Okay so you guys know my views on REITs.

I don’t think this is the absolute bottom.

But for long term investors who don’t use leverage and have holding power, I think prices are interesting enough.

I myself have been meaning to add to my REITs positions, but couldn’t make up my mind on exactly what to buy.

So I decided to use an old trick that regular readers should be familiar with.

Let’s say I own no REITs or dividend stocks today.

And you gave me $100,000.

And gun to my head, I have to invest all of that money.

How would I do it?

Ground Rules – How would I invest $100,000 in REITs / dividend stocks today?

For simplicity’s sake, here are some ground rules:

- No more than 5 REITs / Stocks (to keep it simple)

- Cannot hold cash

- Average 5 year holding period

I just want to point out that (2) is a big one to understand this article.

Given all that is playing out today, with interest rates at their highest in 20 years, with 2 hot wars taking place around the world, with a risk of an economic slowdown the next 12 months.

This probably isn’t the time to go all-in.

I myself am holding elevated cash positions, and I leave for investors to decide what is the right cash allocation for themselves.

When cash is paying 4% risk free, the opportunity cost of being in cash is the lowest it has been in decades.

But the purpose of this exercise is to force me to think about where I would deploy the cash if I were forced to, today.

Hence Rule 2 – but I do want all readers to understand that deploying $100,000, may still mean holding another $300,000 cash elsewhere (for example).

How would I invest $100,000 in REITs / dividend stocks today?

So I thought about it for a bit.

And here was what I came up with, high level.

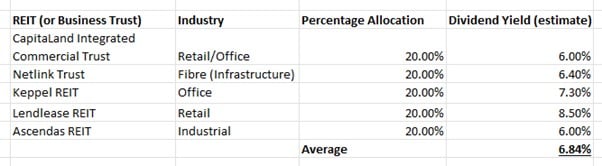

In table form:

| REIT (or Business Trust) | Industry | Percentage Allocation | Dividend Yield (estimate) | |

| CapitaLand Integrated Commercial Trust | Retail/Office | 20.00% | 6.00% | 0.0120 |

| Netlink Trust | Fibre (Infrastructure) | 20.00% | 6.40% | 0.0128 |

| Keppel REIT | Office | 20.00% | 7.30% | 0.0146 |

| Lendlease REIT | Retail | 20.00% | 8.50% | 0.0170 |

| Ascendas REIT | Industrial | 20.00% | 6.00% | 0.0120 |

| Average | 6.84% | |||

Please note that nothing in this article should be construed as financial advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. If you are in doubt as to the action you should take, please consult your financial advisor.

Probably not the bottom for REITs yet?

I’ll walk through each of the 5 names in further detail below, but I wanted to talk a bit about the asset allocation first.

Again, I don’t deny that this probably isn’t the bottom for REITs yet.

The way I see it, until the Feds start cutting rates, you won’t be able to call a definitive bottom.

And when the Feds start cutting, you still need to ask if we’re going to have a recession, and it also depends on how fast they cut, and so on.

But US Treasury Secretary Yellen announced this week that the US Treasury will shift more debt issuance towards short term debt over long term debt (ie. Less long term debt supply coming than what the market is pricing in).

This sparked a big drop in US 10 year yields, and could trigger a meaningful year-end rally.

I guess what I’m trying to say.

Yes, REITs probably haven’t bottomed yet.

But I’m getting paid 6.8% yield with my hypothetical allocation above – while I wait for the turnaround.

And this is only $100,000 of the portfolio, it assumes I have enough cash stashed away in T-Bills, Singapore Savings Bonds, Maribank etc that if further declines do come, I can still take advantage.

How does this compare with the proposed asset allocation a few months ago?

A month or two back I had a question from a reader about investing for dividend.

You can read the full article here – but this was broadly the allocation I proposed.

CICT and Ascendas remain on today’s list, so I guess you could say I’m boring like that for going for the stable CapitaLand blue chips.

Why did I remove Singapore Banks for this asset allocation?

The big change though, is the removal of DBS / OCBC.

If you read the original article – the reader was looking mainly for a dividend portfolio that could last decades.

Sidenote that I don’t think any asset allocation can last decades given how rapidly the world is changing.

(Heck for the first time in decades, you now have a very low probability of a world war erupting – so how do you have a static asset allocation for decades in times like that).

But I digress.

If I were investing for decades, then yeah as a Singapore investor it would make sense to buy Singapore banks, as a bellwether for the Singapore economy.

Risk-Reward for Singapore Banks?

But with a shorter time frame, I think the analysis changes somewhat.

Where we are in the cycle – Feds have already paused interest rates hikes since August.

Historically speaking, after a 6 – 12 month pause, what usually follows is rate cuts.

While early warning signs for the US economy are showing.

At 1.4x book value, with possible interest rate cuts and a slowing economy moving forward.

I’m just not sure I like the risk-reward on Singapore banks.

So I left out the Singapore banks in my asset allocation – but don’t crucify me for this.

I completely get that for longer term investors who don’t market time, Singapore banks are probably a good buy and hold.

Individual REITs / Dividend Stocks I would buy?

Let’s talk a little more about the individual REITs.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

CapitaLand Integrated Commercial Trust

CICT – I don’t think this REIT needs any introduction.

The largest S-REIT in Singapore.

Sponsored by CapitaLand, holding a mix of retail, office and integrated assets.

I used CICT (and Ascendas REIT and Netlink Trust) to form the bedrock of the portfolio, so I can take more risk elsewhere.

Ascendas REIT

Ascendas is the other blue chip REIT I included.

Sponsored by CapitaLand, holding primarily Singapore industrial properties.

Again one of the biggest S-REITs, I don’t think Ascendas REIT needs much introduction.

Unfortunately the prices have rebounded quite a bit since last week given the sharp drop in US 10 year yields.

Netlink Trust

I actually considered Keppel Infrastructure Trust as an alternative to Netlink Trust for this place.

The main point was to offer some diversification away from real estate, while getting decent yields.

Both offer very interesting diversification to real estate – Netlink Trust with fibre assets, Keppel Infrastructure Trust with energy/infrastructure assets.

Keppel Infrastructure Trust is the higher risk play, as reflected in its higher dividend of 7 – 8%.

In the end I picked Netlink Trust for the stability and ridiculously low leverage (23%).

Netlink Trust won’t see much growth going forward though, because of the nature of its business (cannot increase prices significantly).

Keppel Infrastructure Trust may see more growth potential, but that also means the risk of earnings going down.

So yeah… pros and cons.

Keppel REIT

I like Keppel REIT, but it seems that the market does not.

Even after the big rebound this week.

Keppel REIT still languishes near its decade lows.

At a 7%+ dividend, holding pretty solid Grade A offices in Singapore.

This was what I wrote for Patreons previously:

“Keppel REIT has never been a well-loved REIT, partly because it doesn’t hold 100% stakes in its key properties (eg. Ocean Financial Centre, Marina Bay Financial Center).

Rather these properties are held in a joint venture with other non-Sponsor third parties, which robs the REIT of operational control.

This is unlike other REITs by Mapletree/CapitaLand who usually only joint venture with their sponsor or hold 100% stakes (giving them full control over what to do with the asset – eg. Sell the building, perform AEI etc).

That said, the Singapore office exposure is still of very high quality.

And Singapore office is a very different market from the US – the work from home trend is nowhere as pronounced, and Singapore office buildings are still seeing very strong occupancy levels.

While there is more Grade A office supply coming online in 2024 (via IOI which TOPs next year), the market *should* be able to absorb that supply as there is still demand for Singapore office spaces from global MNCs (at the expense of HK).

Current prices trade at 7%+ yield, which is a close to 4% yield spread vs the 10 year.

I’ve been watching for this level for a long time, and just like Netlink, the key question now is whether this support holds.

If it breaks, that would be very bearish as there isn’t any support until the 2008 lows of 0.50.

But if current supports hold, I don’t mind adding to my position.”

It looks like the 0.80 support has held for now, but the weak rebound despite the broader market bullishness for REITs this week is a worrying sign.

Suggests there may be further downside in play.

For the record – Keppel REIT and Lendlease REIT are the “higher risk” REITs on this list, where I take on more risk for a higher dividend.

The full list of REITs I am looking at, with target prices, is available on Patreon.

Lendlease REIT

I had space for a retail REIT on this list, and it was a toss up between Starhill Global REIT and Lendlease REIT.

Both trade at 8%+ yields.

Both have sponsors that are okay-ish, but not best in class like CapitaLand or Mapletree.

Starhill’s crown jewel is Ngee Ann City.

While Lendlease’s crown jewel is Jem.

Both are arguably best in class properties.

I went with Lendlease because I do really like their property portfolio with Jem and Somerset 313 and Parkway.

But there are a lot of risks in play – namely the high leverage, the possibility of an equity fundraise to buy Parkway and so on.

Lendlease REIT did recover strongly this week together with the broad recovery for REITs, so perhaps the selling pressure is exhausted.

But ideally, I actually want to give more time for this REIT to play out, given all the news around Lendlease REIT.

Let’s see.

As always – will be sharing updated views on individual REITs with Patreons as it plays out.

Closing Thoughts: What is the right Asset Allocation

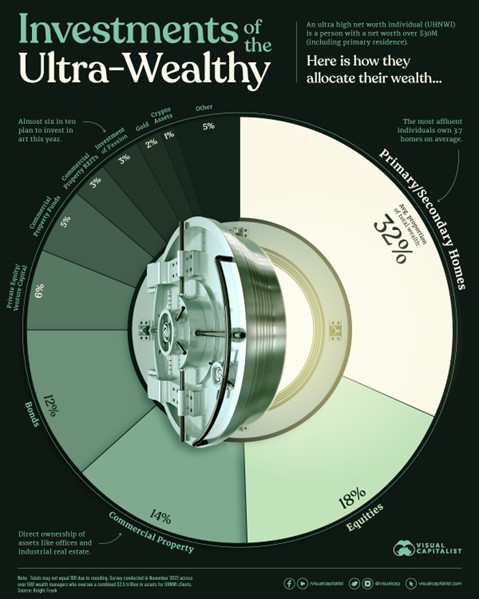

I came across this chart this week, which I promptly shared on Twitter (do follow me on Twitter if you haven’t already, I share great stuff there).

It sets out how the Ultra-Wealthy allocate their wealth (net worth over $30 million).

Interestingly, it goes like this:

- 32% Housing

- 18% Equities

- 14% Commercial real estate

- 12% Bonds

Caveat that this is US data, and the source is Knight Frank, so take it with a pinch of salt.

But still very interesting nonetheless.

It also shows that when you are rich, you want to run a broadly diversified portfolio across multiple asset classes to preserve wealth.

When you are building wealth though, then a more concentrated portfolio may make sense – provided that you understand the risks you are taking!

I leave readers to draw their own conclusions – and the right asset allocation for yourself!

This article was written on 3 Nov 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

I just updated the Stock / REIT watchlist for Patreons recently, on the Stocks / REITs I am keen to pick up (and approximate target pricing).

With the recent sell-off some of the big blue-chip REITs are starting to look interesting for long term investors.

Full list on Patreon if you are keen!

WeBull Account – Get up to USD 5000 worth of shares (Best promo of 2023)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

If one wants to own reits in diversified way, why not consider reits ETF like NikkoAM-StraitsTrading Asia ex Japan REIT ETF (ticker code: CFA)? Pay 0.6% expense ratio for less hassle, more diversification and automatic re-balancing.

I personally don’t like REIT ETFs. My own reasons:

1. The ongoing management charges eat into returns.

2. The better quality Singapore-listed REITs have quite good liquidity and small bid/offer spreads. I’ve not checked the bid/offer spreads on CFA, but they might be higher and the liquidity might not be great.

3. REITs are one of the easier types of investments to analyse (I recommend the Fifth Person’s Dividend Machines training course if you’re a relative novice).

4. The ETF will hold a some of the poorer quality REITs that tend to underperform and are best avoided.

5. I think it’s possible for the competent amateur to objectively do their own research and pick the better REITs. Much easier than for listed securities in general.

(There is no “right answer” on this sort of thing, but this is my own approach and I’ve done well with the REITs I own)

Pretty much agree with this. Personally not a big fan of REIT ETFs, but I’m probably slightly biased on this one haha.

It’s fine if you don’t want to stock pick. But ETFs for S-REITs are not so efficient given the small market size, and by its very nature ETFs mean buying the whole index, including the weaker REITs. Not to mention the expense ratio as well!

Hi FH, great article as always! Curious as to why you didn’t include Mapletree pan Asia commercial trust? I’m guessing it’s cos after the merger of Mct with mnact it’s just not quite as attractive with the foreign real estate proving to be a major drag? That and essentially the fact that management haven’t yet proven the merger to be a good thing for holders of mct, thus somewhat sullying the (previously) top tier management’s reputation

Just shared my views on MPACT here: https://financialhorse.com/mapletree-pan-asia-commercial-trust-drops-to-7-year-lows-will-i-buy-this-reit-at-6-4-dividend-yield/

I like the Sg assets for MPACT. But no doubt the HK/China portfolio may be a drag in the near term.

Hello,

Quick question, why or will you not consider stock like capitaland china or India trust? I mean respectable sponsor and quite high dividend and ok NAV too. I think

Thanks

I actually own CapitaLand China Trust as well. But no doubt China is going through a secular deleveraging, so their economy will be slow for a few years.

India – Not a market I follow closely, so can’t really comment. Real estate is a local business, I wouldnt go out of my circle of competence.