It’s been quite a while since my last article on fixed deposits.

And I have been getting a couple of questions on the best place to park some spare cash today.

3 things I wanted to discuss today:

- What are the Top Fixed Deposit Rates in Singapore today (Feb 2025)?

- Why are T-Bills yields so much higher than fixed deposits?

- Where would I put my cash today?

Top Fixed Deposit Rates in Singapore offer 2.90% yield (Feb 2025)

The full table is further below in the article, but I’ve summarised the best interest rates for the 3-, 6- and 12-month tenures below.

Funnily enough the best fixed deposit rates all come from Bank of China.

But in terms of the interest rate curve – you can see how the 3 months tenure is the most attractive at 2.90%.

Which drops to 2.75% at 6 months, and 2.60% at 12 months – as the market price in interest rate cuts in 2025.

Frankly, this isn’t all that attractive, as there are much better options which we’ll discuss in this article.

| Tenure | Best fixed deposit interest rate (Feb 2025) | Bank |

| 3 months | 2.90% | Bank of China |

| 6 months | 2.75% | Bank of China |

| 12 months | 2.60% | Bank of China |

Best Fixed Deposit Rates yield 2.90% if you deposit with Syfe Cash+ (to access institutional fixed deposit rates)

The rates above are assuming that you deposit with the bank directly as a retail customer.

Another way to do it is to use Syfe Cash+ Guaranteed.

The way this works is that you park the cash with Syfe, who will then deposit the cash into an institutional fixed deposit account.

This allows you access to institutional fixed deposit rates.

These are the latest interest rates from Syfe Cash+ below:

- 3 months – 2.90%

- 6 months – 2.80%

- 12 months – 2.75%

Frankly, it’s not all that much higher than the best retail fixed deposit rates we saw above.

Note that Syfe Cash+ is not SDIC insured, but given that the underlying is fixed deposits risk should be on the low side (but not risk free).

6-month T-Bills yields rise to 3.04%, 12 month T-Bills yields close at 2.95%

By contrast, T-Bills yields look pretty attractive of late.

At the most recent T-Bills auction, the 6 month T-Bills closed at 3.04% yield:

While the 12-month T-Bills closed at 2.95% yield:

Comparing interest rates for T-Bills vs Fixed Deposits vs Syfe Cash+ Guaranteed across all tenures (Feb 2025)

I’ve tabulated the interest rates for the 3 cash options below, as well as with money market funds.

You can see how T-Bills yields are quite a bit higher than the fixed deposit rates – almost 0.30% (30 bps) higher.

| 3 months | 6 months | 12 months | Risk Free | |

| T-Bills yields | NA | 3.04% | 2.95% | Yes |

| Fixed Deposit (direct to bank) | 2.90% | 2.75% | 2.60% | Yes (if below $100,000 SDIC limit) |

| Syfe Cash+ Guaranteed (Institutional Fixed Deposit Rates) | 2.90% | 2.80% | 2.75% | No |

| Money Market Funds | ~2.9% | No | ||

Best Fixed Deposit Rates yield 2.90% – if you deposit directly with the bank (as of Feb 2025)

The full list of Fixed Deposit rates is set out below (bold being the most attractive for each tenure).

After the table I’ll share my views on:

- Why are T-Bills so much more attractive than fixed deposits today?

- Where would I put my cash today?

| Bank | Interest rate per annum | Tenure | Minimum amount |

| Bank of China | 2.90% (mobile placement) | 3 months | S$500 |

| 2.75% (mobile placement) | 6 months | S$500 | |

| 2.60% (mobile placement) | 9 months | S$500 | |

| 2.60% (mobile placement) | 12 months | S$500 | |

| ICBC | 2.90% (mobile placement) | 3 months | S$500 |

| 2.45% (mobile placement) | 6 months | S$500 | |

| CIMB | 2.70% | 6 months | S$10,000 |

| 2.65% | 3 months | S$10,000 | |

| 2.55% | 9/12 months | S$10,000 | |

| Maybank | 2.70% (mobile placement) | 6 months | S$20,000 |

| 2.55% (mobile placement) | 9 months | S$20,000 | |

| SBI | 2.65% | 6 months | S$50,000 |

| 2.50% | 12 months | S$50,000 | |

| Hong Leong Finance | 2.60%(mobile placement) | 6 months | S$50,000 |

| 2.55%(mobile placement) | 8 months | S$50,000 | |

| RHB | 2.58% (mobile placement) | 3 months | S$20,000 |

| 2.58% (mobile placement) | 6 months | S$20,000 | |

| 2.58% (mobile placement) | 12 months | S$20,000 | |

| HSBC | 2.48% | 6 months | S$30,000 |

| 2.28% | 3 months | S$30,000 | |

| DBS/POSB | 2.45% | 12 months | S$1,000 (max S$19,999) |

| 2.35% | 9 months | S$1,000 (max S$19,999) | |

| OCBC | 2.45% (mobile placement) | 6 months | S$30,000 |

| Standard Chartered | 2.40% | 6 months | S$25,000 |

| UOB | 2.40% | 6 months | S$10,000 |

| 2.20% | 10 months | S$10,000 |

Why are T-Bills so much more attractive than fixed deposits today?

If you’ve been following T-Bills and fixed deposit rates for the past 2 years, you’ll realise that there are times when Fixed Deposit rates are more attractive, and times when T-Bills rates are more attractive.

A 0.3% (30 bps) spread between the two is quite stark – why the huge disparity today?

There’s no easy answers for this as it goes back to the bank funding costs as well, and their need for cash.

But the way I see it is that the bank fixed deposit rates tends to lag the market by a bit.

So when rates are rising sharply, T-Bills yields will be higher, and when rates are falling sharply, fixed deposit yields tend to be higher.

Whereas today we’re at a point where the market is pricing in higher rates going forward, and while that has been reflected in T-Bills yields, it hasn’t been reflected in the bank rates (yet).

Follow Financial Horse to avoid missing any post!

Interest Rate Outlook? 2 more rate cuts in 2025?

The market is currently at a point where only 2 rate cuts are priced in for 2025.

And frankly while 6-month yields are flat across the board.

The real action has been on the long end – you can see how Singapore 10 year yields bottomed at 2.4% literally on the day the Feds cut interest rates, and have gone from 2.4% to as high as 3.1% since.

If you ask me, market yields are slightly ahead of the banks here in pricing in a higher rate regime due to a resilient US economy.

But hey – take all this with a pinch of salt because sometimes the short answer is that no one has any clue.

Where would I put my cash today?

Whatever the case it – it’s fairly clear that T-Bills are a better choice than fixed deposits today, as you’re getting up to a 0.30% higher yield at some tenures.

T-Bills are completely risk free as well (backed by the Singapore government), the only issue is that the liquidity is tied up as you cannot get the cash back before maturity.

So if you asked me, that’s probably where I would be parking my spare cash going forward.

If you wanted a bit more liquidity, you can check out some of the options below:

UOB One, DBS Multiplier, OCBC 360 – High Yield Savings Accounts

This one is self-explanatory, so I won’t dwell on it.

A high yield savings account like UOB One pays 4.0% blended yield on $150,000, that is fully liquid and can be withdrawn any time.

If it works for you, high yield savings accounts like these are probably the best option.

If they don’t work (whether you can’t meet the requirements or don’t have enough spare cash), then just use the other options on this list.

Money market fund instruments (like MariInvest) or fintech plays (like Chocolate Finance/GXS/FD) on the short end

Alternatively there is MariInvest which is a money market fund that pays about 2.9% over the past 30 days for me.

It’s definitely come down because of the rate cuts, but for something that is pretty low risk and with good liquidity (first $10,000 can be withdrawn instantly, rest is T+1 liquidity), it’s a decent option in my view.

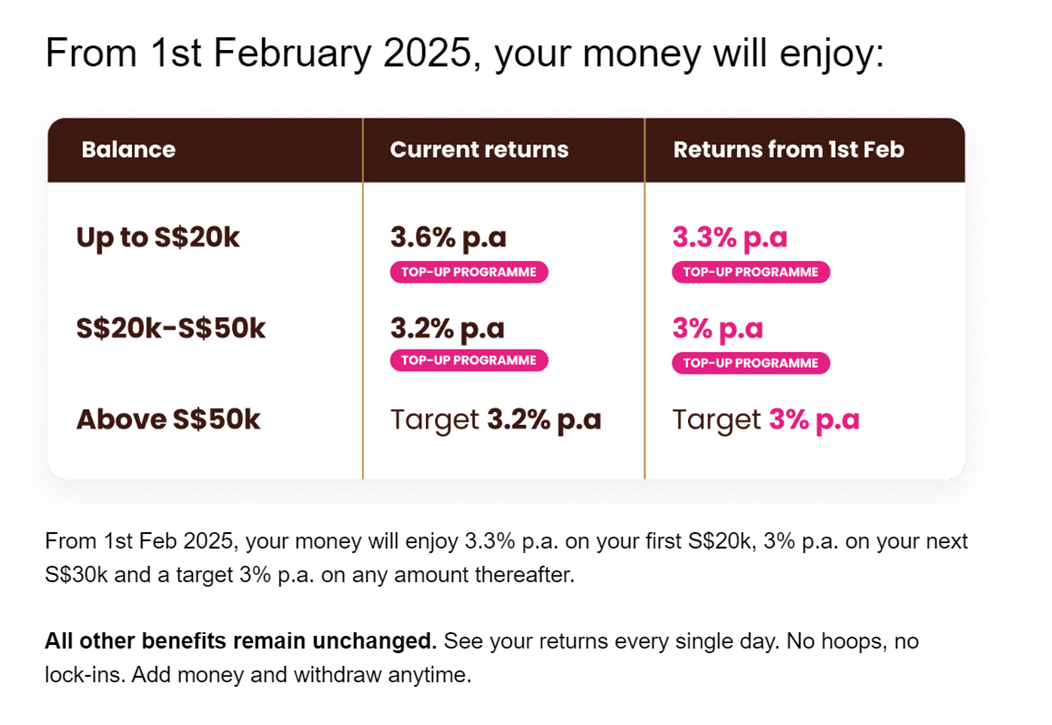

Alternatively, there’s stuff like Chocolate Finance that even after the drop in rates, will pay about 3.3% on the first $20,000 (fully liquid, but note not SDIC insured).

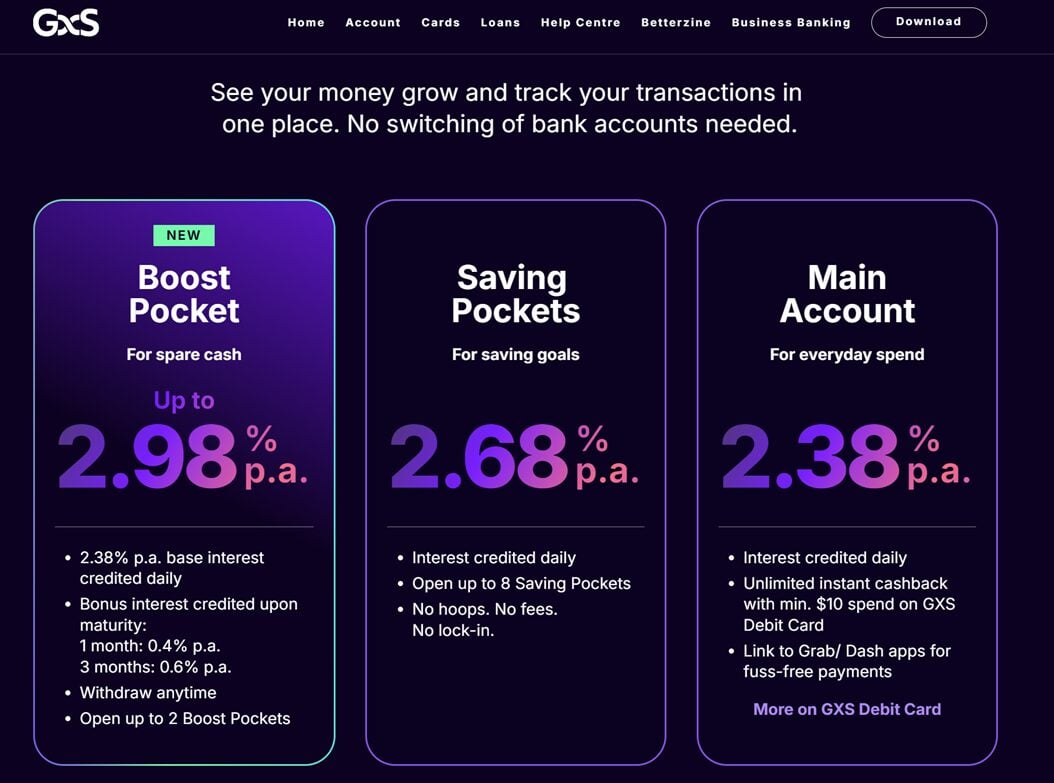

While GXS is paying 2.98% for 3 months:

There is some investor discretion required here as unlike T-Bills, not all the instruments above (eg. Chocolate Finance / money market funds) are risk free.

But generally speaking I think all of the above are decent enough alternatives to T-Bills and Fixed Deposits.

Singapore Savings Bonds are decent…

Alternatively there are the latest Singapore Savings Bonds which yield 2.76% for the first year.

Frankly this is not too bad and competitive with the latest 6 or 12 month Fixed Deposit rates.

So this is another option too, as they can be withdrawn any time (get your money back at the start of the next month).

For more duration – Bond Funds

For more duration, you can consider buying a bond fund.

But bond funds are quite a complex instrument, and not for everyone.

Because if interest rates go up, you can suffer capital losses.

And there is no way to hold to maturity as the bond fund will automatically reinvest proceeds, so the timing at which you sell matters too.

I wrote quite a few articles on this in the past, and do check them out for more information (see here or here).

This post is written on 31 Jan 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.