It’s been a really interesting 2 weeks.

We had a Biden win, we had a 90% efficacy COVID vaccine, and we had the mother of all rotations from tech into value stocks (which was partially undone the next day).

But in today’s article, I wanted to look at another Singapore classic stock – OCBC Bank.

After the massive rally the past week, is it still a good investment?

Note: The research for this article, and most of the charts here, are sourced from ShareInvestor Webpro. It’s a great way to quickly perform research on Singapore stocks, far more comprehensive and flexible than other options like Yahoo Finance.

You can learn more in my review on ShareInvestor Webpro here.

Basics: What is OCBC Bank?

OCBC Bank needs no introduction.

It’s one of the 3 largest local banks in Singapore, alongside DBS and UOB.

Singapore is their largest market (58% of asset base), followed by China (17%) and Malaysia (13%).

The China business is mostly concentrated in Hong Kong, because of OCBC’s purchase of Wing Hang bank in 2014. It’s also why OCBC’s share price hasn’t been doing too great since the trade war and HK protests.

Financials of OCBC Bank

The financials tell the same story as DBS and UOB (and the US and European banks).

Basically:

- Net Interest Income is down

- Fee income is down

- Trading income is up a lot

What is OCBC’s core business?

Now trading income is nice, but nobody really invests in a bank for trading income – those tend to be lumpy, and very one-off.

You buy a bank for its core business – which is lending.

It’s one of the oldest businesses in the world. You borrow money at 2%, you lend it out at 4%, and you earn the spread. And you make sure that the profit is enough to cover the bad loans.

That’s it, it’s not rocket science.

So the profitability depends on 4 things:

- Loan demand

- Interest rate the bank lends at

- Interest rate the bank borrows at

- Bad loans

Let’s look at each individually.

1. Loan demand is weak

There’s a nice chart below which shows the impact on loan demand compared to previous years.

Loan demand has fallen off a cliff.

It’s very different from previous recessions where everybody wanted money, but the banks didn’t want to lend.

In this recession, capital markets are partying like it’s 2000, so it’s very easy for a strong company like Amazon (or Nanofilm) to go to public markets and do a big fundraising. SIA issued a 5 year bond yesterday at 1.625%, and it was four times oversubscribed. You’d never see something like that in 2008 or 1997.

But those are the good ones.

The bad ones, like the weaker airlines, hotels or cruise liners, no bank in their right mind wants to increase exposure to them – because who knows if the loan will be repaid.

So it’s created a situation where the banks want to lend to the strong companies, but they don’t need a loan because they can easily tap capital markets. And the weak companies want a loan but the banks don’t want to lend to them because they fear the loans cannot be repaid.

And hence, very poor loan growth, which is bad for business.

2. Interest rate the bank lends at

Back in March, the Federal Reserve cut interest rates all the way to zero.

Bank loans are pegged to SIBOR, which tracks global interest rates.

And accordingly, the interest rates the bank lends out at has plunged.

Mortgage rates are close to 1% for a 30 year loan these days, which is absolutely ridiculous.

3. Interest rate the bank borrows at

But banks are smart, so they also cut the interest rate on accounts like OCBC360 or DBS Multiplier.

This is how they borrow money, and they’re now able to get money cheaper, which offsets the fall in interest rates.

Long story short – The rate the bank lends out at has fallen, but the rate they borrow at has fallen too. These cancel out to a certain extent, but the net effect is still less profits for the bank.

4. Non-performing Loans

Non-performing loan (NPL) levels are unbelievably low given that we’re in the midst of a pandemic and the worst downturn since WWII.

As at Sep 2020, it’s a miniscule 1.6%, which is exactly the same level it was in Sep 2019.

Because of all the government stimulus, loan reliefs etc, we’re not able to see the full impact of the pandemic just yet. We’ll only start to see the real impact in 2021, when more of the loan reliefs start to run off.

OCBC’s CEO thinks the same:

While 3Q20 saw a recovery from the trough of the previous quarter, we may not have seen the full extent of the lagging economic impact of the crisis yet, which will have more visibility next year. In the meantime, we are proactively following and responding to the government relief programme exits in all markets.

What will 2021 look like?

The million dollar question though, is what is 2021 going to look like.

What we know, is that interest rates will stay low. That won’t change much going forward.

What we don’t know, is:

- Will loan demand pick up?

- How many loans are going to go bad?

And ultimately, this goes back to the strength of the Singapore economy.

Which in turn will depend on:

- How well is COVID handled globally? How quick is the vaccine rolled out?

- How aggressive is the Singapore government with their support?

My personal take?

Personally, I think it’s a really tough call. I genuinely see two possible futures – one with soaring bad debt and another with a flying economy.

It really depends on the vaccine, and the pace of government support.

Sometimes in investing, it’s important to know what you don’t know. And I just think it’s super tough to predict how the economy will play out in 2021.

Let’s put it this way, imagine there is a coin toss. 50-50 chance it lands heads up. If its heads, you win $100. If its tails, you lose $20.

Is this a bet you should take?

Absolutely – as long as you can afford to lose the $20, and go again.

And that’s what investing is like to me. Make enough bets with the odds on your side, and you’ll make over the long term.

And so we need to look at valuations – to decide whether the risk-reward makes sense.

BTW – we share commentary on the COVID crisis every weekend, so please sign up for our mailing list, its absolutely free.

It’s a weekly newsletter that goes out every Sunday, and rounds up the week’s posts so you never miss anything.

Don’t forget also to join our Telegram Channel!

[mailmunch-form id=”928667″]

Valuations of OCBC Bank

I pulled the numbers from ShareInvestor, and to sum up:

- OCBC is trading at 0.92x book value

- This is in line with UOB’s valuation (0.95x book value)

- DBS has a premium valuation at 1.2x book value now

The 0.92x book value is about 1.5 standard deviations below its long-term average. So OCBC is very cheap on a historical basis, even after the recent rally.

If OCBC goes back to its long term average of 1.29x book value, that translates to $13.46, which is about a 40% upside from here.

Personal take? I think the current valuations are decent. In 5 years time, we’ll probably think this was a great price.

But I liked OCBC a lot more at $8.5 (80%) book value, where it was just a few weeks ago.

Why does OCBC have a big discount on its scrip dividend?

I came across a DBS research report that I found very interesting:

Maintain BUY for UOB and HOLD for OCBC.

We believe potential negatives in 3Q20 results for UOB (SGX:U11) are largely priced in and further improvement in loans under moratorium for UOB should be viewed positively.

OCBC (SGX:O39) remains a HOLD; we remain watchful over potential M&A activity as it continues to apply a discount on its scrip dividend in 2Q20.

As background, shareholders of OCBC can opt to receive their dividend in shares instead of cash. And the price of OCBC shares if you do so? $7.81, which is a 10% discount to the VWAP when it was priced.

In other words – OCBC wants shareholders to choose the scrip dividend, so that OCBC can save cash. Which begs the question, why does OCBC need to save up cash?

Neither DBS or UOB have such big discounts on their scrip dividend, and both are going through the same pandemic.

DBS Research seems to think that OCBC may be preparing for a big M&A / strategic move, and I would be inclined to agree with them.

This one is really interesting. If a big M&A is coming, I probably wouldn’t want to buy OCBC because of the uncertainty. Especially when UOB/DBS are equally viable right now.

Big M&As in this climate usually don’t work out well for the guy buying. Most of the time, you overpay, blow your cash position, and never get to realize the “synergies” the consultants talked about.

Interesting point – UOB is cutting costs

If your core business is not doing well, how else do you increase profits?

Of course, you cut costs.

What UOB has done, is that:

In an internal memo, the bank told senior staff that it expects the situation to worsen before improving when the Government cuts some of its support, reported Bloomberg yesterday.

Salary increases and promotions will be put on hold until further notice, Bloomberg quoted the memo as saying. It reported that the hiring restrictions will last until December next year.

A freeze on salaries and promotions until Dec 2021 is a drastic move, and makes me wonder what does UOB know that we don’t.

UOB has been the most aggressive of the 3 banks in cost cutting, while OCBC is somewhere in between.

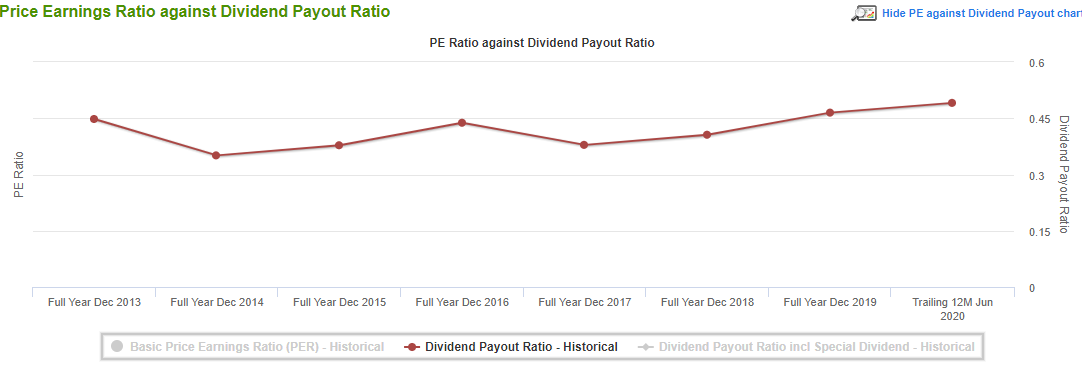

Dividend of OCBC

OCBC paid out a $0.159 dividend for Q2 2020, which works out to about a 3.3% yield going forward.

It’s okay, but nothing to shout about.

Dividend payout ratio is in the 40% range which is in line with DBS and UOB.

Ownership of OCBC

Unlike DBS, OCBC is not a Temasek linked company.

The OCBC Lee family owns about 20% of OCBC and is the largest shareholder. The rest is public shareholders.

Insider Trades for OCBC

Insider trades are mostly due to scrip dividend, so nothing meaningful here.

Note: ShareInvestor WebPro is a great and very cost-effective way to do analysis like this – beats trawling through the SGX announcements one by one. If you do such analysis regularly, well worth checking it out. Our review on WebPro here.

OCBC Share Buybacks

Buybacks are interesting, where OCBC was buying in quite big tranches all the way down during the March decline.

Will I buy OCBC bank?

To be really honest, there is not much to choose between the 3 local banks.

There’s slightly different flavours to each of them – DBS with the Temasek backing and strong investment banking, OCBC with the Wing Hang exposure, UOB with Singapore SME exposure etc.

But at the end of the day, all 3 operate in the same space, and are impacted by the same factors.

If Singapore’s economy does well in 2021, all 3 of them will do well.

If Singapore’s economy tanks, all 3 will drop.

Why I don’t own OCBC Bank

I have quite big positions in both DBS and UOB, and I added to them during the crash this year. You can check out my full stock portfolio on Patron if you’re keen.

But I don’t have a position in OCBC, and never added even when it was at $8.5.

It just never really appealed to me.

DBS and UOB both achieved the same function of getting exposure to Singapore banks, and without the HK exposure through Wing Hang.

So I don’t own OCBC bank, and I probably wouldn’t buy OCBC going forward, but this reason is unique to me. The same may not work for you.

And objectively, I think OCBC bank is a very decent stock, and it holds its own very well against UOB and DBS.

For long term investors, these are great prices to be averaging in at.

Closing Thoughts

Even after the massive rally, OCBC is still cheap valuations wise, at about 0.92x book value.

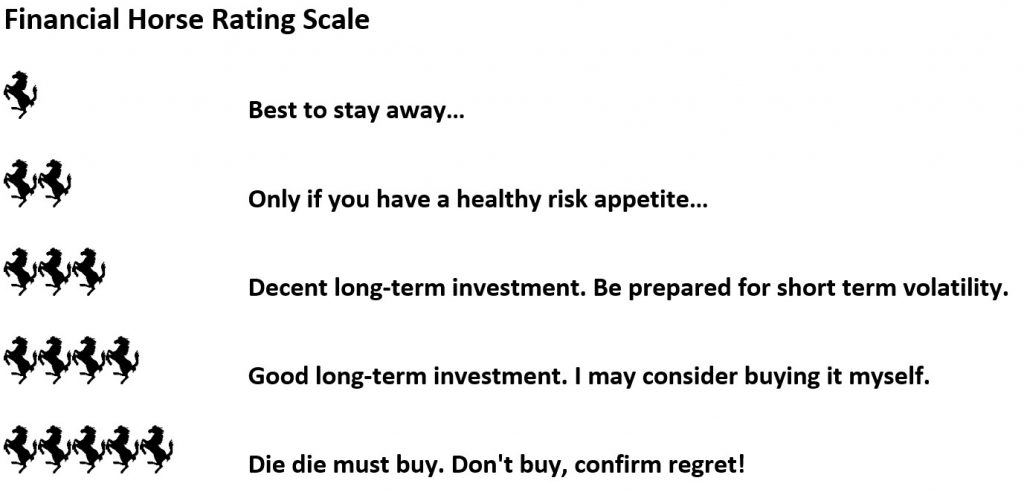

At this price, it’s probably a 3 to 3.5 horse rating for me.

Back at $8.5 (0.8x book value) though, it was a solid 3.5 horse rating. We may see such prices again before the end of this crisis, so be vigilant!

Btw – This is Part II of our series on banks. Check out Part I on DBS here. We’ll finish up by looking at UOB soon.

OCBC Bank – Financial Horse Rating Scale

Than you for doing a piece on OCBC. Looking forward to read your final article on UOB. Thank you

Thanks, glad you like it! Feel free to let me know if there is any article you want me to cover. 🙂

Newly joined your weekly newsletter, was great and interesting to learn a lot of things from your explanation and point of views. Looking forward to your UOB view points. Thank you.

Since YZJ ship building will not longer be on the STI index, what will be the impact on its price in the futures. Hope to have your view point on this particular stock too. Thank you

That’s interesting, will have a look at YZJ. Thanks. 🙂

Nice!! Thanks for the article. Looking for more breakdown on local stocks.

Great, let me know if there’s any stock in particular you’re keen on! 🙂

Isn’t it a big positive with OCBC’s ownership of Great Eastern, the only local big 3 with an insurance arm?

Not so sure about this one, the insurance income has fallen during this crisis. Usually when I invest in a bank I prefer to invest in the core lending business.

Really interesting point though. Why do you see it as a plus point?

I think Insurance income is a plus point for OCBC, although it is not as volatile as DBS, I am with the opinion to go in as long as P/B is below 1

Thanks. Quite a few readers have raised this point, and I do think it’s fair. I will probably have to revise the analysis to take into account the insurance business.

You kinda missing out one of the biggest profit center, wealth management and Bank of Singapore. Add that to GE, this are what sets OCBC apart from the other 2 banks, bancassurance and WM which is more sticky than loans and deposits.

Thanks. Quite a few readers have raised this point, and I do think it’s fair. I will probably have to revise the analysis to take into account the insurance business.

Most readers have elaborated on my point. COVID-19 impact is a temporary setback for long term investors. Insurance premiums are collected upfront with payouts (if happen) in future, sometimes decades later.

Thanks. Quite a few readers have raised this point, and I do think it’s fair. I will probably have to revise the analysis to take into account the insurance business.