Unless you’ve been living under a rock this week.

You’ve probably heard that Trump has won the US elections.

This has led to a sharp repricing in interest rates across the curve, namely:

- Short term interest rates have gone up

- Much less interest rate cuts priced in over the next 12 months

This has pretty big implications on where you want to park your cash (and how to invest generally).

3 questions I wanted to discuss today:

- Top Fixed Deposit Rates in Singapore (Nov 2024)

- How has the Trump win impacted interest rates across the curve?

- Where would I put my cash today?

Top Fixed Deposit Rates in Singapore offer 3.20% yield (Nov 2024)

The full table is further below in the article, but I’ve summarised the best interest rates for the 3, 6 and 12 month tenures below.

The 3 and 12 months rates are generally more attractive than the 6 months tenure (for now), which is why I’ve been saying you either want to go ultra short duration or go longer duration, and skip the 6 month duration.

This could well change in a week or two though, given the changes from Trump’s win.

| Tenure | Best fixed deposit interest rate (Nov 2024) | Bank |

| 3 months | 3.00% | Bank of China |

| 6 months | 2.95% | Maybank |

| 12 months | 3.20% | DBS/POSB |

DBS offers the highest Fixed Deposit rate in the market today?!

Funnily enough, the most attractive fixed deposit rate today is 3.20% for 12 months, with DBS / POSB Bank.

Note that apparently if you are above 55, DBS will actually give you a bonus rate of 3.30%.

This is a pretty good deal, and if you haven’t done it already it’s well worth your time.

The catch is that the maximum you can deposit is $19,999.

And you cannot be cheeky and split it up into 2 fixed deposits, because once you hit the $19,999 quota for your account anything beyond that will earn 0.05% (yes I know because I tried it myself).

Best Fixed Deposit Rates yield 3.15% if you deposit with Syfe Cash+ (to access institutional fixed deposit rates)

The rates above are assuming that you deposit with the bank directly as a retail customer.

Another way to do it is to use Syfe Cash+ Guaranteed.

The way this works is that you park the cash with Syfe, who will then deposit the cash into an institutional fixed deposit account.

This allows you access to institutional fixed deposit rates.

These are the latest interest rates from Syfe Cash+ below:

- 1 months – 3.15%

- 3 months – 3.1%

- 6 months – 2.95%

- 12 months – 2.80%

It’s higher than retail fixed deposits at the short end (less than 6 months) and worth looking at if you’re into squeezing out every single bp for your cash.

It’s not SDIC insured though, but given that the underlying is fixed deposits risk should be on the low side (but not risk free).

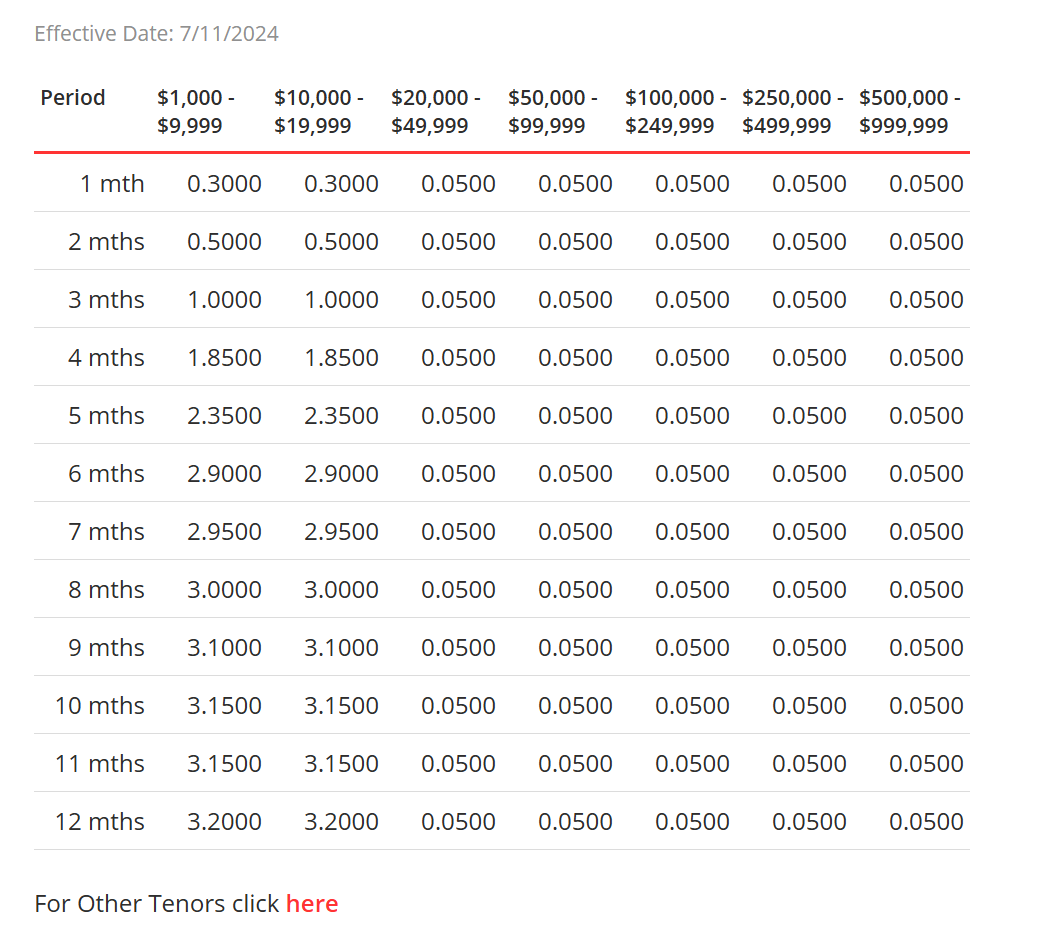

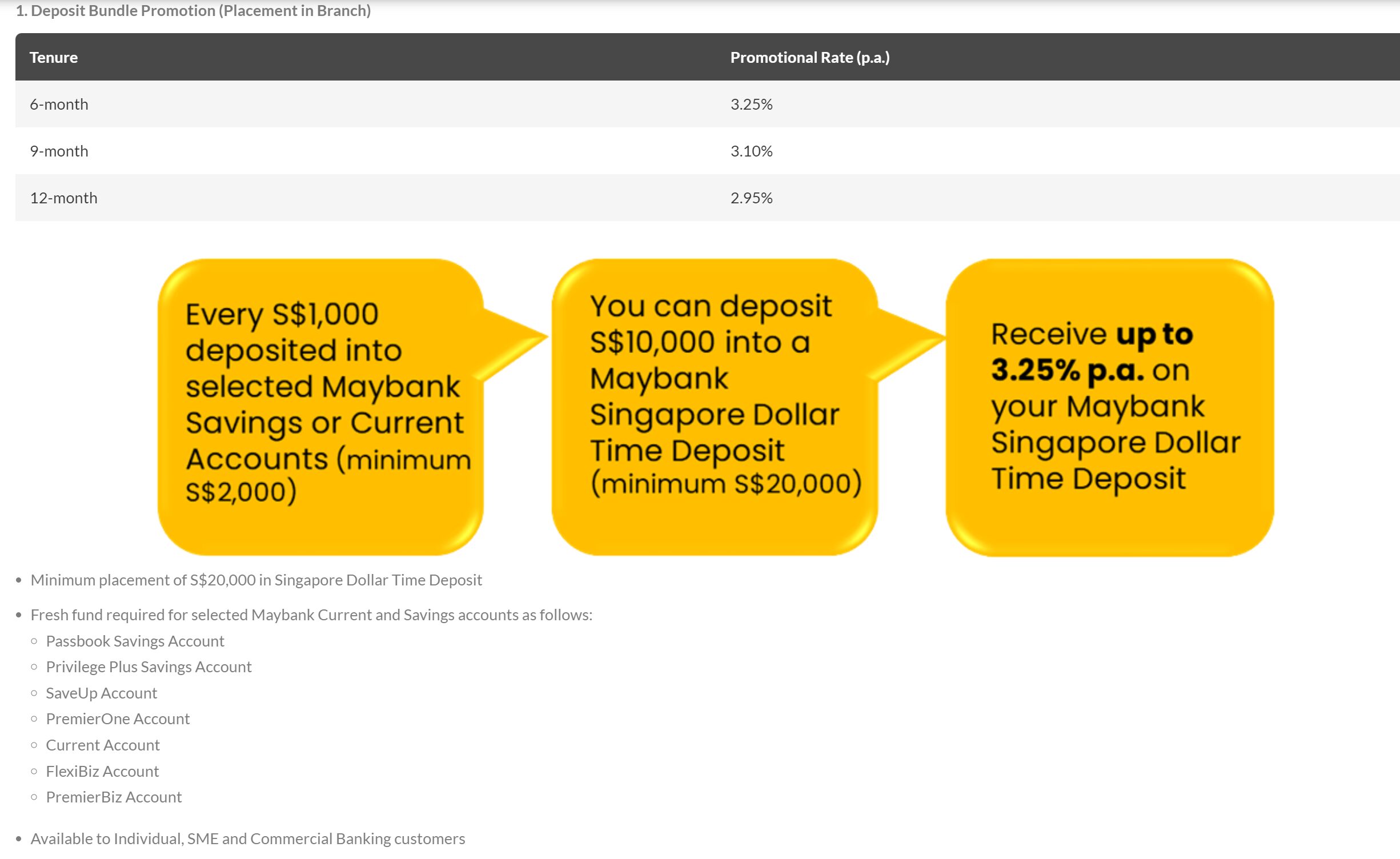

Maybank’s 3.25% headline fixed deposit rate is a promotional rate

Now every time I write one of these articles someone will tell me that Maybank pays 3.25% on their fixed deposit.

Just to clarify, yes 3.25% is the headline rate.

But for every $10,000 you park in fixed deposit, you need to park $1,000 into a Maybank account.

And if the $1,000 earns 0% interest rate, then it brings the effective interest rate down to 2.95%.

So how attractive Maybank is really varies for each investor.

Comparing interest rates for T-Bills vs Fixed Deposits vs Syfe Cash+ Guaranteed across all tenures (Nov 2024)

I’ve tabulated the interest rates for the 3 cash options below.

DBS’s 3.20% for a 12 month fixed deposit continues to look like an outlier, and it looks a bit like they deliberately left it there as a carrot for retail investors.

| 3 months | 6 months | 12 months | Risk Free | |

| T-Bills yields | NA | 2.97% | 2.71% | Yes |

| Fixed Deposit (direct to bank) | 3.00% | 2.95% | 3.20% | Yes (if below $100,000 SDIC limit) |

| Syfe Cash+ Guaranteed (Institutional Fixed Deposit Rates) | 3.10% | 2.95% | 2.80% | No |

| Money Market Funds | ~3.1% | No | ||

Best Fixed Deposit Rates yield 3.20% – if you deposit directly with the bank (as of Nov 2024)

The full list of Fixed Deposit rates is set out below (bold being the most attractive for each tenure).

After the table I’ll share my views on:

- How has the Trump win impacted interest rates across the curve?

- Where would I put my cash today?

| Bank | Interest rate per annum | Tenure | Minimum amount |

| DBS/POSB | 3.20% | 12 months | S$1,000 (max S$19,999) |

| 3.10% | 9 months | S$1,000 (max S$19,999) | |

| Bank of China | 3.00% (mobile placement) | 3 months | S$500 |

| 2.80% (mobile placement) | 6 months | S$500 | |

| 2.70% (mobile placement) | 9 months | S$500 | |

| 2.70% (mobile placement) | 12 months | S$500 | |

| Maybank | 2.95% (mobile placement) | 6 months | S$20,000 |

| SBI | 2.90% | 6 months | S$50,000 |

| 2.50% | 12 months | S$50,000 | |

| RHB | 2.80% (mobile placement) | 3 months | S$20,000 |

| 2.80% (mobile placement) | 6 months | S$20,000 | |

| 2.55% (mobile placement) | 12 months | S$20,000 | |

| Hong Leong Finance | 2.80%(mobile placement) | 6/7 months | S$50,000 |

| 2.65%(mobile placement) | 11 months | S$50,000 | |

| ICBC | 2.80% (mobile placement) | 3 months | S$500 |

| 2.45% (mobile placement) | 6 months | S$500 | |

| CIMB | 2.75% | 3/6 months | S$10,000 |

| 2.55% | 9/12 months | S$10,000 | |

| HSBC | 2.65% | 3 months | S$30,000 |

| 2.55% | 6 months | S$30,000 | |

| UOB | 2.60% | 6 months | S$10,000 (fresh funds) |

| 2.40% | 10 months | S$10,000 (fresh funds) | |

| Standard Chartered | 2.60% | 3 months | S$25,000 |

| OCBC | 2.60% (mobile placement) | 6 months | S$30,000 |

| Citibank | 2.40% | 3/6 months | S$50,000 |

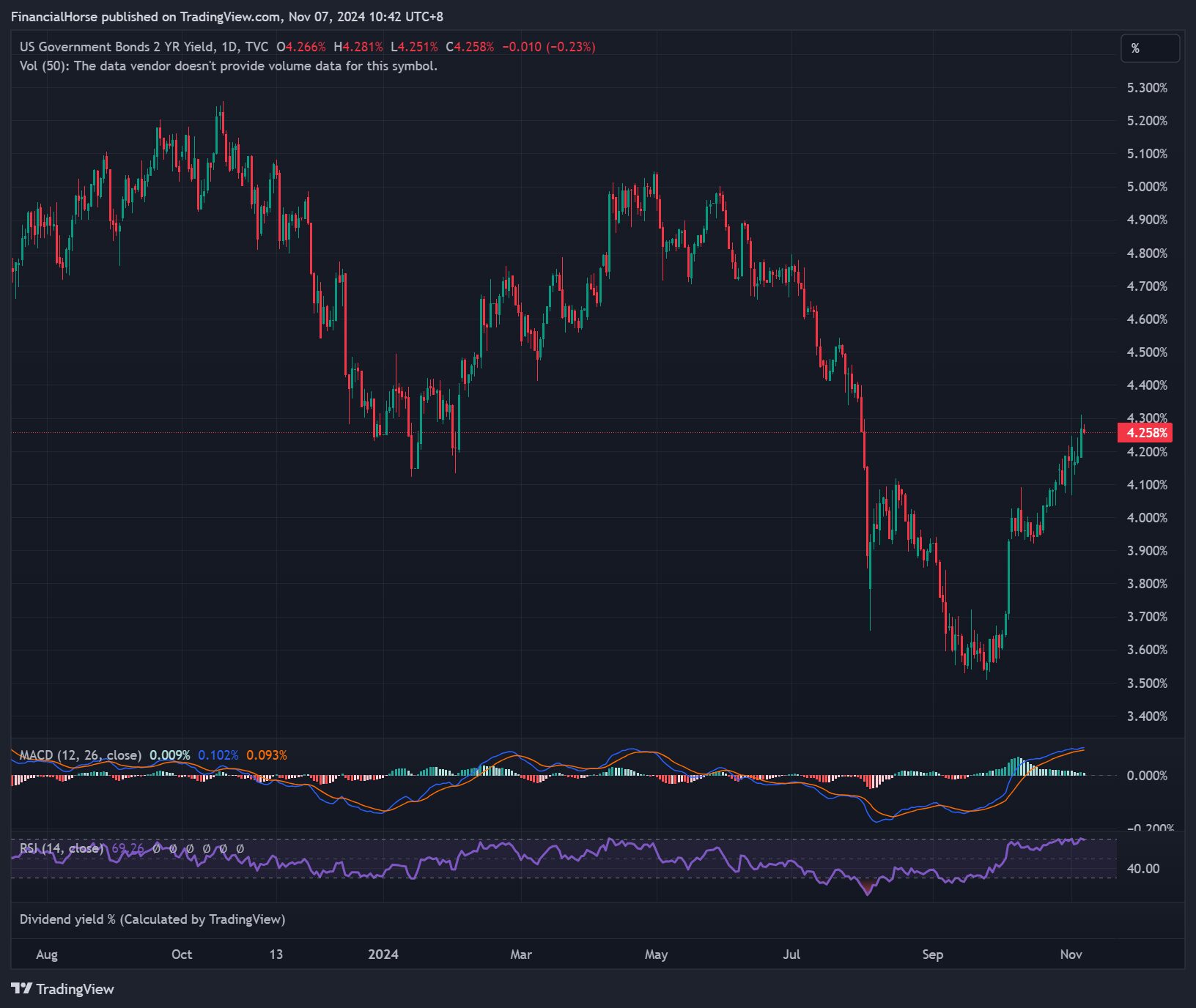

How has the Trump win impacted interest rates across the curve?

Singapore interest rates are not as liquid, so let’s look at US interest rates for a better picture.

Simple answer – is that short term interest rates have shot higher ever since the Fed rate cut.

It’s funny because the Fed rate cut has signalled the short term bottom in interest rates, and if that doesn’t scream policy mistake then I don’t know what does.

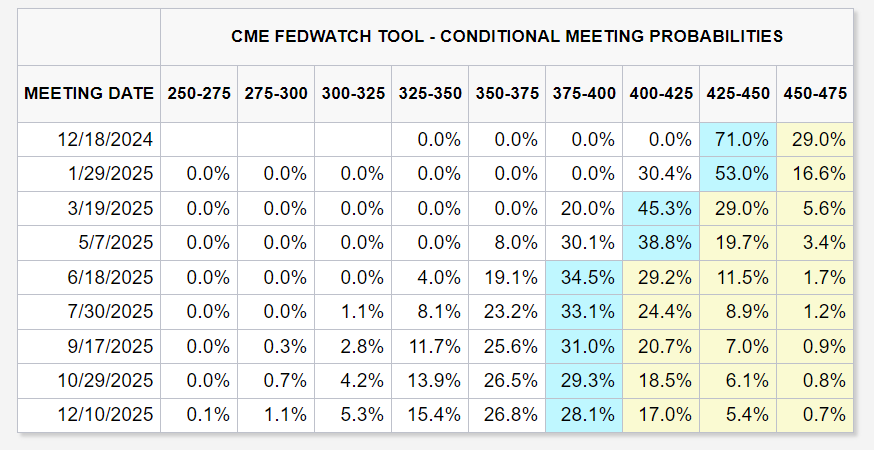

The market has also priced in much less interest rate cuts from the Feds going forward.

The logic of course, is that with Trump having won in a Red Sweep (Republicans also control the Senate now), this gives Trump a lot of power to enact whatever policy he wants.

And we all know what he likes – big fiscal spending, tariffs, America first policies.

All of which are inflationary in nature.

This has the potential to be very inflationary in 2025, and how the Feds are going to react, wow that is a really tough one and I do not envy Jerome Powell’s job.

Follow Financial Horse to avoid missing any post!

Better question – how much cash to hold in this climate, if 2025 will be inflationary?

Perhaps the more appropriate question after this week is how much cash/bonds to hold, if indeed 2025 under Trump will be inflationary?

And really, that’s the million dollar question.

It’s tricky because if you really think about it, the most logical for thing for the US to do here is to cut short term interest rates as much as they can, and let economic growth run hot above inflation.

This allows them to inflate away their debt.

And logically they would want to push lever that as hard as you can – as long as long term interest rates / inflation don’t blow out.

Think back to Liz Truss’s administration, and the line in the sand when UK Bond yields finally blew out and forced them to capitulate.

The Trump administration, and in particular Jerome Powell and whoever the next Treasury secretary will be, needs to tread very carefully to avoid doing the same.

And if indeed this is the case, boy that could be a scenario in which you want to own a lot of inflation hedges / hard assets.

Where would I put my cash today?

But coming back to the topic at hand.

I have no doubt that the events of this week has materially changed the interest rate outlook for 2025.

For now though, the Feds are still projected to cut interest rates the next couple of meetings, so the 6 month part of the curve still doesn’t look very attractive.

For now at least, I still think you either want to park at the ultra short end (1 – 3 months), or you take on slightly more duration (1 year+).

Generally speaking I don’t find the 6 month part of the curve very attractive today, which is why I have primarily been parking my cash in:

- Ultra short term instruments (stuff like UOB One, Money market funds (like MariInvest) or fintech plays (like Chocolate Finance/GXS/FD) on the short end

- And a bit more duration (2 – 3 years) on the long(er) end for higher yield (PIMCO GIS Income Fund for example)

(1) gives me the liquidity at a decent yield, while (2) gives me higher yield (but with the potential drawback of needing to leave the money locked in).

Some potential options below:

UOB One, Money market fund instruments (like MariInvest) or fintech plays (like Chocolate Finance/GXS/FD) on the short end

I’ve maxxed out UOB One Account, which pays 4.0% on the first $150,000.

I also use MariInvest which is a money market fund that pays about 2.9% over the past 30 days for me.

It’s definitely come down because of the rate cuts, but for something that is pretty low risk and with good liquidity (first $10,000 can be withdrawn instantly, rest is T+1 liquidity), it’s still decent.

Alternatively, there’s stuff like Chocolate Finance that even after the drop in rates (on 1 Nov), will pay about 3.6% on the first $20,000.

While GXS is paying 3.28% for 3 months:

There is some investor discretion required here as unlike T-Bills, not all the instruments above (eg. Chocolate Finance / money market funds) are risk free, while DBS/GXS will be risk free as long as you stay within SDIC limits.

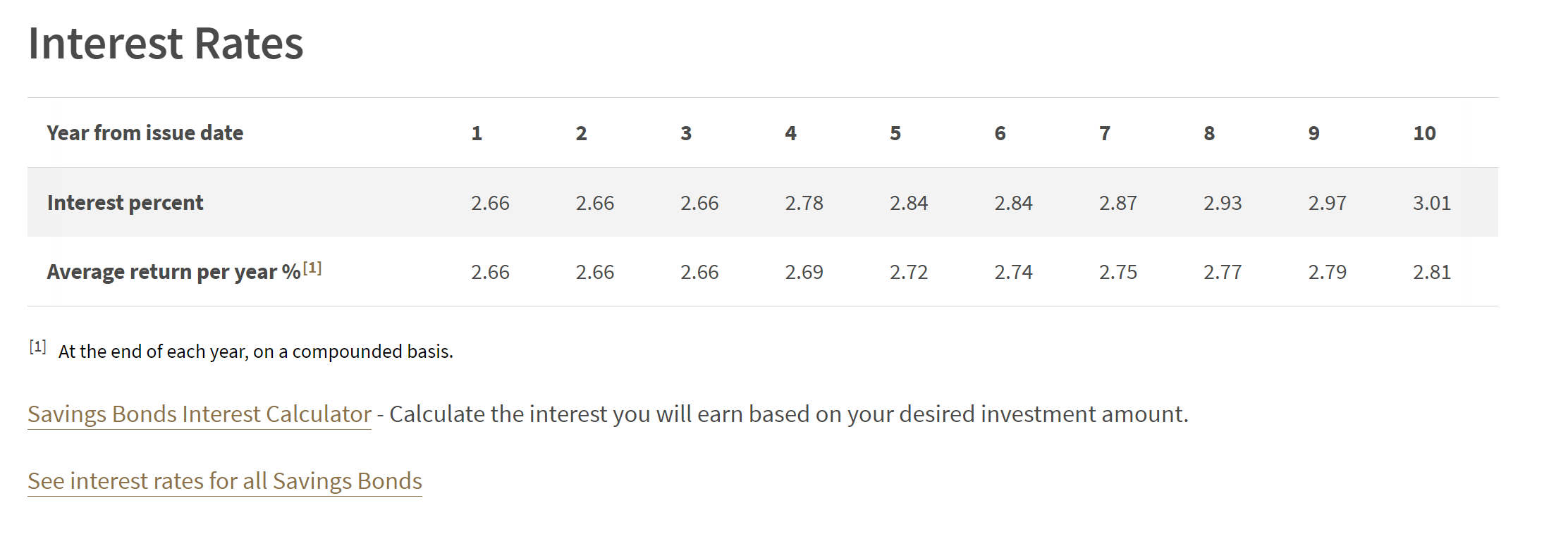

Singapore Savings Bonds

These are the latest interest rates on the Singapore Savings Bonds, but I do not find them particularly attractive.

This may change in the months ahead though.

For more duration – Bond Funds

For more duration, you can consider buying a bond fund.

But bond funds are quite a complex instrument, and not for everyone.

Because if interest rates go up, you can suffer capital losses.

And there is no way to hold to maturity as the bond fund will automatically reinvest proceeds, so the timing at which you sell matters too.

I wrote quite a few articles on this in the past, and do check them out for more information (see here or here).

One reason dbs maintain 3.2% for 12mths (below 20k) could be because a sizable amount of housing loan is tied to that.

Interesting comment. I suppose this is possible. Although usually the local banks are so flush with cash that they have more cash than they know what to do with it.