Mortgage decisions in Singapore are often discussed in shorthand: how much you can borrow, what the monthly instalment looks like, and whether the rate on offer seems lower than the next bank’s.

But housing loans are rarely that simple.

MAS makes clear that loan rules are guardrails, not proof that a purchase is comfortable or risk-free.

Several myths continue to shape how Singaporeans think about home loans.

This article was written by a Financial Horse Contributor.

Myth 1: You need 25% in cash upfront

Not quite.

For a bank loan on a residential property, an individual with no outstanding housing loans can borrow up to 75% of the property value, with a minimum cash downpayment of 5% at that LTV tier. The remainder of the downpayment may be met using CPF savings and or more cash.

That does not mean buying is easy. It means the cash hurdle is often misunderstood.

Buyers should consider both upfront and ongoing payments when deciding what they can afford.

In practice, that means looking beyond the headline downpayment to stamp duty, legal fees, renovation costs and a buffer for emergencies.

A 2024 CNA report illustrated the gap between theory and reality.

One 28-year-old buyer who purchased a one-bedroom condominium for about S$1.4 million paid half of an estimated S$350,000 downpayment, while her parents covered the other half.

This buyer was able to do so only with family support.

She was also repaying them monthly and hoped rental income would help offset the home loan.

The example underscores a broader truth about Singapore’s housing market: even where loan rules and minimum cash requirements make a purchase look feasible on paper, the real hurdle for many younger buyers is still access to family wealth, strong savings, or both.

The minimum requirement, in other words, is not the same as a comfortable entry point.

Myth 2: If the bank approves the loan, the home is affordable

Approval is a ceiling, not a safety stamp.

Monthly instalments for HDB flats and certain executive condominiums are subject to the Mortgage Servicing Ratio, while overall debt obligations are subject to the Total Debt Servicing Ratio. The TDSR threshold is 55% of gross monthly income, while MSR is 30% for the relevant HDB and EC purchases.

Those rules are designed to limit excessive borrowing.

They do not mean a household will feel comfortable carrying the loan through different stages of life.

Banks told CNA in 2024 that younger borrowers were increasingly entering the market, but also warned against stretching too far. OCBC’s head of home loans, Maryanne Phua, said a home loan is “a long-term financial commitment”.

That caution matters because affordability changes over time.

Renovation loans, children, ageing parents, a weaker job market or a jump in rates can all turn a manageable mortgage into a stressful one.

Myth 3: The lowest advertised rate is always the best package

A low teaser rate can hide expensive terms elsewhere.

Before a borrower signs a bank home loan, the bank must provide a property loan fact sheet. This factsheet highlights how interest-rate increases may affect monthly instalments and sets out key features such as the lock-in period, repayment schedule, effective interest rate and penalty fees.

That means the real comparison is not just rate versus rate.

Borrowers also need to weigh clawbacks, conversion fees, early repayment penalties, bundled products and what happens after the promotional period ends.

Borrowers should compare updated repayment schedules, advertised rates, effective interest rates and the fine print before switching packages.

Late last year, CNA reported on borrower Denise Chan, who repriced her DBS mortgage from 3% to a two-year fixed package at 1.6%, reducing her monthly instalment by about S$500.

The case shows why many home owners review their loans once the rate environment turns in their favour: even a seemingly small change in percentage terms can translate into meaningful monthly savings on a large outstanding mortgage.

But the headline saving is only part of the picture. The same report noted that borrowers weighing a refinance or reprice should also account for the associated frictions, including legal and valuation fees in the case of refinancing, or administrative charges for repricing.

In practice, that means the right question is not simply whether a new package offers a lower rate, but whether the total savings after costs, lock-in terms and future reset risks still make the switch worthwhile.

Myth 4: Fixed-rate loans are always better than floating-rate loans

Neither is always superior. The better choice depends on what kind of risk a borrower is willing to live with.

Homeloans can be fixed or floating, and that possible increases in interest rates should be understood before a borrower commits.

Borrowers should review their loans regularly, particularly after a lock-in period ends.

A fixed rate gives short-term certainty. A floating package may become cheaper when rates ease, but it also passes more rate risk back to the borrower.

That trade-off became more visible as bank mortgage rates fell. CNA reported in December 2025 that bank mortgage rates had moved below the 2.6% HDB concessionary rate, prompting more borrowers to review their options.

The point is not that one structure is always right. It is that borrowers should choose based on cash-flow resilience, not on the assumption that fixed automatically means safer or cheaper over the life of the loan.

Myth 5: Using CPF makes the mortgage cheap or almost free

CPF can ease monthly cash flow, but it still carries a cost.

CPF Board says that when a property is sold or transferred, sale proceeds are used to pay off the outstanding housing loan and refund the CPF amount used for the property. The refund amount generally includes the CPF principal withdrawn and accrued interest.

That means CPF used for housing is not simply erased. It is money that would otherwise have remained in the member’s CPF accounts earning interest.

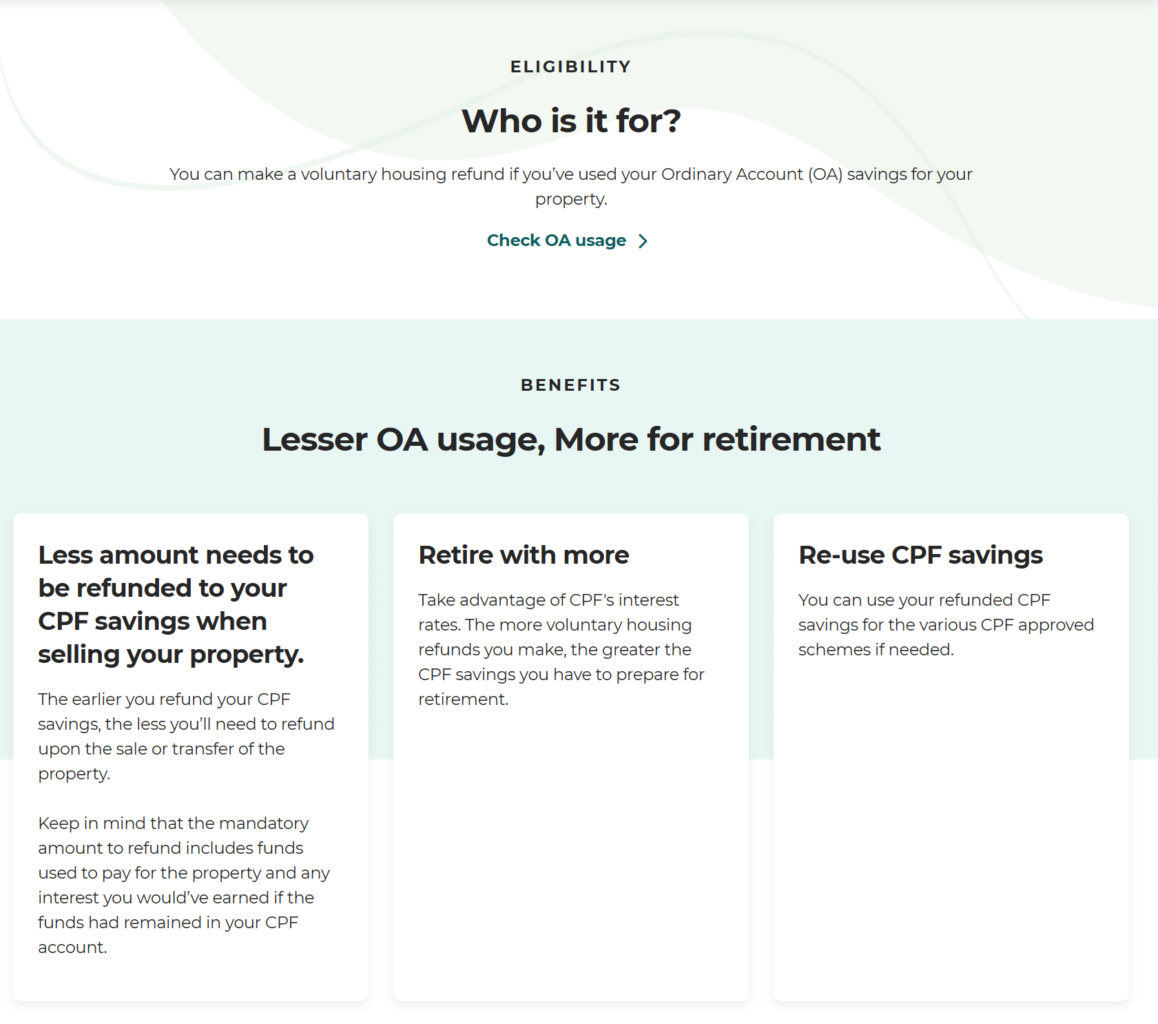

CPF Board also says members who have used Ordinary Account savings for property can make voluntary housing refunds. It notes that the earlier such refunds are made, the less will need to be refunded upon sale or transfer later, and that doing so can leave more cash proceeds after a sale.

The practical takeaway is simple: CPF can make a home feel easier to carry today, while reducing future retirement compounding and future sale flexibility.

Myth 6: Once you choose a mortgage, you are stuck — or you can always switch back later

This is only partly true.

Borrowers are not necessarily locked into one package for the full life of the loan. Refinancing means switching to a new lender, while repricing means moving to a different package with the existing bank. It also says borrowers should review their home loans regularly to see if savings are possible, especially after the lock-in period.

But the second half of the myth is more dangerous.

HDB flat buyers are not allowed to refinance an existing bank loan with an HDB loan. In other words, moving from an HDB loan to a bank loan can be a one-way decision.

That matters more when bank rates fall below HDB loan rates. HDB said the concessionary interest rate for April to June 2026 remained at 2.6%, and CNA reported that some owners were switching to bank packages to reduce interest costs.

But the same CNA report also cited a mortgage adviser warning that borrowers should do so only if they understood they could not return to an HDB loan and were “prepared for volatility”.

More than a rate decision

The deeper misconception may be that mortgages are mainly about qualifying for the biggest possible loan or securing the cheapest available package.

Affordability, in other words, is not just about qualifying for a loan or surviving the first few years of instalments. It is about whether a household has enough financial buffer to absorb shocks, whether its overall debt load leaves room for the rest of life, and whether the mortgage would still feel sustainable if interest rates move higher in future.

CPF Board makes clear that housing payments made with CPF still affect retirement balances and future sale proceeds. MAS rules place limits on borrowing, but those limits do not remove the need for prudence.

For many buyers, the better question is not how much the bank will lend.

It is whether the mortgage still works if rates rise, expenses increase, or one income weakens for a period of time.

That is usually where the myths end and the real cost of borrowing begins.