Okay so I have been getting a lot of questions on PIMCO GIS Income Fund.

It invests primarily in US investment grade bonds, and:

- Pays a 6.1% yield (approximately)

- Has a 3 – 4 year effective duration

- SGD hedged

Does this make it a better buy than T-Bills?

At the same time I know a lot of you are still interested to continue the T-Bills series of articles.

So we’ll try to cover both bases today.

3 questions I will discuss:

- Is PIMCO GIS Income Fund a good buy at 6.1% yield?

- Estimated yield on the next 6-month T-Bills auction?

- Why I stopped buying T-Bills – and switched to a mix of short duration bonds / money market funds instead?

PIMCO GIS Income Fund – estimated yield of 6.1%?

The investment objective of PIMCGO GIS Income fund is (emphasis mine):

The Income Fund is a portfolio that is actively managed and utilizes a broad range of fixed income securities that seek to produce an attractive level of income while maintaining a relatively low risk profile, with a secondary goal of capital appreciation.

This fund seeks to meet the needs of investors who are targeting a competitive and consistent level of income without compromising long term capital appreciation. The fund seeks to generate a competitive monthly dividend while also maintaining a focus on the total return objective. The fund aims to achieve this by employing PIMCO’s best income-generating ideas across global fixed income sectors with an explicit mandate on risk-factor diversification. The fund offers daily liquidity.

This fund is designed for investors who seek steady income: it takes a broad-based approach to investing in income-generating bonds. The fund taps into multiple areas of the global bond market, and employs PIMCO’s vast analytical capabilities and sector expertise to help temper the risks of high income investing. This approach seeks to provide consistent income over the long term.

But what exactly does that mean in plain English?

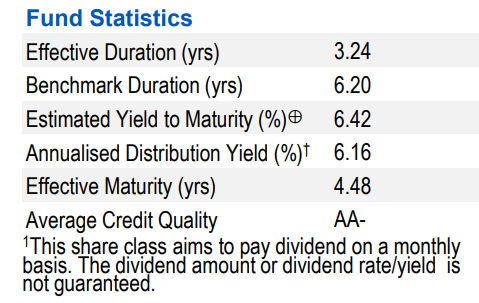

Some simple numbers below:

- Estimated gross yield to maturity of 6.41%

- Historical annualized distribution yield is 6.16%

- Effective duration is about 3 years +

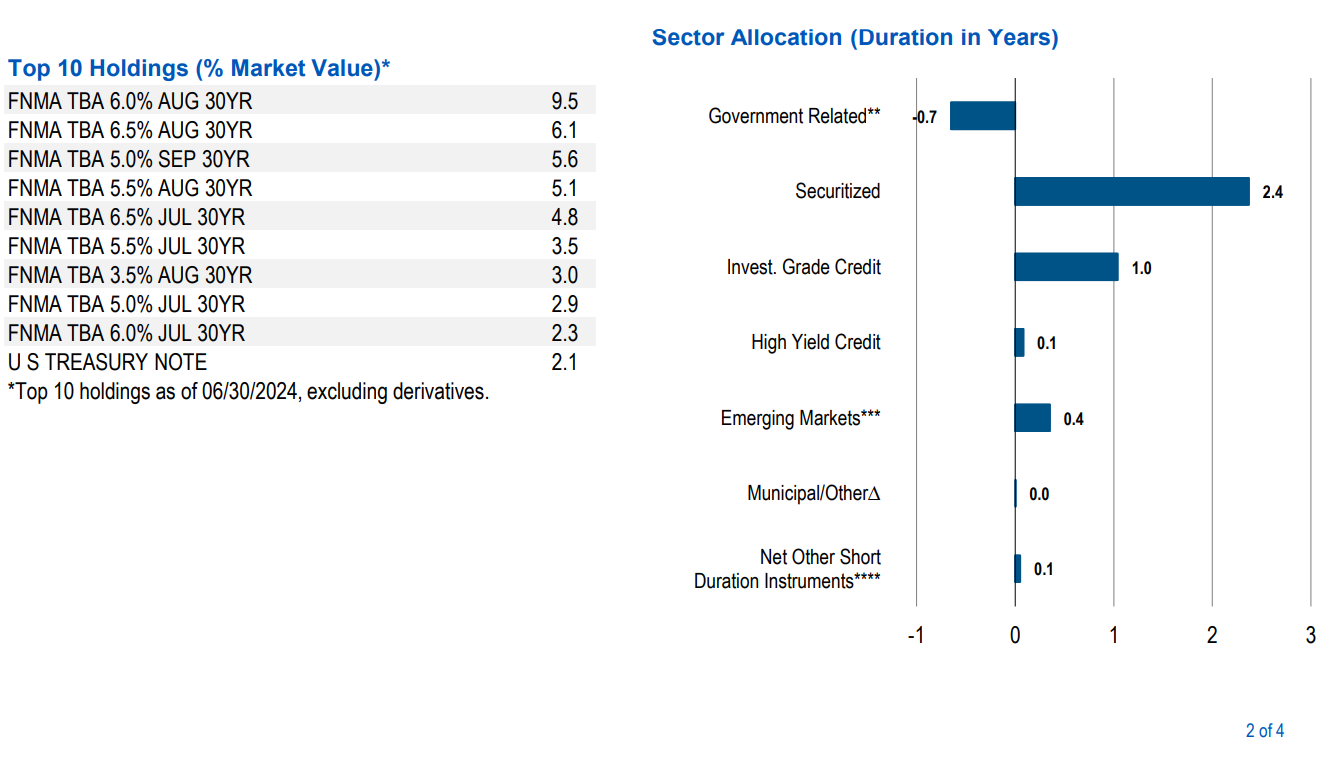

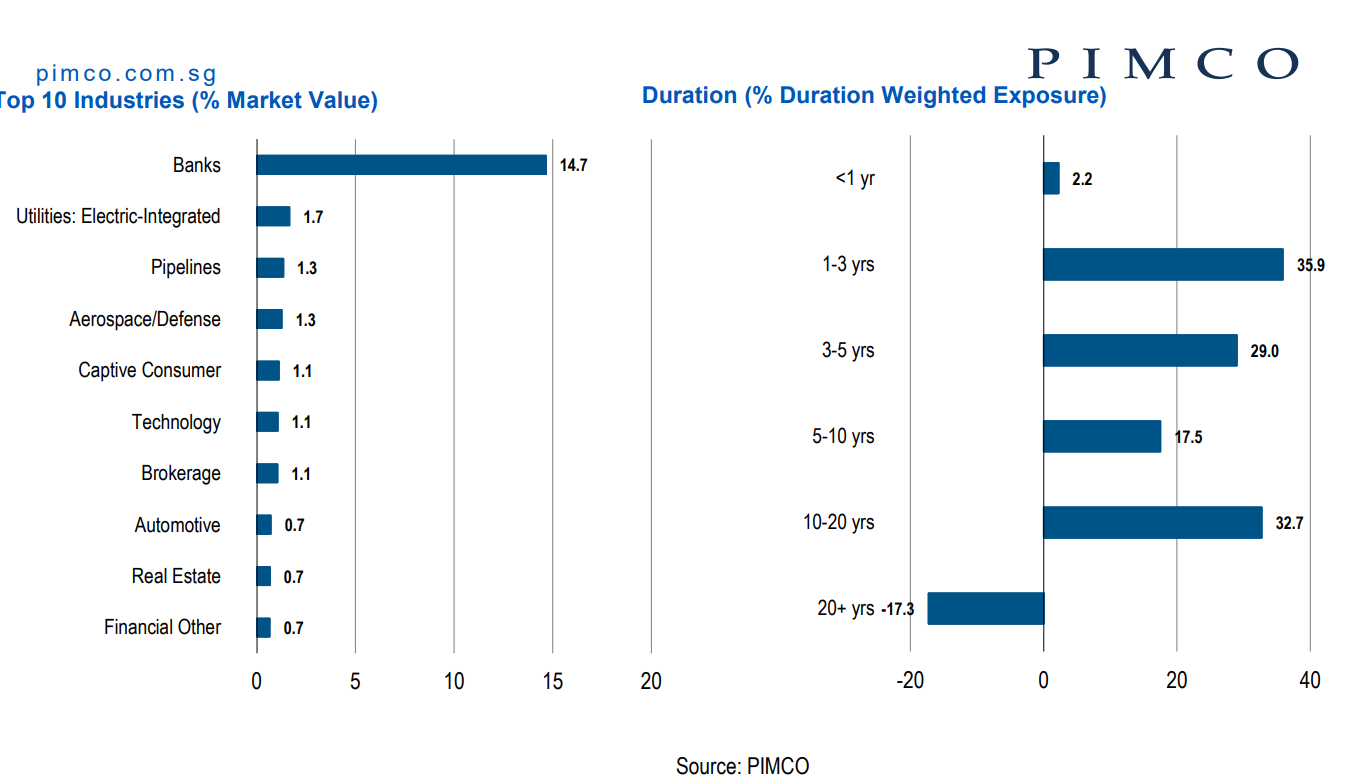

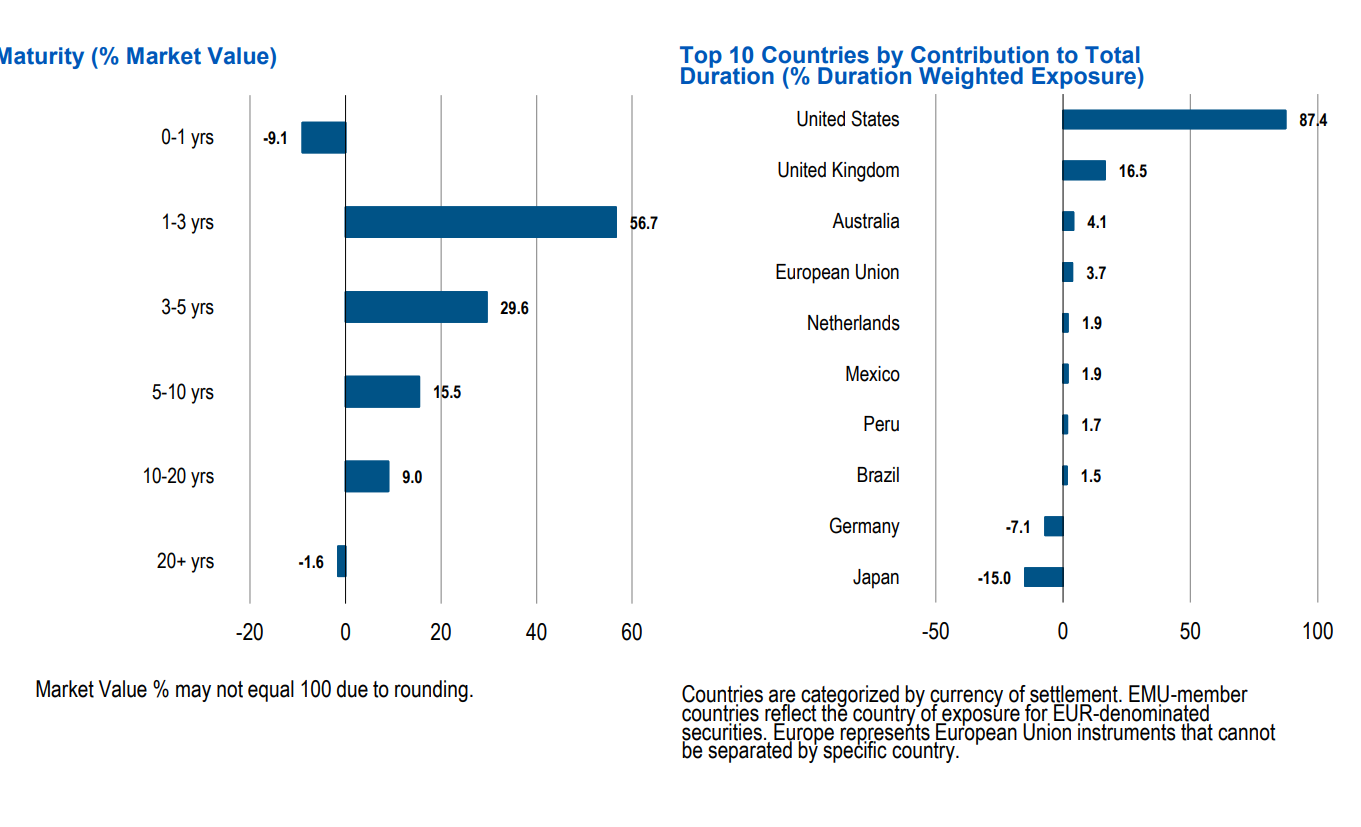

What is the asset allocation of PIMCO GIS Income Fund?

You can see the general asset allocation below.

The largest country exposure is US.

The largest industry exposure is banking.

The bulk of the bonds are 1 – 3 years duration.

And so on.

How risky is PIMCO GIS Income Fund?

But the million question – how risky is PIMCO GIS Income Fund?

6.16% annualised yield, SGD hedged, generally investment grade, what’s the catch?

I do want to stress that Bond funds are quite a bit more complex than a simple T-Bill.

I covered some of the intricacies in a recent article, but to sum up, with a bond fund there is no way to hold to “maturity”.

So yes while you will get the distribution each month.

To get your “principal” back, you need to submit a redemption request to the manager, and they will redeem at NAV (net asset value).

This fluctuates on a daily basis depending on market interest rates, and could be higher or lower than your buy in price.

So it’s not as straightforward as a T-Bill, as the timing at which you redeem the bonds does make a different to the amount you will get back.

On top of that there is default risk, but because these are generally lower risk investment grade bonds the risk should be on the lower side, but definitely not zero like a T-Bill.

There’s also SGD FX risk, but this one is more easily solved by buying the SGD hedged share class (which you should).

My personal view on PIMCO GIS Income Fund?

In the spirit of full disclosure, I myself am invested in PIMCO GIS Income Fund.

There’s definitely no free lunch in this world, and you do need to appreciate that this bond fund carries risk.

The better question is whether the risk-reward is worth it.

As shared previously, personally I’ve shifted to having a strategy of parking cash in ultra short term instruments (eg. money market funds, fixed deposit, SSB), and taking on a bit of duration (2-3 years) for the rest of the cash in exchange for a higher yield.

And PIMCO GIS Income Fund is one of those funds I have been using for the higher duration.

Risk is on the lower side (but not risk free), and duration at 3 years approximately means the capital loss will not be that bad if interest rates continue going up.

But again this is not risk free, and I leave for investors to decide for themselves if its worth it.

How to buy PIMCO GIS Income Fund? Which is the cheapest platform?

There’s broadly 2 options:

- Buy via Endowus, Syfe, FSMOne, Bond Supermart etc

- Buy via your private banker

In my experience (1) usually tends to be cheaper than (2), but it does vary depending on the fund in question and the promotion in play.

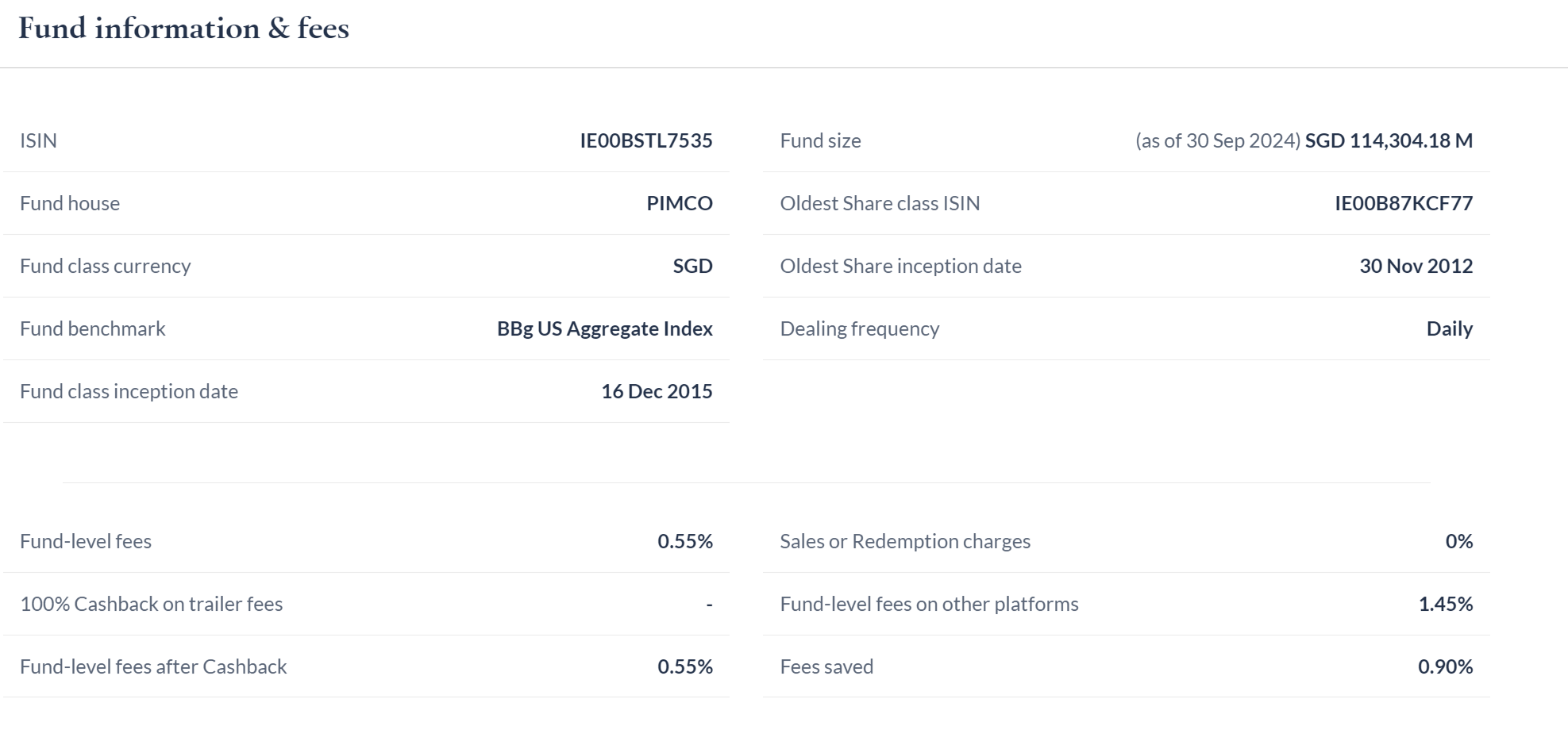

For PIMCO GIS Income Fund, the fee is 0.55% on Endowus.

Throw in the 0.30% Endowus fee and it’s 0.85% all-in.

If any of you out there have a cheaper all-in fee to buy PIMCO GIS Income Fund, please let me know.

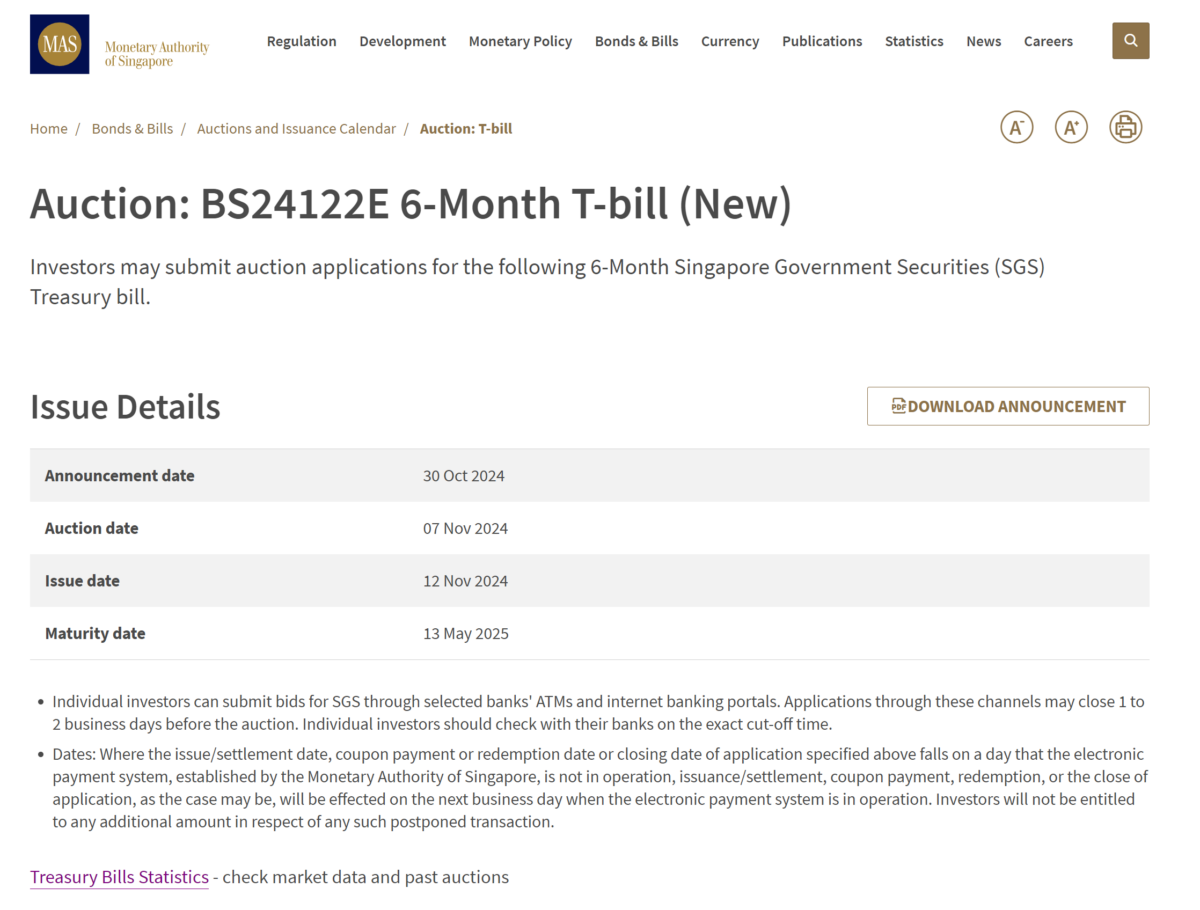

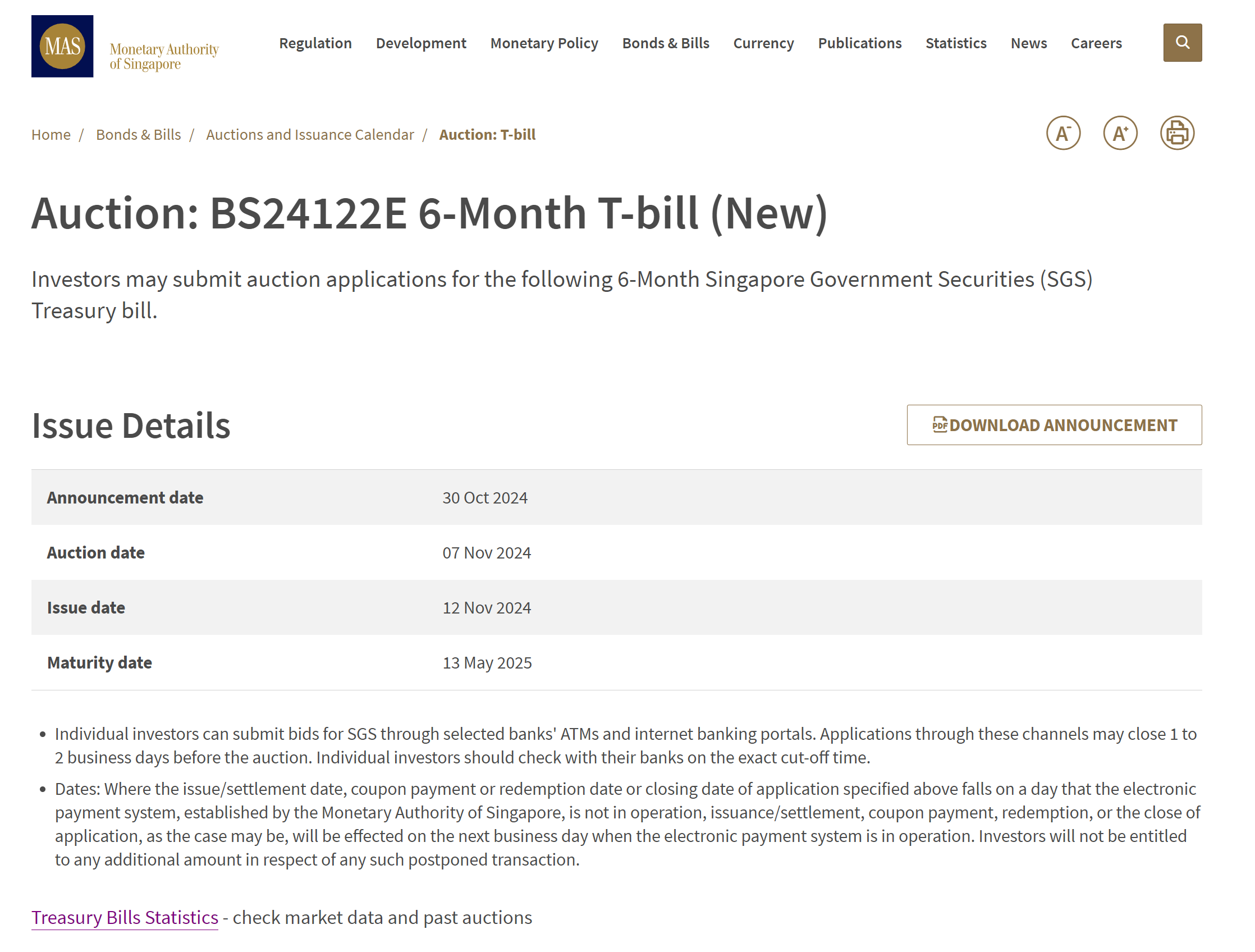

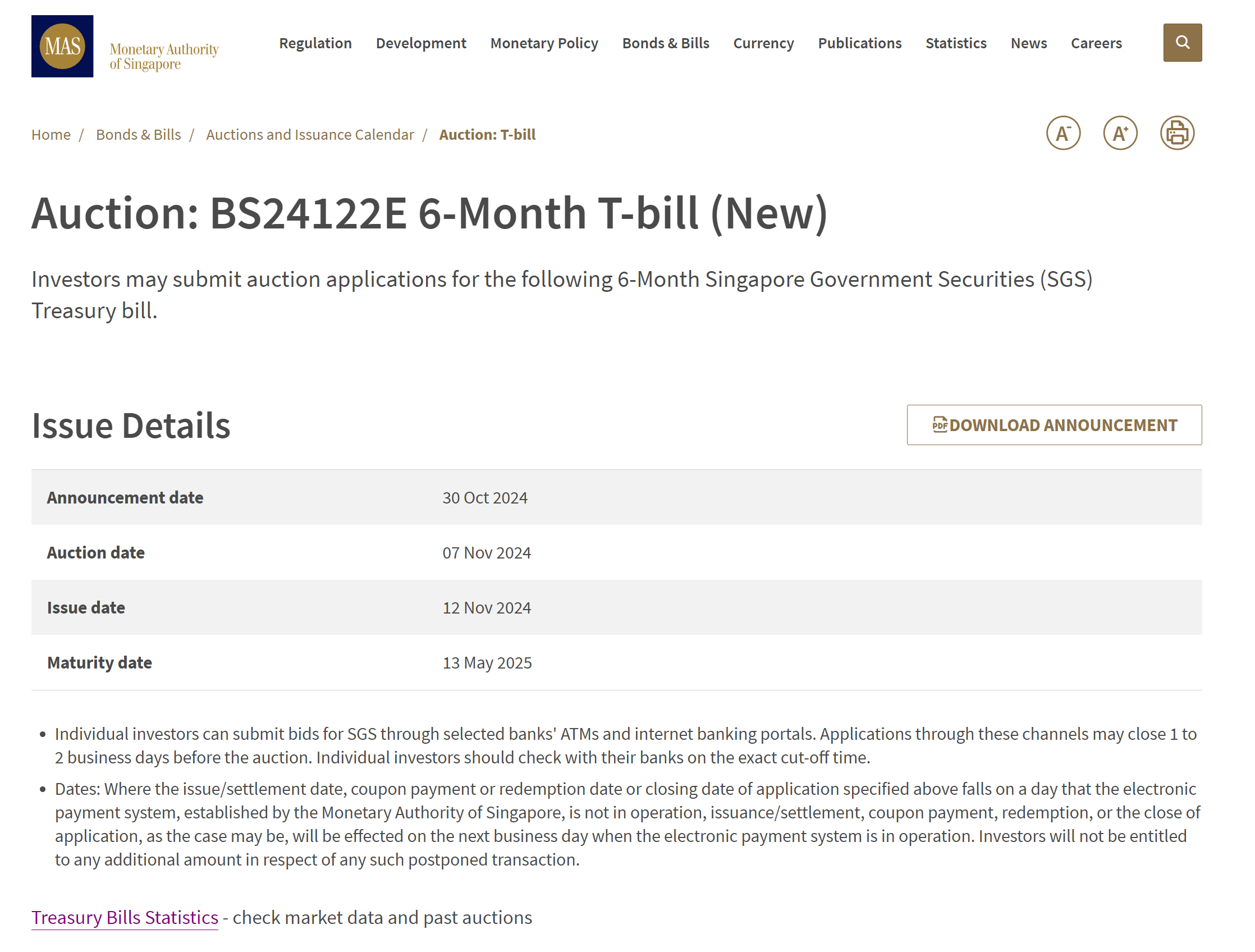

Estimated yield on the next 6-month T-Bills auction?

The next 6-month T-Bills auction is on 7 Nov (Thurs) for those keen to apply.

Deadline to apply is therefore:

- 9pm on 6 Nov (Wed) for cash applications (and CPF-OA applications via DBS or OCBC internet banking)

- 9pm on 5 Nov (Tues) for UOB CPF-OA applications

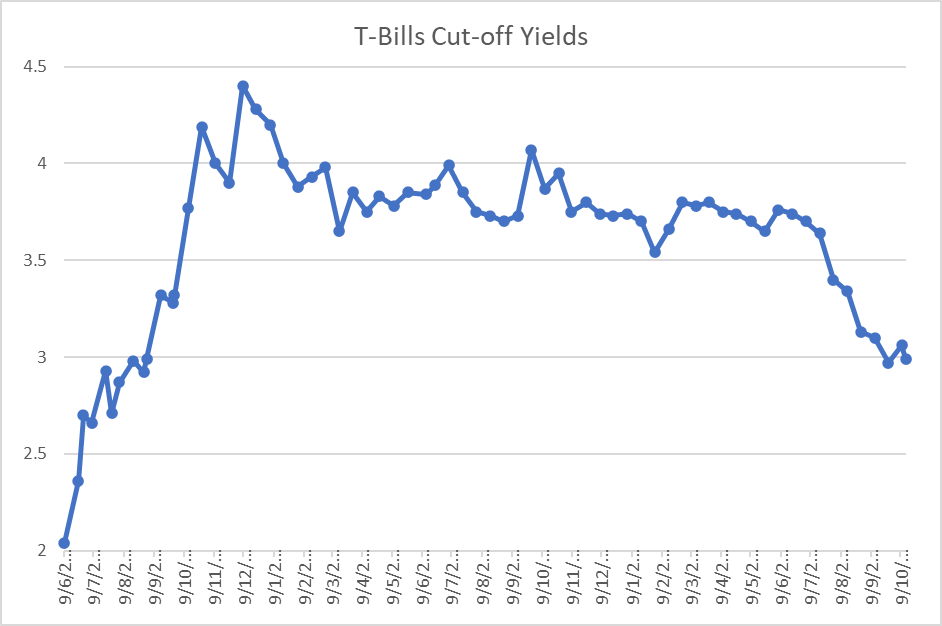

6-month T-Bills yields dropped to 2.99% at the most recent auction (was 3.06% previously)

In the most recent 6-month T-Bills auction, cut-off yields dropped to 2.99% (was 3.06% the previous auction).

Despite the fall in T-Bills yields, demand remains high.

Yes demand has come down slightly, but generally is still very high relative to 2023 levels (when rates were much higher).

6-month T-Bills yields slide on the open market – trading at 2.99%

Follow Financial Horse to avoid missing any post!

On the open market – 6-month T-Bills trade at 2.99%.

That being said – trading liquidity on the T-Bills is so thin that actually the market pricing is not that useful.

So I would caution against placing too much reliance on market pricing on T-Bills.

T-Bills Supply is flat at $6.8 billion (same as past few auctions)

On the supply side, auction amount is flat at $6.8 billion, so this is neutral for yields.

You can see how the auction amount has stayed flat since about June:

Estimated yield of 2.95% – 3.05% on the 6-month T-Bills auction?

All in – I’m going with an estimated yield of 2.95% – 3.05% for the next 6-month T-Bills auction.

Why I stopped buying T-Bills at 3% yields?

At 3%ish on the 6-month T-Bills, I really don’t see them as a must buy anymore.

A year ago when T-Bills were paying 4% yields risk free, they were a no brainer.

But at today’s yields, I think there are a lot of other options there equally if not more attractive than T-Bills.

Why I switched to buying short duration bonds / money market funds instead?

What I’ve been doing is putting my cash into a mix of:

- Cash equivalents like UOB One, Money market funds (like MariInvest) or fintech plays (like Chocolate Finance/GXS/FD) on the short end

- Short duration bond funds on the long(er) end (PIMCO GIS Income Fund for example)

(1) gives me the liquidity at a decent yield, while (2) gives me higher yield (but with the potential drawback of needing to leave the money locked in).

Simplistically if you assume (1) pays about 3% yield today, and (2) pays about 5% yield today, and you blend them in a 50:50 mix.

That’s about a 4% blended yield, with the flexibility to withdraw half of that almost instantly.

Potentially even higher based on how much liquidity you’re willing to trade off.

In my view that’s been superior to just parking the cash in T-Bills, and is generally what I’ve been doing with my own cash and maturing T-Bills.

I’ve discussed the bond funds above, so let me just touch on the cash instruments quickly.

UOB One, Money market fund instruments (like MariInvest) or fintech plays (like Chocolate Finance/GXS/FD) on the short end

I’ve maxxed out UOB One Account, which pays 4.0% on the first $150,000.

I also use MariInvest which is a money market fund that pays about 2.9% over the past 30 days for me.

It’s definitely come down because of the rate cuts, but for something that is pretty low risk and with good liquidity (first $10,000 can be withdrawn instantly, rest is T+1 liquidity), it’s still decent.

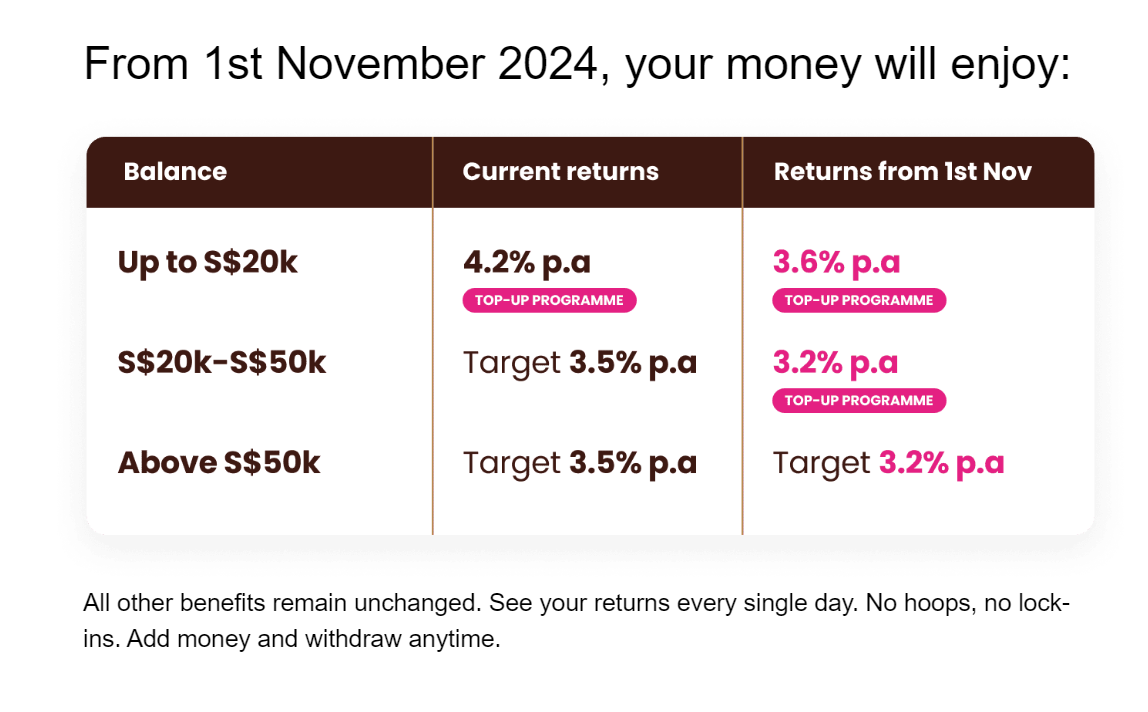

Alternatively, there’s stuff like Chocolate Finance that even after the drop in rates (on 1 Nov), will pay about 3.6% on the first $20,000.

Alternatively there’s stuff like DBS Fixed Deposit paying 3.20% for 12 months, higher than T-Bills:

While GXS is paying 3.28% for 3 months:

There is some investor discretion required here as unlike T-Bills, not all the instruments above (eg. Chocolate Finance / money market funds) are risk free, while DBS/GXS will be risk free as long as you stay within SDIC limits.

But in my view, if you know what you’re doing you should be able to get pretty decent 3%+ yield on cash, for very low risk in today’s climate.

And yet retaining the option of instant liquidity (vs a T-Bill where it is very hard to exit before maturity).

Why I switched to buying short duration bonds / money market funds instead?

So that’s what I’ve been doing for my own cash / maturing T-Bills, but I’m not saying that it’s the only way to do it.

There’s no doubt with this approach the bond component does carry risk, so it really depends on the risk appetite of the investor – and some thought is required as to what is your split between cash / bonds.

If you just want something risk free – then you can stick with T-Bills / government bonds.

Deadline to apply for the T-Bills auction on 7 Nov (Thurs)

The next 6-month T-Bills auction is on 7 Nov (Thurs) for those keen to apply.

Deadline to apply is therefore:

- 9pm on 6 Nov (Wed) for cash applications (and CPF-OA applications via DBS or OCBC internet banking)

- 9pm on 5 Nov (Tues) for UOB CPF-OA applications

This post is written on 1 Nov 2024 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Bond funds are subject to price fluctuation. My bond fund dropped 5% to 20% in past 2 years.

That’s exactly right. Hence bond funds are a great deal more complex / nuanced vs just buying a T-Bills.

Not for everyone.

But this works both ways. A bond fund that can drop 20%, can also go up 20% in the right conditions.

Thank you, I have two comments:

1. Buying govt securities isn’t a make or break decision as implied in the article because it is not even an investment decision. Real investors do that because they can’t find commensurate opportunity to invest their cash in the markets.

2. Current US interest rates are rising and so long as it does, the principal or redeemable “NAV” will fall for the “bond funds”.

Hi Ethan,

Thanks for the comment.

Just to clarify, I’m not saying that buying govt securities is a make/break decision, and my apologies if it came across that way.

I myself continue to hold govt bonds for eg. via MMFs or SSBs and existing T-Bills.

Point of the article was more to say that I prefer the extremely short end of the curve right now, and perhaps the 2 year duration mark – rather than the 6 month.

But like you said, this could easily change in the next week or so, with the US elections and Fed rate cut in play.

What is your view on the PIMCO INCOME FUND SGD-H which is 6.3% ? Why did you choose the USA 6.1% instead ? Thanks

I’m using the PIMCO Income Fund SGD E class.

It’s the SGD hedged share class, with institutional fee class.

Apologies if I used the wrong screenshot.

I bought through FSM, such had zero fees, only holding fees, and then transfer to Stan Chart (which levies 1% sales charge but no holding fee). The transfer process was slow so I had to pay for one quarter holding fees to FSM, but it was minimal, and all still worth the hassle.

Interesting – appreciate the sharing very much.

BTW just to clarify – the one you bought via FSM is the institutional share class? Not the retail share class?

Retail

PIMCO has different share classes. EndowUS is the institutional class. Banks distribute different retail classes (e.g. I know one local bank is admin class, one foreign bank is E class).

https://www.pimco.com/sg/en/investments/gis/income-fund/e-sgd-hedged-income

This website contains the details of each share class.

Do we solely look at the fee? I realize that each class has different YTD return and also different distribution.

How do I work out the total return for each share class

To my knowledge they are the same underlying fund, the difference is the fees.

So as long as it’s the same underlying fund, pick the one with the lower total expense ratio (TER).

Total return for the share class is basically the performance net off fees, hence the biggest difference is fees.

Unrelated, but now would be a good time to take out your crystal ball and speculate on the macro economy with Trump at the helm!

Inflation : Resurrection (2025)?

Indeed, I just did an article on this last week! https://financialhorse.com/how-i-would-invest-in-2025-after-trumps-win-will-inflation-return/

Thanks for the sharing – this is really interesting.

Btw, I personally use POEMS for funds – they also offers the E class at 0% sales and platform fee, and I like that they have the option to withdraw or reinvest the monthly distribution at no cost. Also helps that the minimum investment is $1.

Thanks for the sharing – very much appreciated!

What’s your view on Pimco Balanced Income and Growth, which is 60stocks/40bonds, bonds component some similarities in holdings as this Pimco Income Fund.

I prefer to use PIMCO only for the bonds which are harder to replicate by myself. The stocks component I can easily replicate via a low cost ETF if I am so inclined.

I think PIMCO can be bought from DBS at 0.82% sales charge flat.

Need to check which share class you are buying into, as the retail share class carries a higher expense ratio vs the institutional share class.

DBS is charging me 1% sales charge for PIMCO GIS Income Fund (Admin Shareclass)