A lot of you have been asking for my views on the Singapore residential market in 2021 / 2022.

In the midst of COVID, weak economy, job insecurity – yet HDB resales are going for a million a pop, and condos are making new highs every week.

What gives?

So I wanted to pen this article to share my views – and also the fact that I bought a second condo in Singapore in 2021.

I will share my personal experience and thought process, and hopefully it will be useful for you in your decision making.

This is a modified version of the article that first appeared on Patreon. If you enjoy articles like this, do support FH as a Patron and receive exclusive content, my personal stock watch and personal portfolio!

What Singapore Residential Property did I Buy in 2021?

Before this I already owned a leasehold condo.

In 2021, I went ahead and bought a freehold condo.

How did I buy another property in Singapore in 2021?

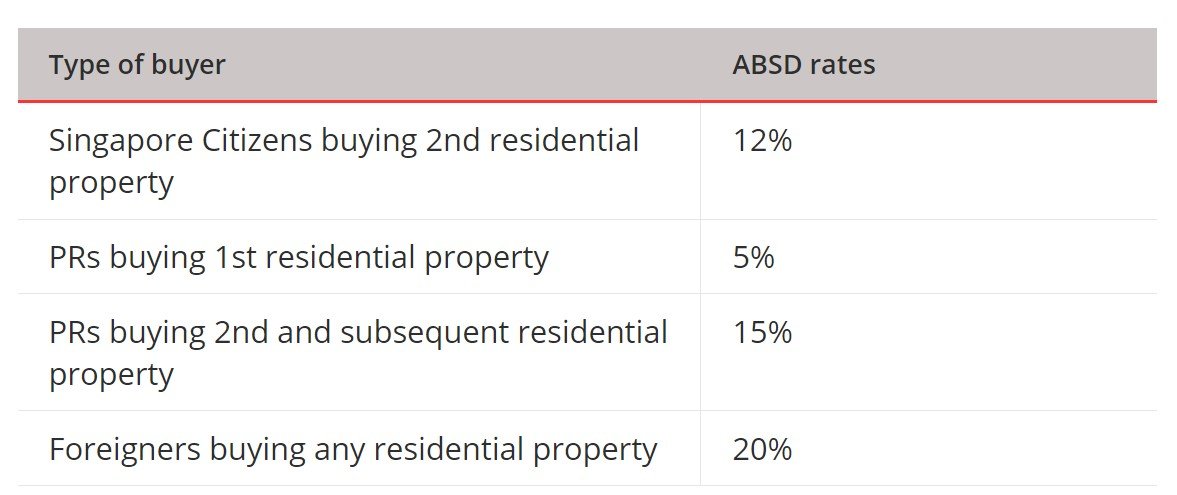

To avoid Additional Buyer’s Stamp Duty (ABSD), I had to “decouple” my existing property.

Very simply – I sold my stake in the property to my spouse, freeing up my name to buy another property.

Fees wise, I had to pay (1) legal fees (about $5k plus), and (2) buyers stamp duty (on the 50% stake I was selling).

Sidenote: Property investing is a much poorer investment if it’s a second property, because it significantly affects the loan you can take (45% for second home vs 75% for first), and ABSD is a gamechanger. 12% on a 3 million property is $360,000 (payable in cash), which really affects buy price.

General Observations on the Singapore Residential Property Market (from personal experience)

I’ll keep this discussion to the private residential market, but many of these comments are applicable to BTO/Resale as well:

- Rental Market is very strong now

- Supply chain disruptions are really bad – Construction costs have gone up materially

- Structural demand-supply mismatch

- Sellers are asking sky high prices, buyers are not willing to match

- Low interest rates are a very powerful tailwind

Rental Market is very strong now

The rental market is very strong now.

Anecdotally, I’m seeing 10% – 20% rental increases just compared to late 2020.

It’s hard to pinpoint the exact factors, but I would say it’s a mix of:

- Singaporeans moving out of their house and renting

- the usual foreigners who need a place to stay

For (1), because of COVID and work from home, many Singaporeans decided to move out to rent a place. This created additional demand that wasn’t there before.

The impact of (2) came down slightly the last few months as the government tightened entry restrictions due to COVID’s delta variant. But going forward, it should start to pick up again as Singapore continues to reopen to the world.

As a landlord, it’s very easy to rent out a house now, with a decent increase in rent.

Supply chain disruptions are really bad – Construction costs have gone up materially

The cost of building materials has gone up, and the cost of labour has gone up.

This has impacted construction costs in a big way.

For labour – think about all the migrant workers who now need to be tested for COVID regularly, and need special accommodation. And all the migrant workers who can’t enter Singapore. There is, and I kid you not, a bidding war for blue collar workers right now.

Somebody needs to pay for that cost.

For now, developers are absorbing the higher costs, but at some point they will want to pass it on to buyers. With the recent Pasir Ris 8 launch, many developers seized that opportunity to raise prices across the board.

Structural demand-supply mismatch

There is a structural imbalance in the market currently. Supply cannot keep up with demand.

Supply of new properties (both private and BTO) has been delayed drastically because of COVID’s impact on migrant workers, which delayed construction anywhere from 6 – 12 months.

Just this week it was announced that another 5 BTO projects are delayed because the main contractor is bankrupt. Can’t really blame them, because these contractors are locked into pre-COVID prices, and paying post-COVID prices.

Imagine if you’re locked into a fixed priced contract with 10% margins, and your cost of materials/labour went up 20% across the board.

To continue on the construction project would be a loss maker for them, so bankruptcy is a fair decision. All across Singapore (and the world), many contractors are facing this exact problem.

Meanwhile, demand has gone up due to COVID. A year of work from home has made people realise the importance of their home, and they all want a nicer home + more space.

Throw in HDB upgraders and new couples, and the supply can’t keep up with demand, creating a structural mismatch.

Sellers are asking sky high prices, buyers are not willing to match

Because of supply delays, for homeowners who want to want to move in quickly, resale is the best option.

At the same time – for sellers with an investment property, the rental market is very strong, creating very little pressure to sell.

Most sellers also understand there is a demand-supply mismatch, so they are in no hurry to sell, believing that if they hold the property they can get a better price down the road.

This creates a situation where most sellers are asking for a price 10-20% above last done, which most buyers balk at (understandably).

For now, the impasse is yet to be resolved, so the price index hasn’t moved conclusively either way.

Low interest rates are a very powerful tailwind

Take me for example.

I eventually settled on a 1.05% mortgage, fixed for 2 years.

1.05%. To borrow millions of dollars. For a 30 year mortgage.

That’s just ridiculous to me, and I’ll borrow as much as the bank would give me at these rates.

As comparison – the last time I repriced was 2018, 1.85% for a 3 year loan.

The difference is really big, and we really shouldn’t underestimate the impact of low interest rates on property prices.

Will there be cooling measures for the Singapore residential property market in 2021 / 2022?

A lot of commentators are talking about cooling measures.

I definitely could be wrong here, but my personal view is that cooling measures are unlikely in 2021.

The thing with cooling measures is that they work to cool an overheated market. If people are FOMO-ing into the market, or if developers are going crazy with enbloc bids, then cooling measures help.

Think 2007/2011 (FOMO), and think 2018 (en-bloc fever).

This time around, the problem is structural in nature. Supply cannot keep up with demand.

In a market like this, I’m not sure if cooling measures work. It’s very hard to tailor the cooling measures to only hit the speculators, and not the people who genuinely need a home.

All cooling measures will do is deprive certain people from buying a house, and I’m not sure if that is the right decision here.

Could be wrong though.

BTW – we share commentary on Singapore Investments every week, so do sign up for our mailing list.

Don’t forget to join our Telegram Channel and Instagram (or our Reddit Community)!

[mc4wp_form id=”173″]

Will Singapore residential house prices go up in 2021 / 2022?

Singapore house prices have held up amazingly well all throughout COVID.

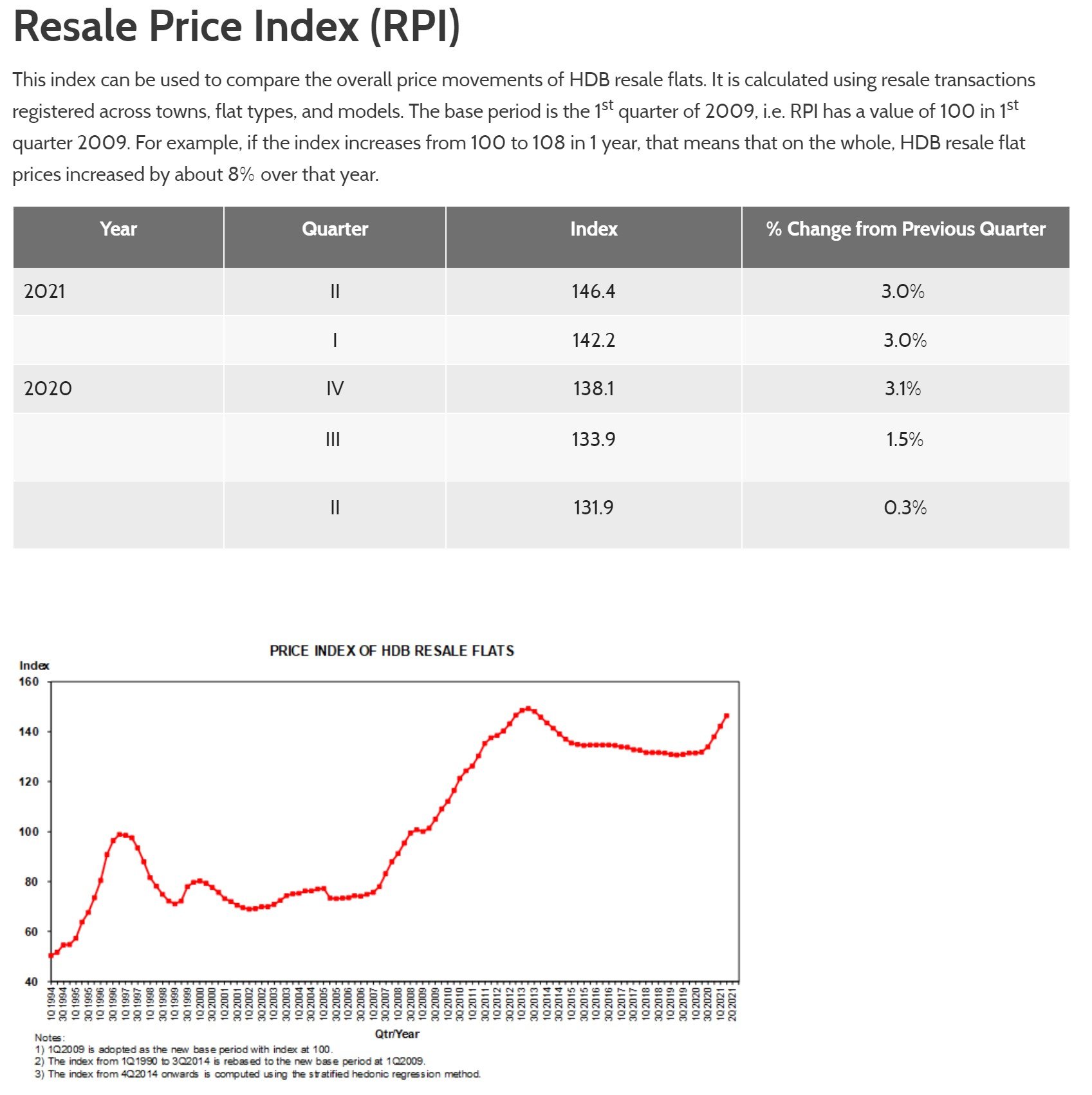

HDB Resale Prices

After some initial weakness in Q2 2020, HDB resale prices have been very strong since, up 3.0% each quarter in 2021.

Source: https://www.hdb.gov.sg/residential/buying-a-flat/resale/getting-started/resale-statistics

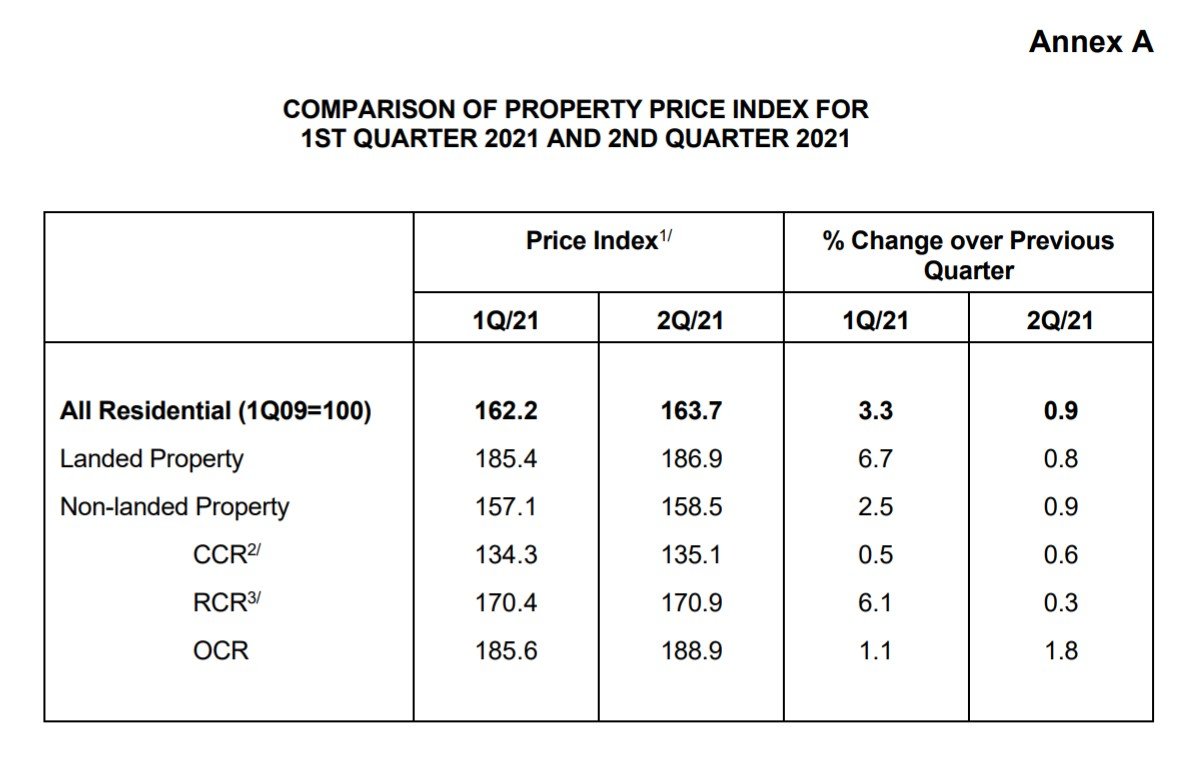

Private Residential Properties

In Q1 2021, Landed properties increased 6.7%, while condos increased 2.5%.

Both of which moderated in Q2 2021 when the Phase 2 Heightened measures kicked in.

The big increase in landed is interesting – it seems families are really prioritizing space.

Source: https://www.ura.gov.sg/-/media/Corporate/Media-Room/2021/Jul/pr21-23b.pdf?la=en

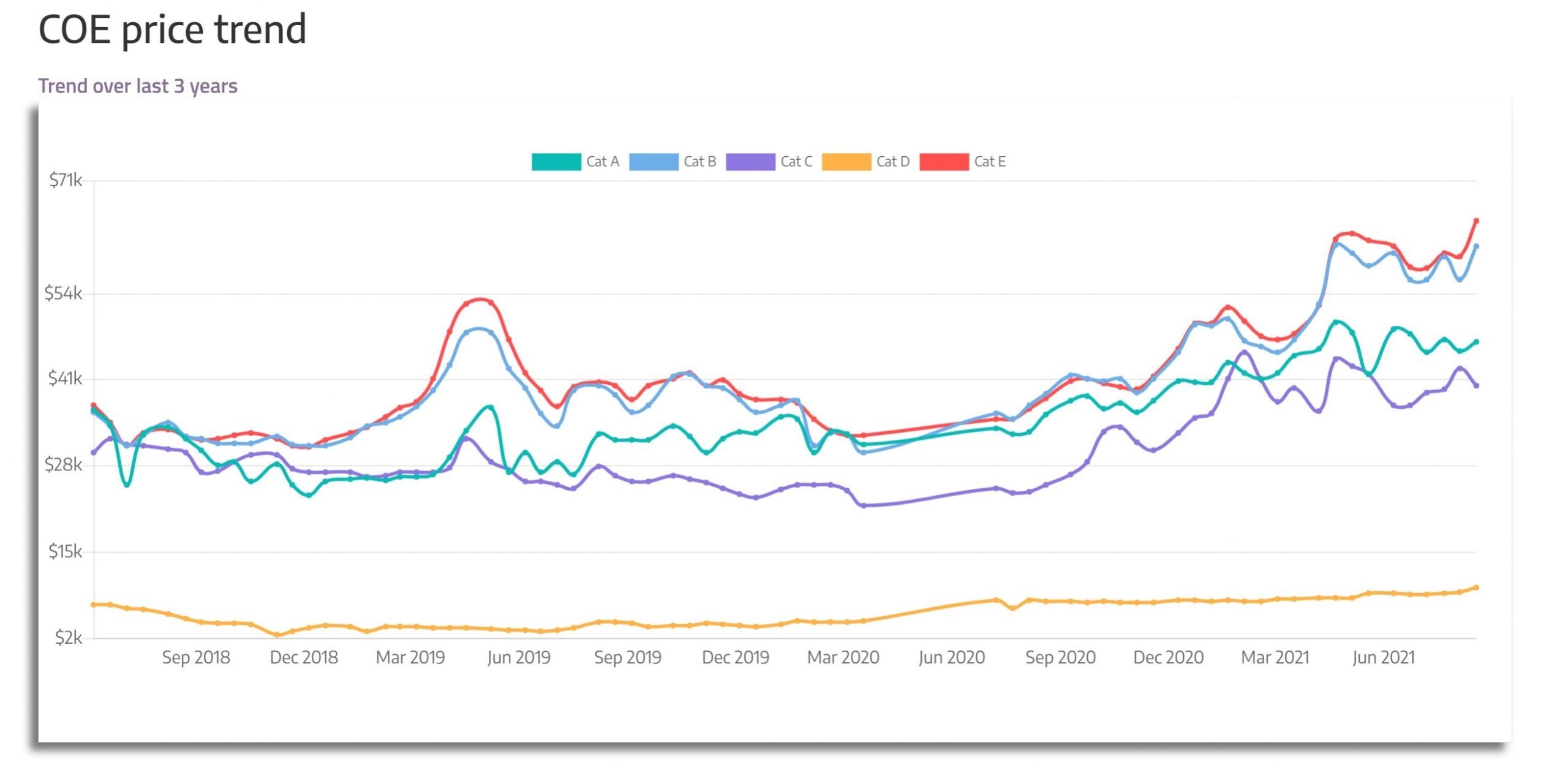

What are COE Prices telling us?

COE prices are a proxy to house prices – offering clues as to how house prices will trade.

And COE prices have generally been very strong so far, backing up the house data.

Source: https://arcade.sg/arcade/coe/index

My 2020 call on Singapore property prices was absolutely wrong

In 2020, I wrote an article saying that property prices may go down in 2021. My thinking was that demand would go down, and supply would continue to go up.

As it turns out – the call was absolutely wrong.

Demand was stronger than ever because the government stimulus preserved a lot of jobs, and work from home meant people treasured their space. While supply was devastated by the impact from COVID on migrant workers.

That just illustrates the difficulty of making predictions in this COVID environment.

So this time around, no predictions as to property prices from me.

Why did I buy another residential property in Singapore (2021)?

That said, I will share my though process behind buying another property, and you can decide if it works for you.

- Time in the market

- Low Interest Rates

- Potential Inflation Hedge

- Earn the rent

Time in the market

Time in the market, vs timing the market.

Fast forward 5 – 10 years, and I think most of us would agree that house prices in Singapore are going to be higher than where they are today.

The Singapore government controls supply carefully, so the chances of an oversupply are not high. As long as economic growth keeps up, and Singapore continues to be a hub for South East Asia, property prices should trend upwards at GDP growth rates longer term (2-3%).

So the question then is whether to buy now, or wait for a better entry price.

As investors – we’re very familiar with such decisions.

Do you buy the S&P500 at all-time highs, or do you wait for a pullback which could come 6 – 12 months later (or not).

Time in the market vs timing the market.

Low Interest Rates

Low interest rates really shouldn’t be underestimated.

With 75% leverage at 1% interest rates, that turns a nominal return of 2-3% on the house, to about 7% return on the equity you put in.

Potential Inflation Hedge

Taking up a big loan is also a way to hedge against inflation going forward.

If there is indeed inflation, house prices go up, but the loan amount stays the same – further juicing returns.

Earn the Rent

The options for me were to (1) live in my existing property or (2) buy a new property and rent out the existing.

I already had the cash set aside for a property, so I decided not to time the market and go with (2).

As long as the market doesn’t crash, I’m already earning the rental yield from the other property every month.

My other property has about a 3.5% yield now (rentals have gone up quite strongly), which means that for every year I rent it out I’m getting about 3% of the purchase price back (after costs). Let it run for 3 years and that’s almost 10% of the purchase price in rent.

Macro Views from a Horse

Okay so this is Financial Horse, so despite my better judgment I’m still going to share macro views.

I think that short term, 6 to 12 months, there is a real risk of deflationary pressures in financial markets.

As shared with Patrons the past week, 3 big factors that worry me short term:

- Credit Impulse peaked in 2H2020

- Path forward is of tightening monetary policy

- Delta Variant

There was an interesting article in the FT about how certain top fund managers have “substantially backed away from a “rich” US equity market”.

I generally share similar views in the short term.

But that’s just short term. Mid term, once you go to mid 2022 and beyond, I think that’s a real case to be made that we’re going to see inflationary pressures.

I think all the supply chain disruptions across the board are really going to impact prices at some point.

But that’s financial markets. The difference is that the Singapore residential market is very tightly regulated and controlled.

Even if stocks crash, it’s going to take 6 – 12 months to feedback into the property market. By which time things could have recovered. Or the government could have intervened.

So for commentators predicting a big crash in Singapore house prices, I’m not so sure.

A 5% – 10% dip is definitely possible, but tough to see a 20% – 30% crash from here. This isn’t 1997 anymore. The world has changed. The bias today is for prices to go up, rather than down.

Closing Thoughts: Am I buying at a top?

Am I buying a property at the top here?

Definitely possible.

But in investing, you always make a decision with information you have today, and move on. Can’t apply hindsight to evaluate the quality of a decision.

So despite all that’s going on with COVID, I decided to buy a property for the reasons above.

I would really love to hear your views on this one though. Am I making a big mistake? Are you also in the market for a residential property? What are your main considerations?

This is a modified version of the article that first appeared on Patreon. If you enjoy articles like this, do support FH as a Patron and receive exclusive content, my personal stock watch and personal portfolio!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with and fund $2000.

Get 2 free Pfizer shares and 5 Haidilao shares (worth $200) you’re new to and fund $2700 + fulfil the trading conditions.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Check out our review on Tiger Brokers and MooMoo.

Join our Reddit community at r/SingaporeInvestments.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

I reckon Singapore property is like China stocks. In both cases, the government has all the tools (ABSD, TDSR for Sg property) AND the readiness to closely manipulate prices – in both directions, up or down. Both do so to make sure the poor doesn’t suffer too much, so that they retain popular support. Therefore in the long term, both prices will gradually increase to offset inflation. But increase will not be as astronomical as in the past decades.

Yes – exactly my view as well. 🙂

I’m with you on the government controlled 2-3% annual growth rate of properties in general in the long term. As with most things, including COVID pandemic, the SG style is tight control with intended outcome within expectations mapped out from the get go. Of course there will always be black swan, barring which 99% can count on things to pan out exactly the way it was intended to.

So the only way is up, but no roller coaster thrill anymore. It’s either you get in NOW or later when it is even higher. I always say sell low buy low sell high buy high net net in the end it is the same. There is never the ‘right’ time to do anything, only a good time for you given all consideration to income, assets, leverage, contingencies, outlook and objective.

Yes – spot on. Agree with this.

Given how tightly the local market is controlled, time in the market is more important.

So if one is flush with cash from an enbloc for example, best to buy back into the market then, rather than trying to time the market.

One year on…. In the rising interest environment, hope things are still doing ok for your second property cashflow. Rental should still be strong.

Yes returns are very strong. I locked in a 3 year fixed rate loan at low 1%, so rising rates should not be a concern for now…

After reading the entire article , I didn’t find what’s your reasons to buy second condo as investment …

1) You got an undervalue property ? What’s the PSF ?

2) You have gotten a rental ? Rental yield expected to be ?

Etc.

My apologies if it wasn’t made clear in the article.

Essentially a mix of the following reasons:

Time in the market vs timing the market

Borrowing large amounts at Low Interest Rates

Potential Inflation Hedge

Earn the rent from my other property (rental yield for the other is about 3.5%)

Given I already had the cash set aside for another property, I decided to just go ahead and buy instead of trying to time. ANd given my macro views, I expected that in time to come the investment will still pay off.

3.5% is nett or gross?

this is after the agent 1 mth comms, fees, condo monthly fee, etc?

Gross. Nett is about 3.0%

Hi FH, thank you for your article and insights. I have recently been reading up on dimensional funds and understand that both Endowus and MoneyOwl offer investors access to them. With the fees being reduced to 0.3% for Endowus, would it be cheaper if I maintain a small amount in MoneyOwl’s funds (to track how they rebalance the dimensional portfolios) while replicating them on my own using Endowus?

Thank you in advance for your advice!

Hi Jon,

That’s a really good question. I haven’t looked too closely into this, but off the top of my head that would be definitely possible actually. 🙂

The whole point of Fund Smart is that it allows you full control to replicate any portfolio you want.

Thanks for this post on property 🙂 it’s the one asset class which every Singaporean has a view on. Some questions from me:

Interest rates are the obvious elephant in the room. Given the bias for monetary policy is tighter from here, how would you stress test your capacity to repay under a variety of higher interest rate scenarios?

Why do you view COE as a proxy for property?

Why did you opt for freehold rather than lease hold for your second property? How did you decide on one vs the other?

What would you recommend for current owners of HDB flats looking to own a second property? To the best of my knowledge the single owner route is not available for hdb owners, so if we buy a second property we have to pay the punitive ABSD.

Hi Moomoo, always great to hear from you. Like you said, every Singaporean has their own views on property. I don’t profess to be right or wrong, but my personal views below:

1. Given how the world is structured today, I think the cycle high for interest rates will be 2-3% (3% was the 2018 peak, which stands to reason it should be lower this time unless we see significant inflation). So I would stress test using that range.

2. I don’t know exactly why it works too, but there is a correlation. I suppose the same dynamic that drives people to buy a house, would also drive them to buy a car?

3. Yeah really good question – might do a fuller article to share my views on this. There’s a massive leasehold vs freehold debate going on right now. I think at the end of the day it boils down to location. To me, Location > Freehold/Leasehold. I was lucky in that I managed to find one in the location I wanted, that was also freehold and at a good price. So I just went ahead to buy it.

4. HDB is tricky. The options are (1) buy a condo as a second property and pay 12% ABSD, or (2) sell the HDB and buy back 2 condos in each spouse’s name (doesn’t need to be immediate, can be over time). The option would depend on individual circumstances, for eg. does one have the cash set aside to buy 2 condos in the current market, where to stay in the interim etc. I would say though that Route (1) because of ABSD + LTV means that the property investment becomes less attractive, it will reduce the return vs something like stocks/REITs.

Thanks for the insightful article yet again, personally mindblown at the 1.05% interest rate, which I agree is bloody ridiculous, considering the potential credit risk that the bank is holding (no personal estimate of your liquidity, but just the sheer quantum being loaned). Of course, to each our own, but I do see the negative externality of the able.. buying additional properties while there is a red hot market, which would naturally crowd our real staying buyers. I suppose your decision was largely triggered by multiple factors, but mostly the ease of finding a renter for your existing property.

Thanks Charlito, appreciate the sharing. I myself was mindblown at the 1.05%, but more than happy to borrow at those rates.

Yes you are right – ease of renting, and also because I had the cash set aside anyway. And low interest rates were a very powerful tailwind.

I have a hard time understanding why people buy property for investment. Yields are very low and appreciation is not fantastic. Why not buy REITs instead? Better yield and appreciation should, at least, match property.

Couple of reasons:

1. Exposure to different asset class

2. Heavy use of leverage

Longer term – Residential property in Singapore is a good store of value, with different risk profile from capital market assets. I’m not saying it’s the best investment ever, but it’s a useful tool for Singapore based investors if you mix it with equities, REITs and fixed income in the right proportions. 🙂

Thanks for your reply FH! I think for COE and Property, probably the underlying driver would be interest rates.

On interest rate scenarios. Think there are 3 variables I would stress across different scenarios. Interest rates, rental rate, and one’s income.

On the options for HDB owners… ah snap that’s quite troublesome.. don’t think I will be able to convince the spouse and the kids to go through so many moves :P.

Property purchase is unique in that it’s heavily influenced by one’s personal circumstances. For example the “divide and conquer” route probably works for you because both you and your wife are fortunate enough got work in fairly high paying fields (I assuming of course 🙂 ). Among many in my social circle, either one or both are not able to qualify for a bank loan to buy a private property solely in one person’s name as the income level of a single spouse is not high enough.

Also, Would like also to ask if you would be willing to share, in the course of your personal journey, how did you go about deciding on which house to buy?

Hi! I recently bought a unit at Geylang, so I thought I’d share my reasons in bullet points (otherwise too wordy, don’t know if anyone wants to read). Feel free to probe for more details, and I’ll share my complete thoughts.

Part 1: Why I chose to buy property (instead of more stocks)

Part 2: Why I chose Geylang

Part 3: Why I chose the particular development in Geylang

WHY PROPERTY

1. Prices should rise in line with inflation.

2. Even if prices stay the same as today (i.e. no appreciation at all), with a small loan that is paid by rental income, property will still have small returns (~1% pa) at end of loan period. Not good, but not disastrous.

3. Even in the worst-case economic scenario, G will not allow property price in Singapore to crash.

4. I am already heavily vested in stocks and need a less volatile asset.

5. Another property serves my vanity (being honest here).

==> But this doesn’t mean any property will do. The G controls overall property prices, NOT prices of individual developments. So it’s key to choose carefully: make sure the property is one that will fall above the national average and not below.

WHY GEYLANG

6. Superb location – city fringe, good food and amenities. Near sports hub and attractions like GBTB, near future commercial hub Paya Lebar.

7. Prices still low despite superb location, due to seedy reputation

8. Shift of Paya Lebar Airbase in 2030-2035 will increase demand/prices in Geylang – partly because easing of height limits, nearby commercial activity in place of airbase, and no more aircraft noise.

9. Geylang’s seedy reputation will gradually become a thing of the past (like Bugis). This is because: (a) Reason for Geylang’s existence as vice hub gets weaker every day – sex has gone online, and into other parts of Sg. (b) G has already started to clean up Geylang (more police presence, surveillance cameras), and property prices there are already rising. (c) Geylang is prime land, and woke trends (e.g. environmental conservation, women’s rights) will put more pressure on G to re-purpose the area – who knows, maybe into an SME hub given its proximity to city centre, or a cultural hub for Singapore given the pre-war architectural heritage there. (d) The increasing residential developments in Geylang will compel authorities to have little choice but to make it safer and cleaner.

10. Because of all the above, prices in Geylang will rise – it’s a matter of when, not if. Just need to be able to wait.

11. Rental demand at Geylang remains very strong. G unlikely to tighten immigration much more because it’s hurting the economy; foreign tenants don’t find Geylang unsafe (it’s Singapore after all).

12. HOWEVER: since it’s ultimately speculative, I mitigated my investment risk by (a) getting a freehold unit, so not pressured to sell and can afford to wait; in worst-case scenario I can stay in it during retirement, then bequeath. (b) Getting smaller unit – in my case, a shoebox, which I argue has potential despite what some naysayers think.

===> So all these mean Geylang is a good prospect, but again, need to choose a development that will be attractive.

WHY DEVELOPMENT X

13. There are brothels next door. This is a GOOD thing because it means prices are more artificially depressed now, which means they will increase relatively more with future clean-up (equivalent of buying low for stocks).

14. Good connectivity – 500m to Aljunied MRT, large parts sheltered, good food and amenities nearby.

16. Good condition: quite new (TOP 2015), pool and gym in good condition, no useless things like waterfall or playground to increase maintenance fees, estimated 50% owner-occupied so condition better preserved

15. Good unit available – south-facing, reasonable view, quiet, functional unit layout

17. Good rental prospects – on average, 1 week to secure tenant in this development

18. Good resale prospects – because of Geylang prospects as a whole, and the positive features of this particular development.

CONCLUSION

19. Nowhere else in Singapore will I get a freehold property at a great location (city fringe, near MRT), highly rentable and with great appreciation potential – all these at such a low price.

20. It’s like buying a blue-chip stock during Covid: low chance of losing money, but high chance of earning in long term, and some chance of a windfall (if G completely re-purposes the land).

Thanks that is fantastic sharing. Personally I am bullish on Geylang too. Like you, I think it’s a question of when does the govt decide to clean up the area.

The one question that I was keen to hear more about – why did you decide to get a shoebox vs a 2 bedder? What were the considerations in play? And was it intended as a yield play or a capital gains play?

Actually, a 2-bedder would be the surer bet. But I only had enough cash to pay down-payment for a shoebox. Would need 1 more year to cough up another ~100K to buy a 2-bedder. But couldn’t wait that long because I felt G might increase ABSD soon (Heng SK and Desmond Lee spoke about it, and the politicians don’t usually comment on something unless it’s been discussed or in the pipeline). So decided to get a shoebox before it’s too late.

I bought the unit for potential capital appreciation. Geylang property while easily rented out doesn’t fetch high rental prices for now. But these prices should increase as the area gets cleaned up.

Unrelated point: thank you for all your articles on FH! I learnt so much from them. You stayed true to your principle of keeping things simple enough for a 6-year-old to understand. This is a remarkable feat 🙂

Understand your point – makes sense.

And thanks for the kind words! Means a lot! 🙂

Great points Moomoo, really does depend on one’s personal circumstances.

Deciding on which house is interesting. Took me close to a year before I finally settled.

Will look into writing a full article on this – including how to pick houses, and what considerations I took into account.

For now I would say the paramount consideration is really location. One cannot hope to buy real estate at a discount, so whatever location one decides on – one must be prepared to pay market value at the time of purchase. With the internet – the market is too effcient for anything else.

So to me, the number one consideration is picking the right location, because that’s the greatest determinant of future returns. It’s like buying a stock – you can buy Google and Facebook at the market price tonight, but which one will deliver the most returns going forward will depend on how much future growth is actually realised (vs what is priced in).

Not sure if this makes sense haha, will do a fuller article in time!

Thanks Vincent for the detailed sharing on how you settled on a unit in Geylang. Very insightful and definitely contains factors I never considered before!

Looking forward to your next article FH! Stocks aside, its surprising how much interest your article on property has generated 🙂

Hi FH, thanks for the great article. Just wondering if you could expand on the following line: “ With 75% leverage at 1% interest rates, that turns a nominal return of 2-3% on the house, to about 7% return on the equity you put in.” ? I didnt quite get it ????

Sure so the logic is like this. You buy a 1 million property, that goes up 3% a year.

But you only put in $250k, the rest is a loan from the bank at 1% a year.

So on the amount that you put in – the $250k, the return is about 7% a year after you factor in the interest repayments. 🙂

Hi, you mentioned that inflation helps to eat debts / loans. Given the forecast of inflation is at its peak in 2021 and slightly decreasing into 2022. Did you took any actions to return ur loan cheaper?

The main decision was on fixed vs floating, and loan duration. I eventually settled for fixed at 1.05% on a 2 year term. If I had gone for 3 the rate would have been higher.

Taking a punt that by the time the 2 years is up in 2024, the market rates could have gone up and then come down already. Could be an absolutely disaster though, I might be refinancing at 2% if inflation stays till then.

Hi, can guide me which conveyancing firm u use for decouple? Do they help to calculate required cash/cpf payments for decouple or we have do calculation ourselves?

The law firm will calculate it for you. If you refinance check with your bank on which are their approved law firms, because usually you can get a refinancing legal fee subsidy.

If you need some recommendations PKWA is a pretty decent option but quite expensive, about 7k plus last I checked. The cheaper options I won’t recommend publicly on this platform because the quality is a bit hit miss, so you need to double check their work. If you’re sophisticated enough you can use them and save the cost, if you’re unfamiliar with how conveyancing works I would say just pay for a decent lawyer.

After so many years of poor returns, people still have hopes in Singapore real-estate market, its beyond me. Look at most of the major cities in the world average capital appreciation are double digits, Singapore miserable 2%.

Would you prefer that Singapore house prices trade like New York or London? I personally – do not.