Okay first off – I did the research for this piece a few days ago, before the carnage that was yesterday.

So some of the charts are not so accurate after last night.

But the point is that – even after the past week, US stock indexes are still very close to all-time highs. While a lot of the big China stocks have corrected quite a fair bit.

As investors, the choice is ours.

Go with US stocks at record valuations into a Fed hiking cycle with rising inflation. Or China stocks that have corrected due to the regulatory crackdown and China economic slowdown.

Whatever your choice, China is one of the largest markets in the world today. Love it or hate it, it pays to at least understand what’s going on there.

Note: Moomoo (Futu) is a great low cost broker to buy China and HK stocks, with very useful features for stock analysis.

Check out my review on moomoo here, and get 1 Apple share (worth ~$200) + $40 cashback* when you sign up and deposit $2700 or equivalent (USD/HKD). Sign up link here.

All views and opinions expressed in this post are from Financial Horse.

China Real Estate Slowdown + Regulatory Crackdown will continue to play out

I do want to emphasise that this is not a post about timing.

China stocks are at quite critical levels now and they look like they’re starting to break down, so some caution is warranted (Update: after the past few days they’ve broken some key technicals, so caution is warranted in the short term).

GDP now forecasts are putting China’s growth at 5%, significantly below the 6-7% pre-COVID.

All while the regulatory crackdowns and real estate slowdown are playing out at speed.

Whatever your views on China, at the very least some averaging in is required, as it’s hard to say what 2022 might bring.

I will probably do a separate post to share more views on market timing, so do check back for that.

Top 5 China Value Stocks to buy for Singapore Investors

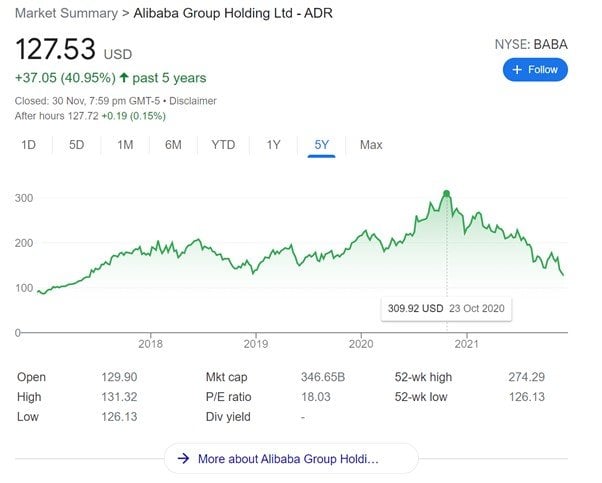

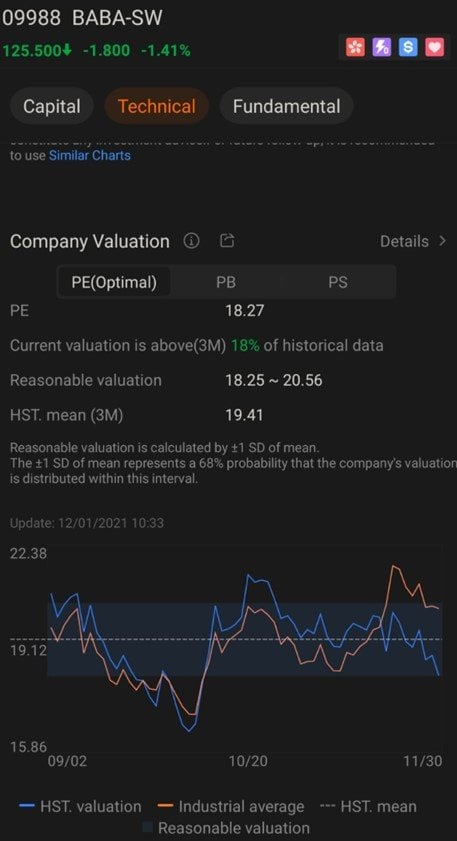

Alibaba

Market Cap: $357b

PE Ratio 18.6

Let me just address the elephant in the room.

So many of you have reached out to ask for my views on Alibaba.

As of closing on 30 Nov, Alibaba is down 59% from all-time highs in late 2020.

Talk about a bear market.

I have a medium sized position with an average cost of about $200, so I’m quite comfortably underwater on this position.

The problem with Alibaba, is that the anti-competitive restrictions have hurt Alibaba really badly.

You know how Alibaba was forced to stop all the monopolistic practices like forcing vendors to only list on Alibaba and not JD (二选一)? Well, it turns out that was crucial to growth after all.

After Alibaba was forced to stop it, all the vendors went ahead to list on every platform, contributing to a big fall in growth.

So there is competition at the high end (Tier 1 Cities, affluent consumers) from JD, and competition from the low-end (Tier 4 cities and beyond) from PinDuoDuo (which also had a disaster of an earnings).

At the same time there is very strong competition from the “new eCommerce” players like Bytedance and Kuaishou, who sell via livestreaming influencers.

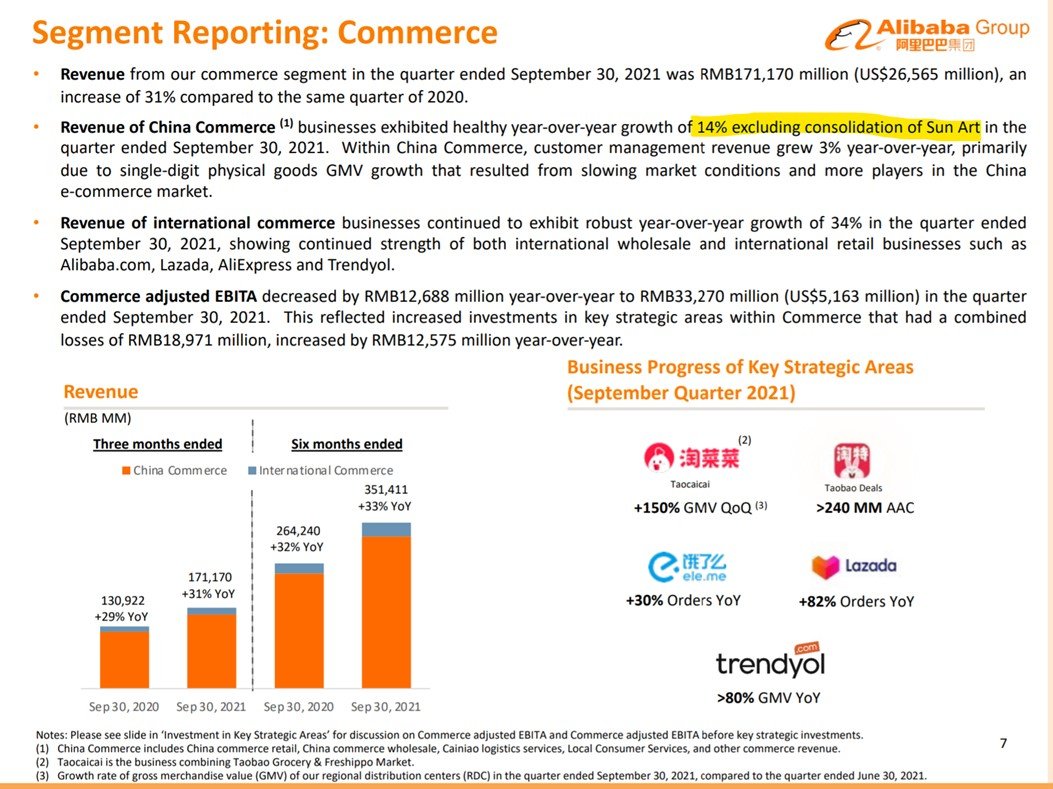

Latest earnings are a disaster – excluding the Sun Art acquisition, the core China commerce business only grew 14%.

So it’s very easy to say that the regulatory crackdown destroyed Alibaba, but the reality is more that Alibaba’s hyper growth relied greatly on anti-competitive practices and abuse of market position.

Once that was taken away, their growth moderated.

To return themselves to growth, Alibaba needs to find new ways of growing the business through innovation, rather than simply abusing their market power.

Which of course you could argue, is exactly the purpose of the regulatory crackdown.

For what it’s worth, Alibaba continues to experience strong growth in:

- International eCommerce (33% year on year)

- Cainiao Logistics (20% year on year)

- Cloud Computing (33% year on year)

And don’t forget that 33% stake in Ant Financial.

It seems Alibaba has been really hurt by the lost of their charismatic leader Jack Ma, and the question is whether current CEO Daniel Zhang has the vision to turn around the company.

Unlike Jack Ma who came from pure entrepreneurial roots, Daniel Zhang came from a banking/financial background, and feels more like a Tim Cook kind of leader.

You know, the kind who can build on existing strength to go to new heights, but not the kind you want by your side killing crocodiles in the Yangtze – which is what Alibaba needs now.

Alibaba’s business execution hasn’t been so great in recent years, look at how they botched the whole Lazada vs Shopee fight in South East Asia.

But for now they still have a very commanding position in China eCommerce, and a lot of financial and talent firepower at their disposal.

It’s probably too early to rule Alibaba out, especially when sentiment is this negative around the stock.

But I would definitely want to see some signs they are turning around the business before adding to my position.

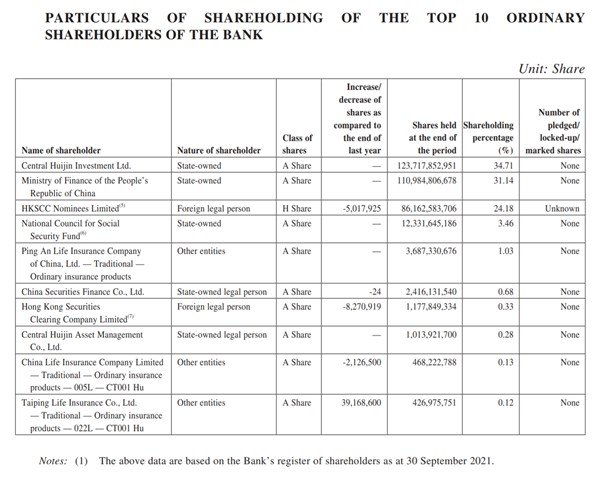

ICBC (or any of the Big 4 China banks or Ping An)

I recently wrote a piece on why I am buying the China banks, so do check it out for my fuller views.

For what it’s worth, capital adequacy ratios are rock solid.

And earnings are growing nicely – 10.5% growth in net profit.

But frankly, this is probably the most important chart – the 34% state ownership of ICBC.

As Singaporeans we’re very familiar with this concept, as DBS Bank is 29% owned by Temasek.

You can argue that the loan book is a black box, there is a risk of ICBC being called upon to do national service, real estate contagion and the whole host of worries around China.

I don’t disagree.

But let’s put it this way, if you believe that China will grow into the largest economy in the world in the coming decades, then an investment in ICBC is kinda like going back to 1980s and buying DBS Bank.

Sure, there was massive volatility along the way, and a real possibility the bank would have gone under if the government didn’t step in.

But there was also a chance to make really big bucks.

At current prices you get a 7.5% dividend (trailing twelve months) too, so at least you’re paid to wait.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

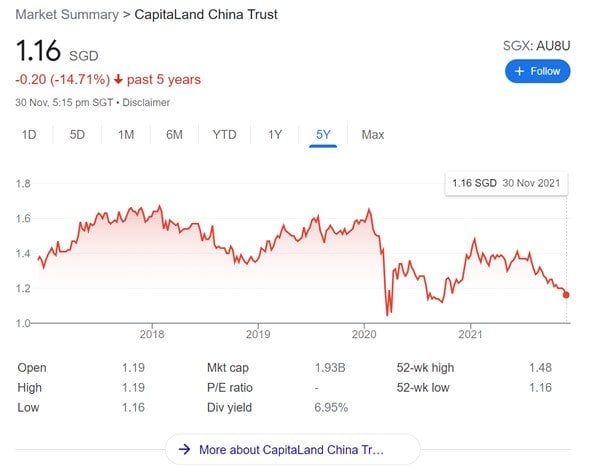

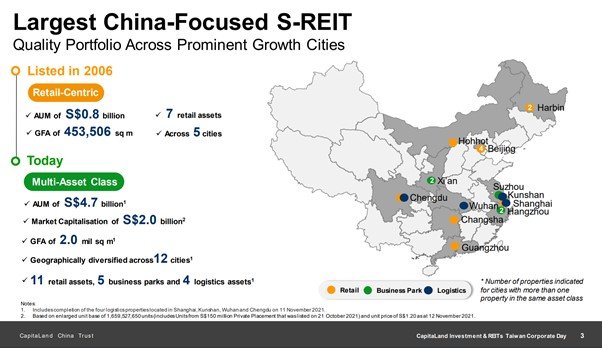

CapitaLand China Trust

Market Cap: S$1.93b

Dividend Yield 6.95%

Price to Book: 0.71

I really wanted to add a real estate counter to this list.

The China real estate crisis is playing out at full speed though, so it’s still a very risky play now.

So I wanted to stick to the offshore players, who have access to offshore financing and are less exposed to onshore refinancing risk.

I’ve heard a lot of good things about Hang Lung, but in the end I went with homegrown CapitaLand China Trust.

The last time I added to this REIT was below $1 in the depths of the COVID panic, and who knows, we may see this REIT trade there before all this is over.

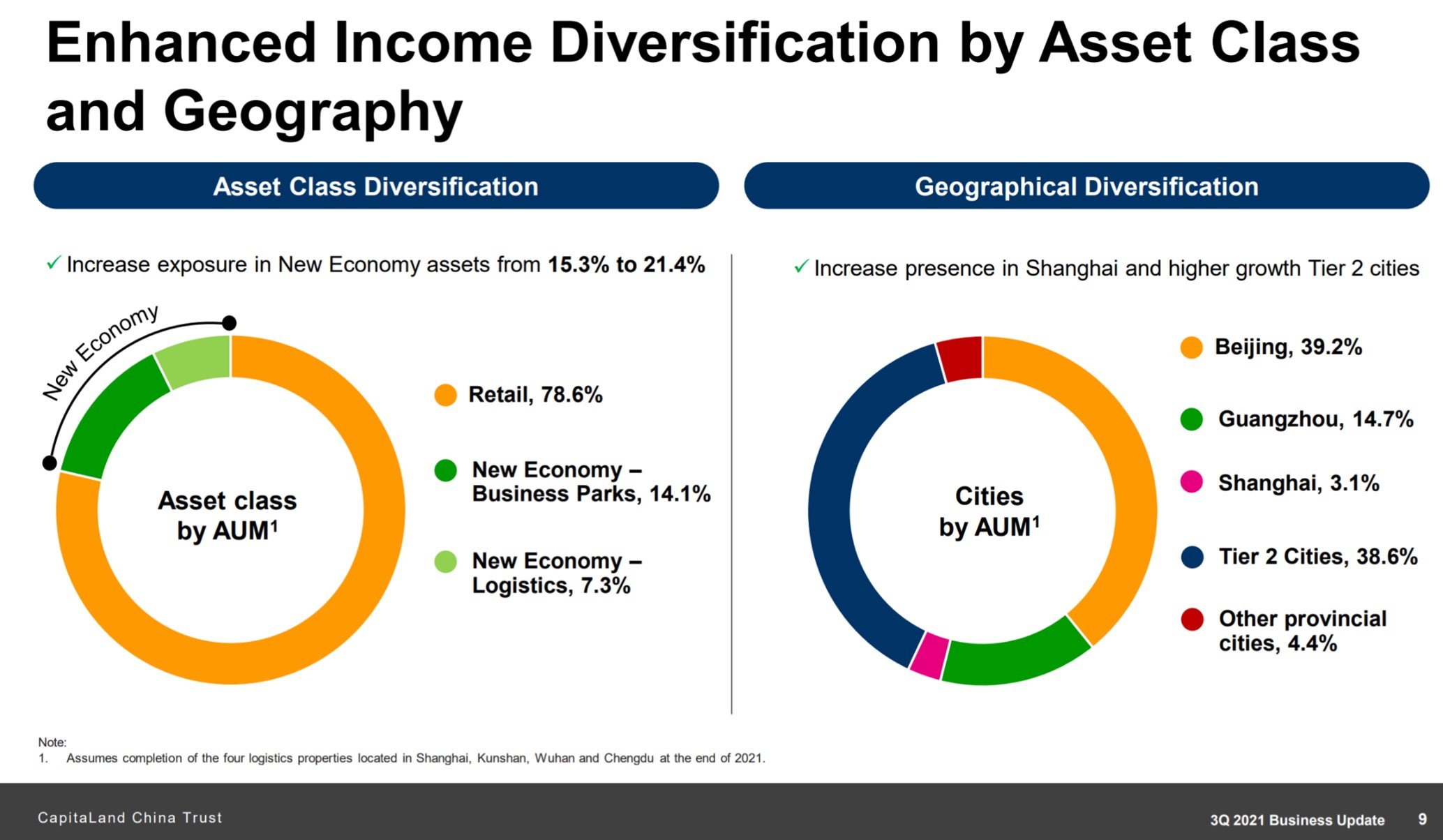

What started out as a pure Retail REIT in 2006 has recently diversified into new economy assets in business parks and logistics.

About 50% of the asset base is in Tier 1 cities (Beijing being the largest), and the rest coming from Tier 2 Cities.

There’s no way around this, because if the REIT is pure Tier 1 Cities you’re going to be getting a very low 3-5% yield, that’s how overpriced real estate in Tier 1 Cities are.

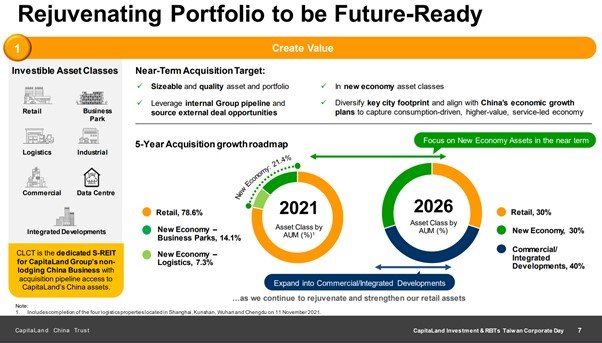

The vision is very interesting too – CapitaLand China Trust positioned as the “dedicated S-REIT for CapitaLand Group’s non-lodging China business”.

By 2026, they want to have 30% new economy and 40% commercial or integrated developments, which signifies big changes for the REIT to come.

At current prices, you’re getting a 30% discount from book value, and a 6.95% dividend yield.

And backing by CapitaLand, which does reduce insolvency risk.

I don’t think China’s real estate saga is over by any chance, so do watch your timing.

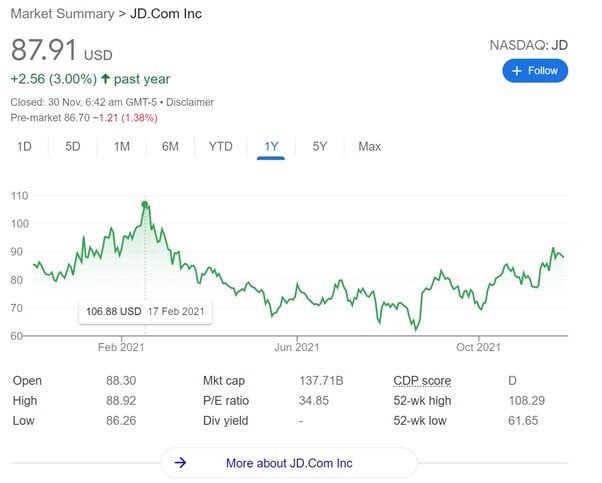

JD

Market Cap: $137b

PE: 34.8

We last wrote about JD back in July when the share price was at $70, and the stock has done pretty well since (compared to the other China tech stocks).

Cathie Wood is a big fan, and she added to her JD position after their recent earnings.

Basically – Alibaba’s loss, is JD’s gain.

Once the anti-competitive practices were taken away, the vendors went to list on every other platform including JD. Less growth for Alibaba, more growth for JD.

JD also owns:

- 65% of JD Logistics ($28.4b)

- 67% of JD Health ($31.5b)

- 100% of Sinolink Securities (5.9b)

- 43% of JD Technology (IPO failed, valued at about ($8.3b)

- Stakes in companies like Farfetch or Vipshop.

Conservatively, these add up to about $50 billion or so.

Almost 36% of the current market cap of $137b.

Like Alibaba, you could argue there is a significant macro headwind from the slowing growth in China, which affects consumer confidence and consequently retail spending.

I don’t disagree, but if you’re bullish on China long term, that could open up opportunities to accumulate.

Tencent

Market Cap: $570b

PE: 19.3

And finally, Tencent.

Like most other China tech stocks, Tencent is down 40% from highs.

For now, they still have dominant positions in many areas, including:

- Number 1 in gaming by users in China

- Number 1 in Video, News, Music and Literature

- Number 1 in mobile payment by MAU and DAU

- Number 2 cloud provider by revenue (number 1 is Alibaba)

And WeChat is still the de-facto app for getting anything done in China.

Look at those 1.26 billion monthly average users (MAU) for WeChat.

Tencent is being forced to open up the WeChat ecosystem to competitors though, which is a good thing in my books.

Always found it ridiculous I couldn’t share a Taobao link on WeChat.

It’s very clear that the path for competition in China going forward is for fair competition, and not dirty tricks like this.

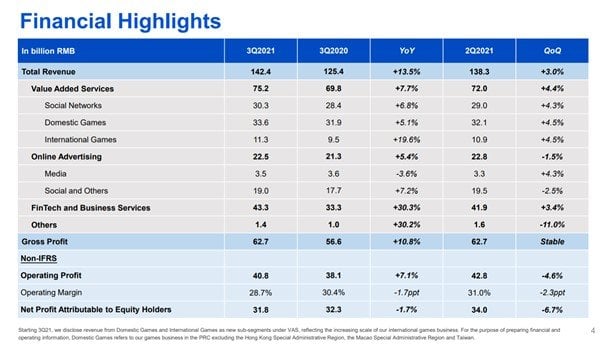

Like Alibaba, growth is no longer amazing, but still chugging along at 13.5% year on year.

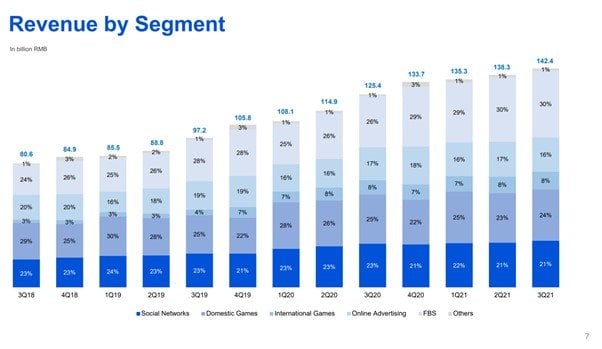

You can see revenue split below, broadly:

- 21% Social Networks

- 24% Domestic Gaming

- 8% International Gaming

- 16% Online Advertising

- 30% Fintech

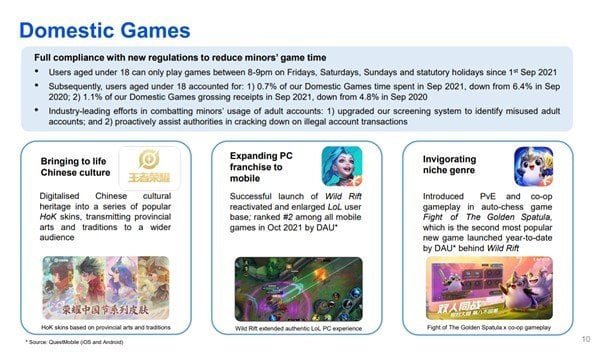

Gaming is 32% of Tencent’s revenue, so many people were very worried about the gaming crackdown.

Under 18 users can only play games between 8-9pm on Fridays, Saturdays, Sundays, and public holidays which is about as draconian as it gets.

According to Tencent – users under 18 account for only 0.7% of the users though, so they don’t anticipate a major impact on earnings.

0.7% looks way too low, I wonder how many of these kids are using their parent’s accounts to play.

Largest VC Portfolio in China

Tencent is one of the largest VC players in China.

Their VC portfolio is worth a whopping $146 billion today at market value, including:

- 20% stake in Meituan

- 100% in Riot Games

- 25% in Sea Ltd

- 18% in JD

- 9% in Pinduoduo.

This accounts for 25% of their current market cap.

You can see the full list here, I’ve extracted the top few below.

Honourable Mention

It’s been a very long post, but I really wanted to discuss a few other key names.

Meituan

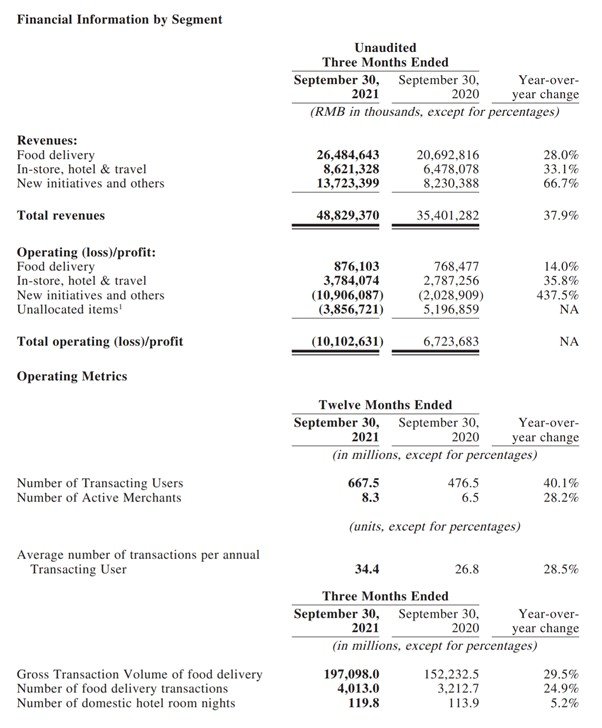

Meituan is a big one.

Recent earnings were a shocker.

Their sales and marketing expenses stayed roughly flat, but year on year growth for:

- Food Delivery dropped from 81% the previous quarter to 28%

- Hotel dropped from 98% the previous quarter to 33%

- Others dropped from 123% to 66%

You can argue some of that is due to base effects (Q2 2020 was a weak quarter), and also the COVID lockdowns, but that’s still a very drastic shift.

Long term growth should remain strong as both the Food Delivery and Hotel business have potential for growth, but the near term growth seems to be really impacted.

Reminds me a lot of the Dot Com Bust in 2000, when after the bubble burst all tech companies had their revenues hit regardless of how strong their business model was.

The fallout was just too widespread.

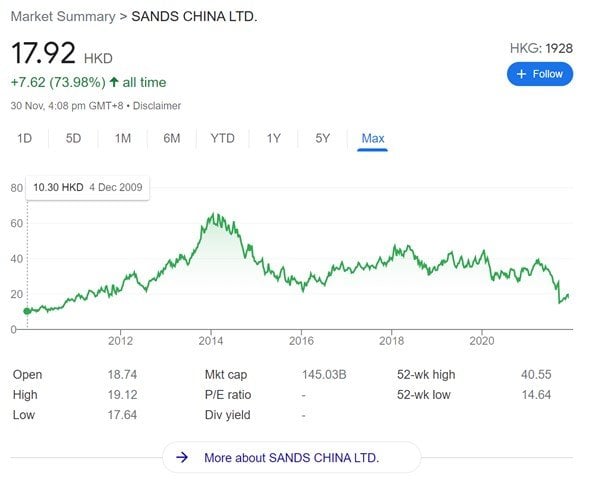

Macau Casino Stocks

Macau Casino stocks – you love them or you hate them.

Big names will include Sands China, Wynn Macau, MGM China.

Here’s the chart of Sands China to put things in perspective, down 70% from the all time high in 2014.

The crackdown on high rollers gambling in Macau has really crushed this sector.

I personally don’t have a strong view on Macau Casino stocks, but I know a lot of you love them.

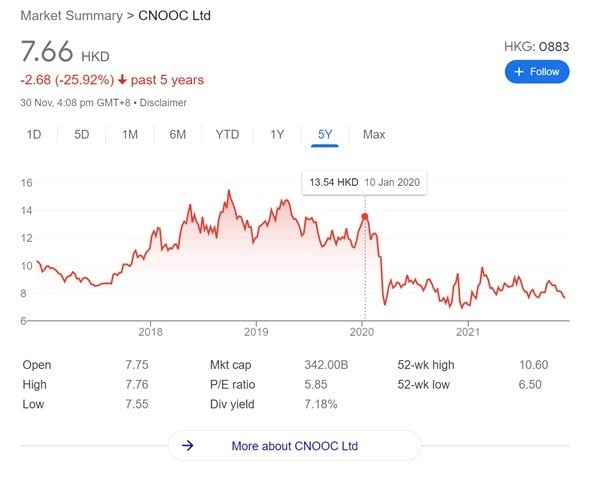

Oil Stocks – CNOOC

CNOOC is one of the 3 largest oil players in China.

And while Oil is back to pre-COVID prices, CNOOC is still down 45% from highs.

CNOOC has sanctions from the US, so that might explain some of the disparity.

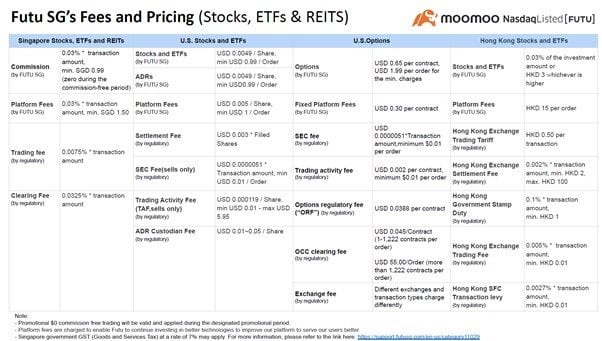

moomoo

moomoo powered by FUTU is a great low cost broker to buy HK listed stocks.

Competitive Fees at:

- Singapore: 0.03% (minimum 0.99) + Platform Fee of 0.03% (minimum $1.5)

- Hong Kong: 0.03% (minimum HKD 3) + Platform Fee of HKD 15

- US: 0.0049 per share (minimum of US$0.99 per order) + Platform Fee of USD 0.005 per share (minimum US$1)

You also get access to features such as:

- 100+ Drawing Tools and Indicators

- Heatmaps to identify top performing sectors at a glance

- Stock Screener

- 24/7 Financial News Coverage

- AI-Powered Analytical Tools

All collated in one place, which is pretty convenient.

Check out my review on moomoo here, and get 1 Apple share (worth ~$200) + $40 cashback* when you sign up and deposit $2700 or equivalent (USD/HKD).

Signup link here: moomoo Referral Code / Sign Up Bonus

Closing Thoughts: Has value emerged in China stocks?

We’re at a very interesting phase in global macro.

12 months ago China stocks were flying high.

12 months later they’ve been absolutely crushed, down 50% or so from highs.

US stocks are flying high now (less so after this week).

But going into a Fed Hiking Cycle, with rising inflation, will we see the same thing happen to US stocks? If things go bad for US stocks, they have a long way to fall.

All this horse knows is that sentiment is a contrarian indicator.

When everybody has turned away from China and towards US, that makes me very nervous about US, and very interested in China.

There are definitely macro risks on the horizon such as a regulatory crackdown and slowing China growth, as well as potential real estate contagion. Very tough to call the bottom on this one.

But prices have corrected very significantly from their highs, and so the question is at what point will they be a good buy again?

As always, this article is written on 1 Dec 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

As always, love to hear what you think!

*Terms and Conditions Apply

The content is provided for entertainment & informational use only. The information and data used are for purposes of illustration only. No content herein shall be considered an offer, solicitation or recommendation for the purchase or sale of securities, futures, or other investment products. All information and data, if any, are for reference only and past performance should not be viewed as an indicator of future results. It is not a guarantee for future results. Investments in stocks, options, ETFs, and other instruments are subject to risks, including possible loss of the amount invested. The value of investments may fluctuate and as a result, clients may lose the value of their investment. Please consult your financial adviser as to the suitability of any investment.

Great post again FH. Nice read on saturday morning. I personally prefer Tencent, because buying Tencent also means buying Meituan, Tesla, Sea Ltd., Gojek etc. Tencent is becoming a Berkshire Hathaway. Stable core business which gives good cashflows, allowing you to make investments around the world.

Haha that’s a very interesting way of seeing it, thanks for sharing the perspective.

I would think if US stock start to correct, will it pull another wave down for Chinese stocks. It is pretty much messy for those Chinese ADR, didi etc

Well the whole world is so correlated today. US stocks correcting will pull down almost every asset class in the world.

Hi FH, Chinese EV makers seem to be immune to the current market turmoil. Perhaps you can do a piece on them.

Actually I meant to cover EVs in this article too but missed it out due to the length of the article. Will see if I can include in the next China article.

Another mention may be Fosun (vested). Fosun is involved in China healthcare, China leisure/tourism. It’s a play on China aging population and growing economy. It’s at 0.5 P/B but it’s dividend yield is low and it has conglomerate discount.

China banks have been carrying the discount for years due to investor’s worries on them being a black box. It is uncertain when such discount will be lifted. And some China banks may issue shares to shore up their equity. Rather than China banks, I prefer Ping An (vested) in China financials space. Nonetheless, Ping An has lower dividend yield than ICBC.

Interesting, thanks for raising this. Will have a look at Fosun.

Yes I meant to include Ping An together with the 4 banks too, as they are a broadly similar play to me. Have updated the article. 🙂

I think you have not done enough homework la, go read the list of regulations and anti-competition measures the Chinese government is planning to put in place in the months to come then you see whether how much it is going to affect those tech and bank counters in your recommendations.

Haha I suppose the question back to you is that knowing what you know today – what price would you buy these stocks? Or what needs to change before you will buy them? Or will you not buy them no matter what happens in the future?

Hi FH, thanks for the insight.

For some of these China stocks that are listed dually in the US, I think some fear is due to potential delisting concerns in the US. Just wondering what your take is on this scenario?

Also wondering what your take is on the scenario that these stocks could potentially be privatized if (since) stocks prices keep falling?

Quite a few questions on this, will see if I can do a full post. 🙂

Long and short is that it depends on the mechanics, either they (1) buy out close to IPO price to avoid lawsuits or (2) option to swap to the HKD counter.

Option 1 is a good arbitrage opportunity, Option 2 not so much as not all the US based investors are allowed to hold HK counters due to investment mandate. Can kind of see why the stock sold off – question now is whether there is an arbitrage play here.

Hi FH,

Thanks for the great post.

If these China companies, for example, BABA, is forced to delist from the US, will it hit the share price very badly?

Due to Hedge funds or many other fund houses having to sell the shares as they no longer fulfilled certain conditions etc?

Many thanks

Quite a few questions on this, will see if I can do a full post. ????

Long and short is that it depends on the mechanics, either they (1) buy out close to IPO price to avoid lawsuits or (2) option to swap to the HKD counter.

Option 1 is a good arbitrage opportunity, Option 2 not so much as not all the US based investors are allowed to hold HK counters due to investment mandate.

Hello ! Thanks for Your article !

If a certain company has a Dual listing, where is it preferable to buy – in Hong Kong or Mainland China? I use Tiger Brokers.

For me I usually go with Hong Kong.

Mainland has higher valuations though, due to capital controls and local population being unable to buy the HK listed shares. Really depends on what you want.

Thank You . I’m looking for greater reliability, and I want to avoid in the future possible delisting (as in the USA)

Yeah HK might be the better bet in that case.