I recently received this question from an FH Premium subscriber:

Hello FH, in view of current Fed action, how would u choose?

Choose a low 3 years fixed rate at 2.5%?

Or a higher rate at 2.75% with free conversion after 12 months?

For the record, this was my response:

That’s a tricky one.

If this were me? I would probably take the 2.75% with free conversion after 12 months – take the punt that rates in 12 months are lower.

But there is definitely a risk that it may not pay off.

Do you mind if I write an article on this?

Would give me room to cover the thought process in further detail.

But as I thought about it a bit more, I realised the answer was not so straightforward.

So I wanted to share fuller views in this article.

What is the path for interest rates going forward?

FH Premium subscribers know my view on this.

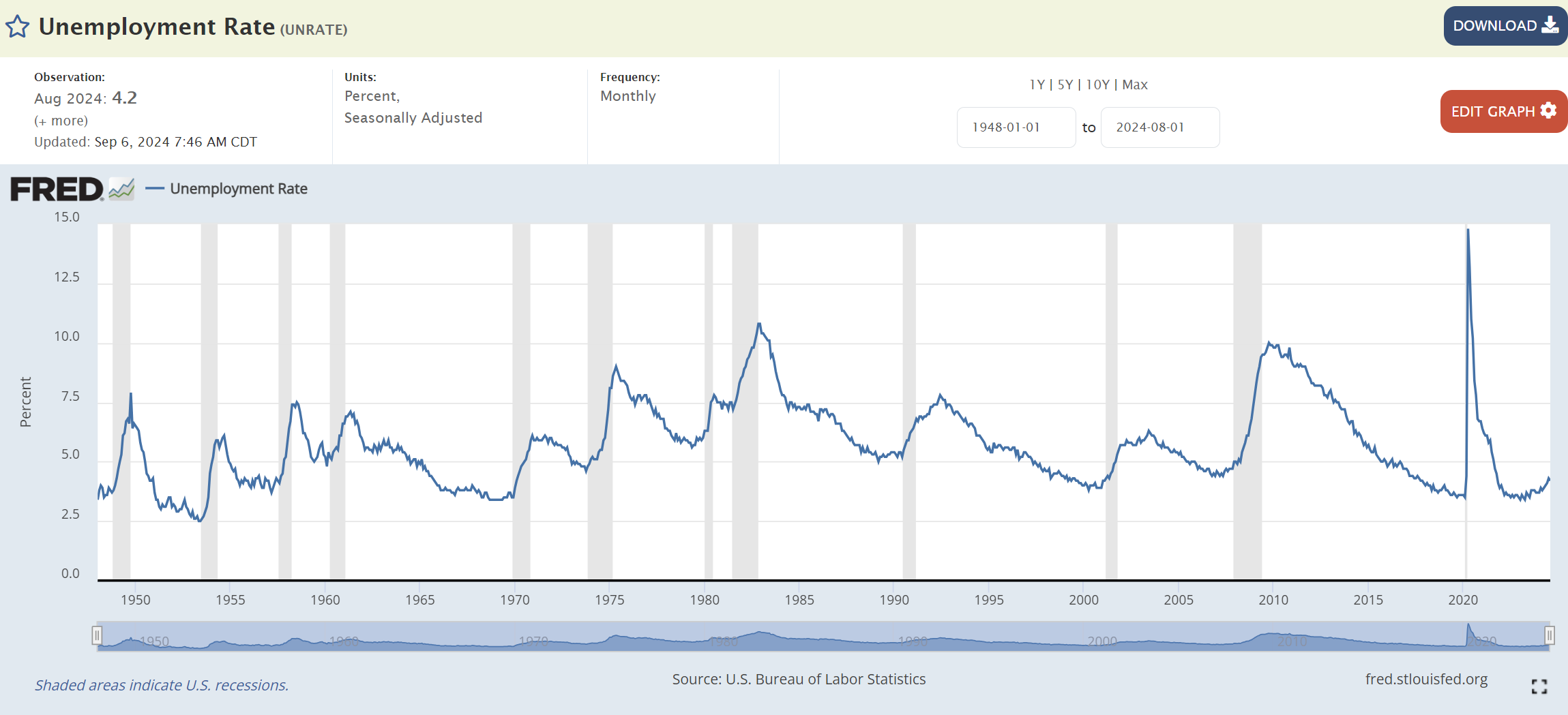

I think that between inflation and unemployment, the risk for the Feds has now tilted towards the latter.

If we take a step back – the problem is that the moving averages of US unemployment has been rising for quite a while now.

And historically, unemployment is not a stationary series.

Whenever it moves up by a certain level, it almost always develops a momentum of its own and continues to go up.

For example the Sahm Recession Indicator signals the start of a recession when the three-month moving average of the national unemployment rate (U3) rises by 0.50 percentage points or more relative to the minimum of the three-month averages from the previous 12 months.

Sahm rule has risen to 0.57%, which hits the threshold for a recession each time the past 40 years (did not trigger in the 1995 soft landing).

Here’s Conference Board’s labour market differential (jobs “plentiful” minus jobs “hard to get”).

It dropped a full 10 points in September, and now its down almost 31 points from its 2024 peak.

The last time it was this low after coming down from a high?

Was 2020, 2007, 2001, 1990, 1970 – all recession years.

Jerome Powell’s “hawkish” cut?

Now if you look at what the Feds have pencilled in in their most recent economic projections.

Jerome Powell is signaling 2 more 25 cuts in 2024, and a further 100 bps in 2025.

But crucially in this scenario – he projects unemployment to rise to 4.4%, and to stay there until late 2025.

The problem of course is as we discussed above.

Given that US unemployment has been rising – will it just stop and stay there for the next 12 months?

The soft landing folks will argue that this time is indeed different as the structure of the economy has shifted post-COVID.

But me I’m not so sure, and I truly think the jury is still out on this one.

While I am not outright calling for a recession, I definitely don’t think that recession odds are as low as what the market is pricing in.

And if I am right, there is downside risk for interest rates here.

But let’s see – time will tell.

What has the market priced in on interest rate cuts?

The market has priced in pretty aggressive rate cuts, and from the discussion above I’m inclined to agree.

What’s priced in is a 62% chance of a 50 bps rate cut in Nov, and a total of 2.0% in rate cuts by mid 2025.

That’s a lot of rate cuts coming.

Which is the best mortgage option to take?

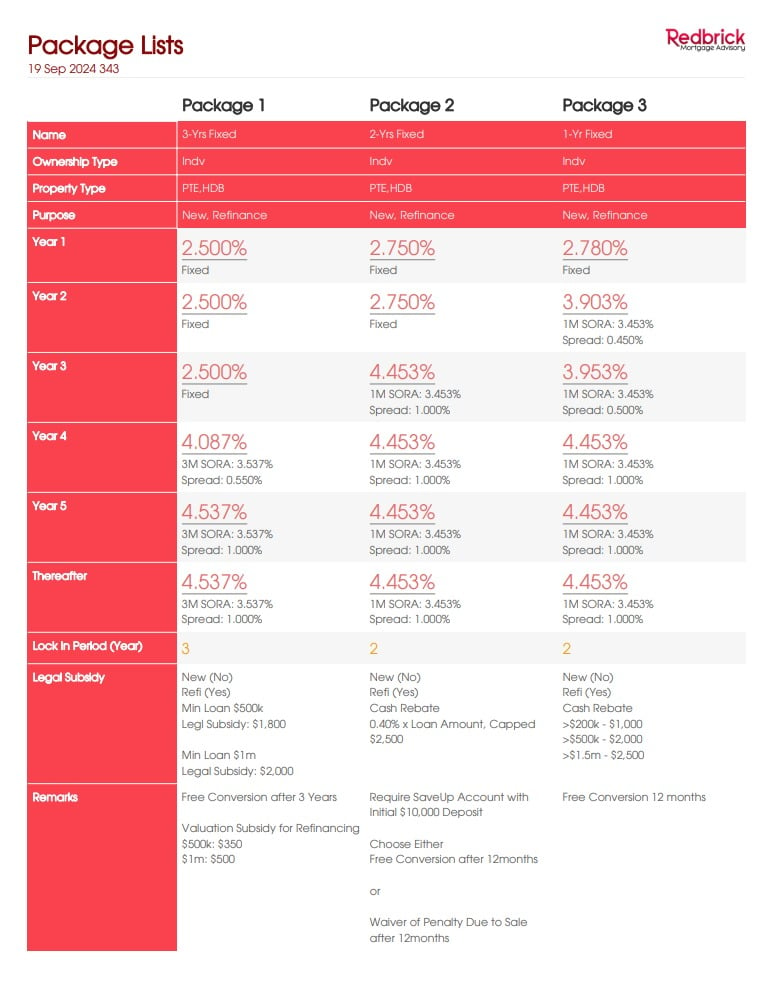

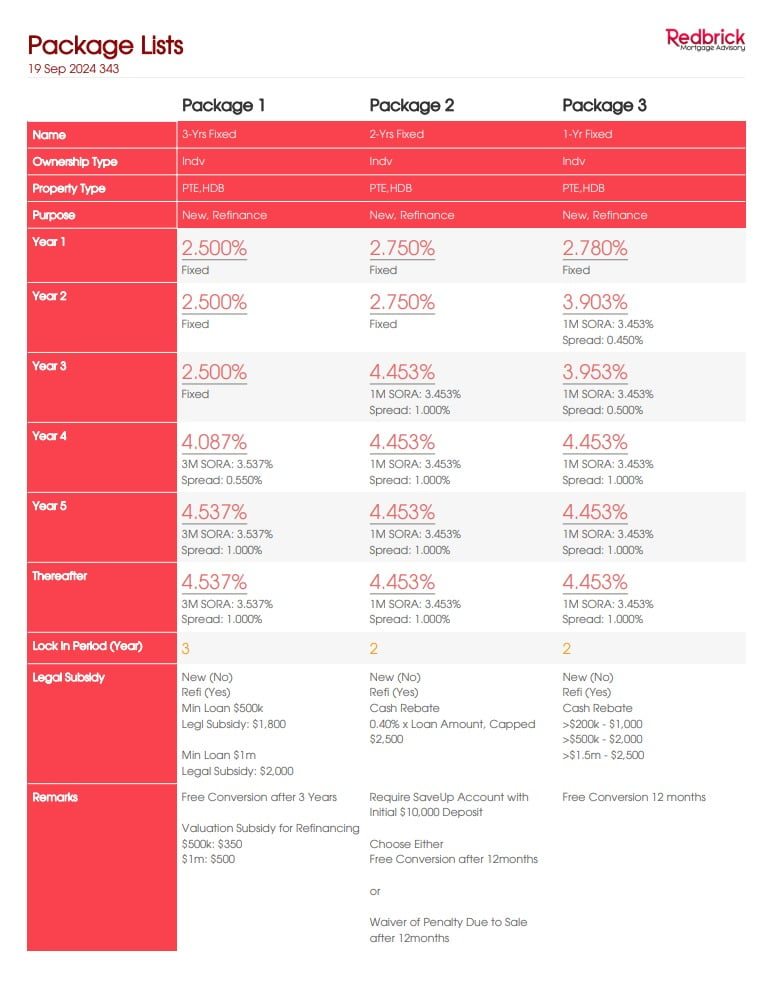

To sum up the 2 options from the reader:

3 years fixed rate at 2.5%

2 year fixed rate at 2.75% with free conversion after 12 months

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

How does this compare vs the risk free rate?

The latest 2 year Singapore government bond yield trades at 2.4% on the open market.

Which means the 2.75% fixed for 2 years trades at a 0.35% spread vs the risk free.

While it’s about 0.1% for the 3 years fixed.

By this logic, the 3 years fixed rate mortgage looks like the better buy.

What is the “cost” of the free conversion after 12 months?

The complexity of course, is that the 2 year fixed rate option has the option to reprice after 12 months.

The way this works is that if interest rates plunge in the next 12 months.

You can go to the bank 12 months later and ask for a free “reprice”.

And say if the mortgage rate is 1.8% 12 months later, the bank may give you a 1.9% rate (small premium lah… bank also need to eat…).

How much is this optionality worth?

Don’t forget you need to factor in the higher interest rate you are paying in the first year.

Effectively you need to be able to refinance to 2.25% in 12 months time, to be able to get an average interest rate of 2.50% for 2 years.

That’s a fairly big drop in interest rates.

If the mortgage rate is higher than 2.25% in 12 months time, you might be better off just going with the 2.50% fixed.

Curveball – a third option? Three year fixed rate with option to reprice?

Then the FH Premium subscriber wrote in with an update:

They just updated me with a 3 year lock in with 2.65% and 12 months free conversion to fixed or Sora

So there’s now 3 options:

3 years fixed rate at 2.5%

3 years fixed rate at 2.65% with free conversion after 12 months

2 year fixed rate at 2.75% with free conversion after 12 months

It’s safe to say that in coming up with these options, the bank has already spent a lot of time crunching the numbers on their end, and so the options do by and large reflect what is priced into the market.

So the question is more of what do you as an individual investor prefer.

My personal view?

Gun to my head?

I think it’s a toss up between the 2 or 3 years fixed, but both with the free conversion option.

Personally I might go for the 3 years fixed rate at 2.65% with free conversion after 12 months.

More on my thought process:

I want the option to reprice after 12 months

Per discussion above, I think in the next 12 months you’ll either see US unemployment continue to rise, or you will not.

In the former – this could be a hard landing scenario, and interest rates might drop quite a bit.

For the 3 year fixed rate you’re paying 15 bps for the optionality to reprice after 12 months.

Personally I would take that bet.

It’s like an insurance against rate cuts if you like.

You’re paying a small extra each month – for the possibility of large savings if rates drop.

If you’re wrong, you just end up paying a slightly higher amount each month, but it’s not like you suffer a huge loss.

2 or 3 years fixed?

The question then is whether to take the 2 or 3 years fixed mortgage.

The way the curve is priced today – it’s flat from the 2 year out to the 5 year mark.

We’re seeing 2.38% on the 2 year SGS, and 2.42% on the 5 year SGS.

Market is basically expecting interest rates to stay flat from the 2 – 5 year mark.

The way I see it – if there isn’t a sharp drop in interest rates the next 12 months, then maybe locking in for 3 years is not a bad idea, as

- It hedges against the risk of higher interest rates down the road

- You save 10 bps on the interest rates

Because of that I *might* go with the 3 years fixed with option to reprice, but I think it’s quite close and I would not fault you for going with the 2 years fixed too.

Closing Thoughts: Which is the best mortgage rate to pick?

Like I said though, I don’t think there is a right or wrong here.

Projections like these have a way of making the best investors look foolish.

So I would take all the projections above with a pinch of salt.

Just make the best decision based on information that you have today.

And live with it.

Worst case, you can always refinance in 2 or 3 years.

This post is written on 27 Sep 2024 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Saxo Brokers – Trade the 100 most popular US stocks commission-free

Saxo is running a promotion where new account holders can trade the Top 100 US stocks commission free (more details).

Special account opening bonus for FH Readers:

- Sign up via the link: Saxo Brokers

Chocolate Finance- pays 4.2% yield on first $20,000

Chocolate finance pays 4.2% on the first $20,000, withdrawable instantly.

The funds are invested in a selection of bond and money market funds, and Chocolate Finance will top up any returns if they are lower than 4.2%.

I wrote a detailed review on Chocolate Finance (note not SDIC insured).

- FH invite link below:

https://share.chocolate.app/nxW9/ep4q7wxp

Stock Café – track your portfolio performance (including dividends)

I use StocksCafe to track my portfolio and dividend stocks (full review).

- FH x StocksCafe Referral Code:

https://stocks.cafe/user/tosignup?referral_code=financialhorse