So… Mapletree Commercial Trust and Mapletree North Asia Commercial Trust called for a trading halt on 28 Dec.

And trading remained halted for the next 3 days.

Speculation in the market went wild about a merger between the 2 REITs.

And it turns out the rumours were exactly true – because it was announced that MCT will be buying MNACT.

Mapletree Commercial Trust Merger Explained

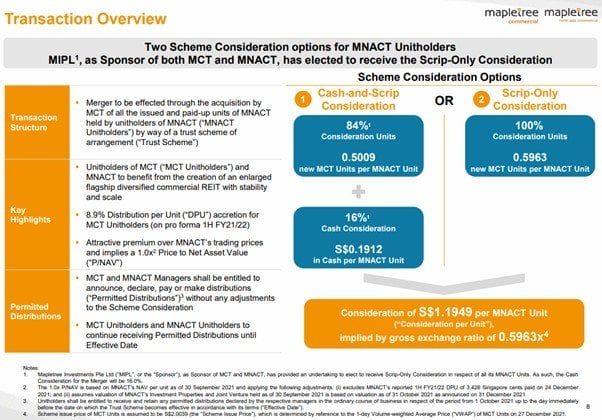

To sum it up – Mapletree Commercial Trust (MCT) is buying over Mapletree North Asia Commercial Trust (MNACT).

MNACT unitholders will get an option of either:

- 100% MCT units – 0.5963 new MCT units at an issue price of S$2.0039 apiece

- 84% MCT Units, 16% cash – 0.5009 MCT units and S$0.1912 in cash

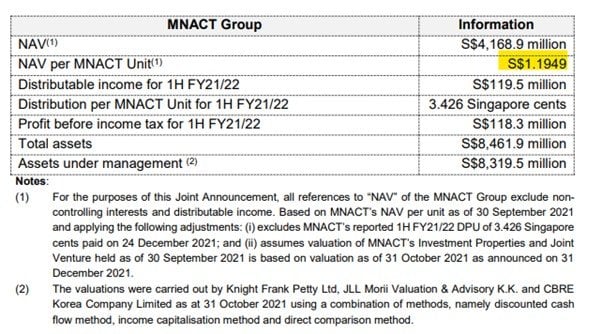

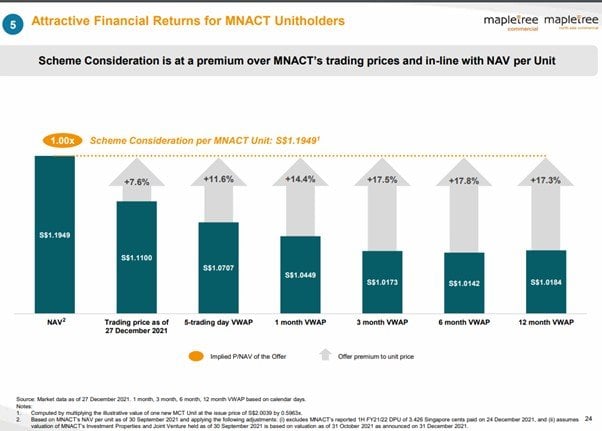

This works out to a total consideration of $1.1949.

S$1.1949 is MNACT’s net asset value (NAV), so MNACT is basically bought out at book value.

This is a 7.6% premium to MNACT’s trading price on Dec 27 and a 17.3% premium to its 12-month volume-weighted average price

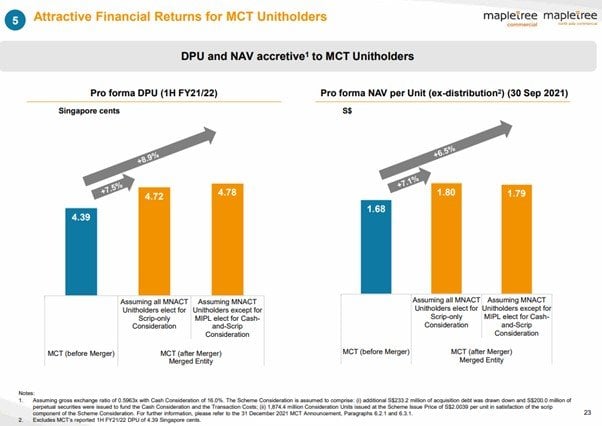

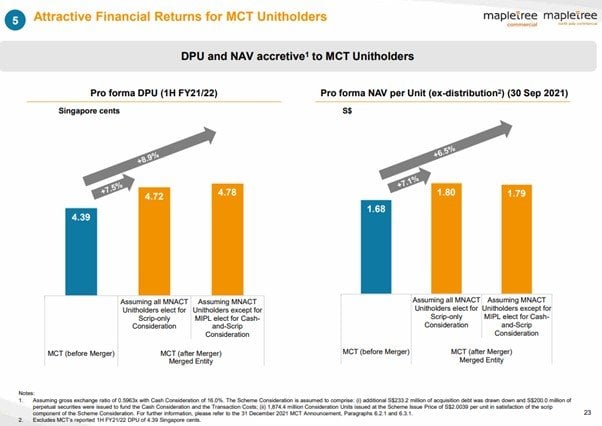

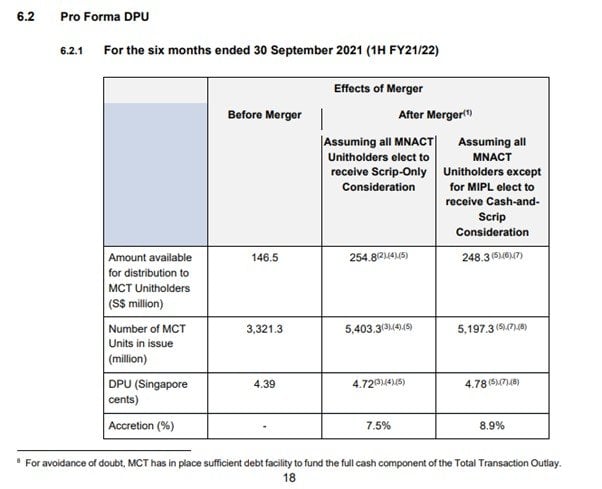

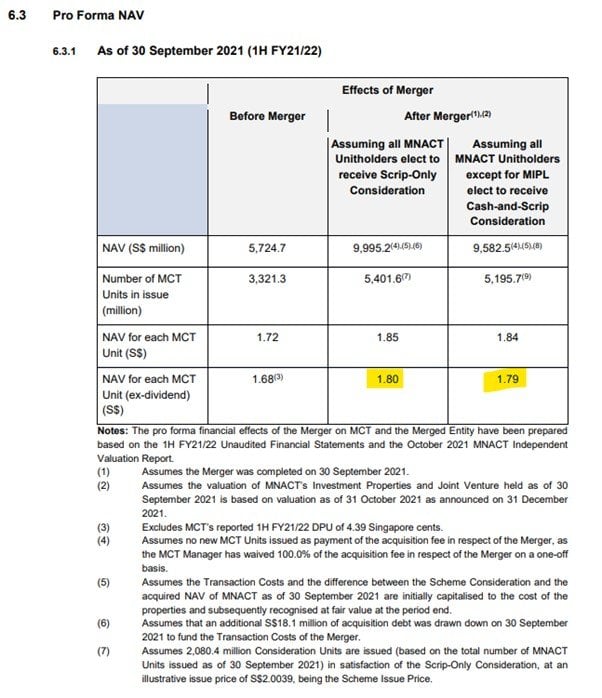

On a pro forma basis, the merger is 8.9% DPU Accretive and 6.5% NAV Accretive for MCT unitholders.

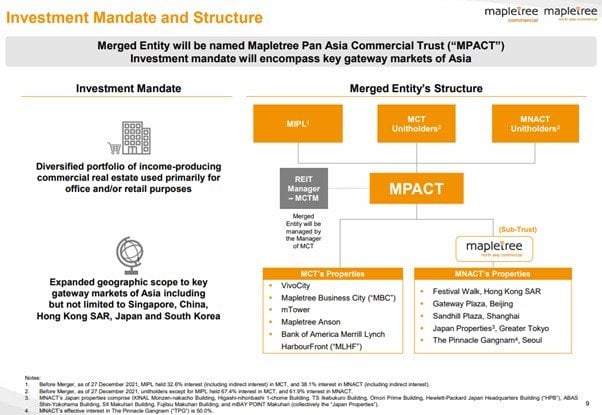

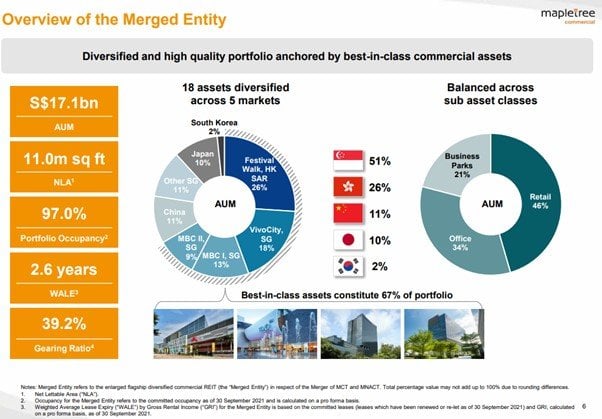

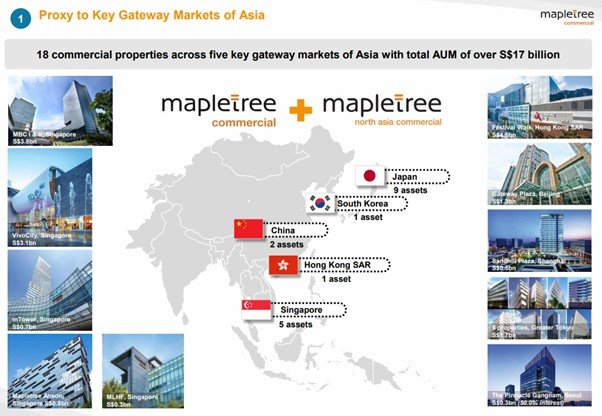

Investment Mandate of Mapletree Pan Asia Commercial Trust (MPACT)

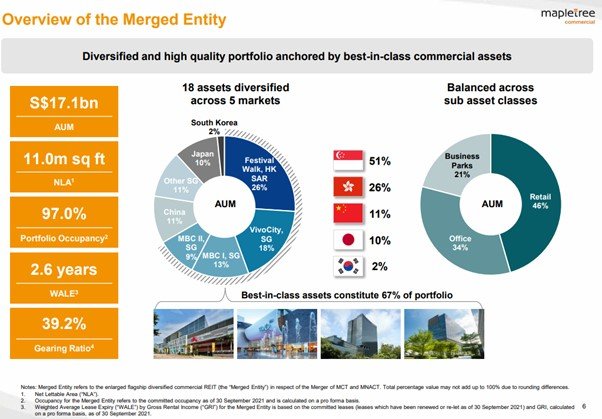

The newly merged REIT will be known as Mapletree Pan Asia Commercial Trust (MPACT).

It’s investment mandate will be office or retail properties in key gateway markets in Asia, including Singapore, China, Hong Kong SAR, Japan, and South Korea.

You can look at the asset allocation of the new MPACT below.

Breakdown will be:

- Singapore – 51%

- Hong Kong – 26%

- China – 11%

- Japan – 10%

- South Korea – 2%

And asset class will be:

- Retail – 46%

- Office – 34%

- Business Parks 21%

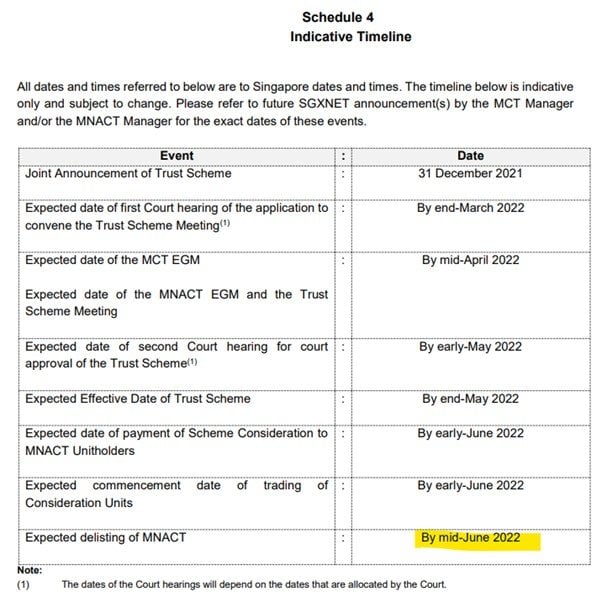

Indicative Timeline for Merger

Indicative Timeline is below, transaction is expected to close by mid-June 2022.

Is this Merger a better deal for MCT or MNACT?

Full Disclosure – I am a unitholder of both MCT and MNACT, so you can’t accuse me of being biased.

And I’m just going to put it out there.

As a MNACT unitholder, I love this merger.

As a MCT unitholder, I am much less pleased.

Mapletree North Asia Commercial Trust (MNACT)

As a MNACT unitholder, I am ecstatic.

I’ve been meaning to exit this position for quite a while now.

The reason why was because I wanted to close off my Hong Kong exposure. Longer term, I’m just not super bullish on Hong Kong real estate.

And frankly, the rest of the MNACT portfolio excluding Festival Walk isn’t exactly best in class, so I wasn’t super keen to hold on long term.

I was actually prepared to sell at anything 1.1+, so when it started trading at $1.11 recently that really caught my eye.

But now it’s getting privatised at $1.19, payable with MCT units at $2.00.

That’s just a fantastic deal for me and I for one, love this merger as an MNACT unitholder.

Mapletree Commercial Trust (MCT)

Regular readers of Financial Horse will know that I adore Mapletree Commercial Trust.

It’s the first REIT I wrote about on Financial Horse, and one of my largest REIT positions.

But as a MCT unitholder… man, where do I even begin.

I wouldn’t necessarily say it’s a terrible deal for MCT, but the analysis is a lot more nuanced as compared to MNACT.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Why does MCT need to do this merger?

Okay a bit of background.

The problem for MCT before this, is that there is no room to grow in Singapore anymore.

All the best-in-class assets in Singapore are held by other REITs, who would never sell to MCT.

And those that aren’t REIT-ed? You need to pay a crazy price to get them, which wouldn’t be DPU or NAV accretive.

So you have to go outside Singapore to grow.

You can look at all the big REITs like CICT or Ascendas, and they’re all buying non-Singapore properties these days.

That brings with it its own set of problems, because you need to source for deals, evaluate it, negotiate price etc. It takes a lot of time and effort to execute, and there’s no guarantee you can buy at a fair price in this market, given how insane valuations are.

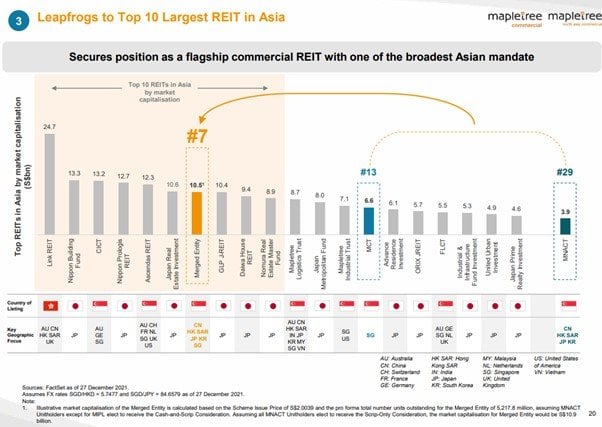

And at the same time, MCT was starting to get outclassed (size wise) by their competitors CICT and Ascendas REIT.

Big is sexy these days, because of index inclusion, liquidity and financing reasons.

Long story short – MCT needed to grow, in a NAV/DPU accretive way, fast.

I can see why MNACT had to do it

And the deal makes sense for MNACT too.

MNACT has been trading at a discount to NAV for the longest time ever, ever since Hong Kong protests back in 2019.

This makes it very hard to do yield accretive transactions, and it’s very hard to raise equity because you would be issuing new units at a discount to NAV.

And over the past few years, they’ve been trying to do everything to bring the unit price up – even the rebrand from Mapletree Greater China Commercial Trust to Mapletree North Asia Commercial Trust.

But nothing really worked so far.

A lot of the recent properties they acquired have also not been performing that well.

You can only blame Hong Kong protests that long before it starts to look like just poor management.

So MNACT needed to find a way to bring the unit price up to book value.

Kill 2 birds with one stone

The quickest way to solve both problems for MCT and MNACT?

Merge the 2 of course.

MCT is trading at a premium to book value, so you use MCT to issue new units (at a premium to book), and buy out MNACT at book value.

MCT unitholders get a NAV and yield accretive transaction.

MNACT unitholders get to “exit” their position at a premium.

Magic right?

So to give credit where credit is due, I can absolutely see why this deal had to be done, and why it makes sense for Mapletree.

Best-In-Class Greater Southern Waterfront Play… no more?

I used to love Mapletree Commercial Trust as a best-in-class Greater Southern Waterfront Play.

Vivocity and Mapletree City were just absolute crown jewels.

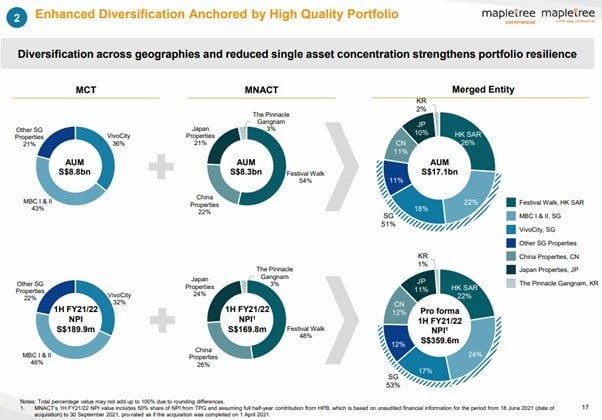

In the past, Vivocity and Mapletree Business City made up 79% of Mapletree Commercial Trust, making it a very efficient bet on Singapore and the Greater Southern Waterfront.

Going forward, both will make up only 40% of the expanded REIT.

So previously if you were bullish on Singapore and bearish Hong Kong, you could buy more MCT and buy less MNACT.

Going forward, that option goes away.

If you buy MCT, you have to accept that 49% of your portfolio is going into Hong Kong, China and Japan.

I raised the same concern with the CMT CCT merger, but at least in that case they were mixing Singapore offices with Singapore malls.

Here – it’s mixing Singapore commercial assets with North Asian commercial assets. Both are very different markets, with very different valuations.

I mean it’s a decent enough acquisition, and if it were 5-10% of MCT’s portfolio I would have no comments.

But this is a $8.3 billion portfolio that will effectively make up 49% of MCT going forward.

So yeah… really not a big fan of this merger.

What is a Fair Price for MNACT?

As a MCT unitholder, I’m effectively buying MNACT out at book value.

For a Hong Kong retail mall, and a bunch of China/Japan/Korean offices or malls. That has been trading at a 15-20% discount to book for much of the past 1 – 2 years.

Buying it at NAV – is it a good price?

I mean you can argue that if MCT went out into the market right now and bought an equivalent portfolio from a third party, they probably have to pay much more.

I don’t disagree with that.

The market is so overvalued right now that if you are going to do a mega deal, this is probably the fair price to pay.

But that said, if given the option between (1) buying MNACT and (2) not buying MNACT, I actually would have much rather preferred the latter.

DPU and NAV Accretive for MCT

The merger is DPU and NAV accretive for MCT though, but that is to be expected when you (a) use a REIT trading at a premium to (b) buy out a REIT trading at a discount.

If you use the pro forma DPU and annualise it, the yield for MCT should be about 4.7% at the last done unit price of $2.00.

If it drops to $1.9 on Monday, that’s about a 5.0% yield.

What is the fair value of Mapletree Commercial Trust after the merger?

MCT traded at a 15%-20% premium to book before this.

Post-merger, I wouldn’t expect it to trade at a premium to book anymore, because of the North Asia assets.

MNACT trades at about a 15-20% discount to book, so both should equalize each other out, and the new MPACT should trade at around book value going forward.

Or at least that would be my idea of fair value.

NAV for MCT post acquisition is about 1.8, so my rough fair value would be $1.8 – $1.9 ish.

MCT last traded at $2.00, so this could imply a pretty large drop on Monday when trading resumes. Let’s see.

Will I buy more MCT if it drops on Monday?

That said, as an investor, I look at the world as it is, not as how I wish it to be.

I don’t like the merger, but I can understand why it needs to be done, and chances are it will likely get done.

This could put a lot of pressure on MCT’s share price short term.

If so, would I be scooping up MCT units?

And the answer is a resounding – Yes.

If I can fill MCT at close to my fair value, I’m probably going to be loading up on MCT units.

I think that even after this merger, there are not going to be many REITs out there that can outperform MCT at $1.8 – $1.9, at this level of risk.

But let’s see.

For those who are keen, you can check out my full REIT portfolio (and stock portfolio) on Patreon.

Closing Thoughts – Leakage of Merger Information?

It’s interesting because MNACT went up 3% on 27 Dec right before MNACT called for the trading halt.

Whereas MCT has been trending down for a while.

It’s quite stark when you plot them against each other – Red being MNACT and Green being MCT.

I wonder if MAS/SGX will look into this – because it seems the unusual trading activity was serious enough that MNACT/MCT had to call for a trading halt 3 days earlier than they would have liked.

Whatever the case – I would love to hear from you.

Are you a MCT or MNACT unitholder? Do you like this merger?

As always, this article is written on 31 Dec 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Thanks for the informative article.

For me, my initial reaction (biggest displeasure) as a MCT unitholder (non-MNACT unitholder) is the shrinking of SG properties to only 51% of the new merged entity. Then, you touched on price… Not exciting.

Yah. To be fair I have a lot more MCT than I do MNACT.

I mean it’s an okay deal, and I would buy more if price drops, but really not a big fan of this one. I liked the CMT CICT deal a lot more.

I guess next question is, when will MIT and MLT merge? Haha. Seems like a sooner or later thing.

That’s true, they can create a behemoth to take on Ascendas REIT.

Annoying, for all the reasons you outlined. Thanks for the analysis.

Glad you find it useful! 🙂

Hi FH,

Long time reader and 1st time to comment.

Am a MNAC holder and Non-MCT holder.

I bought MNAC at 1.2X during the riot and thought it will be over soon. But it went downhill instead. At 1.19, i will breakeven with a small % gain over 2 years.

Will it be possible to sell MNAC at say 1.16-1.18 at Mon open (Assuming it traders at the price range) and if MCT goes down to 1.8X, then scoop up MCT as i am still decently okay with the combine entity. Just that i do not want to go through with the merger exercise and end up with weird odd lots.

Thanks in advance!

Hi Vincent, good to hear from you!

I think the key will be how the price opens on monday. I suspect 1.16-1.18 for MNACT is too aggressive, considering that MCT units are likely to go down on Monday.

what are your thoughts on the change in management fee structure?

for me, tho it seems they are not getting paid more for managing the MNACT assets, but effectively this transaction will increase their fees for the MCT assets from 0.25%(+4.0%) to 10%(+25%). is this your understanding also?

MCT was using the old fee structure where it was AUM based fee. All the newer REITs have shifted over the the MNACT style fee, where it’s more closely tied to performance.

So in a way they’re just aligning with the latest market standards. It might be a small fee increase short term, but longer term it does create more alignment of interests.

what are your thoughts on the change in management fee structure?

for me, tho it seems they are not getting paid more for managing the MNACT assets, but effectively this transaction will increase their fees for the MCT assets from 0.25%(+4.0%) to 10%(+25%). is this also your understanding?

MCT unitholder here. I wholly agree with the points that you have covered in your analysis. Like you said, the merger will probably go through. I will hold on to the units that I have, but moving foward, I will have to decide if I should load up more units if the price of MCT does goes down (I’m not a fan of MNACT’s properties and it’s going to constitute 50% of MPACT’s portfolio post-merger)…

Yeah I get what you mean. I’m not the biggest fan of Festival Walk and MNACT’s portfolio, but if I get a good price I’ll probably still buy it.

Hi FH,

Agree broadly with your analysis. I bought into MNACT at 80 plus cents during their down phase and haven’t bought MCT because valuations have been high for a long time so this is a nice surprise. Recent rentals reversions at Festival walk of minus 10-20% were horrendous and it was a bit worrying. Like you, I do think news leaked in advance because I had noticed MNACT share price shooting up in last couple of days before the trading halt and I was wondering what was happening…so it seems some people somewhere knew.

But in general, not that bullish about retail malls in general given the secular challenges they face, esp if yields are only around 5%. Banks, esp. China banks and maybe FCT which has higher heartland malls and more decent yield at 1.22 price recently look more attractive to me than MCT at current valuations.

Actually I’m quite bullish on retail malls haha. Even if you look at US/China where eCommerce is very developed, it’s quite clear that there still is a place for retail malls where people can go and hang out and get stuff done in the real world.

Especially in Singapore, where the amount of retail space per population is not as high as say the US market. I think if you stick to high quality malls like MCT/CICT/FCT, they will still grow nicely for years to come.

I’m a MCT shareholder and I built on the position because I bought into the southern waterfront storyline. Avoided MNACT as I believed the picture is not going to be rosy for HK, and those properties in Japan and Korea are pretty meaningless in the combined entity.

I’m not going to varnish this. It looks like MCT shareholders have been asked to bail out MNACT, bad management or otherwise. I honestly don’t see any benefits for MCT shareholders – bailing out MNACT at a premium, having to accept a dip in share price, exposure to HK which is not very exciting, exposure to political and forex risks, a quarter of the portfolio taken up by festive walk which has terrible rental reversions and will just be a drag to the performance moving forward. If this needs to be tabled to shareholders for approval, I’ll be voting no.

I suppose you can argue the deal is DPU accretive for MCT, but yes, absolutely get what you mean.

As a MCT holder, I don’t like the merger as it adds exposure to HK and China market which I feel is stagnant. If I like MNACT, i would have been a MNACT unit holder already.

Agree, not a big fan as a MCT unitholder.

Hi FH,

Thanks for the article. I am not a unitholder of MCT nor MNACT but I have to agree with you that the merger is not that attractive from the perspective of MCT unitholders who may not like the exposure to Greater China. Nonetheless, at least the merger does not entail rights issance for MCT, so not that bad lah.

Regards,

Gerald

https://sgwealthbuilder.com

Hi FH

Was expecting your post on this this weekend and you have not disappointed me!

I hold both but very little of MCT having divested pre COVID in mid 2019 to meet my housing needs

That was at around 1.85-1.90, if I remembered right .

Subsequently I added a small amount at 1.97 recently

However, I was lucky enough and toolbar the risk of buying a significant number of MNACT units recently in the 98-104 cents range and therefore have greater stakes in MNACT

It gets dicey from here

Next week, the markets might throw a surprise and we may not see a 1.16-1.18 opening. I feel it might be more muted going by the reaction. Similarly, the on paper NAV and DPU accretion touted about for MCT might mitigate the fall and it may stay in the 1.90 plus range

We need to wait and see. If the MNACT price aggressively runs up, I might sell out and wait with cash and buy MCT slowly and steadily to consolidate gains

We may be in for a surprise though all our projected opening prices makes logical sense

Finally, to dilute HK the MPACT REIT might go on an acquisition spree as early as late 2022, utilizing the relatively Low rates and liquidity situation. This might result in private placements and equity dilution that might destroy whatever we ‘gain’. The CEO clearly said that they are looking at maxing out after merger

Regards

Garudadri

Haha great comment Garudadri. I agree with your points.

Let’s see how the price opens tomorrow, that will determine where the opportunity lies. 😉

Hello,

Looks like not many happy MCT holders.

I hold 5x more MTNac than MCT.

As a FIRE, probably not very happy as i will lose a 7-8% yield counter.

Have to look at Capital China Trt now.

CLCT is 100% PRC, so quite a different risk profile from MNACT unfortunately.

At current standing I found

For year on year difference according to google finance

MNACT having 21% free cash on hand

And

MCT having 192% free cash flow on hand

If there something not known, causing this merger?

Really looks like a bailout for MNACT

Hi FH,

Devastating spell of destruction for MCT. Should you join me at MLT? Whats your take?

Rrgards,

Gerald

https://sgwealthbuilder.com

Haha just shared my views in the latest article!

Hi FH,

It’s all pretty confusing and I don’t fully understand the technicals. So am hoping you can help me?

I got into MNACT at 1.15 in Nov 2019. I held on to it and with this latest news, I’m wondering if I should sell now or wait for the merger to be executed?

Haha well it really depends on your risk appetite and investment objectives! How much risk can you take. What are you trying to achieve with your investment etc.

I dislike the merger too. Doesn’t benefit much on MCT holders.

Well it is DPU accretive, but yeah, I would have much preferred them to stay separate.