So I’ve set out UOB’s chart below, and it’s a pretty unbelievable recovery.

COVID, zero interest rates, and the greatest recession since WWII.

But hey – UOB’s share price is almost back to pre-COVID levels.

We’ve covered DBS and OCBC already, so in this article let’s take a look if UOB is still worth buying – after the massive rally.

Note: The research for this article (and the charts) are sourced from ShareInvestor Webpro. It’s a great way to quickly perform research on Singapore stocks, more comprehensive than other options like Yahoo Finance.

You can learn more in my review on ShareInvestor Webpro here.

Basics: UOB Bank

UOB needs no introduction.

It’s the third largest bank in Singapore by market cap, behind OCBC and DBS.

Each of the 3 banks has a slightly different flavour.

DBS is Temasek backed, and it has the biggest funding base in Singapore because of its merger with POSB.

OCBC has big HK and China exposure because of their acquisition of Wing Hang bank a while back. They also have the biggest exposure to insurance via Great Eastern.

UOB by contrast, has the biggest exposure to South East Asia and SME/Individuals. Which of course, has not been kind on UOB’s share price.

UOB’s Financial Results

A quick look at the financials.

Earnings are remarkably steady, down slightly only from 2019.

Loans under moratorium have fallen drastically, from 16% to 10%.

Interestingly, the bulk of the loans still under moratorium now are in Singapore – because of the measures enacted by the Singapore government.

Non-performing loans is at an unbelievable 1.5%. Real testament to how unprecedented the government stimulus has been this time around.

As mentioned above – UOB’s loan book carries big exposure to South East Asia, and SME/Individual.

For this reason they’re still trading at a discount to DBS, which has a much higher quality loan book.

Loan growth is flat, which is not a surprise in this climate.

No bank wants to extend loans unless it’s an ultra-safe borrower, and the ultra-safe borrowers can easily raise money on capital markets much cheaper.

SIA just raised $500 million USD at 3% a year (5 year bond), and it was oversubscribed more than 5 times.

Strange world we live in.

Balance sheet is really strong. Unlike 2008, very little risk to the banks this time around.

Financials are backward looking

That said, financial results are always backward looking.

They tell a picture of UOB at a specific point in time.

And as investors, we always want to look forward.

And going forward, there’s 3 big things that will affect UOB’s share price:

- Interest Rates

- Bad loans

- Growth going forward

Interest Rates

Interest rates go to the very heart of UOB’s business model.

Banks like UOB borrow money short term, and lend it out long term. When interest rates go up, UOB makes a lot more money from the lending out.

To forecast UOB’s earnings going forward, we need to understand where interest rates will be.

And US interest rates set the stage for the whole world, so we need to look there.

US Treasuries

It’s been a crazy Jan for Treasuries.

10 Year yield opened the year at 0.9%.

After the Democrats won the senate (blue wave), paving the way for A LOT more stimulus, 10Y yields have jumped to 1.1%.

Investors are pricing in a lot more stimulus, which means more inflation, which means the Feds will be forced to raise rates earlier (hypothetically).

Hence bonds sold off, yields rose, and bank prices jumped.

Are yields really going up?

The big question though – is whether this is true.

If interest rates are going up like markets are pricing in, then banks are a screaming buy.

But if they’re staying at 0, then well, banks are about fairly valued.

My personal view – I don’t think interest rates are going up for a long time.

2024 kind of territory at least.

I think the market is getting ahead of itself.

Many Fed Members have come out recently to say that they don’t plan to raise rates for a long time, and I just absolutely agree with them.

With the kind of debt load the world has, and the sluggish economic growth, rising rates will crash the entire world.

If yields get too high, I expect the Fed to step in, possibly with some kind of pseudo yield curve control.

This will not be good for net interest income (NII) for banks.

BTW – we share commentary on the COVID crisis every weekend, so please sign up for our mailing list, its absolutely free.

It’s a weekly newsletter that goes out every Sunday, and rounds up the week’s posts so you never miss anything.

Don’t forget also to join our Telegram Channel!

[mailmunch-form id=”928667″]

Bad loans

The next big one is bad loans.

If companies go bankrupt and can’t repay their loans, UOB loses lots of money.

So far, non-performing loans are at an unbelievable 1.5%, because of all that government stimulus, and loan moratoriums.

As 2021 plays out, more of these loan moratoriums to fall off.

What happens next?

The Singapore government doesn’t have a blank cheque to help everyone (unlike 2020). We’re constrained by financial resources, and 2020 was a case of save everyone first, ask questions later.

But moving forward, I think the government will be more selective. The decision has to be made as to who is worth saving, and who isn’t.

But I think the process has to be managed.

If bankruptcies spikes suddenly, that could derail the economic recovery, and undo all the hard work put in.

So my gut feel is that NPLs will tick up slightly, but they will not go through the roof.

Given the amounts of loan provisions the banks have set aside to cater for bad loans, this is probably not a bad thing.

US Banks

JP Morgan came out last night to release a big chunk of the loan loss provisions set aside in 2020.

According to them – they expect a stronger economy going forward, and the level of los provisions set aside from last year is now excessive.

Pretty bullish stuff.

UOB’s growth

Growth going forward, will depend on 2 things:

- Economic Growth

- Growth of market share

Economic Growth (Singapore + ASEAN)

UOB’s loan book is concentrated in Singapore + ASEAN, so when I talk about economic growth I’m referring to this region.

ASEAN’s going through a rough patch now, but COVID won’t last forever.

When we get out on the other side, I do expect that economic growth will rebound.

So this one I’m less worried.

Mid to longer term, I’m bullish on Asia and on ASEAN. Lots of growth to come in this decade.

Growth of Market Share – the rise of the Digital Only Banks?

Market share is where it gets a bit more tricky.

I’m less worried about the Singapore banks because frankly – I don’t see OCBC/DBS stealing big market share from UOB. The market has just settled into this steady state where each bank has their own audience.

The one that’s more concerning – is the rise of the digital banks.

There are 2 ways to see it:

- Growing the pie – Digital banks will carve out a new niche, a previously unbanked audience. This grows the pie

- Splitting the pie – Digital banks focus on stealing market share from the traditional banks. The pie remains the same size, but the split changes

If we go down 1, that’s ok for UOB.

If we go down 2, that’s worrying for UOB.

The one that I would be worried about is SEA. Their execution so far has been really impressive, and they’re making big moves with their SEA Money in Indonesia.

Really excited to see that they have in store.

The Grab-Singtel partnership I’m less worried – I’ll take a more of a “show me” approach with them.

Tough to predict how this one will evolve, so it will be important to keep an eye on developments here.

Valuations of UOB

|

Bank |

Price to Book |

Market Cap |

|

DBS |

1.35 |

68b |

| UOB |

1.07 |

39b |

|

OCBC |

1.02 |

47b |

DBS is the highest because objectively, it does have the safest loan book and it’s Temasek backing makes it very safe.

OCBC has big exposure to Hong Kong and Greater China, which is a big of a question mark now. Hence the lowest valuation.

UOB has exposure to SEA and SME/Individuals, so it’s somewhere between the two.

My personal view?

Personal view – I think DBS is on the high side in terms of valuation.

UOB and OCBC, they’re probably fairly valued to slightly overvalued. But definitely not in the realm of bubble territory just yet.

UOB’s Dividend

Historical dividends are set out above, but frankly they don’t mean much because banks were required by MAS to cap their dividends in 2020.

Going forward, I think MAS will remove this requirement.

And based on a UOB report, the kind of yields we can expect to see going forward are:

- DBS – 4.0%

- OCBC – 4.7%

Which would put UOB at approx. a 5% yield.

In other words, banks have become the new REITs. You buy them and collect a 5% yield.

Unbelievable.

Historical yield is about 4.5% with a 50% payout ratio, so this could indicate some upside in UOB’s share price when things fully normalise.

Shareholders of UOB

Couple more points to look at, then I’ll round up my views.

The Wee Family (Wee Cho Yaw) is the single largest shareholders. Haw Par Corp (of Tiger Balm fame) is a notable shareholder as well.

Buybacks of UOB

Nothing meaningful in terms of buybacks. Most of this was done in March on the way down.

Will I buy UOB Bank?

It’s a tricky time to be investing.

There’s a lot of liquidity out there, a lot of bullish sentiment, and a lot of froth.

It’s easy to get carried away in times like that.

But longer term, valuations really matter. If you buy a stock at too high a price, it really affects future returns.

So I think this time around, the answer has to be a bit more nuanced.

For me personally

I bought a lot of UOB and DBS last year.

Even before COVID, I already held large positions in both banks, so Singapore banks are a big portion of my portfolio now.

Is there a need for me to add urgently now, and at these prices?

Not really.

If it goes back to low 20s sure I may add, but at 23-24, I’ll probably just hold my existing positions and collect the yield.

Longer term, I do expect the share price to continue its recovery as the COVID recovery plays out.

No big urgency to sell either, because 1.07x book value is reasonable and not a screaming sell.

For new investors

But for new investors who have completely no exposure to banks, I get how this can be a tricky situation.

Banks are an important diversifier in any portfolio, and a bank like UOB is one of the best ways to get broad exposure to the Singapore + ASEAN economy.

Current prices are not cheap compared to last year, but they’re also not demanding from a long term valuations standpoint.

If I had no banks in my portfolio and I were starting out in investing today?

Yeah, I probably would add UOB / OCBC but with a view to averaging in.

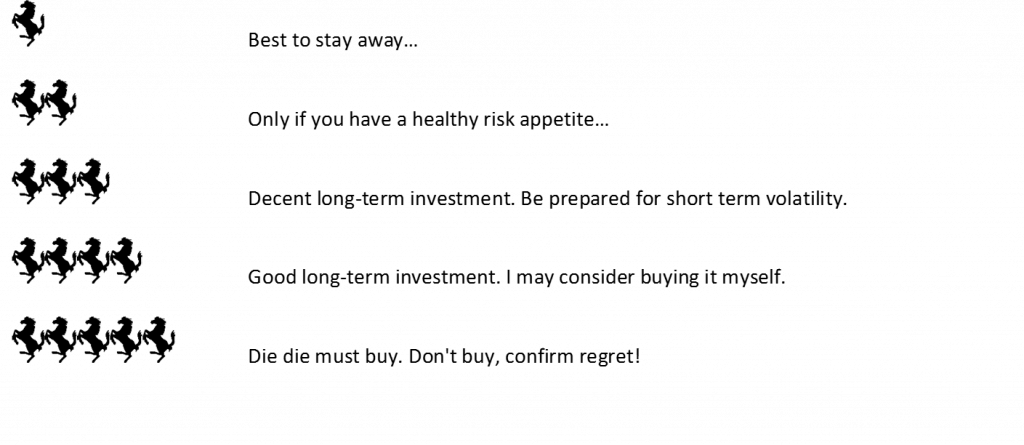

Closing Thoughts: 3 Horse Rating

UOB is a 3 horse rating for me.

Prices have gone up significantly, but the economic climate has also changed significantly since we did the pieces on DBS and OCBC.

A Biden presidency with Democrats controlling both houses portends a lot of stimulus coming. This is bearish for the USD, which is amazing news for Emerging Markets.

And at the same time the Feds are boxed in. They can’t raise rates or the global economy will break, and if yields go up they may be forced into yield curve control.

Very, very similar dynamics to the post WWII period.

The role of banks have changed drastically since the 1940s, but here in Asia they still form a big part of the funding base for companies. It’s a fantastic way to get broad exposure to the Singapore and South East Asia economies.

That said, short term, I think global equity indices are starting to look overbought. Lots of froth in certain areas such as small cap tech and IPOs.

I do think we’ll see a correction some time this year, but it’s unlikely to hit the value names too hard because valuations are still undemanding here.

For me though, I’m not buying UOB at this price because I already own a lot of it. But neither am I selling. I’m just holding on for the ride.

As always, this article is written on 16 Jan 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Love to hear your thoughts!

UOB – Financial Horse Rating

FH Rating Scale

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!