My previous article on 3 Reasons Why I will not invest my life savings with StashAway must have gotten around, because shortly after, the StashAway team reached out to me for a meeting. I met up with the CEO, CIO and IR girl a couple weeks back for a really interesting lunch.

Following the meeting, StashAway sent me an email that very nicely sums up the crux of our discussions. I have replicated it in its entirety below (with their permission of course). I will then set out my personal thoughts, and readers can have a fuller picture before deciding whether to invest in StashAway.

Response from StashAway

“Transparency:

– One of our core beliefs is transparency, and so we’re confident to say that we are not a black box. This is why we have lots of material on our website and we do free seminars ( here’s the link to our webinar tonight, and if you register, you can actually watch it later if you can’t watch it live).

Asset Allocation:

– While it’s true that we’re at the end of a 30 yrs bull cycle for bonds, this does not mean bonds will give negative returns. Bonds offer important diversification to growth-oriented portfolios. Even in a rate hike environment such as 2017 where the US Federal Reserved raise rates three times, bond ETFs were offering investors quality returns. In particular, TLH (10-20y US Govt Bonds) and TLT (20y+ US Govt Bonds) returned 4.22% and 9.18% in 2017.

– It’s not true that US bonds are subject to 30% with-holding tax. Investor can claim back taxes paid on “Qualified Interest Income” (QII) and government bonds’s interest are usually 100% QII, therefore taxation is 0% after reclaim (and StashAway manages the reclaim).

– Customers can choose whether to opt-in or opt-out of the autoreoptimization feature (and they can change this preference at any time). If they opt out, they’ll still receive an email asking them if they want to follow our reoptimization suggestion or not.

Fees:

– Firstly, we don’t believe fees are a solid enough reason to choose a robo-advisor. A few basis points in delta returns will matter much more than a small difference in fees. All three SG robo-advisors give immense savings compared to ILPs or traditional funds. With that said, it is not true that we’re more expensive than Autowealth. Fees depends on (i) size of account and (ii) timeline. We optimize for long-term investors that want to build wealth with us: over a 30 years period investing 1,000$/month, an investor will pay approx 6% less fees to StashAway than to the other 2 robos. I’ve attached a file that shows that over 30 years, someone investing 2k/month in each robo will pay 20% less cumulative fees with StashAway.

Insolvency Risk:

– Investors’ cash and securities are held at our Custodian banks (HSBC for cash, Citi for securities); in practice, if both StashAway and Saxo go bankrupt, customers’ holdings are still safe. The fact that MAS awarded to us a full CMS license for Fund Management and that therefore we need to comply to very strict audit, compliance and minimum capital requirements should give comfort to investors.

Our license: https://eservices.mas.gov.sg/fid/institution/detail/201134-ASIA-WEALTH-PLATFORM-PTE-LTD

Saxo’s license: https://eservices.mas.gov.sg/fid/institution/detail/1553-SAXO-CAPITAL-MARKETS-PTE-LTD ”

Interesting stuff right? For a bit of background, I will also set out the profiles of their senior management team below. Michele is the fast talking Italian CEO (I kid you not he speaks really quickly) who truly believes in his investment product, and Freddy is the nice guy CIO who is the brains behind the asset allocation strategy:

Michele Ferrario

Co-Founder, Chief Executive Officer, 13 years experience in the financial industry and in consumer internet

Michele is the former CEO of Zalora Group and the co-founder of R ocket Internet in Italy and Pakistan. Prior to that, he worked as Investment Manager at Synergo and as Engagement Manager at McKinsey. He earned his MBA at Columbia Business School and his Bachelor of Science in Finance at Bocconi University in Italy. Michele has been invited by Singapore’s Minister of Finance to be a member of the Committee for the Future of the Economy.

Freddy Lim

Co-Founder, Chief Investment Officer, 16 years experience in cross-asset investing and portfolio management

Freddy gathered years of investment expertise as Managing Director and Global Head of Derivatives Strategy at Nomura. He gained his strong background in cross-asset portfolio at Millennium Capital Management and at CitiGroup, after working at Morgan Stanley, Merrill Lynch, and Lehman Brothers. He holds a Bachelor in Econometrics and Quantitative Economics from Monash University.

Financial Horse Response

Asset Allocation

The crux of their argument is:

- Bonds are important diversification

- StashAway reclaims withholding tax for bonds

- Customers can deselect re-optimisation if they so choose

Bonds are important diversification

I agree that bonds are important diversification in any portfolio. When I was coming up with the Financial Horse Alternative to Robo Advisers (FHARA), I found that it was virtually impossible to come up with a portfolio that did not suffer spectacular losses during a financial crisis, without adding in a small amount of bonds. My problem with bonds however, are twofold:

(1) Bonds underperform during the good times

This was a comment raised by many commenters as well. Namely, that during a stock market bull run, if you are holding a large portfolio of bonds, you are going to underperform the stock index by a large amount. Bonds are helpful during the bad times, but during the good times, they can be a hindrance on your portfolio.

The age and profile of the investor are crucial when deciding how much to allocate to bonds. For younger investors such as myself, who have a multi-decade investment horizon, I would like to have at most a 20% bond portfolio, possibly even 0%. I can do this because I maintain a large SGD cash emergency fund (via savings accounts or SSBs), as well as a large CPF buffer (I don’t touch it at all for my mortgage), all of which can be used to invest in a recession, or to tide me through rough times. When I invest in the markets, I therefore aim for maximum returns.

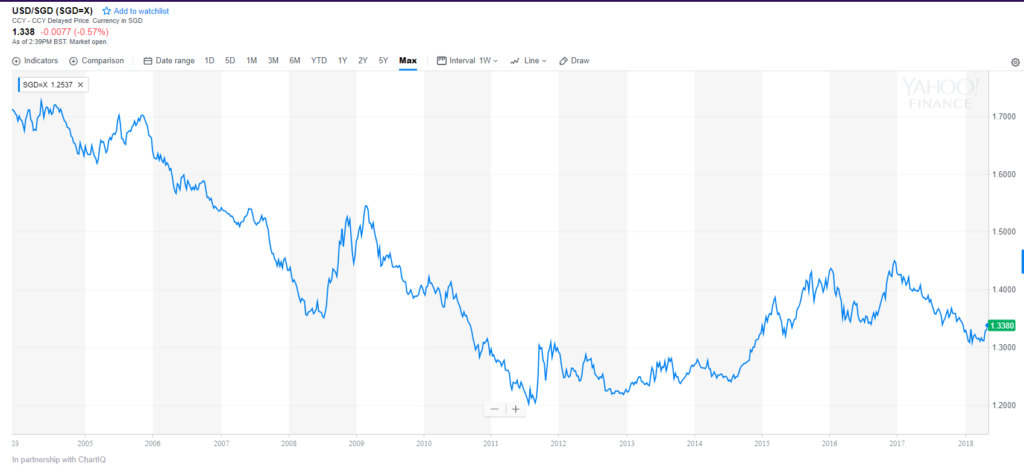

(2) US Bonds expose you to forex risk

By holding US Treasuries, you are exposed to USD forex risk. I’ve set out the 15 year chart of USD vs SGD below. The long term trend is very clear. The USD/SGD pair went from 1.71 in 2003 to 1.33 in 2018, which works out to a -1.66% CAGR.

The MAS maintains a policy of a steady appreciation of the SGD, which means that over time and outside of a financial crisis, you can probably expect the SGD to gradually strengthen against all other major currencies.

In recent years, the US has also demonstrated a willingness to print copious amounts of money (through QE) to artificially debase the USD. They do this to jumpstart the economy, as well as to decrease the real value of the dollar debt owed by the US government. In the next financial crisis, there is a high chance this may repeat itself.

What this means, is that if the past is any indicator, the SGD will gradually appreciate over time, and for a Singaporean investor, USD investments will lose money due to forex losses, to the tune of -1.66% a year. For example, by holding a US treasury yielding 2.5%, a 1.66% depreciation in the USD will result in about a 1% net return, excluding capital gains/losses.

Withholding tax

This is really interesting. What StashAway does, is that they engage a law firm in the US, who will file a tax application on their behalf to reclaim all tax that is paid as withholding tax on bonds. To illustrate, imagine that you buy a bond thorough StashAway and receive a S$300 coupon payment in 2018. You will pay S$90 to the US government as 30% withholding tax, and keep S$210 for yourself. In 2019, the law firm submits an application to the US government to reclaim withholding tax. If this is successful, the US government will pay you back the S$90 dollars in withholding tax in 2019.

Of course, due to the time lag in play, this only benefits long term investors. If you decide to exit your investment before they file the tax application, you won’t enjoy this benefit.

This is pretty nice value add by StashAway, and one that the other Robos don’t offer (at least not that I know of). If you have a 100% bond portfolio, this actually goes some way to justifying their fees. If you had a S$100,000 portfolio with 100% bonds, you’re paying about S$600 in fees a year, but the withholding tax they reclaim for you is about S$900 (assuming 3% bond yields), which is actually pretty significant.

Which opens up some interesting possibilities, for investors who want to buy US bonds but don’t want to pay withholding tax, to use StashAway for a 100% bond portfolio.

Of course, as the StashAway team themselves acknowledged, all this is contingent upon the tax application being successful, as they haven’t had a full tax cycle where they could actually implement this. In tax, nothing is certain until you actually get the tax refund in your hand, so I fully understand their reservations.

Deselect Reoptimisation

Michele (CEO) and Freddie (CIO) gave me a broad overview of their re-optimisation regime. Essentially, their proprietary model looks at a number of economic indicators, such as inflation, employment data, yield curves etc, and determines the ideal asset allocation. This is then signed off on by the investment committee, on a monthly basis. The claim is that when backtested, it identifies all of the previous recessions, leading to pretty decent outperformance (as you can imagine). Unfortunately, given that it’s a proprietary model, they are not able to disclose the exact mechanics of how the model works, and how much weight it allocates to each economic indicator.

I’ve spilt a lot of digital ink discussing my scepticism over the reoptimisation regime, so I will not belabour this point. To me, turning on the reoptimisation feature is basically agreeing to adopt their tactical asset reallocation regime. In the absence of full disclosure on how the model works, it requires an implicit leap of faith that this tactical asset reallocation will outperform a simple buy and hold with rebalancing.

It turns out that users who turn reoptimisation off will still get an email asking if you want to follow the reoptimisation suggestion (eg. if they want to buy more gold, they will ask you if you want to follow). This makes it a no-brainer for me. I would turn reoptimisation off, and when I receive their suggest, I would decide if I want to follow their suggestion. Over time, it would give you some indication of how the model functions, and whether going with their decisions leads to outperformance. Of course, it’s really up to you if you want to save the hassle and just let StashAway do the reoptimisation for you.

Fees

What StashAway is saying is that they have optimised their fee structure for a long term investor who invests S$1000 a month over a 30 year period. Such a hypothetical investor, assuming 6% compounded returns over the course of his life, would pay 6% less fees to StashAway than if he were to use the other Robos.

They sent me a huge excel spreadsheet to back this up. I’ve attached this excel here for users to examine, and I’ve extracted the key portions below.

Note: Autowealth has reached out to inform that the Excel spreadsheet contains certain inaccuracies. I have removed this link in the meantime.

Of course, at the end of the day, the difference in fees between the Robos are quite miniscule, so I don’t advise picking between them based purely on fees. You really need to understand the asset allocation strategy of each Robo, and pick based on that (more on this below).

There were questions from readers as to whether the 0.5 – 0.6% fees make up for the transaction fees, and the forex spread with DIY investing. Don’t forget, when buying ETFs directly, you need to pay transaction fees to your broker, who also earns a spread on your forex. The answer would largely depend on the amounts you are investing. When you are first starting out in investing, and putting in S$2000 to S$3000 each time, transaction fees can really add up, because of the minimum USD10 or USD25 commission you are paying. Once you move up in the investing world and are investing S$20,000 to S$30,000 each time, the commission as a percentage of your investment will fall.

Note that if after this article your decision is to invest with StashAway, then please sign up through this referral link to enjoy 50% off on your first S$50,000 investment for 6 months, which works out to about S$94.

Insolvency Risk

It’s not 100% clear in the response (they’re probably trying to cover themselves from a legal perspective), but during the meeting, they were quite confident that investors do not take on insolvency risk when investing with StashAway. Since they are prepared to confirm this to me in such clear terms, I will take their word for it. Investors in StashAway do not assume the insolvency risk of Saxo, StashAway, or Citi, so this addresses one of the pet-peeves I had about StashAway.

Superior Asset Allocation

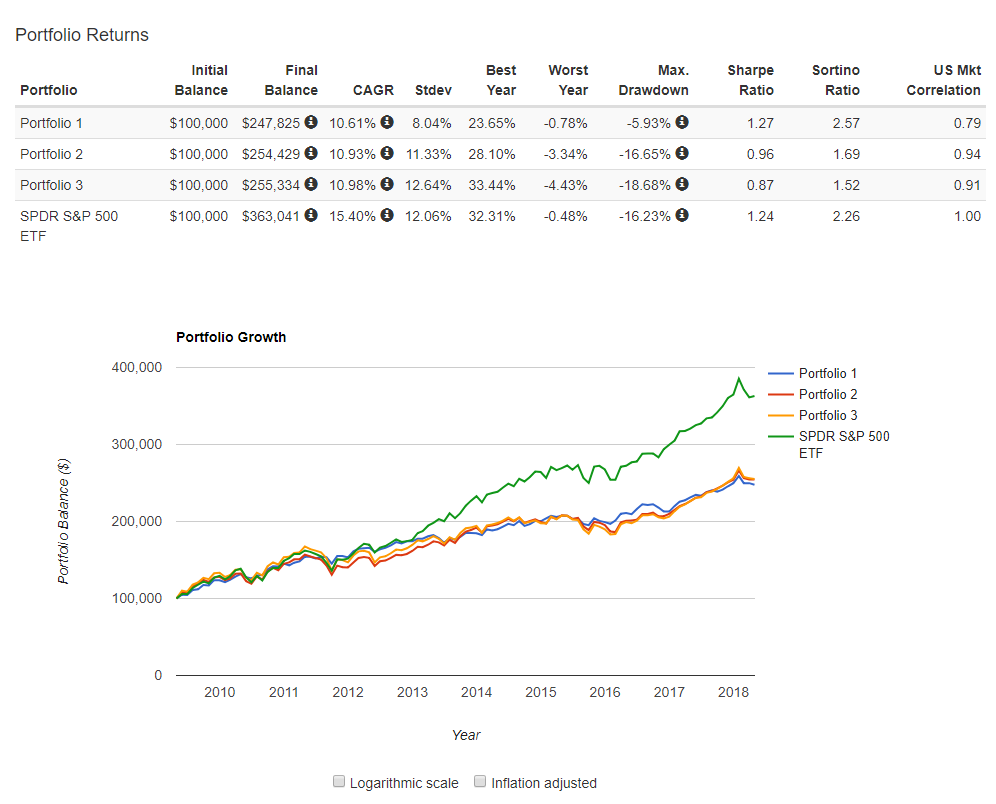

Michele and Freddie went on and on about how they think they are the best robo in town, in terms of asset allocation. And they sounded like they really believed this. This got me intrigued. So I went to StashAway, AutoWealth, and Smartly, and I downloaded the absolute highest risk profile that the system would give to me, with the maximum allocation to stocks possible. Then I backtested all 3 Robo Advisers. And the results just blew me away.

I’ve set out the results below, based on a S$100,000 initial investment (Portfolio 1 is StashAway, Portfolio 2 is AutoWealth, and Portfolio 3 is Smartly. Green is the S&P500 that I used as a benchmark).

The absolute returns for all 3 are virtually identical, at about a 10.6% to 10.9% CAGR. But where StashAway really stands out, is their risk adjusted returns. StashAway’s maximum drawdown was only -5.93% (versus 16 – 18% for the others), and their Sharpe Ratio was an astounding 1.27 (versus 0.8 to 0.9 for the others).

The Sharpe ratio is defined below, and its basically the average returns you are getting less the risk you are taking on (higher is better):

The Sharpe ratio is the average return earned in excess of the risk-free rate per unit of volatility or total risk. Subtracting the risk-free rate from the mean return, the performance associated with risk-taking activities can be isolated. One intuition of this calculation is that a portfolio engaging in “zero risk” investment, such as the purchase of U.S. Treasury bills (for which the expected return is the risk-free rate), has a Sharpe ratio of exactly zero. Generally, the greater the value of the Sharpe ratio, the more attractive the risk-adjusted return.

From Investopedia

What this means, is that all 3 Robos advisers give you pretty much the same in terms of absolute returns (when backtested). However, based on historical returns, the risk that you are taking on with StashAway is far lower than that with either Autowealth or Smartly. In a financial crisis, you will probably lose less money with StashAway than had you invested in the other robos (again assuming that backtested results hold true in the next crisis).

I’ve added a link to the model I used here, feel free to play around with it to see how changes in initial investment/monthly contributions affects returns.

StashAway versus DIY

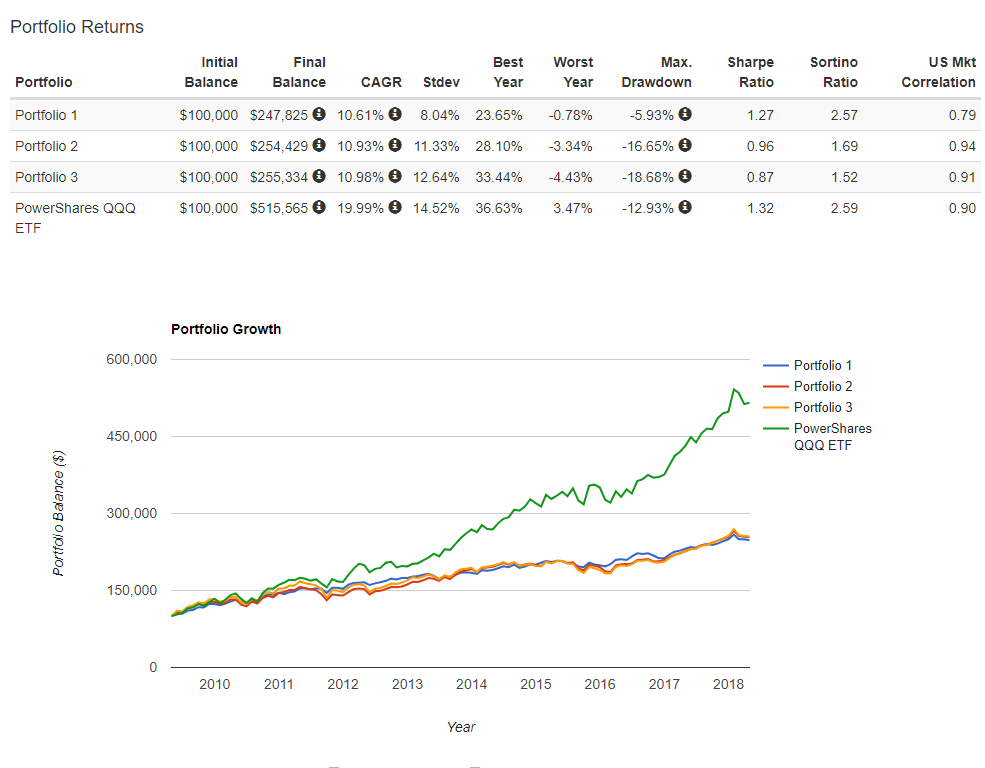

Just for kicks, I also ran the Robos’ performance against a popular NASDAQ ETF (QQQ) and the results are quite amazing. QQQ’s 19.99% CAGR since 2009 is almost double that of the performance of any other Robo. With a S$100,000 starting investment, you would have ended up with S$515,000, versus about S$250,000 for the Robos.

Unfortunately the ETFs used by StashAway don’t go back beyond 2009, so I was not able to backtest further. Link to the model here.

But the point is this. These Robos use a balanced portfolio, that are designed to deliver decent performance in good times, and minimise losses during the bad times. However, during the good times, they will not deliver the kind of growth a 100% equity investment will.

The key is to look at your portfolio in its entirety, and determine your risk appetite as an investor. There is a famous saying in investing that “before you can think about gains, you first have to think about risk”. If apart from your investments, you only have a few thousand in your account, then you can’t afford to take much risk, and perhaps a robo on a medium level risk setting is a good idea. But if you have S$100,000 in SSBs, S$100,000 split over a number of high yielding accounts, and no debt obligations, then perhaps you can afford a higher risk appetite with your investments.

Don’t forget, with a Robo you cannot choose to sell only your bonds during a recession. When you withdraw money from a robo, their will liquidate all your investments on a pro rata basis, selling your shares and bonds equally.

Note: A reader left a highly insightful comment below, that I felt was worth replicating in full here. I think this really illustrates the power and importance of asset allocation, comparing Robos, traditional 60:40 allocations, and 100% equity allocations. Which is suitable for you really depends on your profile and objectives as an investor. Credits: Sinkie:

Hi FH,

Thanks for the comprehensive re-overview & backtesting verification! Interesting to note that the risk-reward for pure S&P500 is higher than for AutoWealth and Smartly?!?

BTW, I know comparing with QQQ is for fun … but for buy-and-holders don’t forget that Nasdaq did go down -80% not that long ago. It’s like looking at Apple & Amazon now and thinking what if … not realizing that one had to suffer -90% drawdowns as true believers in order to reap the maximum rewards.

What goes up must come down, and what does up more comes down more. Tech stocks exploded in the 90s and suffered horrendous losses post dot.com … they didn’t go up as much prior to GFC and subsequently fell less than the S&P500 … now tech / semicon has been leading stocks pretty much worldwide for years already …

Just a point to note though … I believe your backtesting is using current Robo allocations on static basis? Coz the asset allocation for StashAway should change over the economic / business cycle — but that’s impossible to replicate as long as it remains a black box (there I’ve said the B word!).

I’m sure StashAway can provide a 30-year backtested portfolio using the major indexes with their system, and compare against say a traditional 60:40 allocation, pure S&P500, pure MSCI World, pure STI etc.

Yeah quite a lot of research has gone into tactical asset allocation techniques over the last 20 years (particularly in the last 10 after GFC). They all basically showed that in strong bull markets, no TAA method can outperform buy & hold 100% stocks. Their outperformance only comes if there’s a big bear market like GFC or dot.com bust. And if there’s a strong & LONG recovery after a bear, the pure equities method can overcome the benefits of TAA, as can be seen in this current bull.

E.g. Say I invested near the top on 31st Dec 2007 in a portfolio of 70% US stocks and 30% US bonds. My friend goes all-in US stocks.

My max drawdown would have been -34% compared to my friend’s at -48% … and my portfolio would have been ahead of his all the way till end-2013. From 2014 till mid-2016 both our portfolios would be basically neck-and-neck. But after mid-2016, my friend’s 100% stocks would pull ahead of mine.

In other words, if there had been another bear market anytime before 2015, the diversified asset allocated portfolio would have won, even on an absolute returns basis. No wonder the veteran investors have been pulling their hair out over this unnaturally long bull! ????

What TAA does best (and frankly any asset allocation with re-balancing, even a boring 60:40 one, is arguably TAA) is that it helps psychologically, preventing a drastic drawdown in the short-term that can cause most people to sell out at the worst times.

For Buffett-wannabees like us who think we can be greedy when others are fearful & vice versa, we may want to have greater control over our own TAA. For those who don’t want to think or meddle too much, then Robo’s can be an OK solution (with fees of course).

Closing Thoughts

If I had to pick between the 3 robo-advisers in Singapore today, I would probably go with StashAway. The insolvency risk has been addressed, re-optimisation can be turned off, and their risk-adjusted returns on a historical basis far surpass that of Autowealth or Smartly. For me personally, I would select the highest possible risk profile, turn re-optimisation off and evaluate any reoptimisation on a case by case basis. For this reason, I do think a revision to their rating is due. I will upgrade them to a 3 Financial Horse rating.

But holistically, I do still have some reservations about using a robo-adviser. Their usage of USD bonds, and the fact that they not invest in any Singapore stocks or REITs, means that I will not put all my investments into a Robo. If I had to do it, I would invest perhaps 40% of my investments in Robos, and use the rest to invest in Singapore stocks and REITs. This is important because 100% exposure to USD is not ideal for Singaporean investors, and I do want to have some investments parked in Singapore, as I think there are still many attractive investment opportunities on our shores.

Michele and Freddie mentioned that they are looking at introducing new asset classes into the mix, so its worth keeping an eye on this space. However, a lot of the Singapore ETFs, (eg. Nikko AM Bond ETF, STI ETF, REIT ETF) have poor liquidity (and large fees), so it is interesting to see which ETFs they decide to go with..

Financial Horse – StashAway Rating (Revised)

Financial Horse Rating scale

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles!

Hi FH,

Thanks for the comprehensive re-overview & backtesting verification! Interesting to note that the risk-reward for pure S&P500 is higher than for AutoWealth and Smartly?!?

BTW, I know comparing with QQQ is for fun … but for buy-and-holders don’t forget that Nasdaq did go down -80% not that long ago. It’s like looking at Apple & Amazon now and thinking what if … not realizing that one had to suffer -90% drawdowns as true believers in order to reap the maximum rewards.

What goes up must come down, and what does up more comes down more. Tech stocks exploded in the 90s and suffered horrendous losses post dot.com … they didn’t go up as much prior to GFC and subsequently fell less than the S&P500 … now tech / semicon has been leading stocks pretty much worldwide for years already …

Just a point to note though … I believe your backtesting is using current Robo allocations on static basis? Coz the asset allocation for StashAway should change over the economic / business cycle — but that’s impossible to replicate as long as it remains a black box (there I’ve said the B word!).

I’m sure StashAway can provide a 30-year backtested portfolio using the major indexes with their system, and compare against say a traditional 60:40 allocation, pure S&P500, pure MSCI World, pure STI etc.

Yeah quite a lot of research has gone into tactical asset allocation techniques over the last 20 years (particularly in the last 10 after GFC). They all basically showed that in strong bull markets, no TAA method can outperform buy & hold 100% stocks. Their outperformance only comes if there’s a big bear market like GFC or dot.com bust. And if there’s a strong & LONG recovery after a bear, the pure equities method can overcome the benefits of TAA, as can be seen in this current bull.

E.g. Say I invested near the top on 31st Dec 2007 in a portfolio of 70% US stocks and 30% US bonds. My friend goes all-in US stocks.

My max drawdown would have been -34% compared to my friend’s at -48% … and my portfolio would have been ahead of his all the way till end-2013. From 2014 till mid-2016 both our portfolios would be basically neck-and-neck. But after mid-2016, my friend’s 100% stocks would pull ahead of mine.

At 30 Apr 2018, even after the correction, my friend’s portfolio will still be almost 10% more than mine.

In other words, if there had been another bear market anytime before 2015, the diversified asset allocated portfolio would have won, even on an absolute returns basis. No wonder the veteran investors have been pulling their hair out over this unnaturally long bull! 🙂

What TAA does best (and frankly any asset allocation with re-balancing, even a boring 60:40 one, is arguably TAA) is that it helps psychologically, preventing a drastic drawdown in the short-term that can cause most people to sell out at the worst times.

For Buffett-wannabees like us who think we can be greedy when others are fearful & vice versa, we may want to have greater control over our own TAA. For those who don’t want to think or meddle too much, then Robo’s can be an OK solution (with fees of course).

Hi Sinkie,

Wow, excellent comment and points raised. This should be a must read for any reader to the post, I think you really took my argument further and came up with some fantastic insights. I’ll update my post accordingly to incorporate your comment, credits to you of course.

Just to respond to you on the assumptions used when I backtested StashAway:

(1) The StashAway asset allocation is a range, so I used the midpoint of the range.

(2) Yes, this does not take into account reoptimisation, only rebalancing. It is therefore possible that StashAway may outperform the simulation once tactical asset allocation is enabled. Unfortunately, you are right that the only way to get this data is to request from StashAway directly.

I quite liked your point that even if one had invested at the absolute worst time in 2007, a 100% equity allocation would still outperform the 70:30 one, if one holds until today. I realised that if you backtest it even further though, starting from 1987, the 70:30 portfolio will still underperform the 100% equity one.

This is so despite the fact that the 1980s to now have been an unprecedented bull market for bonds. For something similar to happen in the next 30 years, we will need to see bond yields go well into the negative territory (which given the way things are shaping out, may not be entirely out of the question). I think this really illustrates the power of stocks over long, multi-decade periods.

Dangerous to judge them so early. Both positive and negative. If you poke Stashaway, Michele is going to find you. I have no doubts when your article is out that will happen.

Hi Kyith,

Thanks for dropping by! I actually thought the backtested results made it quite clear that the asset allocation strategy of StashAway is far superior to the others on a risk adjusted basis, when backtested from 2009.

I really like Stashaways management team, asset allocation strategy, customer support, and vision for the future. I may consider leaving a small amount with them once they update the system to allow for higher equity allocations.

Cheers.

Hi FH,

Just a followup on the QII exemption from withholding tax.

It apparently has been signed into law on “permanent” basis by Obama back in Dec 2015, allowing interest-type dividends & capital-gains dividends to be tax-free for non-resident investors.

i.e. http://www.klgates.com/permanent-us-withholding-tax-rules-for-non-us-investors-in-rics–a-new-distribution-opportunity-01-12-2016/

Examples:

iShares

JP Morgan

PowerShares

I’m not sure if the tax exemption is at source i.e. at the point when the ETF sponsors make distributions, or whether need a follow-up claim.

From the above description (and logically) should be exempted at source — i.e. pretty much transparent which would make investors’ lives much easier if so!! 🙂

Hi Sinkie,

Wow interesting, thanks for doing the research. What I understand from StashAway is that they engage a law firm to provide this service for them, and that it is performed on a retrospective basis. This would mean that a follow up is required, and also that investors have to stay until the end of the financial year and after the tax refund has been processed to enjoy this benefit.

Unfortunately it would also mean that individual investors like us cannot enjoy this, because the cost of engaging a service provider to perform this submission would probably outweight the withholding tax itself!

Hello FH,

Among other topics, I queried Stashaway specifically on US withholding and estate taxes. I was concerned on the latter and they replied that you avoid the dreaded US estate tax applicable to alien non-residents. I am not sure if the same applies to other Robo advisors but definitely an advantage compared to a DIY when your investments in the US market exceed 60kUS$.

I quote their answer hereafter :

”

4. Taxes for Singapore Tax Residents

As a Singapore tax resident, your StashAway investments are only subject to a 30% dividend withholding tax to the U.S. government. These taxes are applicable as long as you own US listed assets, regardless whether the assets were bought through StashAway, or via your own broker. These taxes are entirely factored into our returns.

Your StashAway investments are not subject to any other taxes (e.g. capital gains, estate taxes).

For estate taxes, these are only applicable for non-US citizens investing as individuals in the United States. As your StashAway investments are treated as corporate investments, they are not subject to estate taxes.”

Br,

LG

Hello LG,

Thanks very much for sharing this. Interesting that you are concerned about estate tax, since the investors who tend to use Robos (and their target audience) tends to be the younger millenial crowd.

In any case, you are right, that will be another potential advantage of robo advisers, since the holding structure will mean that Singapore estate tax will apply (and there are none). Thanks for raising this point.

Cheers,

FH

IR “girl” ? Was she twelve years old?

Haha IR lady then? 🙂

I’m not sure if I’m getting it right. A simple 60/40 portfolio linked below has a weight average expense ratio of about 0.05% with a 10.51% CAGR and 1.24 sharpe ratio. Are the portfolios listed above net of fees?

https://www.portfoliovisualizer.com/backtest-portfolio?s=y&timePeriod=4&startYear=2009&firstMonth=1&endYear=2018&lastMonth=12&endDate=07%2F31%2F2018&initialAmount=10000&annualOperation=0&annualAdjustment=0&inflationAdjusted=true&annualPercentage=0.0&frequency=4&rebalanceType=1&showYield=false&reinvestDividends=true&sameFees=true&symbol1=VTI&allocation1_1=60&symbol2=BND&allocation2_1=40&symbol3=BIL&symbol4=TLT

Yep, that sounds about right, although you’re using the past 10 years which was an unprecedented bull market for all asset classes (other than cash).

No, the portfolios I listed above are before accounting for fees and expenses, so theoretically the returns for the robo advisors should be revised downwards accordingly.

Could you please have a comparison review of StashAway vs Syfe? Thanks.

Haven’t heard of Syfe before this actually, but sure, I’ll take a look at them. 🙂