

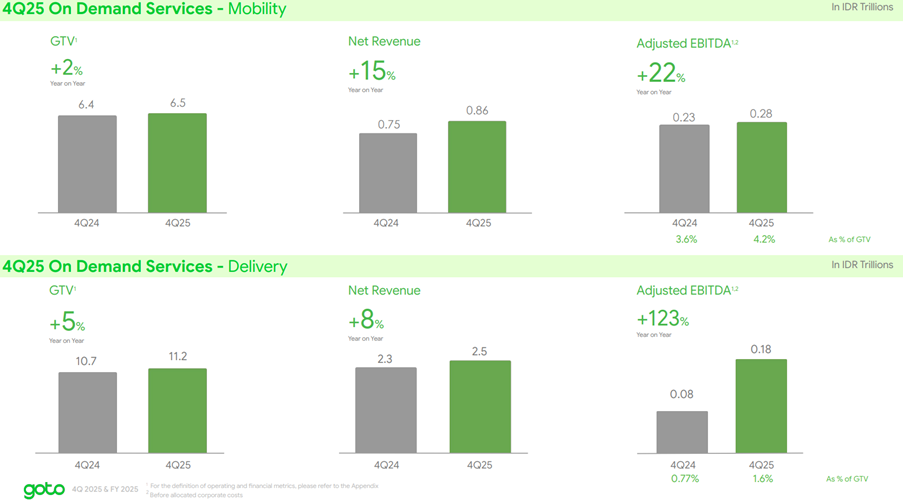

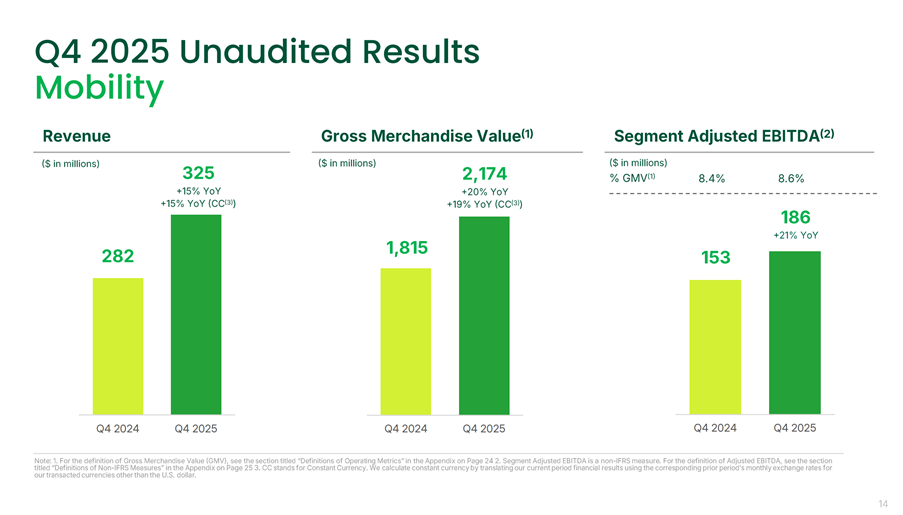

Ride hailing is a close second

What used to be Grab’s core business, ride hailing, now trails the delivery business.

Revenue is up 15% year on year.

Again the business is also profitable, and adjusted EBITDA is up 21%.

Gojek’s ride hailing pulls only $375 million GMV, which is way smaller than Grab’s $2.1 billion.

Again Grab’s 20% growth in ride hailing is far higher than Gojek’s 2%.

All in – Grab is the far stronger player in both deliveries and ride hailing.

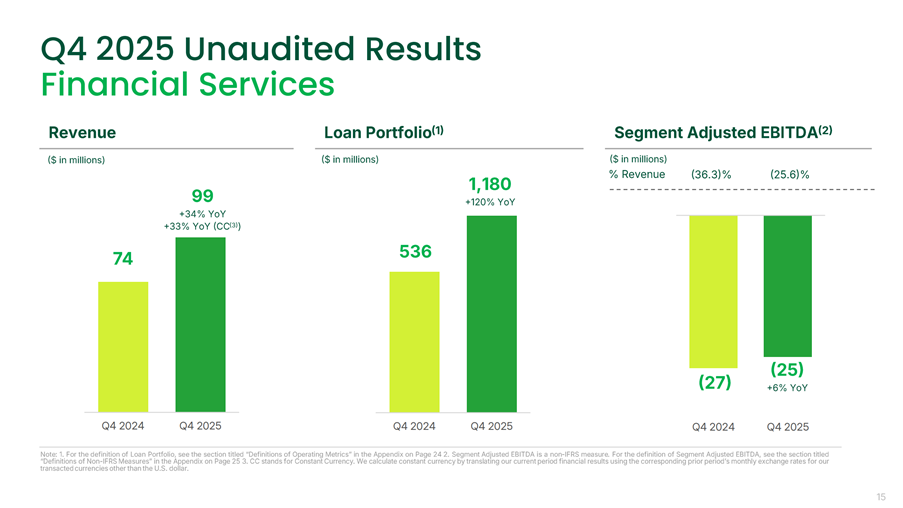

Financial services is the fastest growing

The third business line, financial services, is smallest but also the fastest growing.

34% year on year jump in revenue.

Loan portfolio up 120% year on year.

But this business is still losing money.

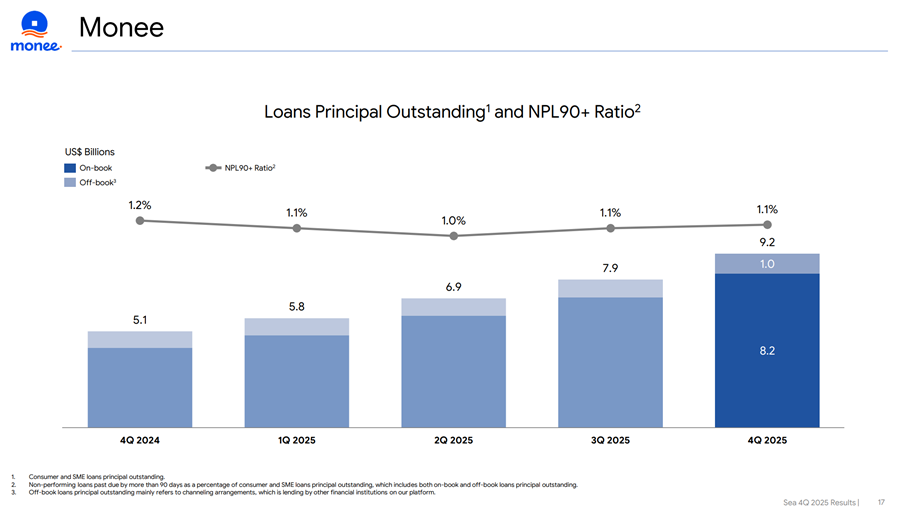

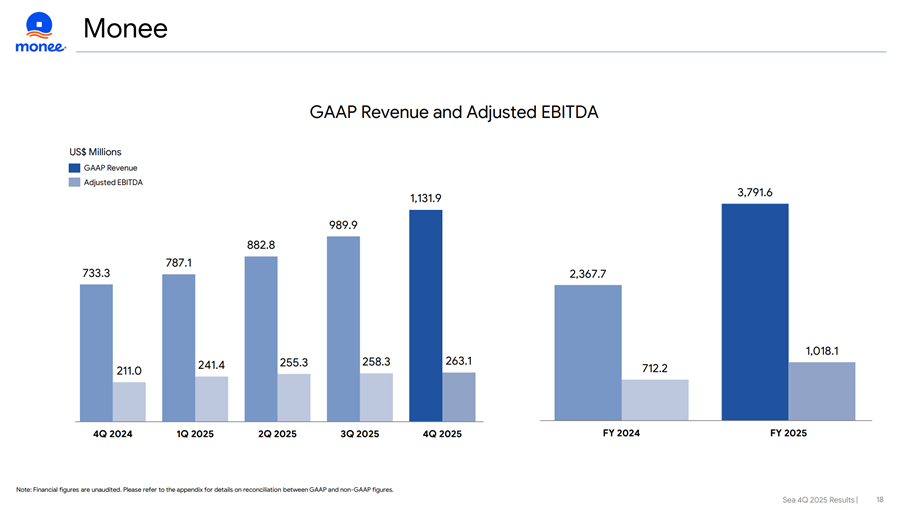

With the financial services arm it is only logical to compare with Sea Ltd’s Monee, which also operates in South East Asia in largely the same countries and under the same conditions.

By contrast you can see how Monee’s loan book of $9.2 billion is way larger than Grab’s $1.18 billion.

While Monee is also profitable on an adjusted EBITDA basis, unlike Grab.

Based purely on these metrics, it looks like Monee is a superior business to Grab’s banking arm.

But that said banking is a funny business.

You can look like you’re making a ton of profits during the good times.

But then an Iran war comes around, oil goes to $100, loan defaults start to spike.

You loan book goes bad, and suddenly you wish you had not been so aggressive with lending.

So frankly – you cannot judge the strength of a banking business in the “good times”.

It’s like that Warren Buffet quote – it’s only when the tide goes out, that you see who is swimming naked.

What is Grab’s acquisition strategy?

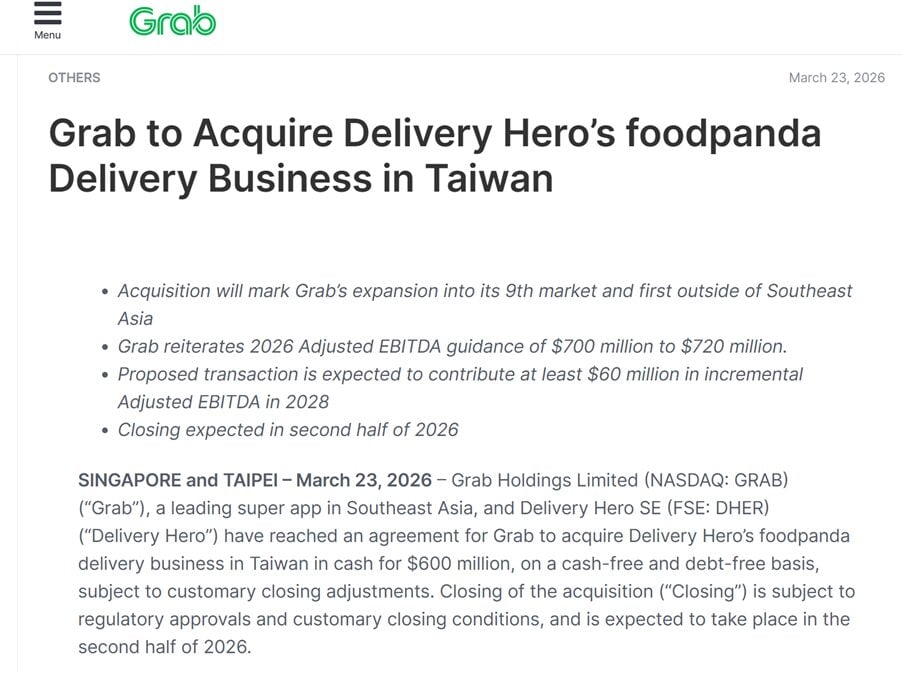

Grab acquires Food Panda Taiwan for $600 million

Grab has been very aggressive with acquisitions recently.

Here’s a $600 million acquisition of Food Panda Taiwan.

Grab acquires Stash Financial at $425 million Enterprise Value

And an acquisition of US Stash Financial at $425 million enterprise value.

But no acquisition of Gojek Tokopedia

But at the same time, the one mega acquisition that everyone is talking about and that would send the share price soaring.

The acquisition of Gojek Tokopedia.

Absolutely no news on that front.

Why does Grab not buy out Gojek Tokopedia?

If you ask me, it’s not that Grab does not want to buy Gojek Tokopedia to take out their biggest competitor, and then raise prices.

In my view – it’s a tacit realisation that this move is going to be fraught with political and anti-competition risk.

I mean just look at what happened when Grab bought Uber in Singapore.

Now imagine the same thing, in a country like Indonesia, where a lot of drivers depend on Grab for their livelihood, where politicians are highly sensitive to on the ground sentiment, and where politicians have a lot of power to make your life very difficult (whether by blocking the deal or preventing you from raising prices).

In my view – for Grab it may be better to just keep the status quo, keep Gojek around on as a very weak competitor, and then justify to regulators that hey it’s not a monopoly and therefore I can raise prices.

After all the numbers above show that Gojek is not really a meaningful competitor to Grab, so why bother buying them out and dealing with the political fallout.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

What then is Grab’s acquisition strategy?

That said, the acquisition of Food Panda Taiwan and the US Stash are interesting.

Food Panda Taiwan I get, it’s a natural bolt on transaction that fits into the delivery business.

Instead of spending years to compete in Taiwan, why not just buy the business and get an immediate large foothold in Taiwan.

Stash is a lot more tricky.

Because Stash is a US based Fintech, with a US customer base, and zero overlap with Grab’s South East Asia business.

I did some digging, and it turns out Stash has kind of gamified investing via their app.

So it seems like Grab wants to take this gamified investing experience, and replicate it across their current South East Asia user base.

Basically to upsell higher margin investing products to their user base.

Now that is a really ambitious shoot for the sky kind of move.

If they pull it off then that’s a huge multiple rerating for the stock, because this is real high margin stuff.

But if you ask me, I think the execution is going to be incredibly challenging, and I would be very impressed if they succeed.

But logic wise I get it. As management you cannot sit on your hands, you do need to try for some moonshots.

$5 billion on the balance sheet

The good news is that Grab is not in any immediate bankruptcy risk.

$5.3 billion in cash on the balance sheet.

With a core business that is profitable.

Both Sea and Grab have learned their lessons from 2022 when interest rates soared, and this shows.

Valuations of Grab vs peers

I ran the valuations of Grab vs its peers.

Because Grab has only just turned profitable, earnings have not yet stabilised so P/E is not meaningful.

The most relevant valuation metric I find to be EV/EBITDA.

On that basis:

- Grab is more expensive than Uber (but to be fair Grab is growing faster)

- Grab is more expensive than Sea (this is not apples to apples because they are different businesses)

- Grab is cheaper than Gojek (which is not justified because Grab is the better business)

- Grab is generally in line with Meituan (but Meituan faces structural Chinese delivery-war margin pressure)

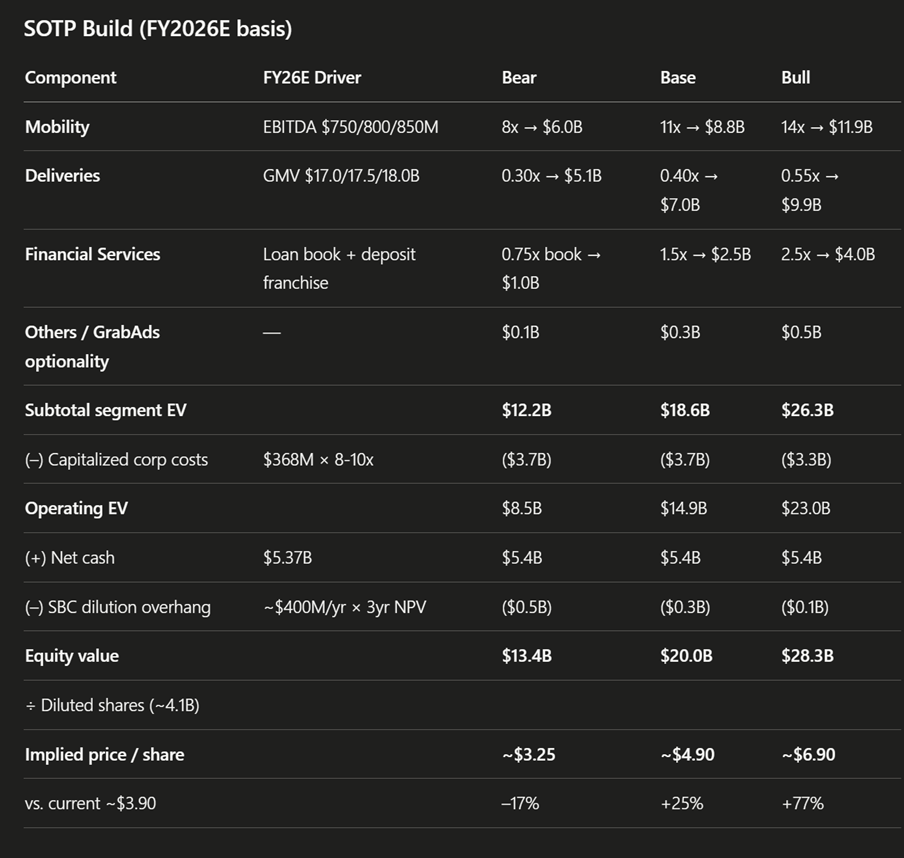

Sum of the parts valuation of Grab

I also ran a sum of the parts analysis for Grab, to value each of the 3 business lines.

My SOTP builds out to a base case equity value of ~$20B (~$4.90/share), vs. current ~$3.90 — roughly 25% upside.

Thinking is broadly as follows:

- Mobility is the anchor (worth ~$8-9B at 11x forward EBITDA)

- Deliveries the scale asset (~$7B at 0.4x GMV)

- Financial Services the biggest valuation wildcard (swinging the total by ±$3B depending on how it performs).

Bear/Base/Bull: works out to $3.40 / $4.90 / $6.90 per share respectively.

So current pricing sits somewhere between the bear and base case.

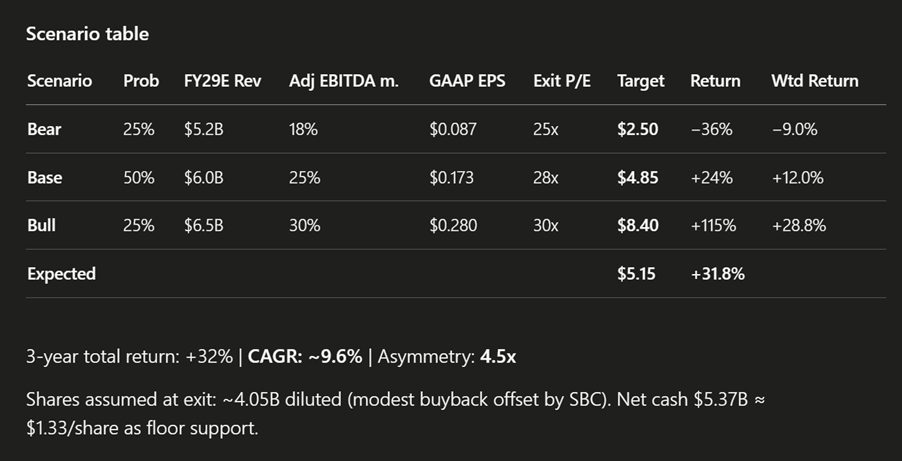

How much do you make when you’re right, vs how much you lose when you’re wrong?

I also ran a bull bear scenario analysis assuming a 3 year holding period (yes I ran a lot of numbers for this article that’s the beauty of AI today).

This was what I got:

In plain English, the bear case is where Indonesia driver-welfare regulation compresses ride hailing margins, and the financial services arm misses its targets.

Base case is where management delivers largely on its 2028 roadmap: revenue ~20% CAGR, Adj EBITDA ~$1.4B by 2028, financial services turns profitable on schedule, Deliveries ad margins scale toward the 4% target. No major surprises either direction.

The Bull case is where the Gojek merger closes and significantly reduces Indonesia competition, and GXS Bank + Stash scale into a standalone digital bank worth $4B+, with autonomous vehicle rollout structurally lowers Mobility cost base.

I make a lot of money in the bull case, lose quite a bit of money in the bear case, and make some money in the bear case.

My thoughts on valuations?

If you ask me.

I think the bull case here is unlikely.

That would require very impressive execution by the Grab team.

If you ask me the base case or the something below it is far more likely.

The problem then is that in the base case, it is a roughly 25% upside for a 3 year holding.

That doesn’t look amazing to me.

It just looks like to make big bucks on Grab, you need to have either (a) management execute flawlessly, or (b) broad multiple expansion for South East Asia businesses.

And if we get (b) I think we see higher upside on the other South East Asia “Super App” Sea Ltd, which coincidentally also has a stronger execution team.

Viewed this way, Sea Ltd could be the better buy, a stock that is also down almost 60% from highs.

Technical analysis on Grab stock

Technical analysis wise the chart is not pretty.

Yes share price has reclaimed the 50 day moving average.

But it’s hard to see this as anything other than a falling knife at the moment.

Grab shares plunge 45% in 6 months – Will I buy South East Asia’s “Super App”?

I think it will come down to 2 things:

- Is the Iran war over soon or will it drag on?

- Can management execute?

Grab’s business is a South East Asian business – where the economies are heavily dependant on oil imports.

If oil is going to stay at $100, it frankly doesn’t matter what management does, the stock will go into the dumps because higher oil prices will crush the delivery and ride hailing business, and we will see rising loan defaults.

Whereas if the Iran war ends soon and oil price comes down, we will see a large relief rally.

Then the question will turn to whether management can execute and deliver on its 2028 roadmap.

Base case I think they can probably deliver 80% of it, but whether they can surpass the roadmap, that I’m not so sure.

Full disclosure that I hold a position in Grab, and I added to my position recently.

But after this article I am kind of regretting my decision.

It’s not that Grab is a bad stock.

It’s more than even if I am right, I don’t make a lot of money. Whereas if I am wrong I could lose a lot of money, and this stock could go nowhere for a while.

Personally I hold both Sea and Grab, and Sea is the larger position.

But that said after having written this article even the smaller position I have in Grab seems slightly too large, and I may reassess my position in the days ahead.

My full personal portfolio is shared on FH Premium, with regular updates on what stocks I buy / sell.

I’ll also update my stock watch this week to share what stocks / REITs I am keen on after the Iran war sell-off.

This article is written on 24 April 2026 and will not be updated going forward. My latest macro views and views on single stocks, are shared on FH Premium, together with my full stock watch and investment portfolio.

Totally unrelated or maybe somehow related

Possible sentiment check as well

-Grab stock – 0 comments

-PIMCO Income fund – 23 comments

Good point haha