Aaaaand… the China tech stock sell-off continues.

What started out as a clampdown on Didi’s IPO, has evolved into a broader clampdown on China tech companies listing overseas.

Triggering a broader sell-off across China Tech stock.

Is this a buying opportunity? Which counters to buy?

Let’s find out.

BTW – we share commentary on financial markets every week, so do sign up for our mailing list, its absolutely free (goes out every Sunday).

Don’t forget to join our Telegram Channel and Instagram or (YouTube)!

[mc4wp_form id=”173″]

Basics: Why is China clamping down on Tech stocks?

Timeline of what’s happened so far:

- Wed 30 June – Didi IPO-ed in US, closing up 1%

- Friday 2 July – China’s cyberspace agency (CAC) launches an investigation into Didi, citing concerns over storage of user data. Shares fall more than 10% intraday

- Sunday 4 July – CAC orders that Didi be removed from Chinese App stores

- Monday 5 July – CAC also launches investigations in Boss Zhipin, Yunmanman and Huochebang (listed in US)

- Tuesday 6 July – Didi plunges 25% intraday

- Wednesday 7 July – WSJ Article, and rumours out of China suggest that this is part of a broader movement to stop China tech from listing in the US. There are suggestions that the VIE structure “loophole” may be closed

What is the VIE structure? Why does it matter for China Tech Stocks?

A bit of background.

Under China law foreigners are not allowed to own internet companies in China, because of national security reasons.

But of course, Alibaba, Pinduoduo, Didi etc are all listed in the US, so clearly this rule has not been followed.

And the reason why is because of the Variable Interest Entity (VIE) Structure.

The actual legal structure is quite complex, but the crux is that investors are able to own economic interest in the company, without actually owning legal ownership.

Think of it like a derivative – you can buy a derivative that will pay you if DBS shares go up, but legally you’re not a shareholder and don’t need to declare it.

Almost every single China tech company listed overseas today relies on the VIE structure.

The fact that China wants to relook the VIE structure, is actually really, really big news. I wouldn’t underestimate the importance of this one.

Short term, I don’t think any China tech is going to list in the US for a while, and we’re already seeing Tencent backed Keep and Ximalaya pull their IPOs.

What is the CCP’s endgame for China?

It’s never easy to read the CCP (China Communist Party).

These guys operate on a different level from the Americans, and their timeframe is also very different.

Possible reasons for the clampdown include:

- Teaching Didi a lesson to IPO in US right before the CCP’s 100th Anniversary

- Send a signal to the US

- Safeguard China user data

- Reign in China tech

- Discourage China tech from listing in US

Your guess is as good as mine here.

Personal view – I think it’s a mix of all, with particular emphasis on points 3 – 5.

I think it’s part of a broader move to regulate China tech more heavily, and to send a signal to use HK capital markets instead of US.

If I am right, then the days of freewheeling China tech are over. And we’re moving into a phase where tech is more closely regulated in China, which will hit margins and growth.

Is China tech a good buy now?

That said, I still see Tech as one of the best ways to bet on China’s long-term growth.

China starts out without the infrastructure of the West, so they are free to build whole new systems from the ground up.

So the equivalent of Visa in China is Alipay, and the equivalent of Disney is Tencent.

Just look at the MSCI China – and a big component of the index is Tencent, Alibaba, and Meituan.

The short term will be choppy though, so averaging in makes sense.

Top 5 China Tech Stocks to buy now – For Singapore Investors (2021)

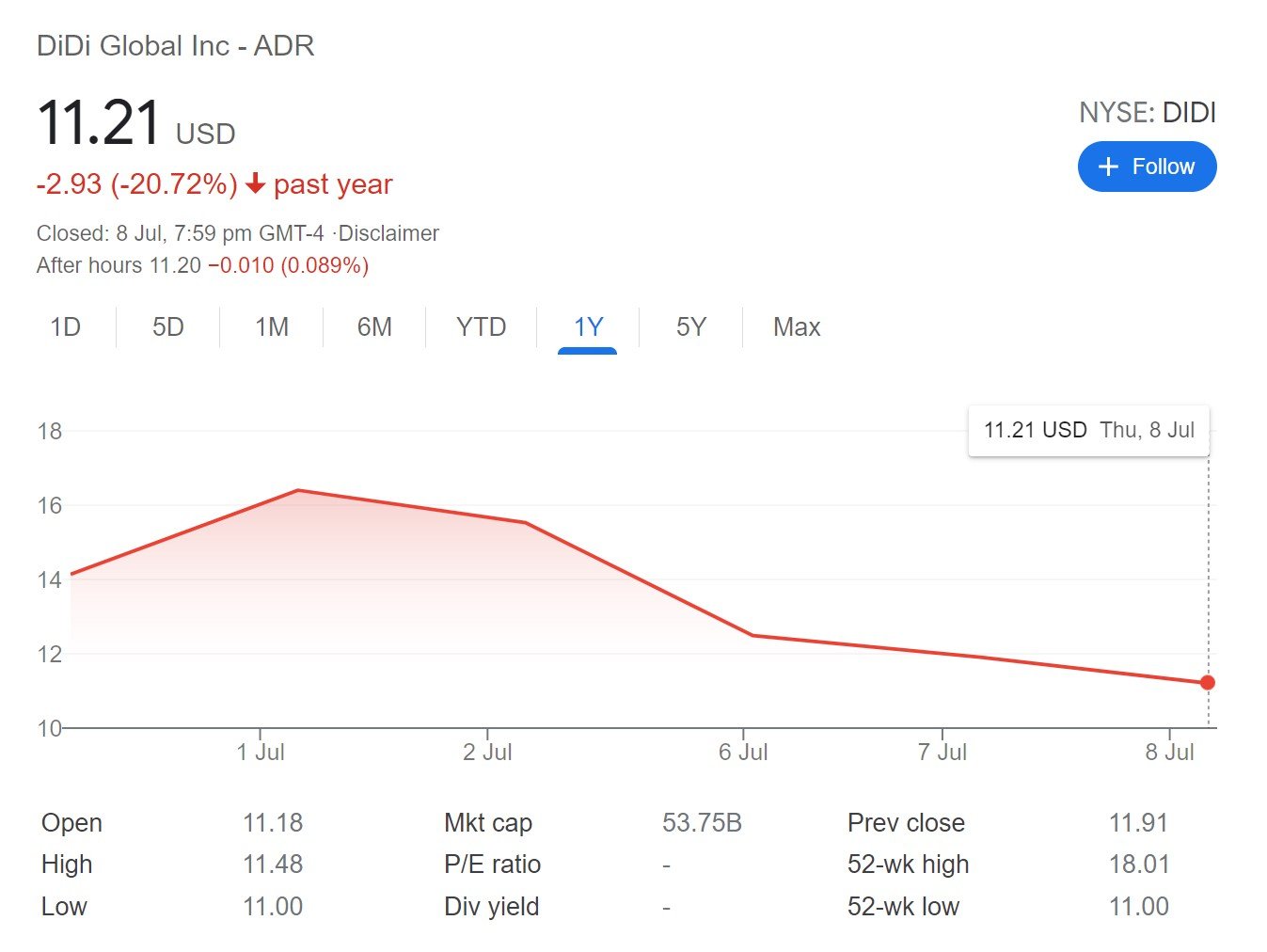

Didi (NYSE: DIDI)

Market Cap: $57b

Price/Sales: 2.4

Price/Earnings: NA (loss making)

Of course the star of the show – Didi.

Basically the Uber/Grab of China.

The rumour is that Didi knew about the clampdown coming, but chose to go ahead with the IPO anyway.

I can see why they did though, because if they miss this opportunity, the next chance could be years away (just look at Ant Financial).

I penned an article for Patrons earlier this week on Didi, so do sign up for more premium content like that.

Didi is a tricky stock because:

- Core ride hailing business is still losing money – Unlike Grab and Uber which have expanded into food delivery, Didi can’t because food delivery is dominated by Meituan. It turns out it’s not easy to make money from the ride hailing business, and it’s hard to say if this will change

- Bulk of business is still domestic… for now – 95% of revenues come from China. The rest is from Latam and Africa, but for now Didi is still a very China centric company. That’s both good and bad.

Our very own Temasek is a shareholder though, and has been joining the financing rounds since 2015.

My view is with Temasek on this one.

I think with Didi’s monopoly position in China ride hailing, it makes sense to allocate some capital there.

I don’t know if Didi will ever be profitable, but with their market share, I don’t want to bet against them.

I can’t rule out the possibility that one day they’ll be able to raise prices, or find a new product vertical to monetise. Or maybe the China Elon Musk will perfect self-driving, and Didi turns profitable overnight.

Don’t forget that Grab is listing at a $40b market cap, and the South East Asia market is so much smaller than China (in terms of purchasing power).

The fact that you get a monopoly player in China, at a valuation only 50% higher than Grab, looks pretty good risk-reward to me.

The short term looks very volatile though, so it’s definitely a stock I would average into.

Tencent Holdings (HKG: 0700)

Market Cap: $650b

Price/Sales: 7.4

Price/Earnings: 22.4

The last time I bought Tencent was at $500, about a year ago.

Since then, it’s gone to $750, and roundtripped all the way back to $510.

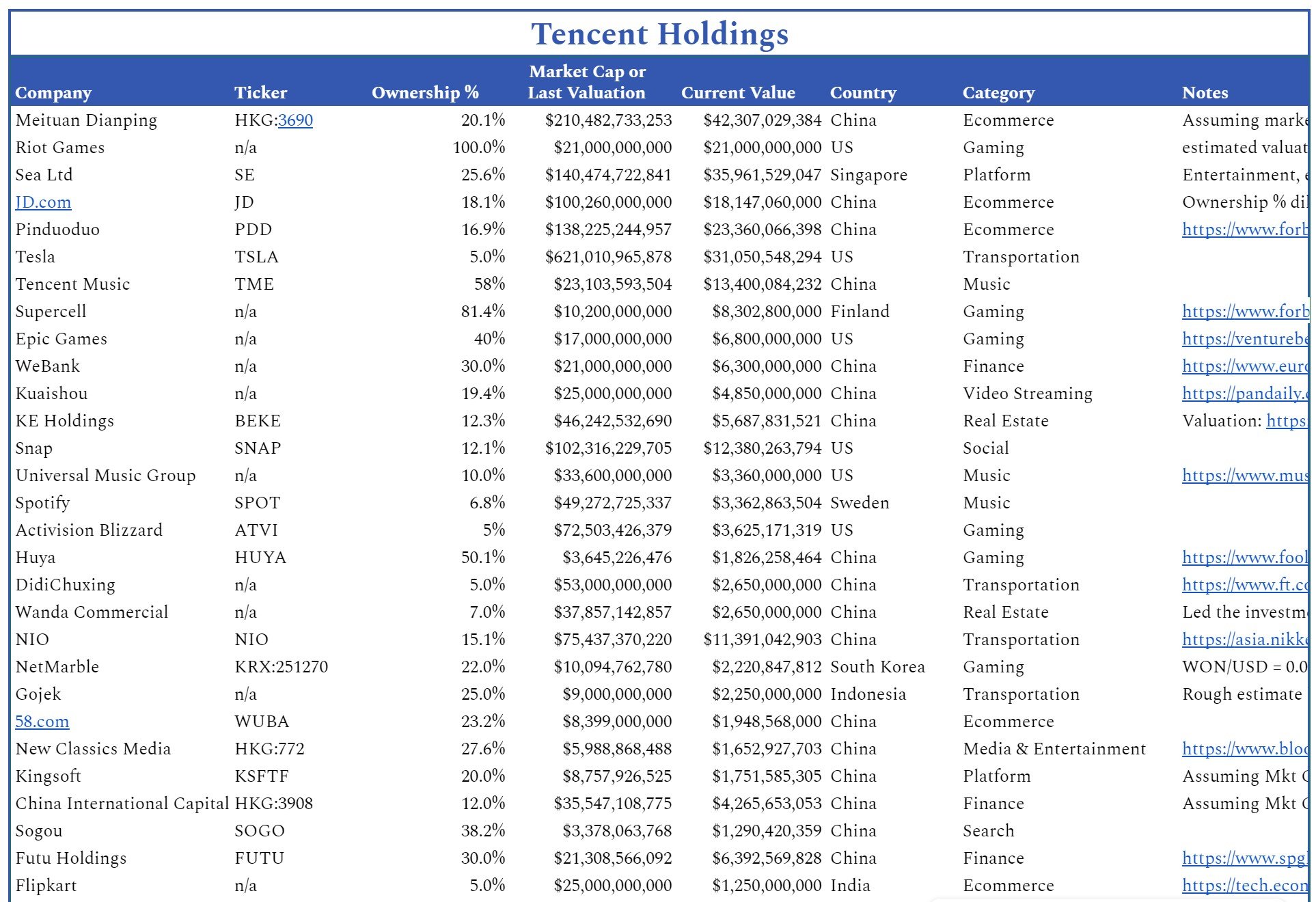

What you get with Tencent, is (1) the WeChat ecosystem, (2) gaming company, and (3) VC Fund.

(3) is an often overlooked part of Tencent.

In fact, Tencent is one of the largest VC Funds in China.

Just look at their list of top 10 holdings. It puts big names like Sequoia to shame.

A fellow blogger has tabulated a full list of Tencent’s holdings, and I’ve extracted the biggest ones below.

At today’s value, this adds up to more than $300 billion, which is almost half of Tencent’s market cap.

It’s hard to describe the absolute dominance of Wechat if you’ve never lived in China.

In Singapore we live our lives around a desktop/laptop, with email as the primary means of work communication.

In China your live revolves around your mobile, Wechat is the main mode of work communication, and your desktop/laptop is an addon to your mobile.

It’s just a fundamental shift in thinking.

Of all the tech players, Pony Ma’s Tencent has been the most willing to play ball with the CCP, so I do see them continuing to survive for years to come.

At $650 billion market cap, don’t expect this stock to double overnight. We’re reaching a stage where the big FAANG names have become value plays rather than growth plays.

But for long term patient capital, I think current prices look interesting.

Meituan (HKG: 3690)

Market Cap: $210b

Price/Sales: 10.0 Price/Sales

Price/Earnings: 244

I have no shame in admitting I missed the Meituan and Pinduoduo boat back in 2019.

Back then, I underestimated the explosive growth of network effects, and the speed at which it would happen.

The trick is that once Meituan sealed their dominance in food delivery, they pivoted that customer attention to other product verticals like movie tickets, train tickets, hotel bookings etc.

Creating a legitimate super-app competitor to take on Alipay and Wechat.

It’s a very impressive feat, and their management team has demonstrated some incredible tenacity and execution to get to where they are today.

In fact it reminds of another management team – SEA with their strong execution in SEA across gaming, ecommerce and payments.

Valuations are nosebleed high though, and I’ve been waiting for a meaningful pullback.

Let’s see what we get.

JD.com (NASDAQ: JD)

Market Cap: 110b

Price/Sales: 0.9

Price/Earnings: 14.06

JD has evolved into a very interesting value play.

It’s not a small player in eCommerce, with about 20% market share mainly concentrated in the more affluent Tier 1 cities.

But JD also owns:

- 65% of JD Logistics ($28.4b)

- 67% of JD Health ($31.5b)

- 100% of Sinolink Securities (5.9b)

- 43% of JD Technology (IPO failed, valued at about ($8.3b)

- Stakes in companies like Farfetch or Vipshop.

Conservatively, these add up to about $60 billion or so. Almost 50% of the current market cap of $112b.

The other alternative would be Pinduoduo at a $138b market cap, but with a lot more growth.

Really depends on individual risk appetite.

Kuaishou (HKG: 1024)

Market Cap: $85b

Price/Sales: 10.5

Price/Earnings: Not Meaningful (loss-making)

For this last one I wanted to go with a bit of a wildcard.

Kuaishou is basically the poor man’s version of Douyin (Douyin is the China version of Tik Tok).

Whereas Bytedance’s Douyin caters towards the more affluent Tier 1 cities, Kuaishou is popular amongst the migrant workers outside of the affluent Tier 1 cities.

If you want a mental picture – think of the migrant worker working in a Tier 2 city as a kuaidi delivery man, thousands of miles away from home, watching a girl streamer and buying gifts for her.

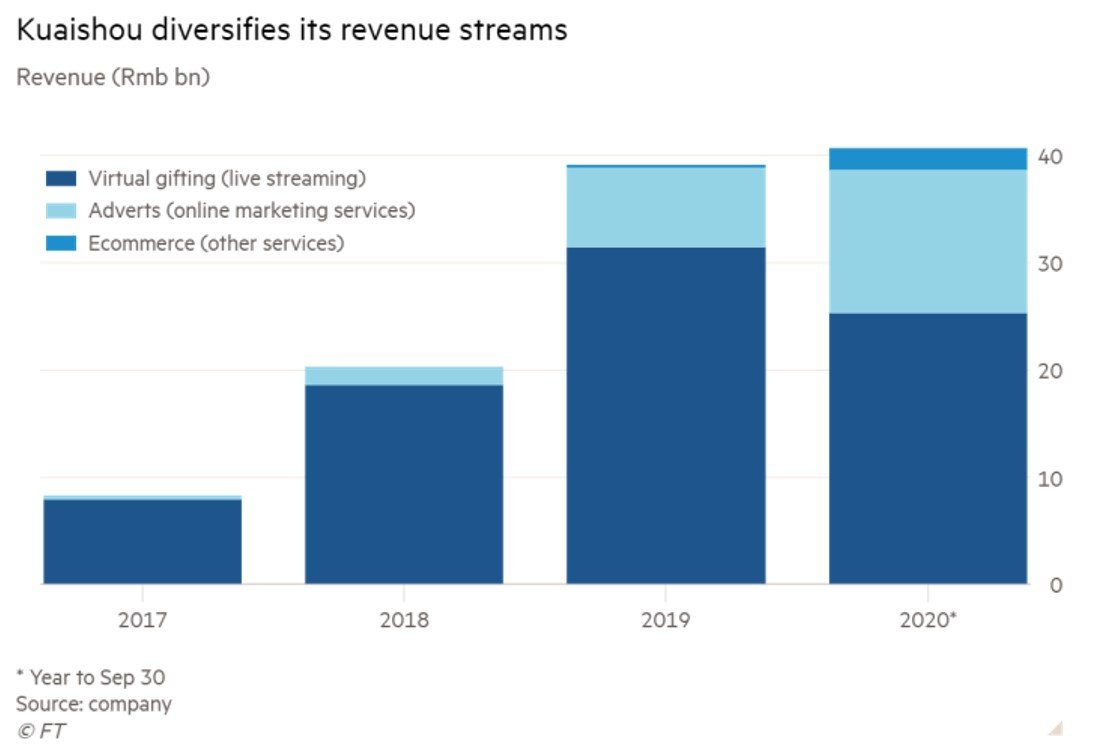

That used to be the core business model for a while, but Kuaishou is definitely taking steps to diversify revenue streams:

The key to me is whether Kuaishou can continue to diversify, and build into a legitimate competitor to Douyin among the less affluent. Or will Bytedance eventually come to crush Kuaishou with its superior technology.

Share price at $156 has plunged more than 50% from its post IPO high of $400.

It’s still not cheap by any means ($85b market cap vs Bilibili at $30b), but at a certain price it could be an interesting pick up.

Honourable Mention – Other China Stocks to buy in 2021

Big honourable mention to the stocks below, that should probably have made it onto the list, but didn’t for some reason or other.

Alibaba

I like Alibaba at this price, and I’ve been accumulating since the Ant Financial IPO got pulled late last year.

I think their dominant position in Ecommerce and Payments will be very valuable in time to come, once the current regulatory scrutiny blows over.

Main reason why Alibaba didn’t make it onto the list is because they already sold off before the Didi saga, so comparatively they’re not all that attractive now.

Tencent Music

Tencent Music I’ve also been accumulating for a while. You can check out my thesis for Tencent Music here.

Didn’t make it onto the list for the same reasons as Alibaba.

Ping An Good Doctor / JD Health

Healthcare in China is a very interesting play. I think in the decade to come, growth in this sector is going to be massive.

But it’s very hard to know which will be the winners.

I have a small amount in Ping An Good Doctor and JD Health, but these are more speculative plays. I don’t think we’re quite at that inflection point for hyper growth in healthcare yet.

Nongfu Spring

Basically the Coca-Cola of China.

It’s not a tech stock, but it trades like one, with a 66 times Price/Earnings.

Like many other stocks on this list, it’s down almost 50% from it’s post IPO highs.

I really like this stock, but I want to be greedy and try for a better price to open.

If we’re going into a more inflationary world, boring old-world businesses like this that generate a ton of cash flow is what I want to own.

China Banks / Insurers

And possibly the most controversial of all – Banks/Insurers.

You know, stocks like ICBC, CCB, Ping An etc.

You either love it or you hate it, and I won’t belabour this point.

If you love it, you get a 6% dividend, 50% discount to book value (or more), and solid backing from the CCP.

If you hate it, then you think the books are a total joke, and that they will be forced to make loans that cannot be repaid for national reasons.

Both point of views are equally correct. It all depends on your perspective.

Closing Thoughts – China Tech Stocks a buy?

Full Disclosure – I have positions in most of the stocks above.

In fact I just bought a bunch of China stocks the past week, with plans to continue averaging in over the next few weeks/months.

If you’re interested, you can check out my full portfolio and watchlist on Patron. I update it weekly for stocks I buy and sell.

I think that while the regulatory framework will tighten, there remains years of growth ahead for China tech.

And to me at least, China stocks is one of the key pillars of my investing portfolio going forward (together with US stocks and Singapore dividend plays – full portfolio here).

The PBOC has been pretty stingy with liquidity in 2021, which has contributed to a weak China stock market.

Going into second half of 2021, I think that will start to change, just as the US Feds start to withdraw liquidity. Which could mark a very interesting shift in market leadership.

But what do I know, I’m just a talking horse.

Love to hear what you think! What are your favourite China tech stocks after the sell-off?

As always, this article is written on 9 July 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Hi FH, as always great analysis. One question – why would a HK listing of these Chinese not attract attention from the US tech funds, assuming they are forced to delist?

Thanks Amit!

Not sure if I understand your question right. The way I see it global capital is just so mobile today. If Bytedance chooses to list in HK only instead of the US, all the top fund managers will still come to HK to buy the shares anyway. And if they don’t or can’t, investors will just find a fund manager who can.

So longer term the implications should not be severe, capital will just go to whereever is the most attractive and offers the best returns.

Is this a typo – “Discourage China tech from listing in China”?

Great article btw. 🙂

Sorry yeah I meant to say discourage China tech stocks from listing overseas, esp in the US given the broader geopolitical context.

Thanks for the spot, and glad you like it. 🙂

Really appreciate the summary at the beginning of the article.

Had been trying to make head and tails about this new saga the whole of this week.

Would this also make sense?

Listing in China/HK, hence usually in China currencies versus in US exchanges which are denominated in USD, also gives the CCP more control/power of things? Since it’s their currency, and they can control the taps.

(It’s a bit vague as I’m not conversant in this topic, so just painting my fuzzy idea to check if it make sense. Maybe you can fill in the blanks of my rudimentary sketch)

Thanks – glad you found it useful!

Yes – that’s all part of the appeal of moving to HK instead. Rumour is that China is not pleased that all these tech companies, with their years of growth ahead of them, are choosing to use US capital markets and enrich the US financial system instead of the domestic one.

With HK – the domestic financial system will benefit (bankers, lawyers, accountants etc), and HK rule of law + currency is under Beijing’s control. So it appears this is going to be the broader direction going forward.

Any hypothesis on how existing VIEs listed in the US will be handled eg the likes of Alibaba, JD etc that have primary listings in the US?

Thanks.

My best guess for now is that there will be an “approval process” for all new VIEs going forward, while existing VIEs are gently “encouraged” to shift back to HK over time.

Hi FH, by the way, what do u think of china tech ETFs, instead of buying individual china stocks ? China tech ETFS, like the 3067 Ishares china tech etf … ??

Yeah perfectly fine as an alternative to stock picking. 🙂

So the investment method is via the US market for those looking to have some exposure in the China market ?

Well some would argue US shares have extra geopolitical risk, so if that really bothers you then go for the HK shares instead.

Hi, I have been reading your interesting articles.

This `Top 5 China Tech Stocks to Buy – for Singapore Investors (2021)’ is very interesting esp on Tencent.

But I am surprise that Biadu is not on your list. Are there some reasons?

Thanks, glad you found it useful!

Baidu is an interesting one. Very cheap stock, but also very hard to see where the future growth will come from. The core search business is not doing well because their search algo is very poor compared to Google, and much of Chinese content is behind walled ecosystems that cannot be crawled easily (eg. WeChat, Taobao etc).

They are investing heavily into AI and self-driving, but for now it remains to be seen if those will reap any rewards.

It’s an interesting stock, but I didn’t open any position for the reasons above.

Thanks for the this, FH! Very useful! Quick question: do you recommend convert Alibaba US stock to HK ones? Thanks!

Personally I hold the US stock, and I don’t see it as a big issue.

But not everyone would agree with me on this. I would say if it bothers you, then just hold the HK stock instead. Very little inconvenience, but potentially saves you a lot of pain and hassle if something does indeed go wrong with the US listing.