Unless you’ve been living under a rock the past week.

You’ll probably have heard that the Astrea PE bonds are back – with Astrea 8 this time.

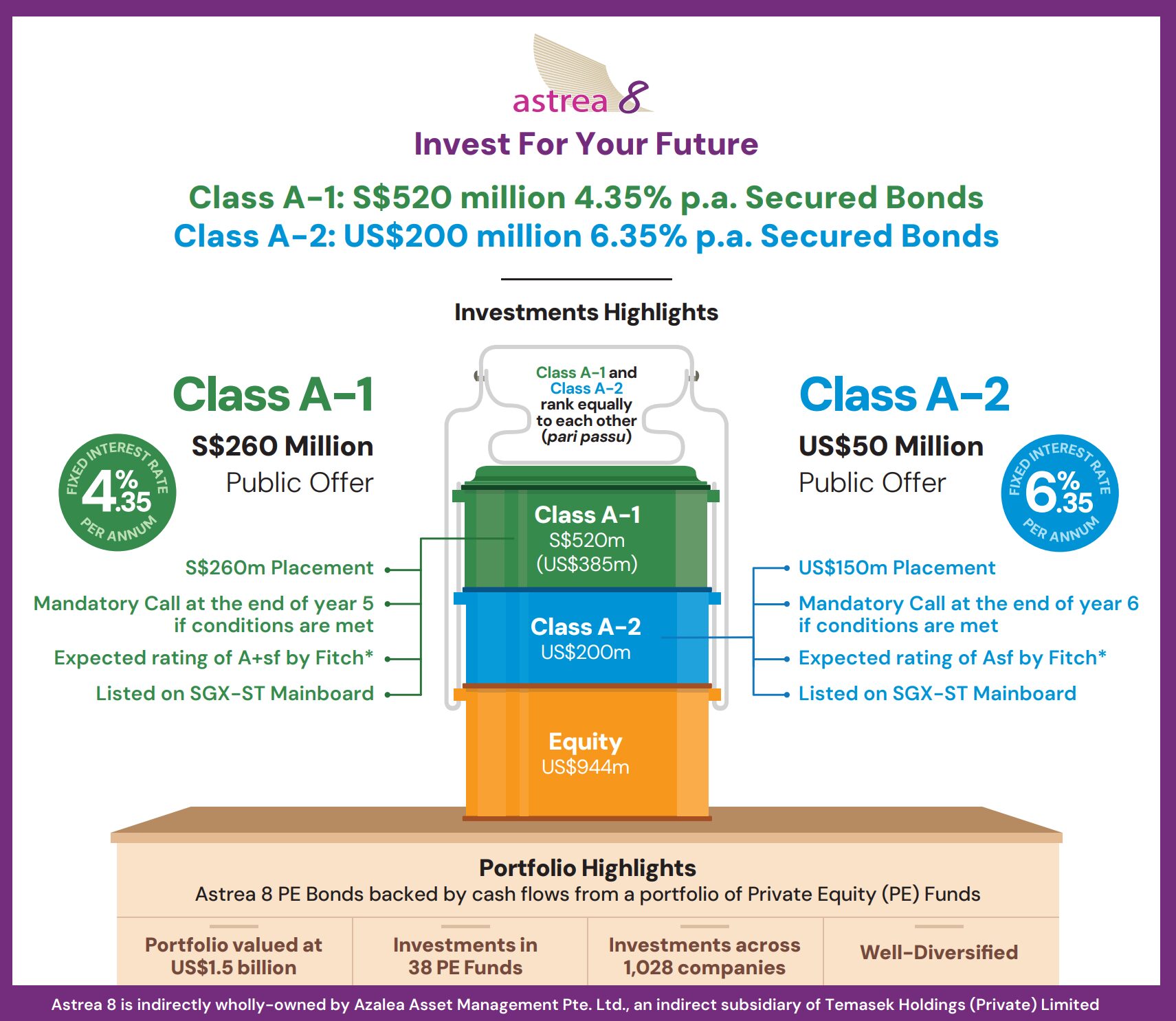

There are 2 tranches up for public offer.

The SGD version yields 4.35%.

And the USD version yields 6.35%.

I’ve subscribed for every round of Astrea bonds since they were available to the public with Astrea 4.

So… will I subscribe to the Astrea 8 PE Bonds as well?

Let’s dive in.

Introduction to the Astrea 8 PE Bonds – Class A-1 (SGD) and Class A-2 (USD)

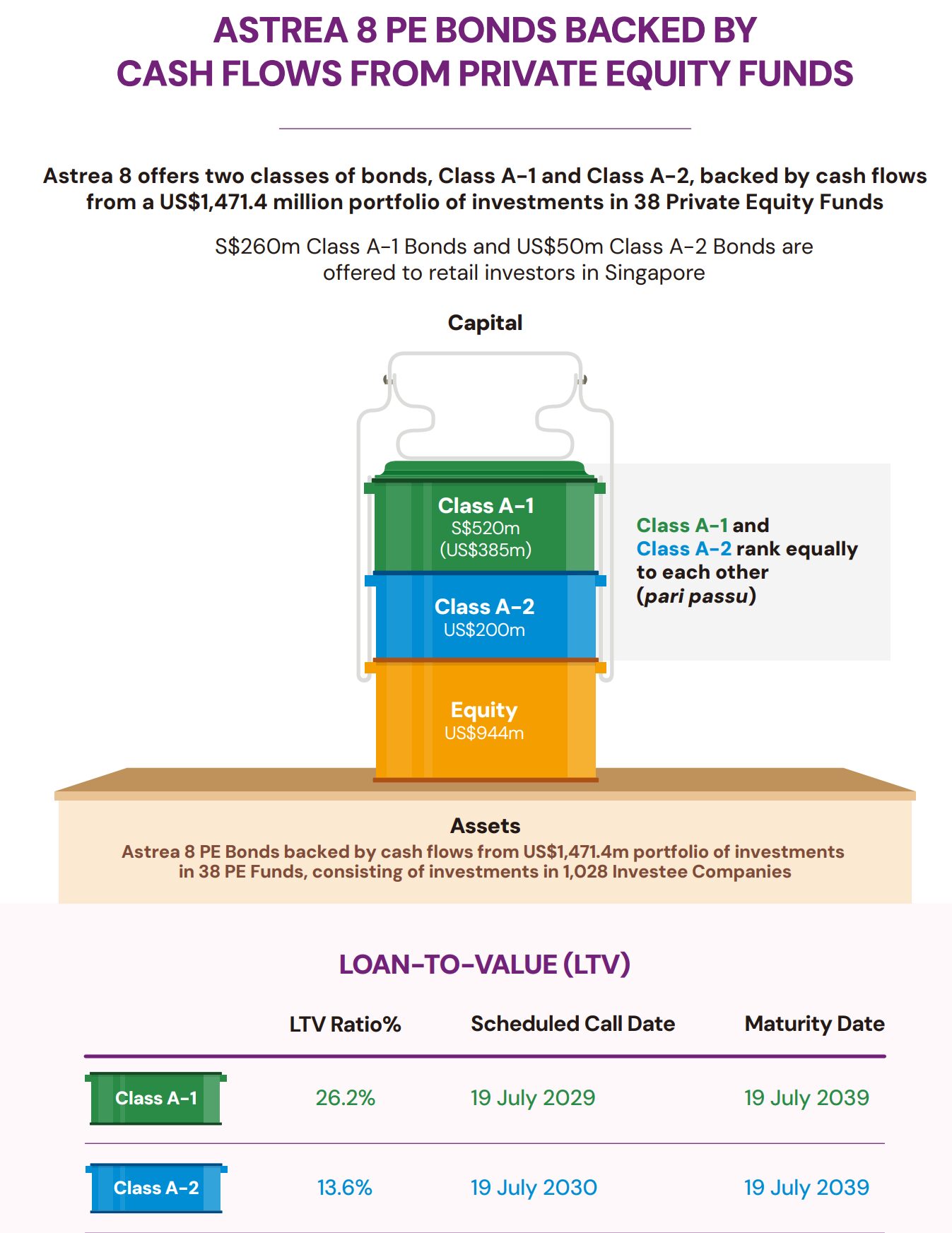

The Astrea 8 PE Bonds are secured against the cash flow from private equity (PE) Funds.

Think about it this way.

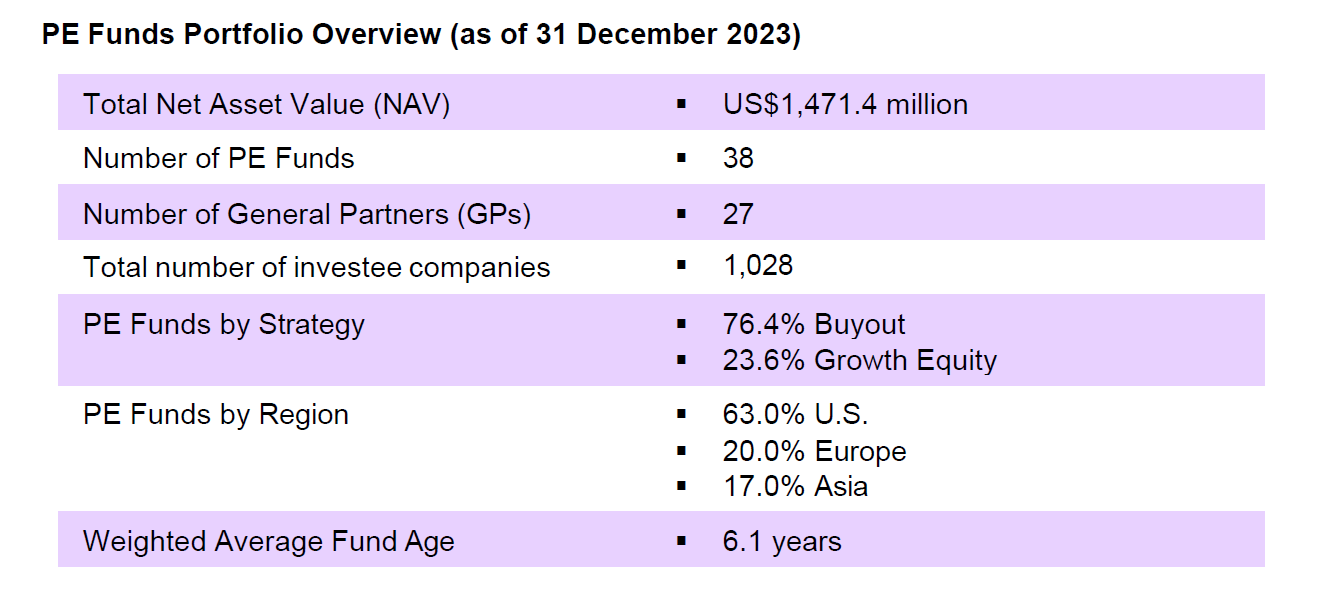

Astrea takes 38 different PE Funds, collectively worth US $1.47 billion.

Astrea borrows US$585 million secured against this portfolio (39.8% LTV).

And there are 2 different tranches, one borrowed in SGD (Class A-1), and one in USD (Class A-2).

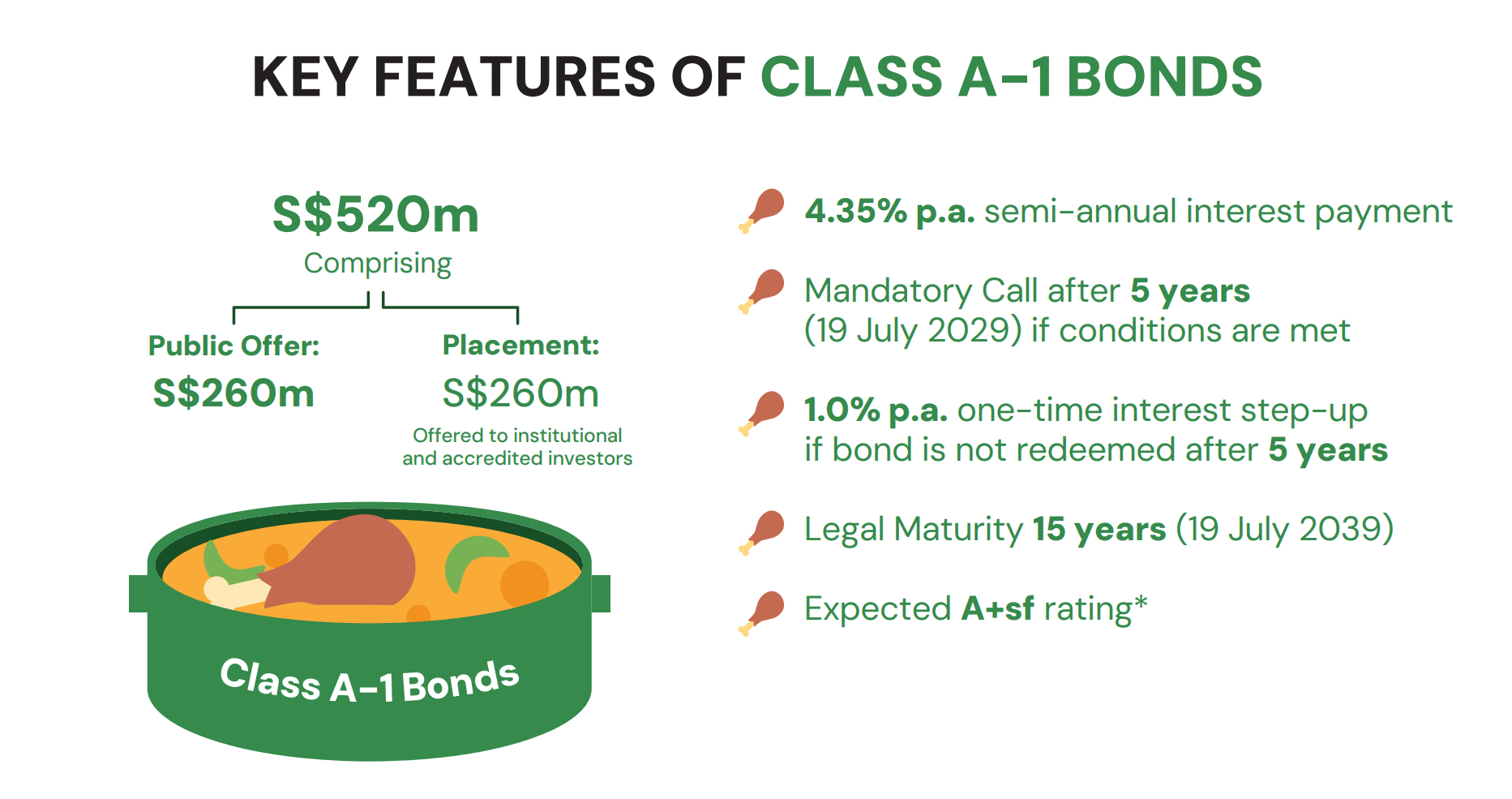

Class A-1 (SGD) Astrea 8 PE Bonds

The key details of the Class A-1 Astrea 8 PE Bonds are set out below:

- 4.35% p.a. semi-annual interest payment

- Mandatory Call after 5 years (19 July 2029) if conditions are met

- 1.0% p.a. one-time interest step-up if bond is not redeemed after 5 years (to 5.35%)

- Legal Maturity of 15 years (19 July 2039)

- $260 million public offer

Legal maturity for Astrea 8 Bonds is 15 years (and not 10 years like previous Astrea bonds)

A key difference for Astrea 8 Bonds is that the legal maturity is extended to 15 years (instead of 10 years for the previous bonds).

The reason given in the FAQs is that:

“The Issuer and Manager observe that the legal maturities of other similar PE-backed bonds in the market are typically 15 years. As such, this revision aligns the legal maturities of the Astrea 8 PE Bonds with those similar bonds, which would allow investors to compare them on an apple-to-apple basis and better demonstrate the relative quality of the Astrea 8 PE Bonds with such bonds. Note that the Class A-1 Bonds and Class A-2 Bonds are subject to mandatory calls at the end of year 5 and year 6 respectively, if conditions are met.”

Basically – to match other PE Bonds which usually have a 15 year maturity (although the mandatory redemption after 5/6 years remains).

You could also argue that this gives the bonds a longer runway in case something really goes wrong, instead of just hitting the default wall at 10 years.

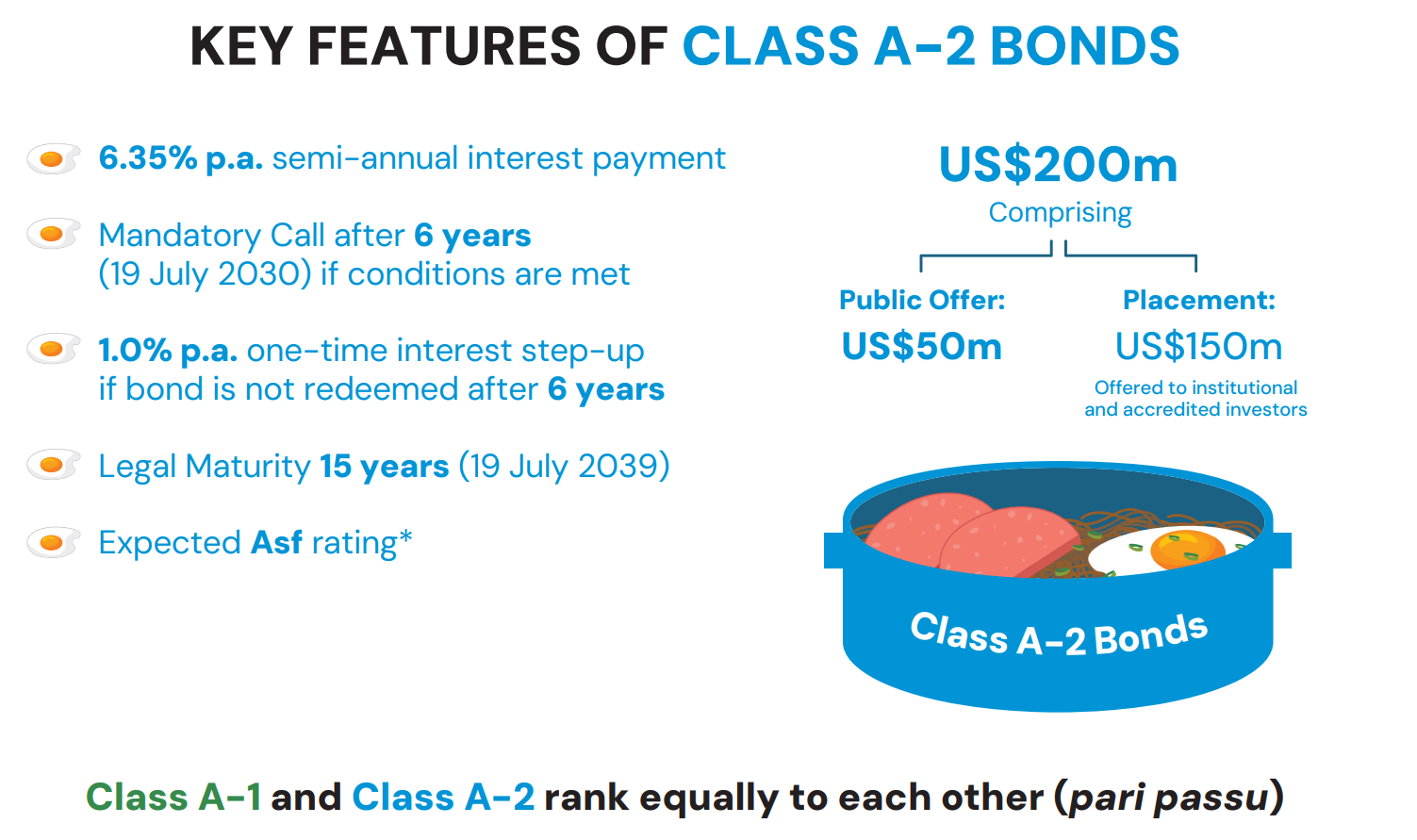

Class A-2 (USD) Astrea 8 PE Bonds

Class A-2 on the other hand:

- 6.35% p.a. semi-annual interest payment

- Mandatory Call after 6 years (19 July 2030) if conditions are met

- 1.0% p.a. one-time interest step-up if bond is not redeemed after 6 years

- Legal Maturity 15 years (19 July 2039)

- $50 million public offer

Exactly the same as Class A-1, only difference is that:

- USD (vs SGD)

- 6.35% yield (vs 4.35%)

- Mandatory call is 6 years (vs 5 years)

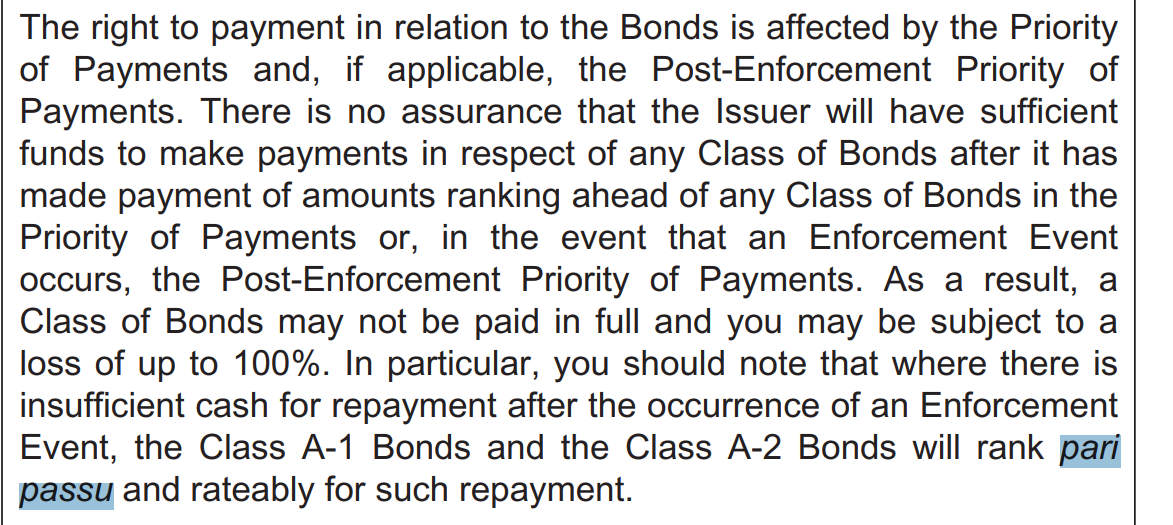

Class A-2 (USD) ranks pari passu to Class A-1 (SGD) – same credit risk for both Astrea 8 Bonds?

In Astrea 7, the USD bonds issued were Class B and therefore “more risky” than the Class A-1 SGD bonds.

This time around the USD Class A-2 will rank pari passu to the SGD Class A-1.

Pari passu is just lawyer speak for equal.

So in simple English – the credit risk for both the SGD and USD bonds is the same in the event of a default.

If Astrea 8 defaults, both Class A-1 and Class A-2 will get a similar proportion of the payout.

So credit risk is the same, but do note that Class A-1 (SGD) will be paid out first at 5 years if the conditions are fulfilled, followed by Class A-2 (USD) after 6 years.

Is the 4.35% yield for the SGD Astrea 8 PE Bonds attractive? (Class A-1)

I’ve compared Astrea 8 Bonds’s yield spread against a 10 year Singapore Savings Bond below, compared against previous Astrea bonds.

|

Series |

Date |

Yield |

10 year SSB at the time |

Yield spread vs 10 year SSB |

|

June 2018 |

4.35% |

2.43% |

1.92% |

|

|

June 2019 |

3.85% |

2.13% |

1.72% |

|

|

March 2021 |

3.0% |

1.15% |

1.85% |

|

|

May 2022 |

4.125% |

2.53% |

1.595% |

|

|

Astrea 8 |

July 2024 |

4.35% |

3.19% |

1.16% |

You can see how the yield spread of 1.16% this time around is by far the worst of all the Astrea PE Bonds.

The 4.35% headline yield is the same as Astrea IV, but don’t forget that back in 2018 the 10 year SSB was only paying 2.43% (vs 3.19% today).

Viewed this way, this round of Astrea 8 PE Bonds (SGD) are actually not that attractive.

Is the yield on Astrea 8 PE Bonds attractive vs T-Bills or Singapore Savings Bonds?

I’m sure most of you are aware that you can easily get 3.70% yield on the latest 6-month T-Bills.

That’s only 0.65% lower, but completely risk free.

Sure you may argue that T-Bills carry refinancing risk, as interest rates may be lower 6 months later.

But even if you buy the latest Singapore Savings Bonds – you’re getting paid a 3.19% yield for 5 years.

That’s just 1.16% lower, for bonds that are risk free and can be redeemed any time with no capital loss.

So… yield on Astrea 8 PE Bonds (SGD) is not attractive?

Frankly I was quite surprised to see the low yield on the Class A-1 SGD Astrea 8 PE bonds.

I was expecting a 1.5%+ yield spread, which would have put the yield at 4.7% and higher, and much more respectable.

In previous series of Astrea Bonds, Azalea (the issuer) usually left some money “on the table” for the SGD tranche for Singapore retail investors (which was what made the Astrea bonds so attractive).

Unfortunately it doesn’t look like they did the same thing with Astrea 8.

Is the 6.35% yield for the USD Astrea 8 PE Bonds attractive? (Class A-2)

Comparatively speaking – the USD Class A-2 Astrea 8 PE Bonds might be more attractive.

Yield at 6.35% is 2.13% higher than a risk free US Treasury.

|

Series |

Date |

Yield |

Yield spread vs 10 year US Treasury |

|

|

Astrea 7 (Class B) |

May 2022 |

6.0% |

3.15% |

|

|

Astrea 8 (Class A-2) |

July 2024 |

6.35% |

2.13% |

|

This is almost double the 1.16% yield spread on the SGD Class A-1.

And from a nominal perspective, 6.35% yield is just a lot sexier.

Given that Class A-1 and Class A-2 rank pari passu in insolvency (so same credit risk), at first glance I actually find the USD Class A-2 bonds more attractive.

But let’s finish up the analysis first.

Will the Astrea 8 PE Bonds default?

The million dollar question – what is the default risk?

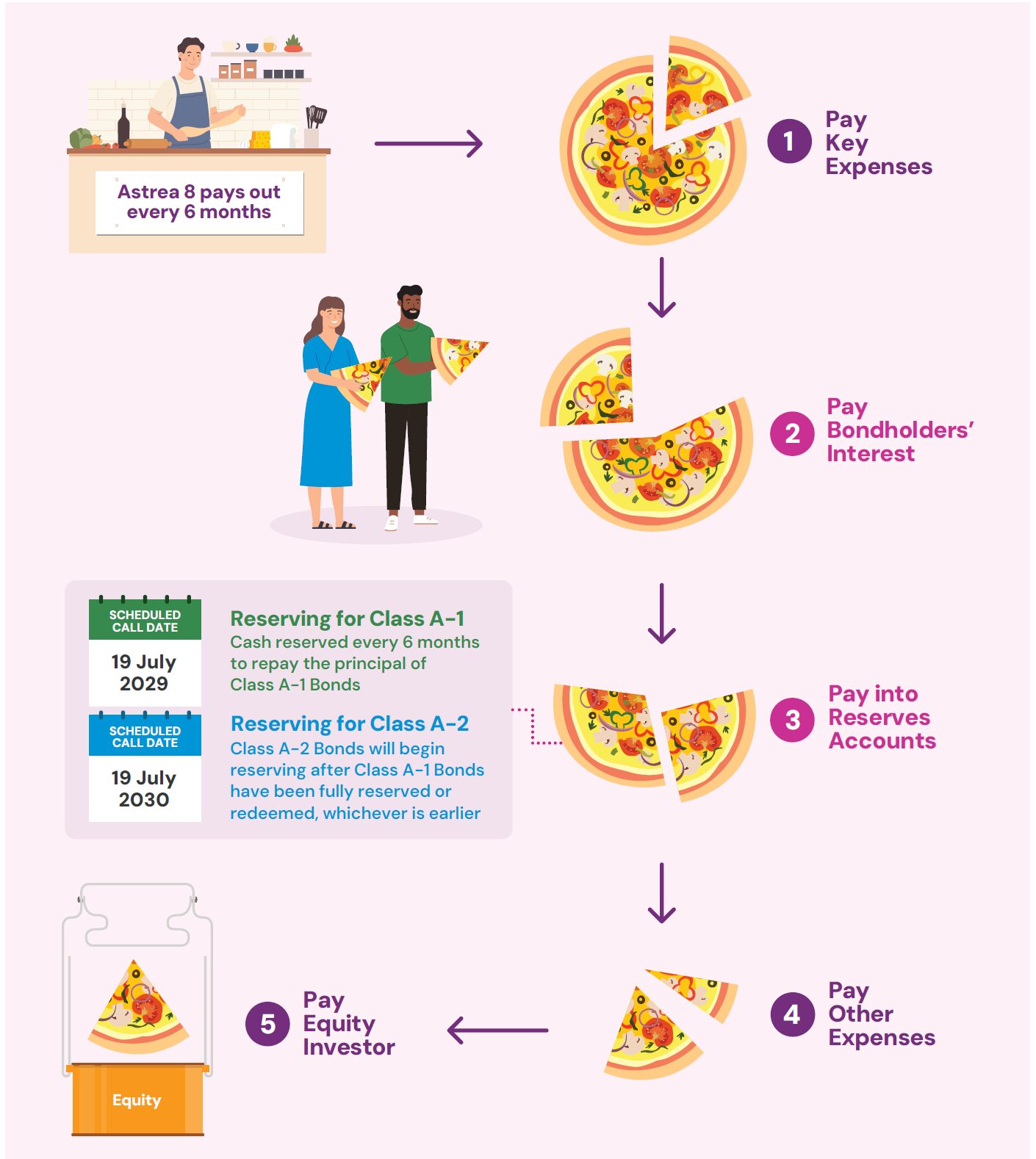

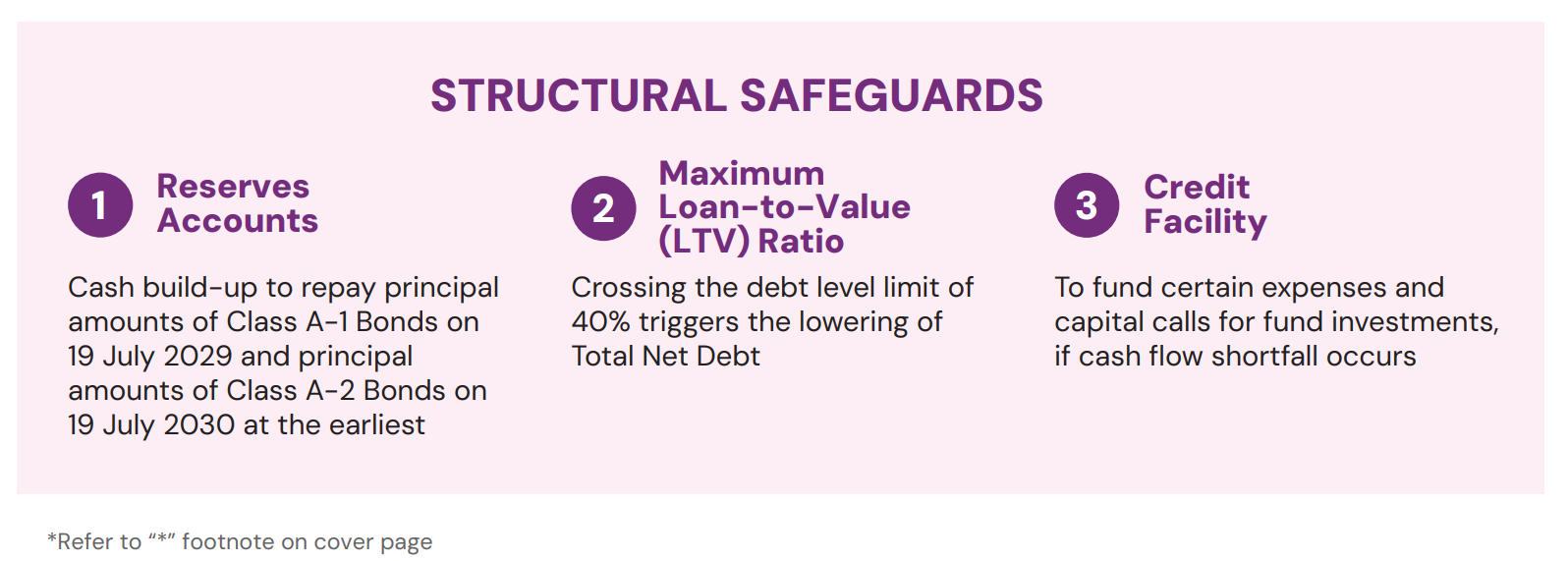

Astrea 8 has pretty similar structural safeguards to previous rounds of Astrea bonds, which you can see below.

The key protections come in 3 forms:

- Overcollateralization

- Diversification

- Portfolio Vintage

Over-Collateralization of Astrea 8 PE Bonds

Think of it like a mortgage.

If you buy a house and only borrow at 40% LTV, you need the value of your house to fall by 60% before you start to reach the value of the debt.

For the bank, this would be a low risk loan – the only difference being that in this case, you are the bank.

I know the most common criticism is that these PE investments are a black box no different from the CDOs that blew up in 2008.

But that’s where the next 2 points come in.

Diversification of Astrea 8 PE Bonds

The underlying PE funds are highly diversified across geographies, fund managers and industries:

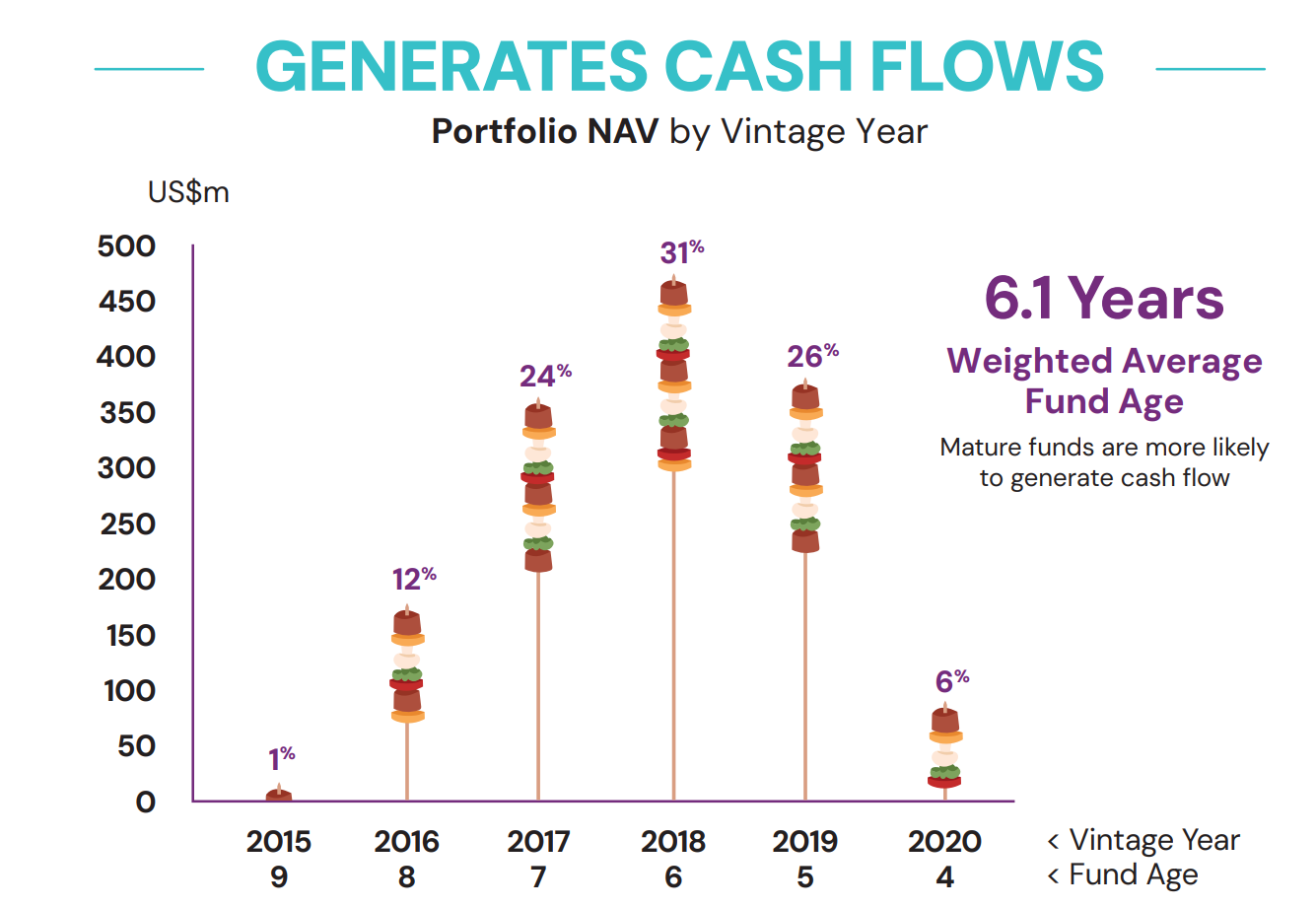

Portfolio Vintage is 6.1 years – and therefore “safer”? Most of these PE funds are from before 2020

You can see the vintage year for the underlying PE Funds below.

This shows the year in which they were created, and generally speaking older is better (as the business has more time to mature and generate cash flow).

The portfolio vintage of 6.1 years means that the bulk of the PE Funds were created before 2020.

The key you would want to avoid is the 2021-2022 period where valuations went crazy from all that COVID liquidity (which means that a lot of bad investments were made by PE Funds during this period).

Of course, the funds are deployed over a couple of years, so some of the 2019 PE funds may have deployed cash in 2021/2022 and so on.

But hopefully with such a long vintage, the underlying businesses will be more mature, and not invested during the crazy valuations of 2021/2022.

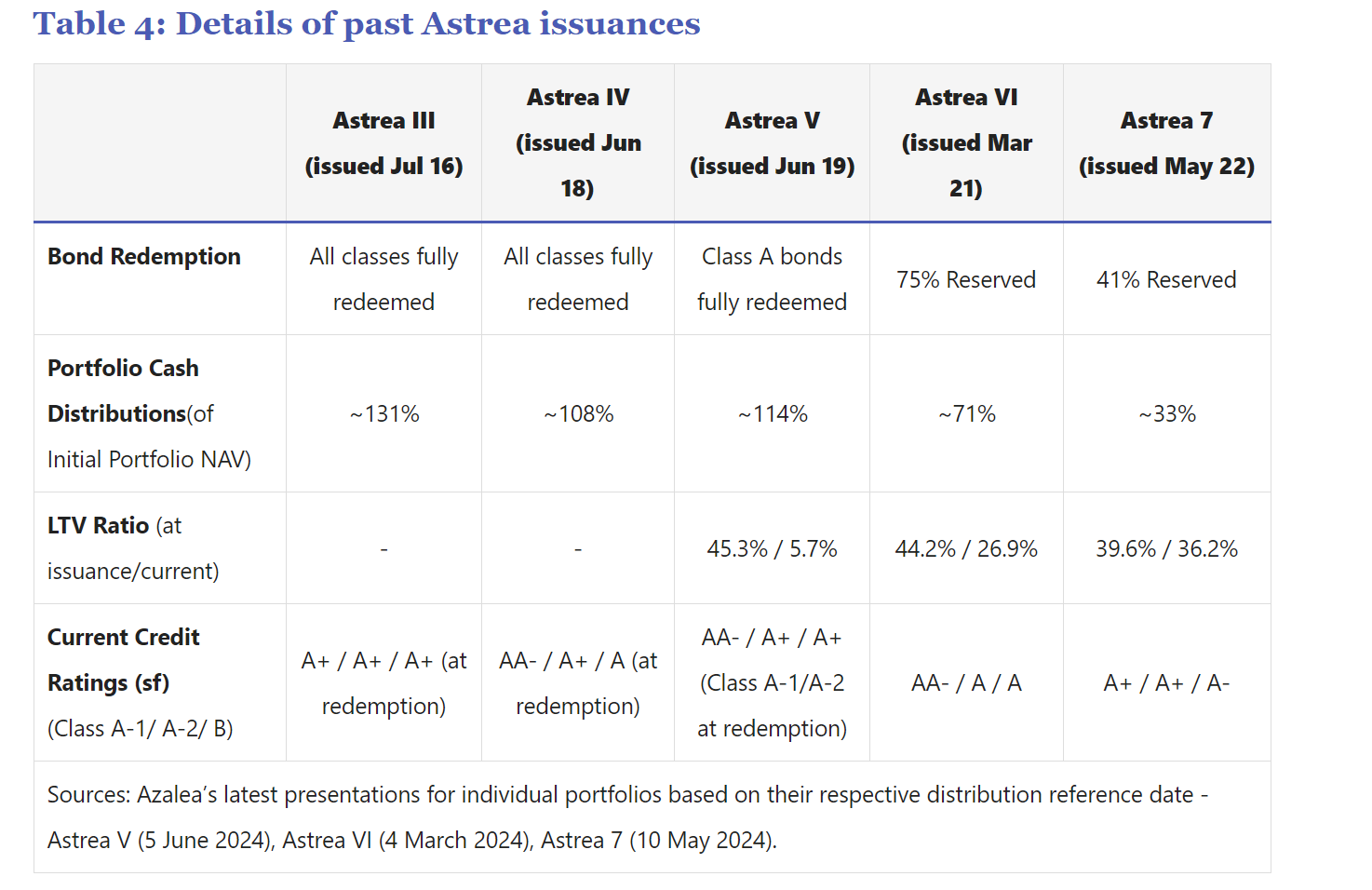

None of the previous Astrea Bonds have defaulted (yet)

The chart from Bond Supermart below the performance of the previous Astrea bonds.

To sum up – none of the Astrea bonds have defaulted (yet).

Both Astrea VI and Astrea 7 are 75% and 41% reserved respectively, so they are nicely on their way to being fully reserved (which means having enough cash set aside to repay the bonds fully).

So… will Astrea 8 PE Bonds default?

The naysayers would argue that in a true financial crisis, it doesn’t matter how diversified you are, the correlation of all these PE Funds goes to one.

And that PE Funds carry a lot of hidden leverage at the fund / portfolio company level.

Such that in a recession, you could see losses for Astrea 8 Bonds despite the 40% LTV and all the safeguards in place.

I mean obviously that is possible.

Nobody is saying that the Astrea 8 PE Bonds are risk free.

If you want risk free for 5 years, buy the Singapore Savings Bonds at 3.19% yield.

My personal view – how risky is Astrea 8 PE Bonds?

Personal view – I think that objectively, the risk of default of the Astrea 8 PE Bonds is low, given the structural safeguards in place.

If a diversified portfolio of PE Funds like that with a 6.1 year vintage experiences a >60% loss in value, you’re looking at depression level economics for the global economy already.

Similar to the previous rounds of Astrea bonds, I think the risk is low.

But for obvious reasons, this is not a zero risk investment.

The better question to ask is whether the yield spread is sufficient to compensate you for the risk.

And as shared above, I do think the 1.16% on the yield spread on the SGD Class A-1 Astrea 8 PE Bonds is a bit low, whereas the USD Class A-2 bonds look more attractive.

Will I be applying for the Astrea 8 PE Bonds? SGD Class A-1 or USD Class A-2?

Let me cut to the chase.

Yes I will be applying for the Astrea 8 PE Bonds.

I will likely apply for both tranches, but current thinking is that I may apply for more of the USD Class A-2 Astrea 8 Bonds.

I share more on my thought process below.

Is the SGD Class A-1 Astrea 8 PE Bonds too expensive? Lots of options for risk free SGD yield today?

I haven’t made up my mind, but I’m inclined to apply for more of the USD bonds than the SGD bonds.

The problem I see is that the Class A-1 only yields 4.35%.

You’re taking on all that credit risk, for only a 1.16% yield uplift vs a risk free Singapore Savings Bond (which can be redeemed any time with no loss).

That doesn’t seem like a great deal to me.

For SGD you might be better off just parking in a mix of T-Bills and Singapore Savings Bonds instead, which is completely risk free.

There are just a lot of other options for SGD cash, for a Singapore investor today.

USD Class A-2 Astrea 8 Bonds offers better “value” for a Singapore Investor?

Whereas with the USD Class A-2 it’s at least a 2%+ spread vs the 10 year US Treasury.

And on a nominal basis – the 6.35% is a lot higher.

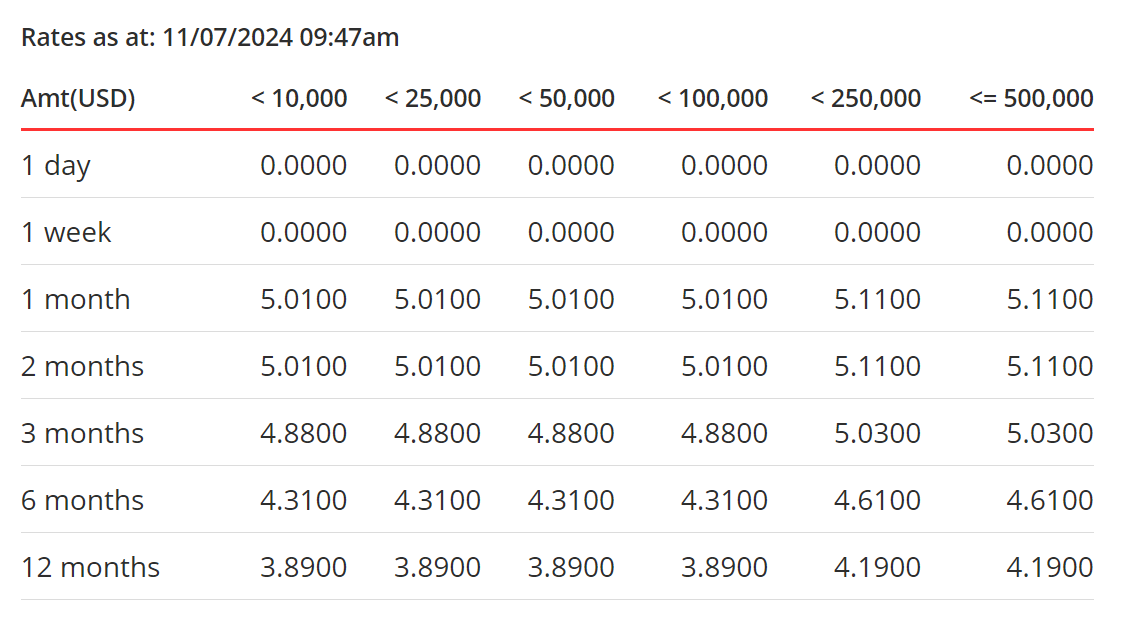

These are the latest USD Fixed Deposit rates offered at DBS.

Yes I’m still getting 5.01% at the 1-2 month, but it falls off quite sharply at 6 months or more.

So for a Singapore investor, the USD option for Astrea 8 Bonds is actually pretty decent as I don’t have a lot of readily available alternatives (to invest that USD in a low risk corporate bond without withholding tax).

Interest rate cuts are coming in Sep 2024

Note also that with the comments from Jerome Powell this week, it looks like a September rate cut is all but a done deal at this point.

The Astrea 8 PE Bonds were priced before this news came out, so in some way you are “earning” from this spread as interest rates fell across the board this week (which is why you saw the jump in REIT prices).

What about the FX risk on the Class A-2 USD 6.35% Astrea 8 Bonds?

If you think about it, the credit risk for the USD and SGD Astrea 8 bonds is the same.

Which means that the key difference is FX.

A 2% higher yield over 5 years is sufficient to cover roughly a 10% FX depreciation in the USD.

This means that as long as the USD is higher than 1.215 in 5 years (vs 1.34/1.35 today), you’re probably ahead with the Class A-2 Astrea 8 PE Bonds.

I’ve extracted the 20 year chart for the USD/SGD pair below, the blue line is the key leve where you would be underwater.

Of course if the US does a lot of money printing we could see the USD depreciate well past that point.

But for now that’s a risk I’m willing to take, for the higher yield.

Worst case I can always sell the USD bonds before maturity to get the USD back, if it the outlook for the USD is terrible (I actually did that with Astrea 7 – I sold the USD Bonds for a profit and parked the cash in a DBS USD Fixed Deposit earning 5.0%).

What split would I apply for? SGD Class A-1 vs USD Class A-2 Astrea 8 PE Bonds?

My current thoughts are to split it 1/3 and 2/3 between Class A-1 and Class A-2 of the Astrea 8 PE Bonds.

Which means that hypothetically if I were applying for $30,000 worth of Astrea 8 PE Bonds.

I would apply $10,000 SGD for the SGD Class A-1.

And $20,000 SGD (whatever is the USD equivalent) for the USD Class A-2.

This gives a blended yield of about 5.7% for broadly similar credit risk, with the caveat that 2/3 of it has USD FX risk.

But I haven’t made up my mind, and I plan to ponder on it further over the weekend.

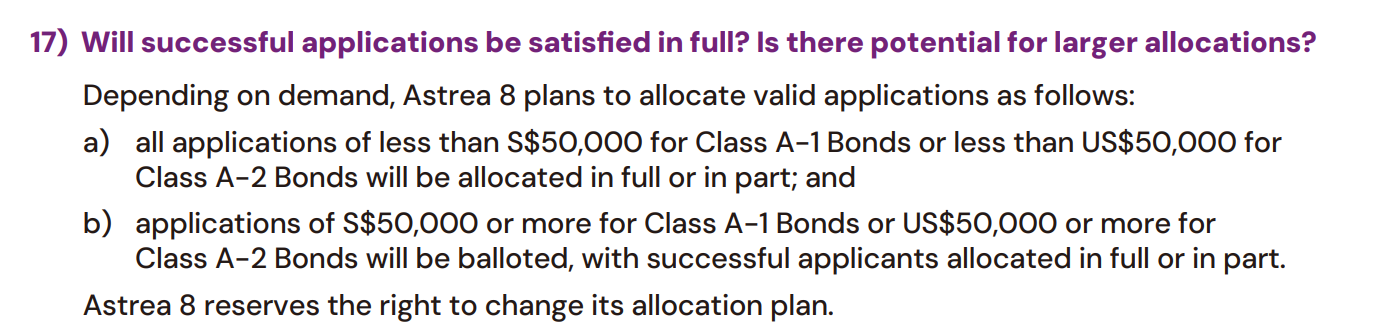

Allotment / Balloting of Astrea 8 PE Bonds

From the FAQs:

Depending on demand, Astrea 8 plans to allocate valid applications as follows:

a) all applications of less than S$50,000 for Class A-1 Bonds or less than US$50,000 for Class A-2 Bonds will be allocated in full or in part; and

b) applications of S$50,000 or more for Class A-1 Bonds or US$50,000 or more for Class A-2 Bonds will be balloted, with successful applicants allocated in full or in part.

Astrea 8 reserves the right to change its allocation plan.

The way I’m reading this (and correct me if I’m wrong).

Is that everyone who applied for less than $50,000 will all get an allocation (whether in full or in part).

And everyone who applied for $50,000 and above will be balloted.

Apply less than $50,000 for guaranteed allotment of Astrea 8 Bonds ($50,000 or more for the ballot)

This means that if you want a big amount of Astrea Bonds (and you don’t want some tiny allocation) – apply for $50,000 or more.

There will be a ballot, and if you are successful in the ballot you will probably get a decent amount.

But if you want a guaranteed allotment, apply for less than $50,000.

There will be no ballot in this case, and everybody will get an allotment (but allotment may be small depending on how strong the demand is).

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Astrea 7 Balloting Results for reference

Just to give you some indication, the Astrea 7 balloting results were as follows:

- Class A-1 (SGD) – Anyone applying S$9,000 and below gets full allocation

- Class B (USD) – Anyone applying US$25,000 and below gets full allocation

Exchange rate is locked in at 1.35:1 (for USD Class A-2 Astrea 8 Bonds)

If you’re applying for the Class A-2 USD Astrea 8 Bonds.

The USD:SGD exchange rate is locked in at 1.35.

Yes I know that the latest USD/SGD FX is 1.34ish so this looks like a bad deal, but US interest rates also went down the past few days which makes the 6.35% yield look comparatively better.

So you can’t really have your cake and eat it.

No FX risk if your application is refunded (for USD Class A-2 Astrea 8 Bonds)

Note that there is no FX risk for an unsuccessful application, per the FAQ below.

You will be refunded in SGD if your application (for the Class A-2 USD) is unsuccessful:

Would I be exposed to foreign exchange volatility if my application for Class A-2 Bonds is unsuccessful or partially allocated?

No, all refunds of unsuccessful or partially allocated applications will also be credited in S$ based on the same predetermined exchange rate of US$1.00:S$1.35 during application.

if you buy the USD tranche, can you get the money back in USD?

I received a couple of questions from readers such as the below:

My experience with USD securities on SGX is that the coupon / dividends payments are made in SGD. CDP converts to SGD automatically. I presume, the same will happen with the principle one day. That’s rather irritating because I may not want to convert. Is there any way to avoid this?

This is the FAQ from Astrea:

Do I receive interest and principal payments for the Class A-2 Bonds in US$ or S$?

Although interest and principal payments on the US$ denominated Class A-2 Bonds are made by the Issuer in US$, if you are a direct securities account holder of CDP who has applied for CDP’s Direct Crediting Service (allowing CDP to credit cash distributions into your designated bank account), you will receive these payments in S$ by default (converted by CDP at such exchange rate provided by CDP’s partner bank).

You may opt-out from receiving payments in S$ via CDP Internet. Upon opting out, your foreign currency cash distribution will not be converted. It will remain in your cash balance with CDP. Please note there is telegraphic transfer fee imposed by CDP in addition to applicable receiving bank charges per withdrawal request.

For more information, refer to the Currency Conversion Service (CCY) section under CDP’s FAQ page at https://www.sgx.com/cdpfaqs.

I would say the dividend is fine to receive in SGD.

But for the principal yes I would generally prefer to get it in USD.

In which case the easiest solution may be to just sell before maturity, and your broker will transfer the USD to you.

I did this for Astrea 7 and I have a nice chunk of USD in a DBS Multiplier now.

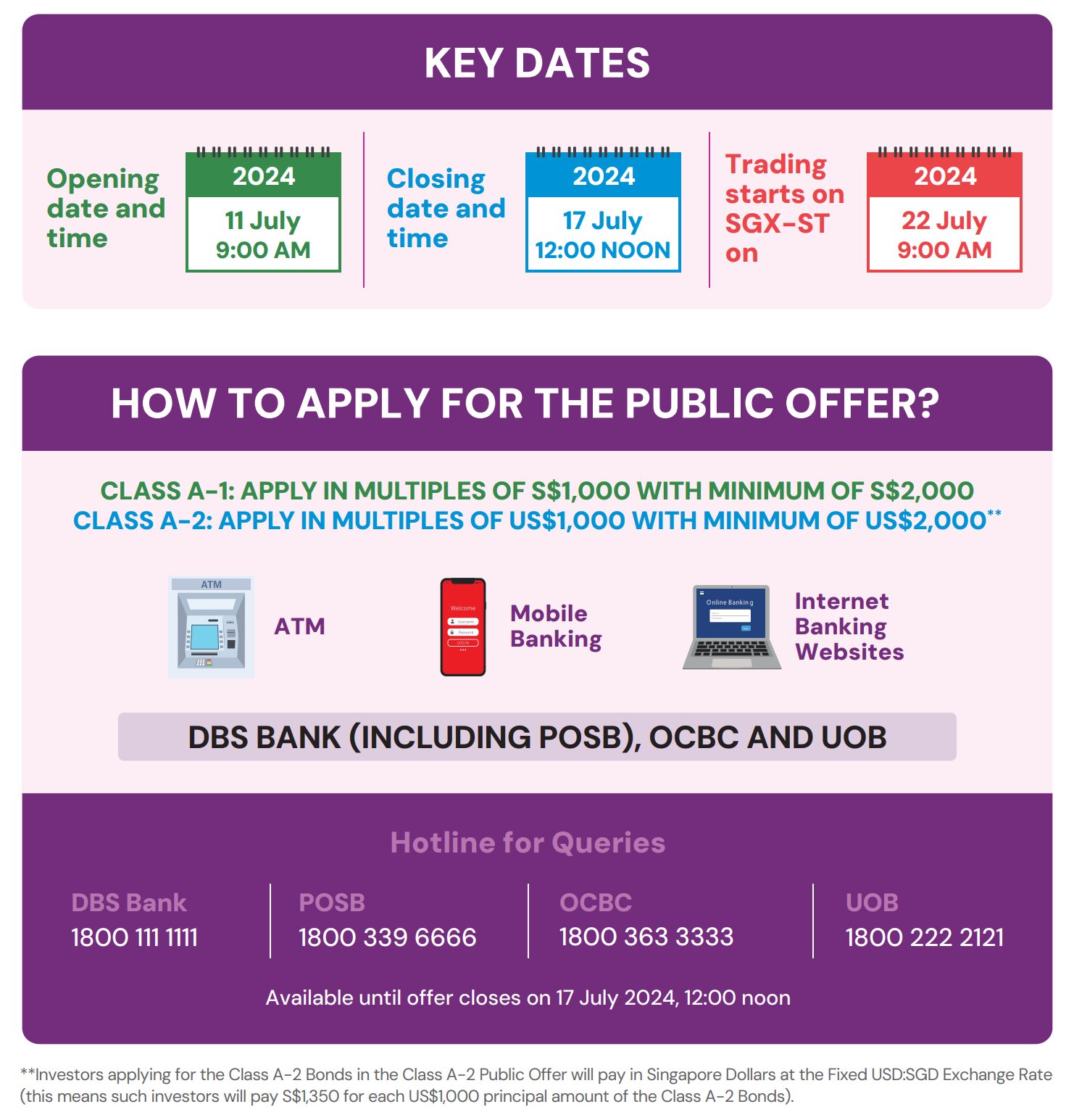

How to apply for the Astrea 8 PE Bonds? Same as a usual IPO

If you’re keen to apply, the key dates are

Opens Thursday, 11 July 2024 at 9 am

Closes Wednesday, 17 July 2024 at 12 noon

Application process is exactly the same as any other IPO.

Via ATM, internet banking, or mobile banking for any of the 3 local banks (DBS, OCBC, UOB Bank).

Closing Thoughts: Astrea 8 PE Bond yields are generally in line with market yields on the previous Astrea Bonds

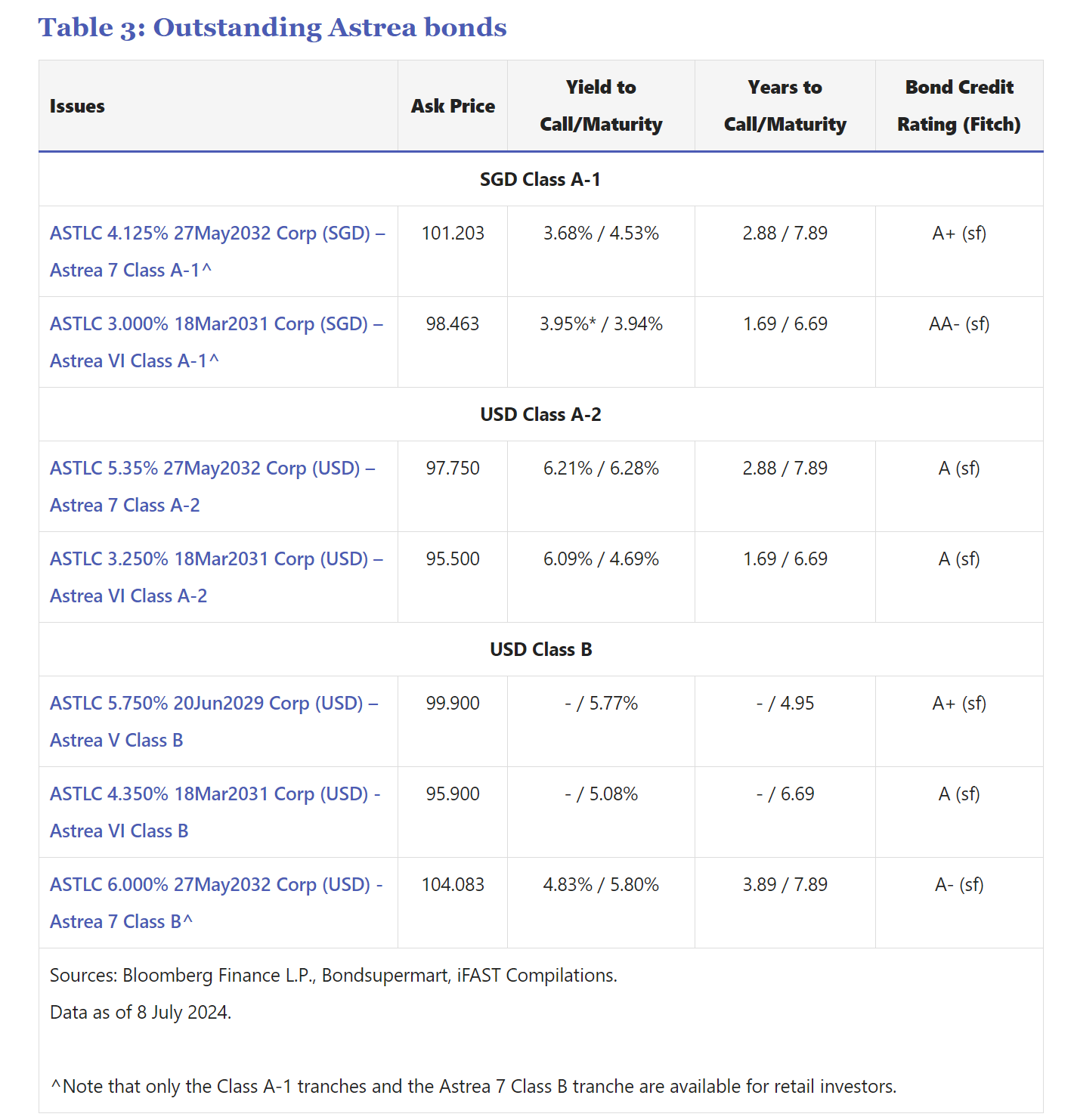

For the record, this is how the Astrea bonds are trading on the market.

You’re looking at about 3.7 – 4.0% yields on the SGD A-1.

And about 6.1 – 6.2% on the USD A-2.

Note that the years to call for those bonds are less than 3 years, so the duration is very different (and therefore not so indicative).

From Bond Supermart

Astrea 7 Class B USD is trading above water – 4.8% yield to call

Interestingly, the Astrea 7 Class B bonds is trading at a 4.8% yield to call on the market (much lower than the Astrea 8’s 6.35% for the USD tranche).

But Astrea 7 is 41% reserved, which I suppose is why the market views Astrea 7 as “safe”.

Trading liquidity on the Astrea Bonds is extremely poor

Do note that trading liquidity on the Astrea Bonds are very poor, you’re typically looking at 10,000 volume a day kind of numbers.

If you really need the cash back before maturity you *should* be able to sell on the market, but you’ll be subject to wherever market prices are at that point in time.

Love to hear your thoughts!

Will you be applying for the Astrea 8 PE Bonds?

Are you buying the SGD Class A-1, or the USD Class A-2 Astrea 8 Bonds?

This article was written on 12 July 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

4.20% on first $20,000 if you deposit to Chocolate Finance (but note that this is not risk free)

I wrote a detailed review on Chocolate Finance, so do check if out if you are keen.

Long story short is that Chocolate finance pays 4.2% on the first $20,000, withdrawable instantly.

The funds are invested in a selection of bond and money market funds, and Chocolate Finance will top up any returns if they are lower than 4.2%.

To be clear this is not SDIC insured and not risk free.

So I leave it for investors to decide if you are comfortable with the risks (see my full review here).

Chocolate Finance currently is invite only, but you can use the FH invite link below if you are keen to try it out:

https://share.chocolate.app/nxW9/ep4q7wxp

– Get USD 400 cash voucher

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 400 cash voucher.

You just need to:

- Deposit USD 2000 (or 10,000 for higher rewards)

- Execute 5 trades (for higher rewards)

Note that Webull is also offering zero commission for US options trading right now.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

hi, would appreciate it greatly if u could suggest where to get the most favourable exchange rates for converting sgd to usd (after accounting for fees, spreads, commission, etc.) thx

You cannot buy the Class A-2 bonds with USD. You can only buy with SGD, at the fixed rate of 1.35.

one of the best review of astrea8 compared to those currently online.

i too am inclined to sub to the A2 USD version. not sure what amount yet. the A1 SGD is a tad too low.

a few questions though”

“A 2% higher yield over 5 years is sufficient to cover roughly a 10% FX depreciation in the USD.”

– how do you calculate this 10% FX depre?

also, if i already have USD in my DBS multiplier., can i just use this stash of USD instead of using their 1.35 fixed FX ?

Thanks for the kind words.

On your questions:

1. Simplistically, 2% a year over 5 years is 10%. Of course there is some compounding effects and so on, so realistically a 8-12% move in the FX.

2. Unfortunately no. You can only buy in SGD, and the interest rate is locked in at 1.35.

Is it possible to buy the A2 tranche using USD directly?

Not possible unfortunately. You can only buy with SGD, at the fixed rate of 1.35.