In last week’s article, I asked if you guys wanted a deep dive into bonds.

Boy… the response was overwhelming:

Please do a deep dive for Bond Funds. Always talk about Reits and Banks is quite stale.

Second that! Do a primer on bond funds for retail investors! Is it better to ETF or go with active managed? If active, which funds and which platform? Which geographies and high yield or investment grade? Any tax implications we need to take note of?

The issue here is how to invest the bulk of the cash & bonds, and have it earn the stated returns with little to no risk. If a chunk of my funds are in CPF OA (eg $1million earning 2.5%), would you consider that as “bonds”? What would you recommend?

So… let’s do it.

Let’s discuss how a Singapore investor can build a bond portfolio that generates decent yield, without excessive risk.

How to get 5.5% yield buying Bonds in 2024?

The logic is similar to stocks.

There are 3 ways you can buy bonds:

- Buy individual bonds by yourself

- Buy a bond ETF

- Buy a bond fund

In my personal view – a mix of Option 1 and Option 3 is the best approach (and what I have been doing myself).

But I know not everyone agrees with me, so let’s walk through each of the 3 options.

Buy individual bonds by yourself

Now the main problem with buying bonds by yourself.

Is that most of the “good” bonds from say DBS or HSBC or SIA are not offered to retail investors.

Which means that you need to be an accredited investor to buy, and in many cases the minimum subscription amount is as high as $250,000 (not to mention the hefty transaction fees).

Even if you had $1 million to invest in bonds, you would only be able to buy 4 – 5 bonds, and that’s a lot of concentration risk.

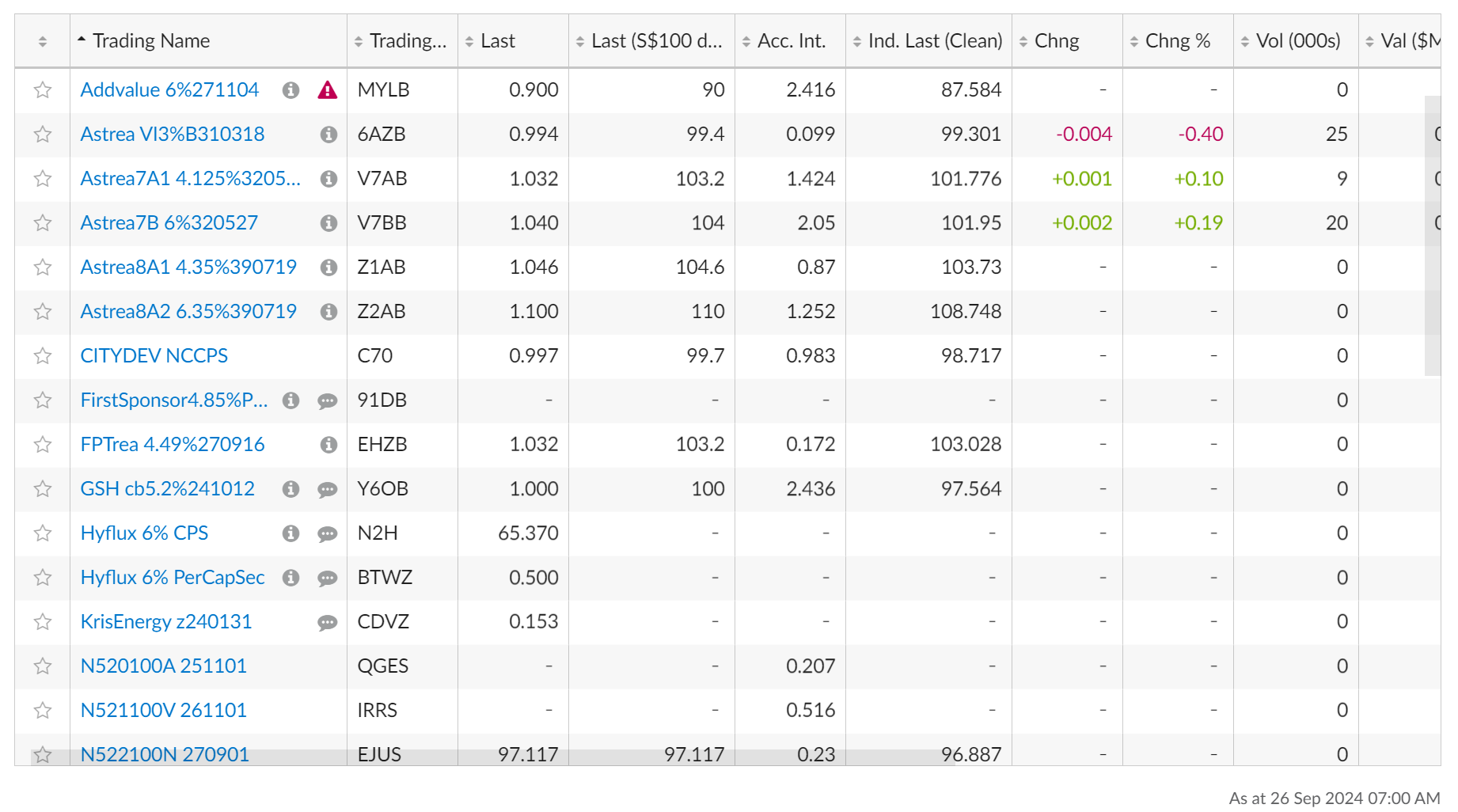

The alternative is to buy retail bonds – bonds from Astrea, Frasers Property etc.

The main problem is that there are very few of such bonds.

You can go to SGX and look at the full list of retail bonds, the list is miniscule:

And let’s say you decided you want to buy Astrea 8A1 on the open market.

This is what the trading liquidity looks like – close to non-existent.

Long story short is that yes you can buy individual bonds, and I myself will buy the occasional bond as well.

But on a portfolio basis – the challenge is in assembling a diversified bond portfolio by yourself (in a way that provides decent exit liquidity if ever required).

It’s just not easy.

Buy a bond ETF

Then we have bond ETFs.

Note that you cannot use US listed bond ETFs because of withholding tax (30% withholding tax), which means you’re largely confined to SGX or LSE (London).

Singapore Listed Bond ETFs

Nikko AM SGD Investment Grade Corporate Bond ETF is one of the larger bond ETFs listed in Singapore ($600 million AUM).

Fees are dirt cheap too – a mere 0.26%.

You can see the top holdings below – it’s a nice mix of bonds from Temasek, DBS, HSBC, NTUC, UOB and so on.

The main problem though, is the yield.

Yield to maturity for the bond portfolio is about 3.4%.

Yes this is higher than the 5 year Singapore government bond yield (2.4%), but objectively it is still on the low side.

London Listed UCITS Bond ETFs

The alternative is to use a LSE listed UCITS ETFs.

This gets around the withholding tax issue.

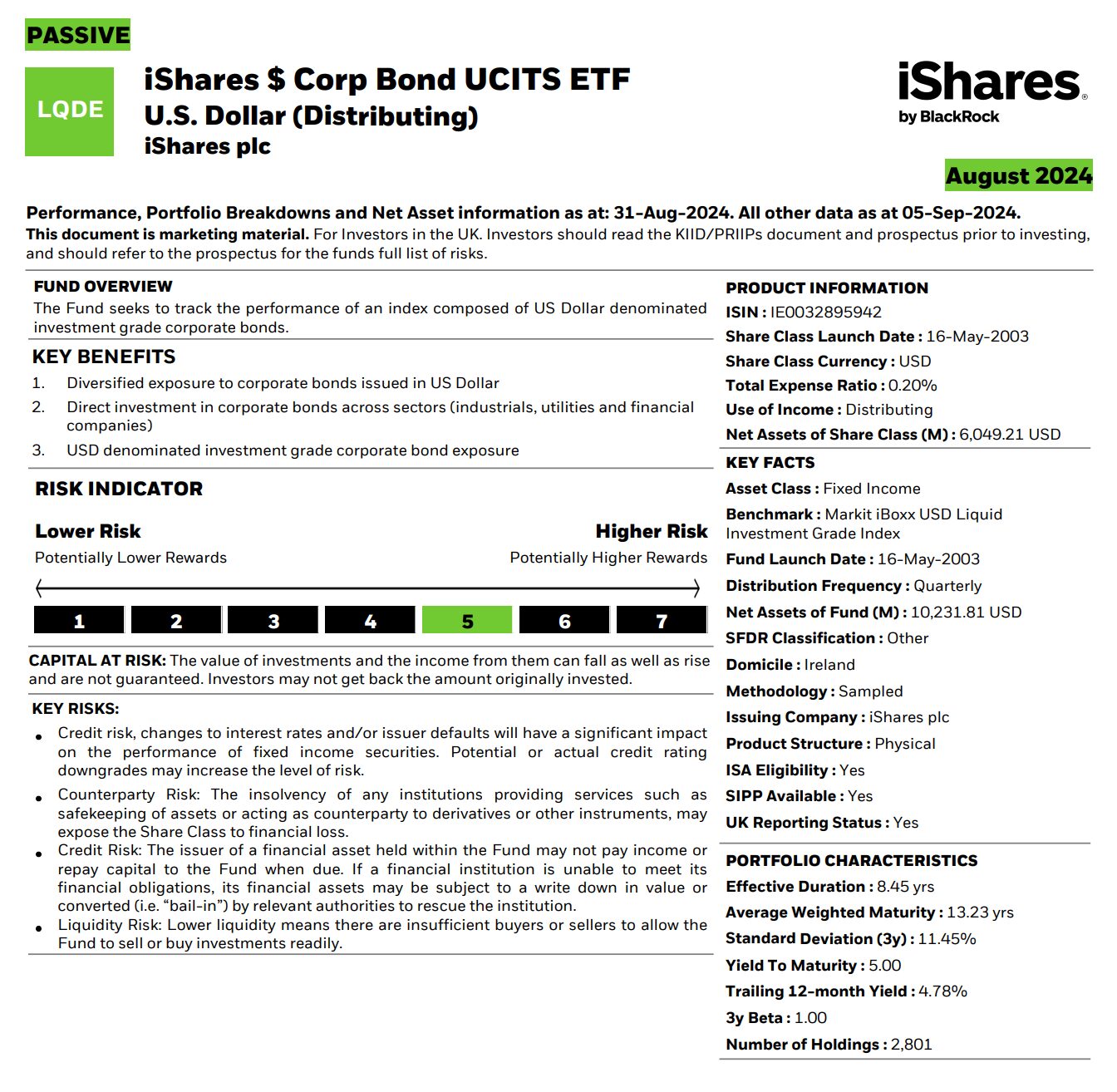

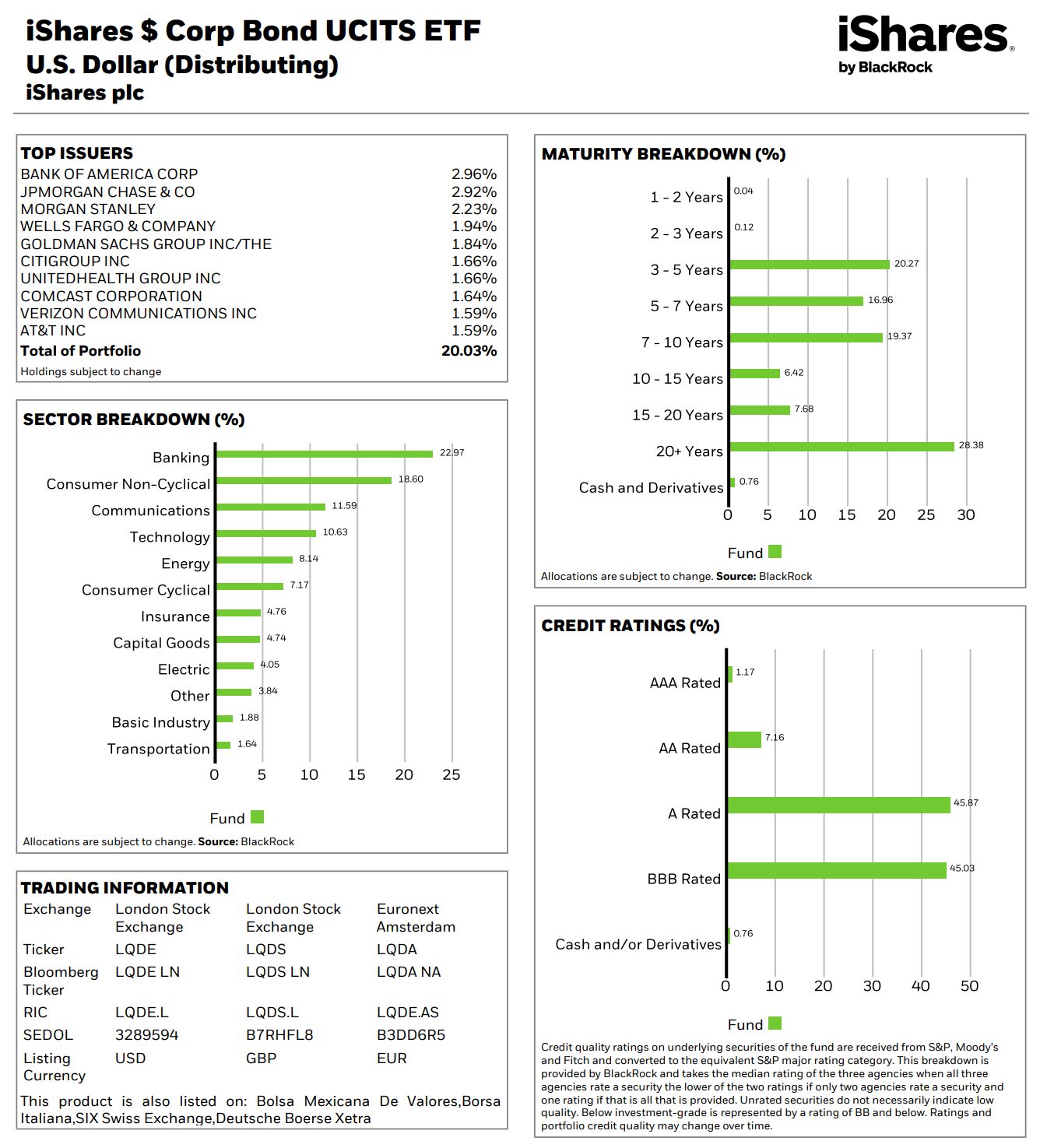

Here’s iShares $ Corp Bond UCITS ETF U.S. Dollar for example.

$10 billion AUM, 0.20% expense ratio, yield to maturity of 5.0%.

Nicely diversified as well across industries and durations:

The main problem though in my view – is FX risk.

Why FX Risk is so crucial for bonds?

The difference when you buy bonds is that the upside you make is largely capped to the coupon (the yield).

Let’s say you buy a USD bond yielding 5%.

And the USD depreciates by 10%.

That’s 2 years worth of yield risk there.

Because of that, as a bond investor it does not make sense to take on the FX risk, in exchange for a fixed return (unlike equities where the upside is theoretically unlimited).

If you buy a bond ETF like that, the biggest risk in my view is the FX.

Sure you can hedge FX by hedging the SGD/USD pair yourself, but hey that brings a whole different level of complexity (and cost) to the table.

Buy a bond fund

The other solution – is to buy a bond fund.

If you buy a SGD hedged UCITS bond fund (and you should), then the fund manager will take care of the SGD hedging for you, and the withholding tax should not be an issue because of the UCITS structure.

Both Endowus and Syfe offer a pre-curated bond fund portfolio that you can use (or *cough* learn from) as a Singapore investor:

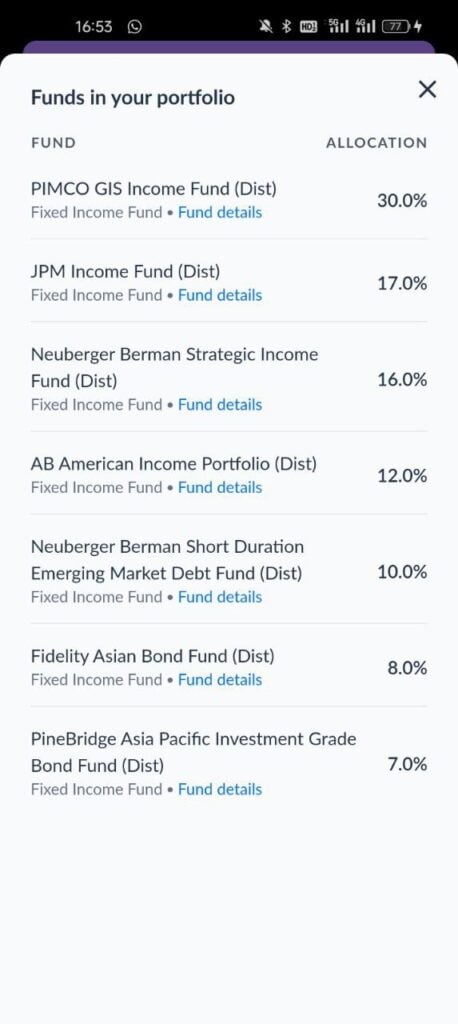

Endowus Income Bond Fund Portfolio

The bond funds are:

- PIMCO GIS Income Fund (Dist) – 30.0% allocation

- JPM Income Fund (Dist) – 17.0% allocation

- Neuberger Berman Strategic Income Fund (Dist) – 16.0% allocation

- AB American Income Portfolio (Dist) – 12.0% allocation

- Neuberger Berman Short Duration Emerging Market Debt Fund (Dist) – 10.0% allocation

- Fidelity Asian Bond Fund (Dist) – 8.0% allocation

- PineBridge Asia Pacific Investment Grade Bond Fund (Dist) – 7.0% allocation

Syfe Income+ Preserve Bond Fund Portfolio

The bond funds are:

- PIMCO GIS Global Bond Fund (40%)

- PIMCO GIS Income Fund (32%)

- PIMCO GIS Asia Strategic Bond Fund (13%)

- PIMCO GIS Global Investment Grade Credit Fund (10%)

- PIMCO GIS Asia High Yield Bond Fund (5%)

What is the estimated yield?

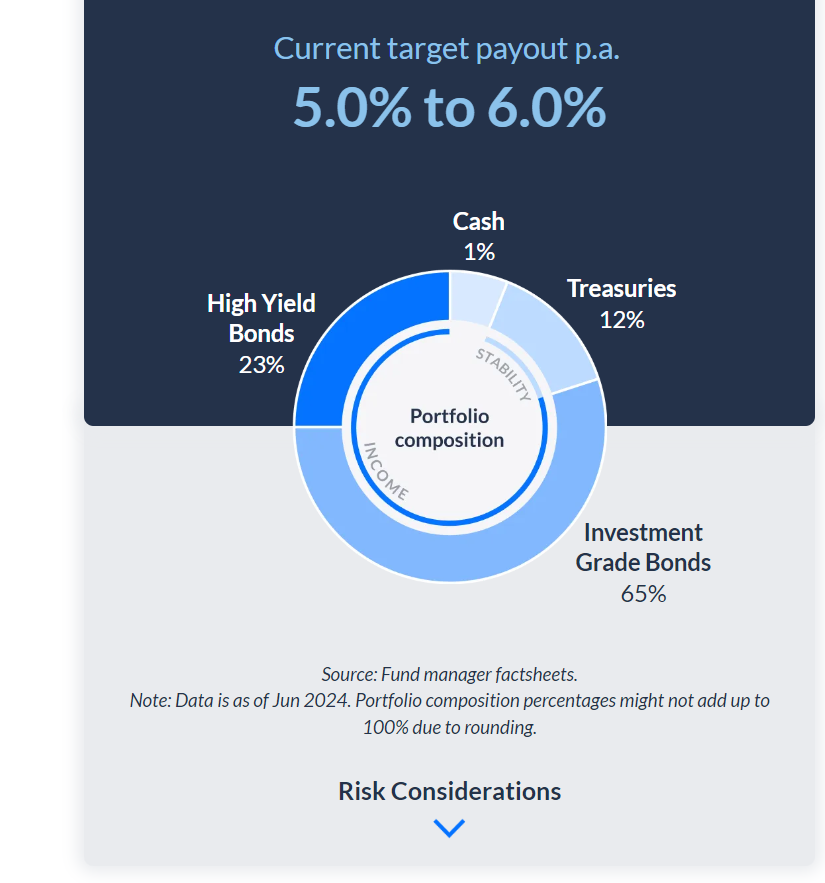

For Endowus they project the yield to be about 5.0 – 6.0%, while Syfe projects about 5.0 – 5.5%.

Diversification (with decent yield)

Let’s look further into individual bond funds.

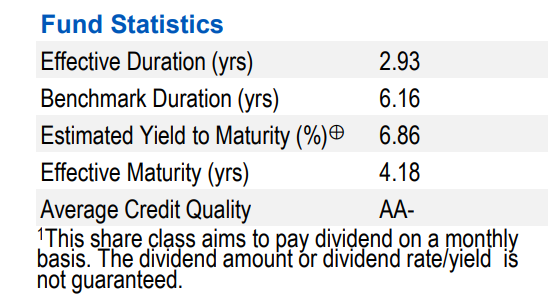

Take the PIMCO GIS Income Fund for example – which features prominently for both Endowus and Syfe.

Estimated yield to maturity is about 6.8%.

Even after you hedge that back to SGD, and even after fees, yield should be decent.

What kind of bonds are you holding?

The bulk of it is US bonds – with a good chunk of it coming from mortgage backed securities from Fannie Mae (this may give you 2008 chills, but to be fair the situation has been cleaned up massively from 2008).

And don’t forget that’s just one bond fund.

Let’s say you throw in PIMCO Asia Strategic Interest Bond Fund (SGD Hedged), and it gives you vastly different exposure to Asia instead:

So by using a portfolio of bond funds as Endowus / Syfe as done, you can construct a broadly diversified bond portfolio across geographies and industries.

Average duration is about 4 – 5 years, which I think is the sweet spot to lock in yields, without excessive duration risk (the risk of capital loss if interest rates go up – a real problem if you use >10 year bonds)

What is the default risk?

What I would say is this.

If you want risk-free it’s a 5 year Singapore government bond at 2.45%.

If you want to earn a higher yield, by its very nature you have to accept some level of risk.

And if you take $1 million and buy 4 different bonds from your private banker, if one of them defaults (the Credit Suisse AT1 saga for example) you’re looking at a 25% loss in capital.

So its not a great solution either.

The benefit of the bond funds is that because its so diversified globally and across industries, it diversifies away the single issuer risk.

Then the risk becomes more one of a macro risk, which cannot be diversified away if you want a return higher than the risk free rate.

You can protect again such risk through more active macro investing, but then it goes back to the kind of investor you are).

The downside – much higher fees?

While bond funds solve the diversification, yield, SGD hedge, and withholding tax issues.

The biggest downside is the fees.

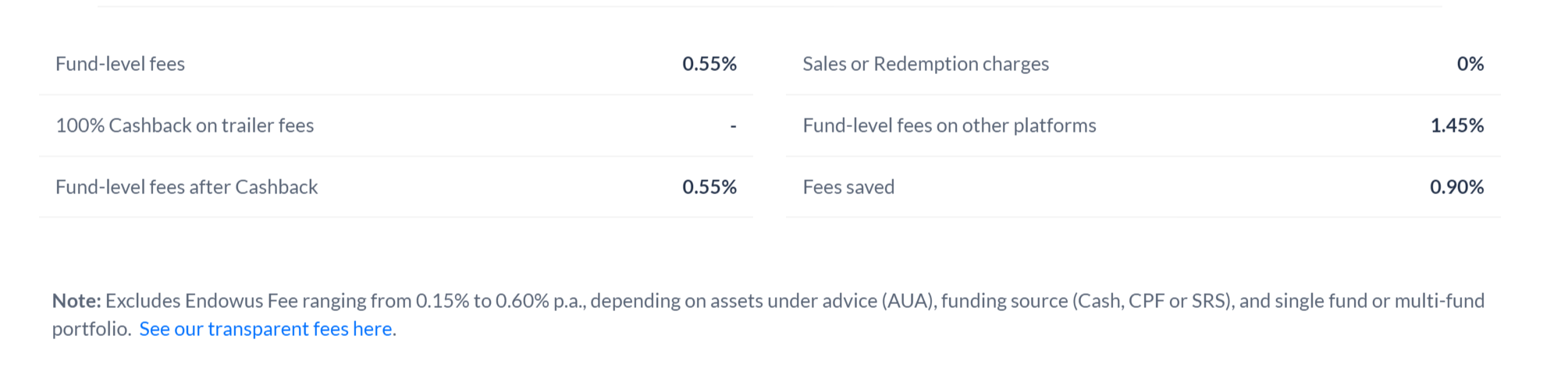

Let’s say you buy via Endowus with the trailer fee rebate.

You’re looking at about 0.55% fees from the fund (after trailer fee rebate), and 0.60% from Endowus (if below $200,000).

That’s an all-in fee of about 1.1 – 1.2%.

You can check on Syfe or FSMOne or Bond Supermart and it typically works out to about the same all-in fee (may be higher if you go via private banking).

Taking Endowus’ estimated payout of 5-6%.

A 1.1 – 1.2% all-in fee works out to anywhere from 20-25% of your potential payout (before factoring in capital gains).

As one FH Premium subscriber put it:

…we need to pay at least 1.5pc mgt fees pa for a projected 5pc yield, that is like giving away 30pc of our dividends away to the bond fund manager, seems exorbitant in my opinion.

Okay it’s more like 20-25%, but yes it’s still a lot.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

So… which is the best way to get decent yield buying Bonds in 2024? (as a Singapore Investor)

To sum up the discussion above.

The problem with buying bonds yourself is that it’s hard to get meaningful diversification.

The problem with using a Bond ETF is that aren’t that many Singapore Bond ETFs, and the ones that exist don’t have very good yields.

And if you use a LSE listed Bond fund, you’re opening yourself up to FX risk.

The problem with buying Bond funds is that the fees are high, but that said it does solve the diversification, yield, FX risk and tax issues.

So… what’s a Singapore investor to do?

Which is the lesser of the evils?

My personal view, and this is what I’ve been doing, is a mix of Option (1) – Buy Individual Bonds and (3) – Buy bond funds.

I buy the Astrea bonds (and whatever other individual bond if I find the risk-reward attractive – perhaps even stuff like Netlink Trust) whenever they come along.

But those alone are not enough (nor sufficiently diversified) to build a bond portfolio.

So I throw in some bond funds into the mix for diversification and a higher yield.

Yes I know that the bond funds come with 1.1 – 1.2% all-in fees which are not cheap.

But frankly it’s the lesser of the evils in my view.

Of course, on top of that I supplement that with stuff like T-Bills, Singapore Savings Bonds etc but I view those more as cash rather than bonds.

Which Bond Funds to use?

Some of you have asked which bond funds to use.

You can see above that both Syfe Income and Endowus Income have pre-curated a list of bond funds for you.

And frankly the way they do it is very instructive.

Personally I like Endowus Income’s portfolio more, which I extract below:

- PIMCO GIS Income Fund (Dist) – 30.0% allocation

- JPM Income Fund (Dist) – 17.0% allocation

- Neuberger Berman Strategic Income Fund (Dist) – 16.0% allocation

- AB American Income Portfolio (Dist) – 12.0% allocation

- Neuberger Berman Short Duration Emerging Market Debt Fund (Dist) – 10.0% allocation

- Fidelity Asian Bond Fund (Dist) – 8.0% allocation

- PineBridge Asia Pacific Investment Grade Bond Fund (Dist) – 7.0% allocation

You will note that there is a very heavy US focus on these bonds, and that is by design.

The universe of corporate bonds in Asia is just nowhere as developed as the US, and a big part of that is China High Yield bonds (which you want to stay away from given the challenges China is currently going through).

How to buy a bond fund? Which is the cheapest platform?

Some of you have asked the best way to buy a bond fund.

There’s broadly 2 options:

- Buy via Endowus, Syfe, FSMOne, Bond Supermart etc

- Buy via your private banker

In my experience (1) usually tends to be cheaper than (2), but it does vary depending on the fund in question and the promotion in play.

And within (1), Endowus tends to be quite competitive because of the trailer fee rebate, but again it really depends on the fund as some may be cheaper on FSMOne / Bond Supermart.

If you know exactly which fund you are buying, and are buying a large amount, it’s worth just doing a quick comparison across platforms before you buy.

It’s messy and imperfect I know, but that’s just how it works today.

Promo codes for both Endowus and Syfe below if you need:

Endowus Promo Code

Join me to get S$20 off your Endowus Fee. Use my unique promo code XX9YZ at https://endowus.com/invite?code=XX9YZ

Syfe Promo Code

Hi! I’m using Syfe to invest, join me and earn up to S$200 after account opening and funding.

https://www.syfe.com/invite/wealth/SRPTVERUZ

Closing Thoughts: Cash =/= Bonds

Coming back to this final question:

The issue here is how to invest the bulk of the cash & bonds, and have it earn the stated returns with little to no risk. If a chunk of my funds are in CPF OA (eg $1million earning 2.5%), would you consider that as “bonds”? What would you recommend?

I do think it’s worth differentiating between “cash” and “bonds”.

In my view cash is short duration instruments (less than 12 months) you can access readily. Stuff like T-Bills, Singapore Savings Bonds, Fixed Deposit and so on.

Bonds are medium duration instruments (1 – 5 years) that locks in yield for a longer period, at the expense of liquidity. Stuff like Astrea Bonds, Temasek Bonds, Bond Funds and so on.

If you had $1 million in CPF-OA earning 2.5%, I would classify that as “cash” simply because the yield is not amazing, and technically you can withdraw it any time to pay your mortgage or buy a second property for example.

Whereas if you had $1 million in CPF-SA earning 4.0%, and you are 10 years away from being able to withdraw, that would be more of “bonds”.

As to how to “earn the stated returns with little to no risk”.

Again– risk free rate for a 5 year government bond is 2.45%, so if you want higher yield you do need to accept some risk okay.

Question is what level of risk is acceptable for you, not how to eliminate risk.

The way I would do it is the start with the cash as the base, and then layer on the bond exposure on top (a mix of individual bonds and bond funds) based on risk appetite.

But hey that’s just me – I would love to hear what you guys think!

This post is written on 27 Sep 2024 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Saxo Brokers – Trade the 100 most popular US stocks commission-free

Saxo is running a promotion where new account holders can trade the Top 100 US stocks commission free (more details).

Special account opening bonus for FH Readers:

- Sign up via the link: Saxo Brokers

Chocolate Finance- pays 4.2% yield on first $20,000

Chocolate finance pays 4.2% on the first $20,000, withdrawable instantly.

The funds are invested in a selection of bond and money market funds, and Chocolate Finance will top up any returns if they are lower than 4.2%.

I wrote a detailed review on Chocolate Finance (note not SDIC insured).

- FH invite link below:

https://share.chocolate.app/nxW9/ep4q7wxp

Stock Café – track your portfolio performance (including dividends)

I use StocksCafe to track my portfolio and dividend stocks (full review).

- FH x StocksCafe Referral Code:

https://stocks.cafe/user/tosignup?referral_code=financialhorse

Hi FH,

The question I’m dying to know is – How to get access to US Treasury as a retail investor? Reasonably?

Also, if you bought at 5% yield, would it be reasonable to expect it to jump 20% if interest rates be cut by 1 %?

I actually wrote an article on this previously: https://financialhorse.com/how-to-buy-us-treasury-bonds-yielding-5-0-risk-free-as-a-singapore-investor/

Let me know if this answers your queries, or if there are any issues.

How to buy bonds ?

Bond funds can be bought on endowus but I don’t find option to buy bonds. Please advise, thank you.

You can find it under the Endowus Income or Fundsmart option.

Thanks for the effort.

This is the reality of a Singapore investor. I’ll likely stay put with my CPF OA, even after the end of SA 4% come next year. Call it cash or bonds, it’s risk free, no fees no charges.

The alternative is to take a bar bell strategy or put more into reits or dividend stocks to push up the returns. Else work harder longer to build a bigger savings. Conclusion – it’s NOT EASY to achieve a comfortable 4% passive income as many would want to believe.

That’s a fair comment, I don’t disagree with you. The reality is that if you want to achieve a yield above risk free, you have to accept some level of risk. Question is what level of risk is acceptable – that’s personal to each investor.

I looked at the Endowus Income bond fund performance chart and calculated that the average fund performance is only 2.32% over 8 years (2016 to 2023) after deducting the endowus annual 0.6% fee. Isn’t that rather low for a bond fund? Is my calculation is correct?

I think this is one of those where historical performance =/= future performance.

The pre-COVID era was one of much lower interest rates, and the 2020-2021 era was one of zero interest rates. So bond funds delivered very low returns during that period (because of low interest rates).

The better question is what will returns be like going forward.

Hi FH, i see that in the Endowus and syfe bond fund portofolios, the bond funds’ base currency is in USD but share class currency is SGD – is this what you mean by Endowus and Syfe bond fund portfolio hedges the USD forex risk?

Yes that’s right. You want to use the SGD hedged share class to avoid FX risk.