In case you haven’t been following, AEM Holdings has been on an unbelievable run this year.

AEM Holdings is a SGX listed semiconductor testing company.

The stock started 2026 at $1.7 — and this week it touched as high as $8.

That is a 370% increase in 4 months — an unbelievable move for an SGX-listed stock.

$2.5 billion market cap too, so its not exactly a penny stock.

So… will I buy AEM Holdings at these levels?

AEM Holdings soars 370% in 2026

Here’s the price chart for reference.

AEM Holdings was at $1.7 at the start of 2026.

It hit $8 this week — a 370% increase.

The more notable point is the velocity of the move. As recently as end-February, the stock was still trading at $2.

It then went from $2 to $8 in the span of 2 months — which puts the recent move firmly in parabolic territory.

What does AEM Holdings do?

Now what does AEM Holdings do?

Broadly, AEM has three business lines:

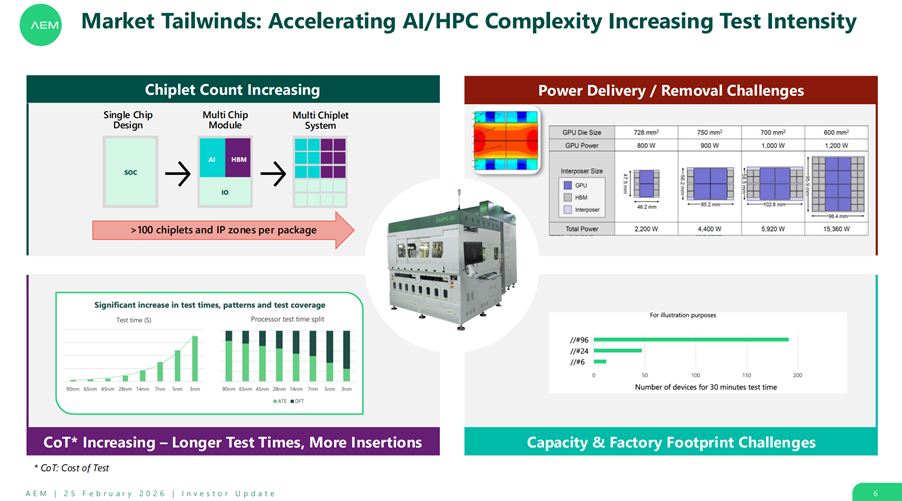

- Test Cell Solutions (TCS): This is AEM’s primary revenue driver. They design and manufacture advanced test handlers for System Level Test (SLT), burn-in tests, and functional tests. Their proprietary modular platforms integrate mechatronics, active thermal control (which is crucial for cooling high-power AI chips during testing), and vision inspection to detect defects and verify package integrity.

- Instrumentation: AEM provides specialized testing instruments and equipment for laboratory, manufacturing, and field-use applications.

- Contract Manufacturing: Beyond dedicated semiconductor testing equipment, AEM offers contract manufacturing services. This includes printed circuit board (PCB) assembly, wire-harness systems, and sub-assembly manufacturing for various industrial applications.

In plain English?

AEM Holdings makes testing infrastructure for processors – like the equipment picture above.

Historically, their biggest customer was Intel — but as we’ll see below, the customer mix is shifting.

Earnings are decent – but it’s the AI tailwind doing the heavy lifting

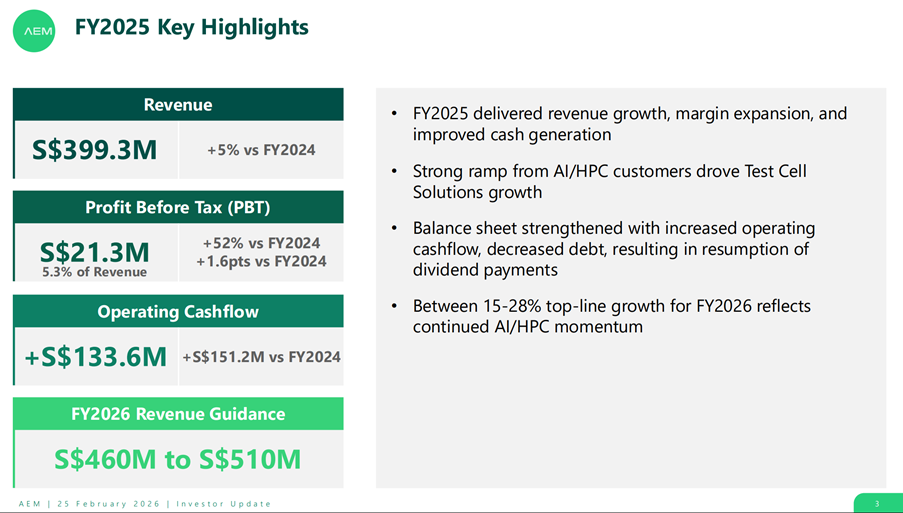

FY2025 earnings were nothing remarkable — up 5% from 2024.

But nobody is buying AEM Holdings for historical earnings. The story here is the growth runway from FY2026 onwards, driven by AI.

Management is guiding for 15–28% revenue growth in FY2026, largely on the back of AI demand.

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

AEM Holdings used to be all about Intel — but that has changed

Now historically, AEM Holdings was almost entirely a play on Intel.

At peak during the 2018–2021 cycle, Intel accounted for over 90% of AEM’s revenue and profits.

If you owned AEM, you effectively owned an Intel supplier.

Based on AEM’s latest results, that picture has shifted meaningfully.

Intel revenue actually declined year-on-year, and the FY26 guidance of S$460 million to S$510 million is now underpinned by three legs:

- A new anchor AI/HPC customer — management has explicitly guided that this new customer will overtake Intel to become AEM’s top customer by revenue in FY2026. This customer already accounted for over 25% of AEM’s Test Cell Solutions (TCS) segment in FY25.

- A second AI/HPC customer — expected to scale up from here, with the potential to become AEM’s largest customer by revenue over time.

- A tier-1 memory customer — equipment evaluation is on track, with production units slated for delivery in late FY26 ahead of a full production ramp in FY27. Market speculation points to Micron or SK Hynix given the HBM testing context, but neither has been confirmed.

This is a meaningful change for the AEM thesis.

If all your revenue comes from one customer (as was the case historically), that is significant concentration risk.

If it comes from two, it is still concentration risk — but the picture looks much better.

And with three large customers, plus potentially a fourth in the pipeline, this is a fundamentally different business from the old AEM Holdings that was effectively an Intel supplier.

Who is this new anchor customer?

I did some digging around on this.

Based on the speculation and information I could find, it looks like the new anchor customer is AMD (with NVIDIA as a lower probability alternative).

It makes sense too, because AMD plays in the x86 space just like Intel, so the Intel testing equipment can likely be easily repurposed for AMD.

If this is true, this is great news for the AEM story as AMD is well-placed to ride the AI capex cycle (arguably better than Intel).

AMD’s share price has also gone parabolic per chart below.

Valuations of AEM Holdings

The latest valuations are below.

Trailing P/E is not particularly meaningful given the sharp inflection in growth.

Using FY26 forecast earnings, we’re looking at about 49x forward P/E.

For context, AEM has never sustained a forward P/E above ~25x outside of brief peaks, and its long-run average is closer to 15x.

What this means, is that the current re-rating only “works” if you think that this current earnings boom is structural and not cyclical.

In plain English – AEM’s current valuations have never been sustained for long historically. For AEM to stay at these levels, you basically need to believe that this huge AI earnings boom is here to stay for AEM Holdings, and it is not that case that after 1 year customers stop buying so much testing equipment and demand falls off a cliff.

Benchmarked against peers, AEM sits in the middle of the AI test-equipment cluster — Teradyne at 40–50x, ASMPT at 42x, and Cohu at ~83x.

The important qualifier is that the entire semiconductor space is itself trading at AI-cycle highs.

So AEM is not a cheap stock relative to peers; it’s a fair-value stock in a richly-valued sector.

The closest comparison for AEM is Cohu. Both are pure-play test handler specialists, both are smaller-cap names with concentrated customers, and both have whipsawed through the Intel and now AI cycles. Cohu trades at a higher absolute P/E (~83x) but with more diversified end-markets across auto, industrial, mobile, and AI — so AEM trading at a discount to Cohu looks fair, given its higher customer concentration risk.

In summary — AEM Holdings is hard to call cheap on a valuations basis.

The most defensible read is that AEM is fairly valued relative to its semiconductor peers, but the sector as a whole is richly valued.

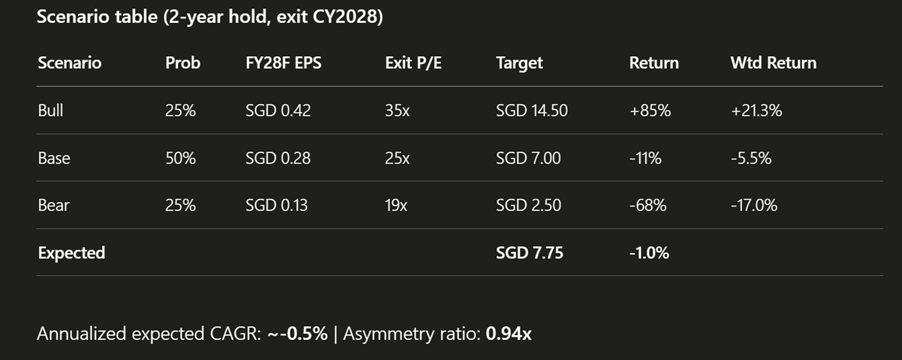

Bull, base, bear scenarios for a 2-year hold

I ran the bull, base and bear case scenarios with target prices for each.

Assuming a 2-year hold, these are the numbers:

What needs to happen in each scenario?

The bull case requires the AI capex cycle to last through 2028, the second AI/HPC customer to become AEM’s largest by revenue as guided, and AEM to win share in adjacent areas like memory testing.

The bar is high — but not impossible with strong execution.

The base case has the new anchor customer (rumoured to be AMD) ramping as guided through FY26–27, then growth normalising. Revenue lands at ~SGD 720m with a 13% margin and EPS of ~SGD 0.28. The P/E multiple compresses to 25x as the law of large numbers kicks in and AI capex enters a digestion phase.

Realistic — but much depends on whether the AI cycle will continue.

The bear case has the AI capex cycle ending early, with AMD, Intel, or NVIDIA cutting orders. The market realises this time is not different and that semiconductors remain a cyclical industry at heart. AEM gives back most of its AI gains.

Not impossible too.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Is AI in a bubble? Or is this time different?

If you ask me – it all comes down to one question.

Is AI a structural change to the semiconductor industry?

Does AI mean demand for semiconductors is structurally higher, for years to come?

Or is this a cyclical boom — where companies pile into capex for a while, then come to realise they have built too much capacity, start cancelling orders, and send the entire semiconductor complex into a Dot Com–style crash?

That is the central question for anyone investing in semiconductors today.

For what it’s worth, I don’t have a confident answer to this one.

I am a heavy user of AI myself, and I have little doubt this technology — like the internet before it — will reshape the world.

But when I see companies rushing to build AI compute at all costs and assuming demand will catch up, I cannot help but recall the frenzy around networking stocks like Cisco in 1999.

The technology can and will change the world.

But if too much capacity gets built in too short a window, and demand fails to materialise on schedule, you can still get a meaningful bust.

And the parabolic move in semiconductor charts over the past 2 months — where stocks like AEM Holdings have gone up 300% in that window — makes me very nervous.

AEM Holdings is up 370% in 2026 – Will I buy this Singapore semiconductor stock?

Full disclosure — I hold a basket of semiconductor and AI-related stocks, but AEM Holdings is not one of them today.

I trimmed some of my AI exposure recently, and in hindsight I regret it given the parabolic move that followed.

Yes I am still up on my semiconductor basket (I took profit and bought less overvalued AI stocks), but my profit would have been a lot higher had I continued holding some of my original positions.

The takeaway for me is that when there is a structural move underway like AI, the stocks can grind higher for far longer than seems reasonable.

Looking back, I’ve been selling AI stocks for the past few years, and the sector has continued to grind higher.

So it is genuinely difficult to look at current price action and say with conviction that this is the top.

That said — after a 370% move in this stock in 4 months, I find it hard to justify buying a position at these levels.

The uptrend is strong, and the stock could well go to $10 next week.

But with a move this parabolic, and with the broader semiconductor complex looking stretched, even if I wanted to build a position I would let things play out for a week or two first to see how the stock handles its first real pullback.

That being said, I would be looking to add AI and semiconductor exposure on any weakness, and you can see my full portfolio and stock watch shared on FH Premium.

So that’s how I’m thinking about AEM Holdings today. Love to hear what you think!

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

Hi FH,

https://sgwealthbuilder.com/2026/03/29/aem-share-price-in-massive-comeback/

On 30 April 2026, MAS proposed new framework for the proposed Global Listing Board (GLB) that will facilitate dual listing in Nasdaq and SGX, paving the way for GLB to go live in mid 2026. Being a deep tech, AEM is a prime candidate for GLB. After all, Nasdaq is an exchange saturated with tech like homegrown Grab. The heavy buying from institutional buyers also sent AEM share price to the Moon, causing it’s market cap to cross $2 billion, the threshold to qualify for GLB.

Previously, I have written that 2026 would be a “make or break” year for AEM share price. It turns out that my prediction was quite accurate given the recent supersonic form of the counter. With the emergence of JP Morgan and ASE as new shareholders, things are getting pretty interesting.

Back in 2022-2023, investment bank Morgan Stanley and institutional players like Aberdeen and Malaysia EPF were still substantial shareholders of AEM. That was the period when rumours were rift of AEM being on its way to being listed in Nasdaq due to the presence of investment bank Morgan Stanley.

However, Chairman Loke Wai San wasn’t supportive of the idea as he felt that the time was not right given that the market cap of AEM was less than US$1 billion. Subsequently, Morgan Stanley, Templeton and EPF all sold off their stakes in AEM and ceased to be the substantial shareholders after Intel fell into troubles. Now with JP Morgan and Temasek Holdings as backers, will AEM become one of the first few homegrown companies to be dual-listed in Nasdaq and SGX?

https://sgwealthbuilder.com/2026/03/29/aem-share-price-in-massive-comeback/

You are speculating based on what if on a stock that has a current PE of 177. 177 years to get your ROI. It’s a huge gamble should Nasdaq listing mot materialised

Hi Fred,

Yeah, it’s called taking calculated risk. I didn’t all in obviously. Just used a small portion of my wealth to speculate in AEM. Even if AEM share price crashed to $0, I would not be bankrupted. I don’t leverage. So I do apply risk management.

Interesting – what price did you pick up AEM at. I saw the parabolic move at $3 and thought about trading it but didn’t buy in the end. Big mistake.

Sorry I just read your article – thanks for sharing! You held from 5.22 to <2 and back to $8? Boy... respect...