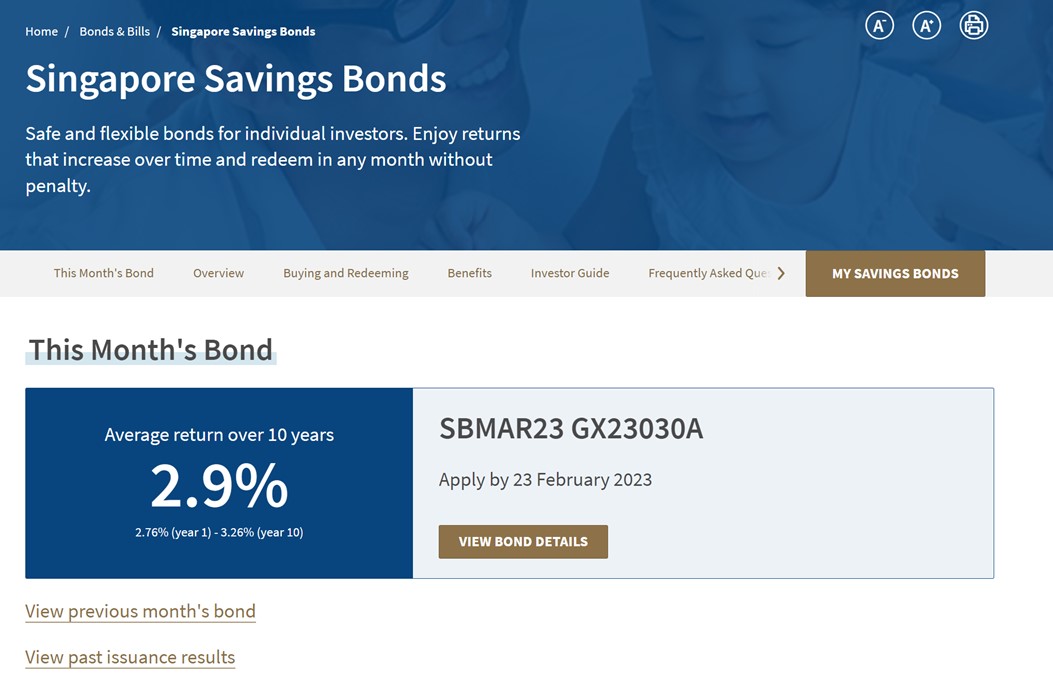

Okay so the latest Singapore Savings Bonds interest rates are out.

And the rates are absolutely terrible.

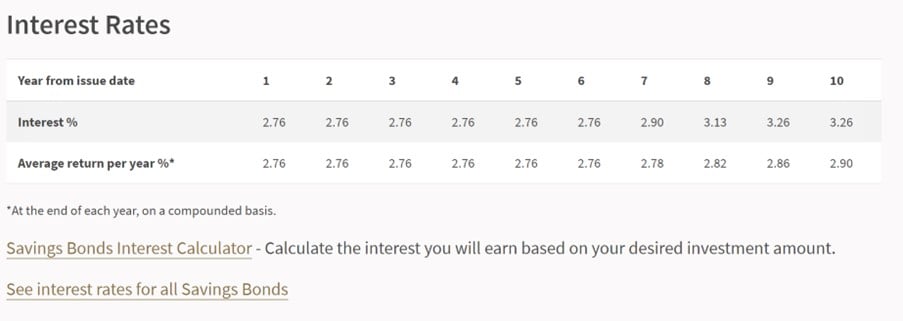

2.76% for the first 6 years.

And going up to 2.9% over 10 years.

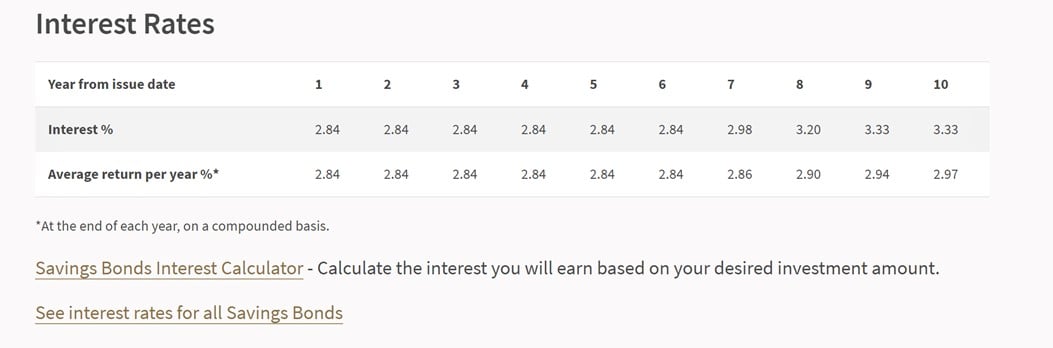

By contrast here are the rates for the previous round of Singapore Savings Bonds.

2.84% for the first 6 years.

I mean it’s still terrible, but better than the latest Singapore Savings Bonds.

Why are market interest rates going down?

Okay let’s address the elephant in the room – why are market interest rates going down.

A lot of you point to the fact that the Federal Reserve just raised interest rates 0.25% – and yet interest rates on Singapore Savings Bonds, T-Bills and Fixed Deposit keep dropping.

Why is that the case?

The short, soundbite version (of why interest rates are going down)

Well the short, soundbite answer is that market interest rates price in everything the market knows as to the future.

So Powell hiking 0.25% is already priced in – and it’s whether he is more dovish vs expectations that will move market interest rates.

And this week, the market “interpreted” Powell as being dovish (relative to expectations), hence interest rates went down.

The slightly longer and more complicated reason…

(of why interest rates are going down)

At least that’s the short, soundbite version.

The long version is much, much, much more complicated.

And you can read my macro piece yesterday for my in depth views on why this was the case, which is not so easy to summarise.

If I were to try, it would be that the market is expecting a soft landing.

Market expects inflation to go from 6% (currently) to 2% by end of the year.

And for the Feds to do 1 more 0.25% hike, hold it steady for a few months – before cutting interest rates in Q3 – Q4 2023.

I mean yeah… if the markets are right about inflation going from 6% to 2% in 2023 without a problem, then this is fair.

As shared yesterday though, I think that’s very optimistic given the red hot labour market, to say the least.

Where do I think interest rates will go in 2023?

I shared the broad framework in yesterday’s article.

I think interest rates (yields) go down short term.

This, together with loosening financial conditions, with result in economic growth picking up.

Throw in a US labour market that is on fire right now (see 517k jobs print on Friday), and you have a perfect recipe for inflation to pick up later this year.

Which would force the Feds to respond with further interest rate hikes.

So gun to my head, I think interest rates go down short term, and then go back up again later in 2023.

Timing wise is tricky because this is going to be path dependant.

Best guess I say maybe rates go back up in Q2 / Q3, but I think you really want to watch the data on this one.

Why are interest rates on Singapore Savings Bonds going down?

In any case, for Singapore Savings Bonds they actually track the average interest rates on Singapore Government Securities for the previous month.

So the rates you see for SSBs below, they’re based on the average of January’s interest rates on Singapore government bonds.

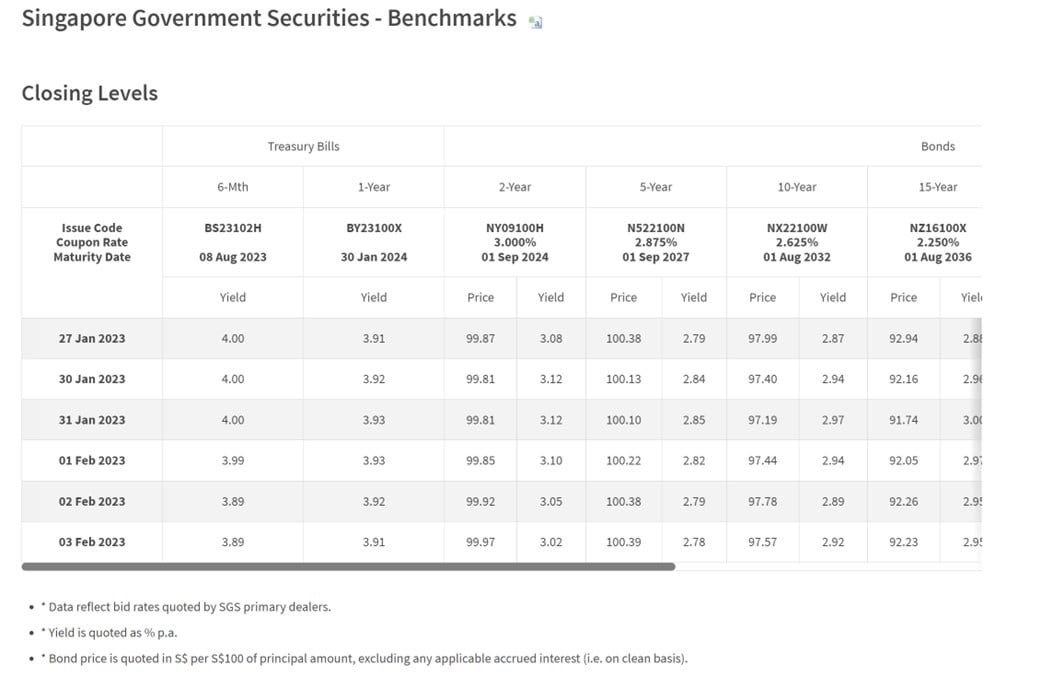

There is another slight technicality in that the short term interest rates for Singapore Savings Bonds cannot be higher than the long term interest rates.

This is a big problem right now when the yield curve is inverted.

You can see this below, the 1 year interest rate on the SGS at 3.91% is waaaay higher than the 5 year interest rate at 2.78%.

So the Singapore Savings Bonds have a formula to artificially smooth out the interest rates, such that interest rates will only be flat or increase every year.

Which gives you the following interest rate curve – with interest rates on Singapore Savings Bonds flat for the first 6 years.

T-Bills and Fixed Deposit Interest Rates are going down too

For what it’s worth – both T-Bills and Fixed Deposit interest rates are going down too.

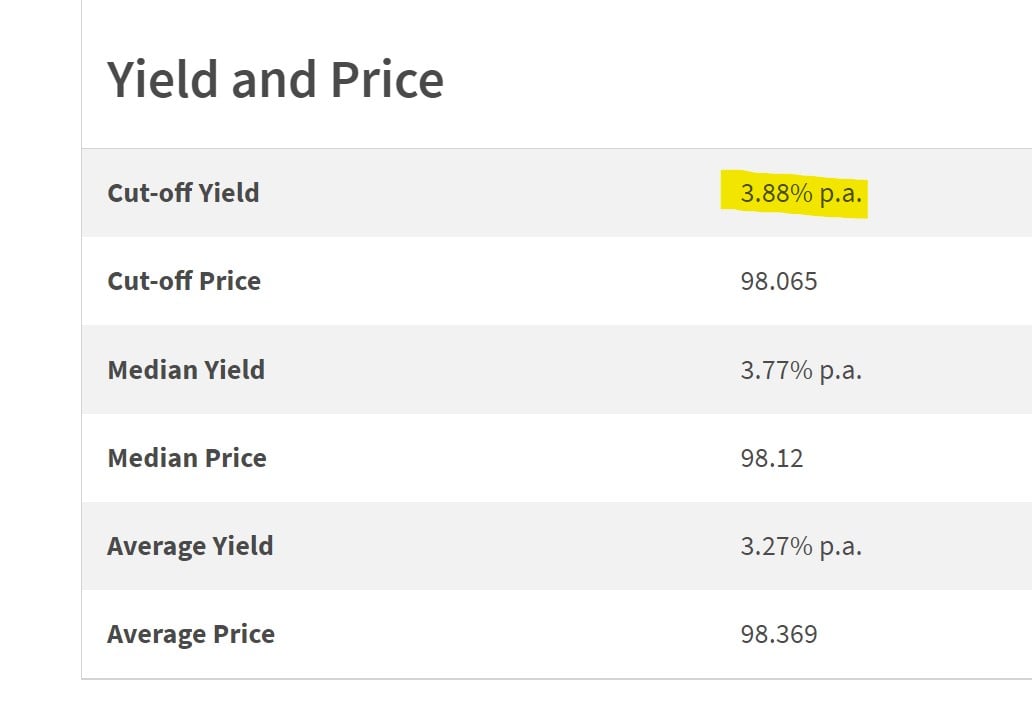

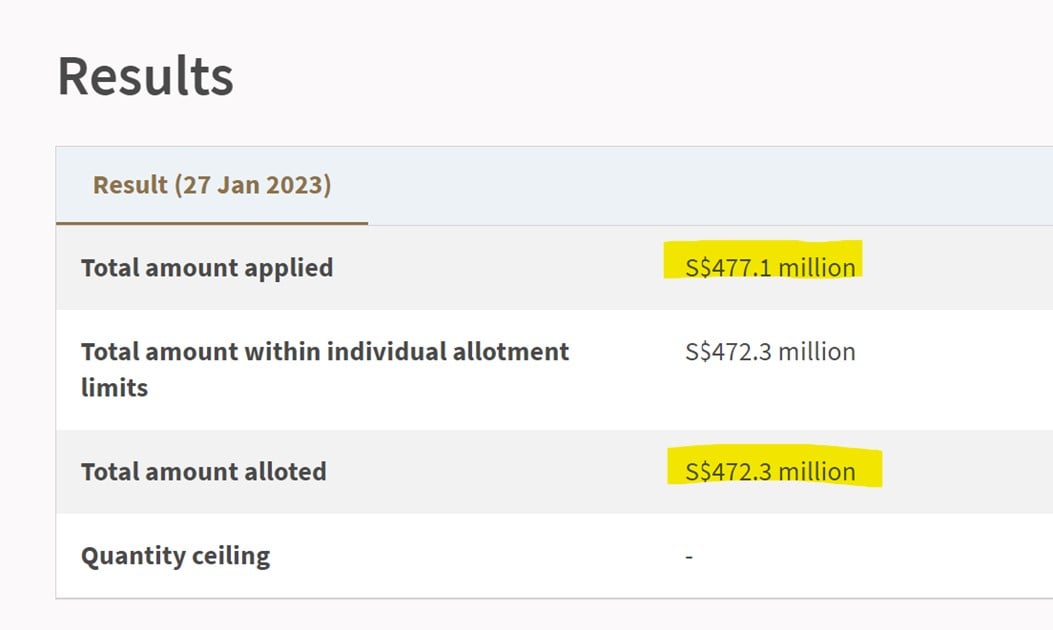

Latest 6 month T-Bills closed at 3.88% yield.

While CIMB’s Fixed Deposit, previously coming in at 4.2% – has now plunged to 3.7%:

Based on current trend, I do expect this to continue.

You might see banks revise their fixed deposit rates down once the promotion ends.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

So FH… buy Singapore Savings Bonds, T-Bills, or Fixed Deposit?

With that in mind, it may not be a bad idea to lock in current interest rates.

Yes, with my view I do think interest rates go back up later this year, but there is a lot of uncertainty over the exact timing of that move.

And what’s the saving about a bird in hand vs two in the bush?

As to whether to buy Singapore Savings Bonds or T-Bills or Fixed Deposit, I think it depends very much on your objectives as an investor.

Why buy Singapore Savings Bonds?

The main benefit of Singapore Savings Bonds is the option to hold to up to 10 years, and to get the money back any time with accrued interest.

It’s a good place to park emergency funds.

The drawback of course, is that the short term interest rates are not so high as compared to T-Bills or Fixed Deposit.

The bright side is that with the current not so attractive interest rates, you are looking at full $200,000 allocation for the previous round of Singapore Savings Bonds.

Which is likely to continue for the March Singapore Savings Bonds.

This is helpful if you want to buy a large amount of Singapore Savings Bonds at one go.

Will I buy Singapore Savings Bonds?

As shared – I took the opportunity the past 2 months to redeem all of my 2018 / 2019 Singapore Savings Bonds.

And I have been religiously applying for Singapore Savings Bonds the past 6 months or so – to the point where I am maxxed out on my $200,000 allocation today.

All of my current Singapore Savings Bonds I am holding have interest rates higher than the March Singapore Savings Bonds, so I will not be applying for the March SSBs.

That said, those of you still holding onto older Singapore Savings Bonds should take the opportunity to redeem and refresh them.

You can redeem and apply in the same month FYI, as long as you have the cash to do so (you need to pay for the application before you get the redeemed cash back).

Yes I get that the interest rates for Singapore Savings Bonds are not as attractive as T-Bills / Fixed Deposit, but I think the liquidity alone is valuable.

It’s a good place to park some emergency funds there.

Why buy T-Bills or Fixed Deposit?

That said if you want higher interest rates, and you don’t need the liquidity, T-Bills and Fixed Deposit are very attractive.

At current interest rates I think Fixed Deposit is more attractive.

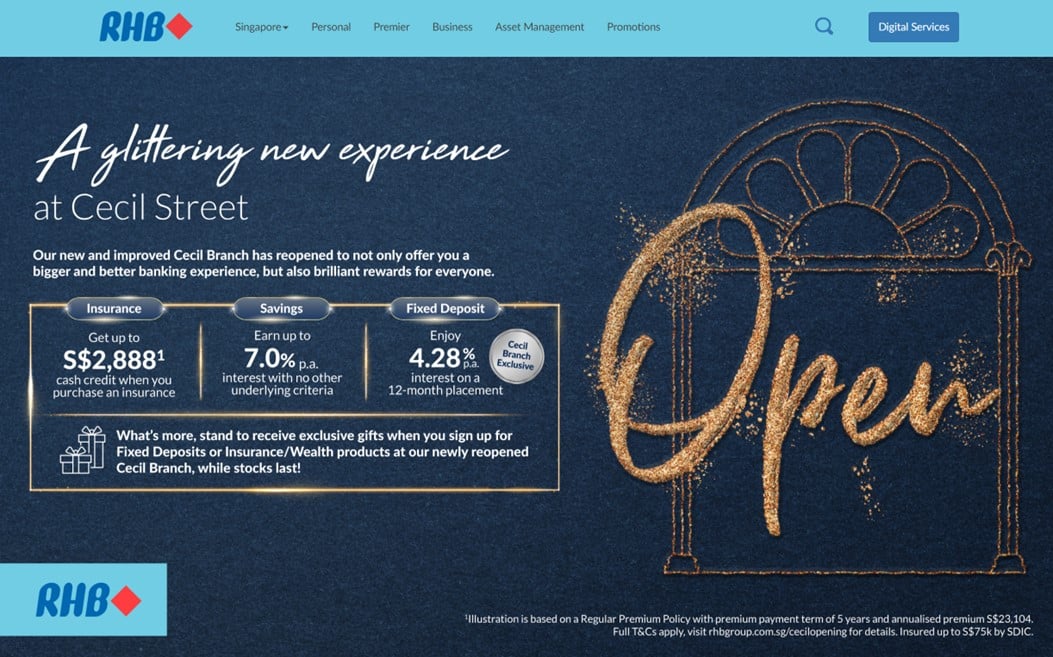

Your options are 4.28% with RHB Bank (you do need to go down to the physical bank branch though).

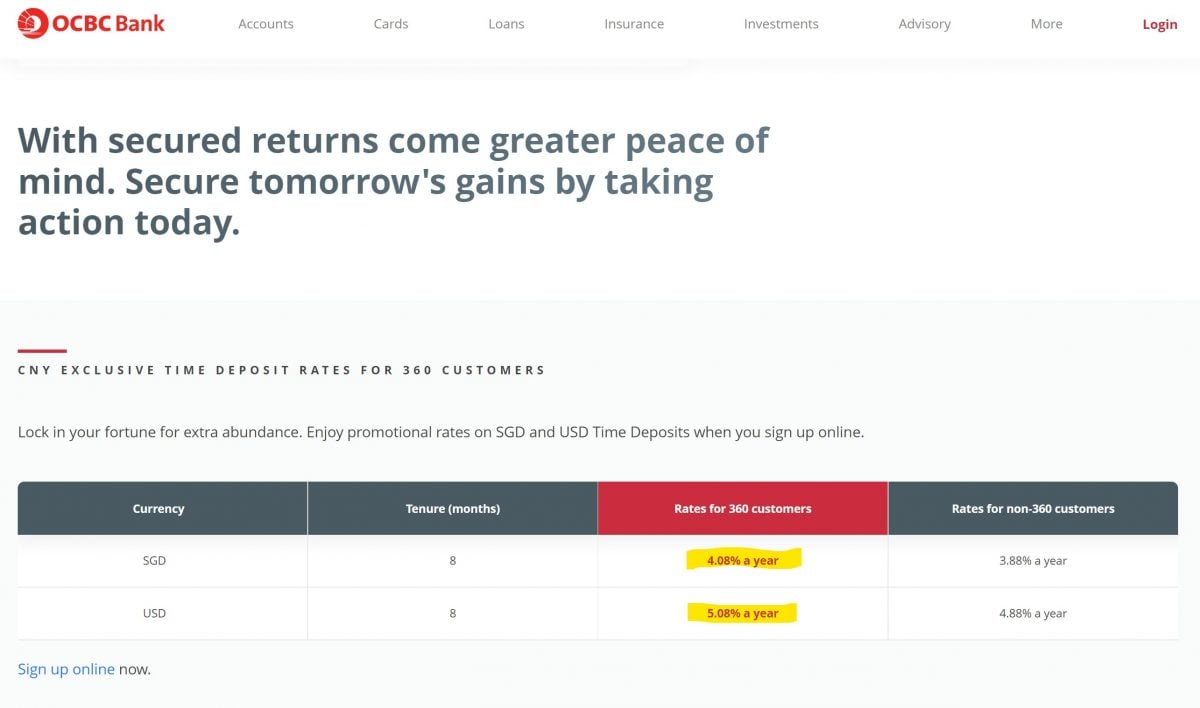

Or 4.08% with OCBC (you do need an OCBC360 account to enjoy this though).

Will I buy T-Bills and Fixed Deposit?

Yes, I see T-Bills or Fixed Deposit as a good way to earn some extra yield on short term cash that I’m not using.

Personally I’m not big on going down to the bank, so I just chucked a bunch of spare cash into OCBC’s 8 month 4.08% fixed deposit this week.

Given that it’s a higher yield than the latest 6 month T-Bills at 3.88%, seemed like a no brainer to me.

Singapore Savings Bonds Application / Redemption Timeline

If you’re keen to buy (or redeem) Singapore Savings Bonds, here’s the timeline.

You want to submit your application or redemption orders by 9pm on 23 February 2023!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi FH,

For the 2 upcoming 6-Month T-Bills in Feb-23 (Announcement Dates = 09-Feb & 23-Feb), is it right to say that buying the 23-Feb is better as it matures 05-Sep & allows us time to roll over & buy T-Bills in same month (Sep-23) to avoid loss of revenue (since CPF not pay in that month) ?

T-Bill / Announcement Date 09-Feb / Maturity Date 22-Aug

T-Bill / Announcement Date 23-Feb / Maturity Date 05-Sep

Yes, that’s correct. Although another way to see it is that if you buy the 9 Feb T-Bills you start earning the higher interest 1 month earlier!

Look at US 6 months T-Bills. It is going up.

https://ycharts.com/indicators/6_month_treasury_bill_rate

Look at SG 6 months T-Bills, it is going down.

Your views are strictly yours.

Sorry not quite sure what you mean. My view is rates down short term, up mid term.

This is broadly the case with the US2Y.

US6M wont reflect this because market is pricing in cuts in 2H2023, which won’t show up in the 6M.

Hi FH, SSB GX22080V, first year 2% and 5th average 2.82% and 10th year average 3%. Latest SSB GX23030A, first year is 2.76% and 5th year average is 2.76% and 10th year average is 2.9%. Latest SSB has higher average interest in the first 4 years, but lower average interest thereafter. Does it make sense to redeem GX22080V to apply for GX23030A (assuming fully invested and no more spare cash, that’s why have to redeem GX22080V if want to apply GX23030A). Can please share your thoughts on this? Thank you.

I suppose it comes down to whether you want a higher interest rate today, or a higher interest rate tomorrow.

If it were me I would go for the higher interest rate today, bird in hand and all. I rather earn the higher interest today than hold out for higher interest tomorrow. Whatever one’s view on the interest rate path, you do at least need to factor in the possibility that you are wrong, so in such situations always better to get the bird in hand first.