My previous article on StashAway produced a lot of great feedback and debate from readers. Big shoutout to all readers of Financial Horse, great to know that readers are sophisticated investors who would never take a simple 6.9% projected CAGR at face value.

There was a fair bit of feedback to do a follow up piece on Autowealth, given that they have a slightly different asset allocation strategy and lower fees. It’s been something that I really wanted to do as well, since I felt the previous piece was incomplete, and failed to address a few key questions:

1. Are the problems limited to StashAway? Is Autowealth a better alternative?

2. Can we create a complete DIY portfolio for the robo-adviser crowd? Can we achieve similar performance to a robo-adviser without the fees?

3. What is the future of Robo-advisers?

Note: I originally wrote this article using information from the StashAway website, and the StashAway team has since brought to my attention that certain information on their website has not been kept up to date. For my updated take on StashAway, please go here.

Introduction

AutoWealth, like StashAway, is a robo-adviser. Users fill in a set of questions, which is used to generate an ideal portfolio for the user. This is then rebalanced on a regular basis.

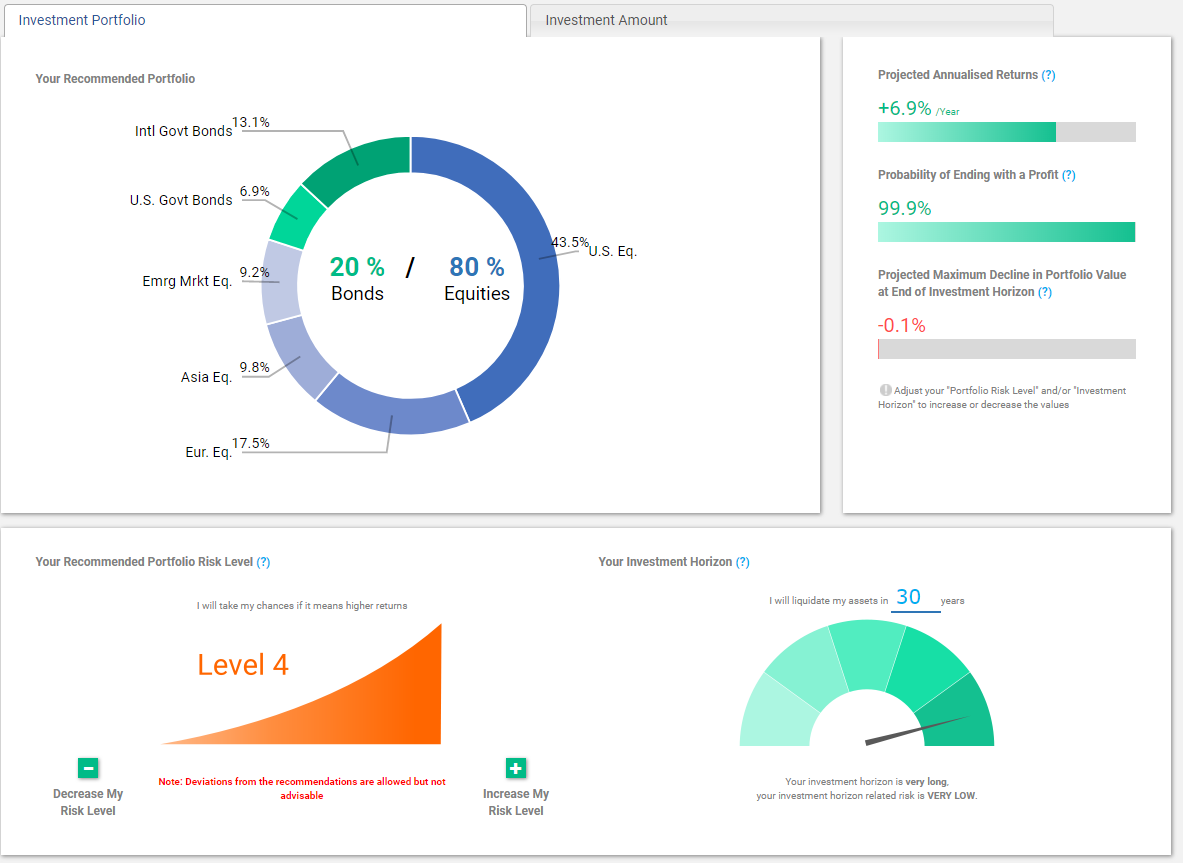

Based on my sample profile (30 years old, S$120,000 income, able to invest 2,000 monthly) AutoWealth generated the following allocation:

| Detailed Portfolio Breakdown |

| 1 | US Equities (VTI) | 43.5% |

| 2 | Europe Equities (VGK) | 17.5% |

| 3 | Asia Equities (VPL) | 9.8% |

| 4 | Emerging Market Equities (VWO) | 9.2% |

| 5 | US Govt Bonds (IEF) | 6.9% |

| 6 | International Govt Bonds (IGOV) | 13.1% |

Source: AutoWealth

What I like about AutoWealth

No “re-optimisation”

What I disliked about StashAway was their opaque “re-optimisation regime”. I do not like the concept where I place money into a robo-adviser, and the robo-adviser performs tactical asset reallocation for me. This looks a lot like market timing and psuedo-active management to me, which I do not want from a passive investment product.

AutoWealth does not perform re-optimisation. Based on an initial asset allocation (eg. 60-40 equities bonds), they will not adjust the initial allocation unless you choose to voluntarily adjust it. The only adjustment they perform is portfolio rebalancing (eg. if equities outperform and you now have 65-35 equities bonds, they will sell equities and buy bonds to rebalance to a 60-40).

This is great because it’s a purer form of investing, and takes you closer to a true buy and hold investor. Clear winner for Autowealth here.

Better control over allocation

I really like the user interface of AutoWealth. I felt it was very direct, and it was very clear how my answers to their questions resulted in my final asset allocation. With StashAway, I had to answer a great deal of questions, and many times it was not entirely clear how my answers affected the allocation. Under AutoWealth, it was very easy to adjust my risk level (from levels 1 to 4), to change the equity bond allocation (each risk level increases the equity allocation by 20%). The whole process was short, sweet and simple, everything I imagined a Robo to be!

The problem however, is that AutoWealth does not have as diverse an asset allocation as StashAway, which includes commodities and convertible securities. AutoWealth sticks entirely to equities and bonds.

It’s very hard to say which is better in this regard. Commodities and convertible securities can truly diversify your portfolio, but over multi-decade periods, its not entirely clear whether they would contribute to outperformance. There is a reason why the classic 60-40 equity bond portfolio sticks to bonds and equities.

I would say it’s a tie here, but you really need to decide as an investor whether you want an allocation to alternative asset classes such as commodities or convertible securities. Personally I would prefer a simple allocation, and for me I would go with AutoWealth.

Source: StashAway

Insolvency risk

With AutoWealth, it is 100% clear that you are not taking on insolvency risk. This is stated explicitly in the their FAQs, and kudos to them for doing so:

In accordance with the Financial Advisors Act, AutoWealth clients’ monies and portfolio assets are held in a personal and segregated custody account at HSBC through Saxo Capital Markets, our partnering MAS-licensed financial institution that is regulated to provide custody services. This means that monies and portfolio assets legally belong to the client and are fully segregated from AutoWealth or Saxo Capital Market’s own monies and assets. Clients enjoy full protection against the insolvencies of both AutoWealth and Saxo Capital Markets.

On the flip side, the problem with doing a fully segregated custody account is that you cannot have fractional units. What StashAway did was that by lumping all securities into a giant account, it allowed them to award fractional units to investors. For example, they could buy an ETF at USD1000 per unit, and on their ledger they would record investor A as owning USD171.5 of that ETF, while investor B owned the rest. This allowed for far more granular asset allocations, especially at lower investment sums.

It ultimately boils down to which is more important to you. Insolvency risk or fractional shares. Personally for me, I far prefer AutoWealth’s approach. I feel that the marginal benefit of fractional shares is not worth the insolvency risk I am taking on. It’s a gain of at most a few bps, versus the potential risk of loss of your entire capital. Once your investment sums start going up, the advantage of fractional shares really falls away, and insolvency risk becomes the overriding consideration.

What I dislike

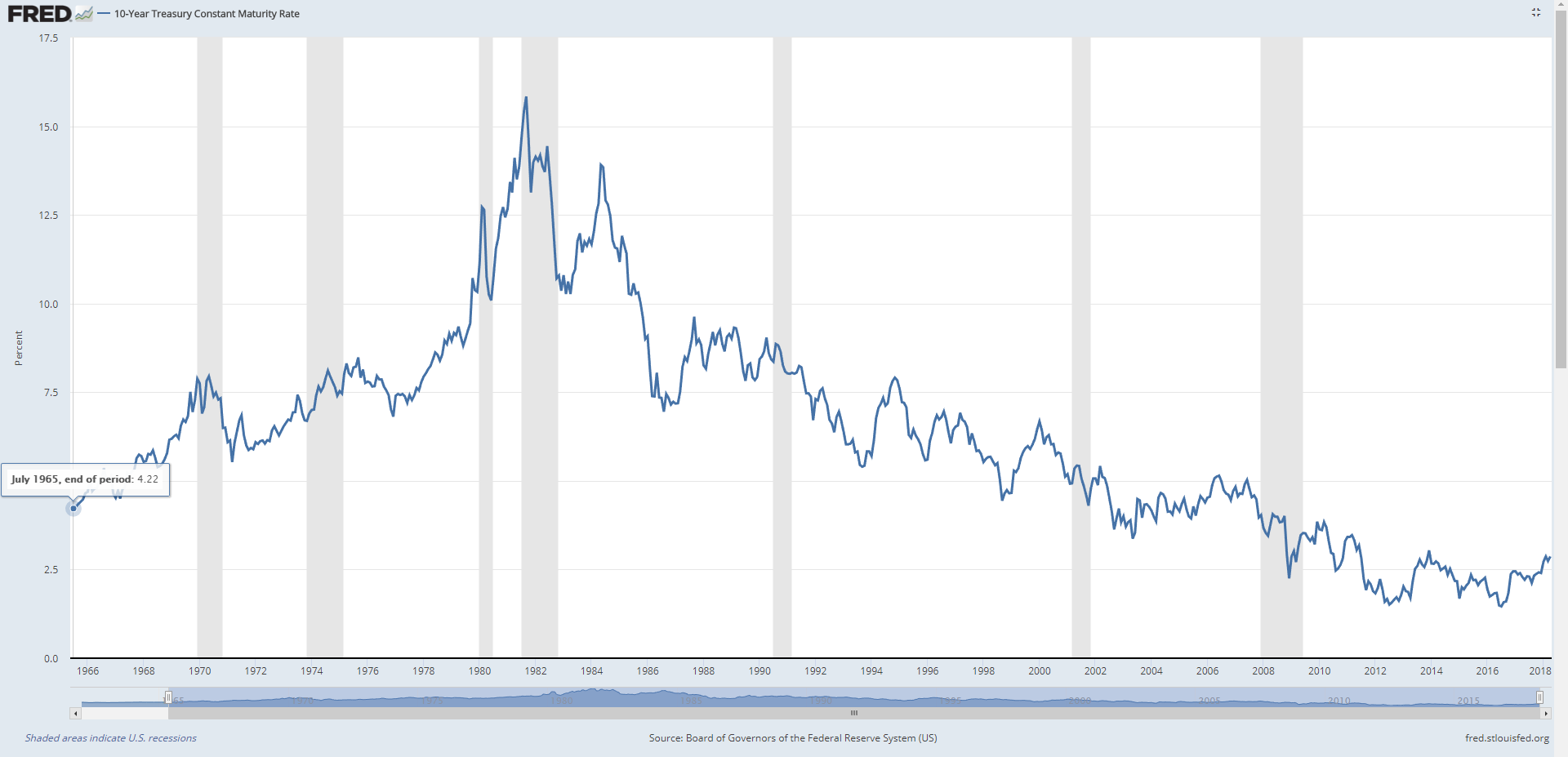

Allocation to bonds

I discussed my dislike for bonds in my previous article. Bond yields have gone from 12% in the 1980s to about 2% today in an unbelievable 30 year bull market.

Source: US FRED

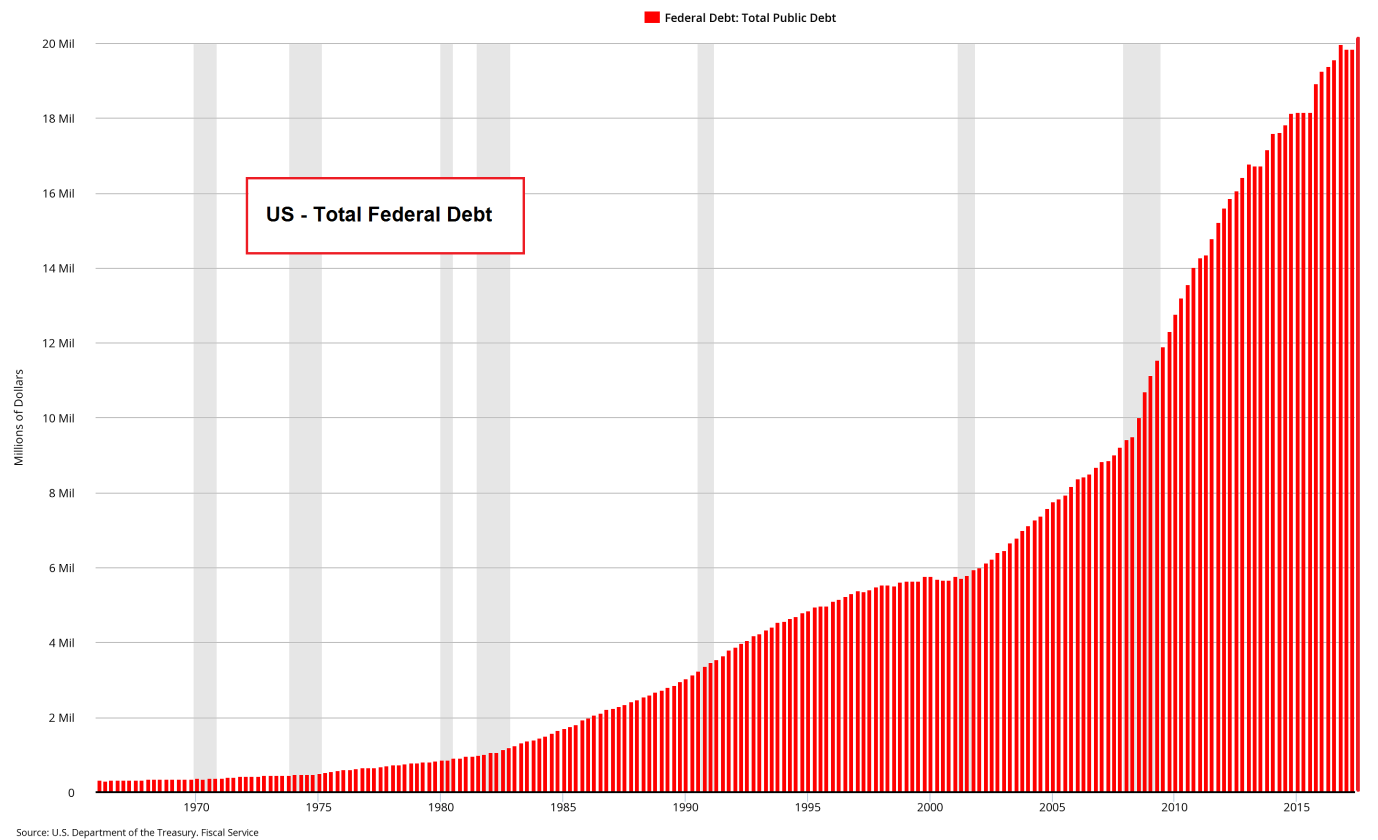

It looks a lot like a lose-lose trade at this point in the economic cycle. In the short term, the Fed is hell bent on raising interest rates, and with inflation rising, bond yields are going to go up (which results in a drop in bond prices). In the longer term, governments around the world have come to rely too heavily on low interest rates for the world to shift to a higher interest rate regime. Just look at the amount of debt the US has accumulated, and think about what happen when interest rates start going up. I suspect that the Fed may try to raise interest rates, but that will eventually trigger a recession and ultimately lower rates.

Source: US DOT

Of course, bonds have a great stabilising effect in a financial crisis when there is a flight to security, when it can really offset the losses in your portfolio. In 2008, when equities were tumbling 40%, bond prices went up 20%, and if you had a 20% to 40% allocation to bonds, it would have really smoothed out your losses.

At the end of the day, for a buy and forget portfolio, you really can’t get away from bonds. What I like about AutoWealth is that they make it very easy to adjust your allocation. By adjusting my risk appetite to level 4, I can easily move to a 20% bond allocation, which is what I would do if I were investing.

So a tie for AutoWealth and StashAway.

No allocation to REITs

Strangely enough, none of these Robo-advisers allocate any amount to REITs. Financial Horse is a great advocate for REITs for the following reasons:

Tax Regime – Singapore has a very favourable tax regime for REITs, allowing full tax transparency for REITs from the point of rental collection until distribution (elaborated on here). This can really boost returns.

Singapore REIT market – The Singapore REIT market is viewed as perhaps one of the best and most vibrant in the whole of Asia. We have a wide selection of REITs with assets that span the globe, and reputable developers such as CapitaLand, Mapletree and Frasers.

Diversification – REITs are ultimately an investment in real estate. By owning a portfolio of real estate and collecting rental yield, you not only diversify your asset allocation, you also enjoy inflation protection as rents go up in tandem with inflation (mostly).

Returns – Owning a broad REIT portfolio would have netted you around 8.0% – 10.0% Compounded Annual Growth Rate (CAGR) over the past 15 years, even after factoring in the financial crisis. These returns are not to be trifled with.

For these reasons, I find it strange that none of these robo-advisers provide a REIT offering. Individual investors will need to manually select and purchase REITs (or an ETF), which is perplexing when the robo is supposed to be a one-stop shop for investing.

It’s a tie here.

Fee

On to my pet topic: Fees. Autowealth has a very simple fee structure, 0.5% of asset size, regardless of how much is invested. StashAway on the other hand, has a tiered structure. The crossover point is approximately S$450,000. This means that for investment sums of less than S$450,000, you pay more fees when using StashAway, but after that, you save on fees when using StashAway.

| Total Investment (SGD) | StashAway | Autowealth |

| First $25,000 | 0.8% | 0.5% |

| Any additional amount above $25,000, up to $50,000 | 0.7% | 0.5% |

| Any additional amount above $50,000, up to $100,000 | 0.6% | 0.5% |

| Any additional amount above $100,000, up to $250,000 | 0.5% | 0.5% |

| Any additional amount above $250,000, up to $500,000 | 0.4% | 0.5% |

| Any additional amount above $500,000, up to $1,000,000 | 0.3% | 0.5% |

| Any additional amount above $1,000,000 | 0.2% | 0.5% |

Personally I feel that 0.5% costs are absurdly high when all they do is buy a bunch of ETFs and rebalance on a regular basis.

You can see for yourself how large the impact of 0.5% fees is:

Assuming a 6.9% CAGR with a S$100,000 starting investment:

| Time | With 0.5% Fees | Without Fees |

| After 30 years | S$678,625 | S$787,798 |

| After 40 years | S$1,284,812 | S$1,567,544 |

| After 50 years | S$2,432,481 | S$3,119,067 |

I understand that there are many economies of scale to be enjoyed with Robo-advisers, so once their Asset Under Management (AUM) goes up, it’s very possible that their fees may drop. That’s a big “if” though. If their AUM doesn’t go up, they could very well decide to increase fees or tweak their business model.

Ultimately, it’s a win for AutoWealth up to S$450,000 investment sums, after which StashAway has lower fees. But the asset allocations for both are quite different, so prospective investors shouldn’t choose between the 2 based solely on fees.

I shall leave you with a quote from John Bogle, the founder of Vanguard Group:

“The miracle of compounding returns has been overwhelmed by the tyranny of compounding costs.” – John C. Bogle

Withholding Tax

Both Robo-Advisers are ultimately subject to withholding tax. Singapore doesn’t have a tax treaty with the US, so there is no way to get around these taxes. There is a trick where some investors buy European listed ETFs because Ireland has a tax treaty with the US, so an Irish domiciled ETF enjoys lower withholding tax on US dividends. The problem with this is that you have to buy on the European markets, which are less liquid than the US ones.

What next?

After all that bashing of robo-advisers, I am going to look like a hypocrite if I don’t suggest an alternative for investors. Financial Horse is many things, but a hypocrite I am not.

In Part II of this Article, I will set out a DIY alternative to Robo-Advisers that requires minimal effort and outperforms them. I will also give my Financial Horse Rating to AutoWealth.

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles!

nice article… have been looking for comparisions with AW and the other robos.

more impressed with your profile though, 120k pa at 30 years of age. wow.

end of the day, i dont think there is a “best” robo out there, per se..

it all boils down to which one you are most comfortable with, and which will enable you to sleep peacefully at night.

Hi FC,

Yes, agreed. Investors should evaluate all options, both robos and DIY investing, and decide what is best for them.

On a side note, all illustrations in this article are an illustration only. Any resemblence with real life, including to that of Financial Horse’s financial situation, are purely a coincidence only. 😉

Cheers.

Excellent analysis.

Glad that you enjoyed the read. 🙂

Am invested in both platforms. The issue with autowealth’s inability to do fractional shares is that at small amounts – dollar cost averaging doesn’t work for small amounts of periodic contributions. As prices fluctuate the quantities of ETF you buy each month do not change.

Thanks for sharing your thoughts. I wrote a follow up article to relook at StashAway vs Autowealth, and i think the asset allocation difference is quite important as well:

https://financialhorse.com/stashaway-responses-from-the-ceo-and-my-thoughts/

Hi FH, I have read quite a bit of your posts and it’s really informative and helpful! But on this topic, I am a bit hesitant because some of your posts are quite pro-StashAway (SA) and some pro-AutoWealth (AW). Understood both might have upgraded versions improving their selling points. I am still rather torn in-between. Do you think it’s silly if I just decide to put $10k each to try out both SA & AW for a short period of say, 5 years and measure the outcome from there? Or do you think it would be better if I just select one (either SA or AW) and pump in $20k in order to generate me higher returns after 5 years?

Absolutely not. If you’ve done your due diligence and are still split between the two, splitting your money in both could be a great option. Unfortunately I havent been keeping up to date with the changes on either of Autowealth and StashAway, so I’m not able to comment meaningfully on the performance/asset allocation of either as they likely would have changed significantly since the time of my article. 🙂

Thank for replying – for some reason. I didn’t get this message until a few years later!

Oh dear, hope it wasn’t too late! 🙂