Imagine a Singapore investor who dies holding S$1.5 million of US stocks in a brokerage account.

Their family expects to inherit S$1.5 million.

The IRS can take more than S$500,000 of it first.

Singapore abolished estate duty in 2008, so most of us assume death is tax-free.

On the Singapore side, it is.

The trap is on the US side — and it lands squarely on the assets most of us hold the most of, US stocks and US-listed ETFs.

Here’s what I want to discuss today:

- How does US estate tax actually work for a Singaporean, and what would it really cost?

- Does holding through IBKR, Tiger or moomoo protect me?

- What are the fixes, ranked by how practical they actually are?

- And what do you do if you pick single stocks like Nvidia, where there’s no easy wrapper?

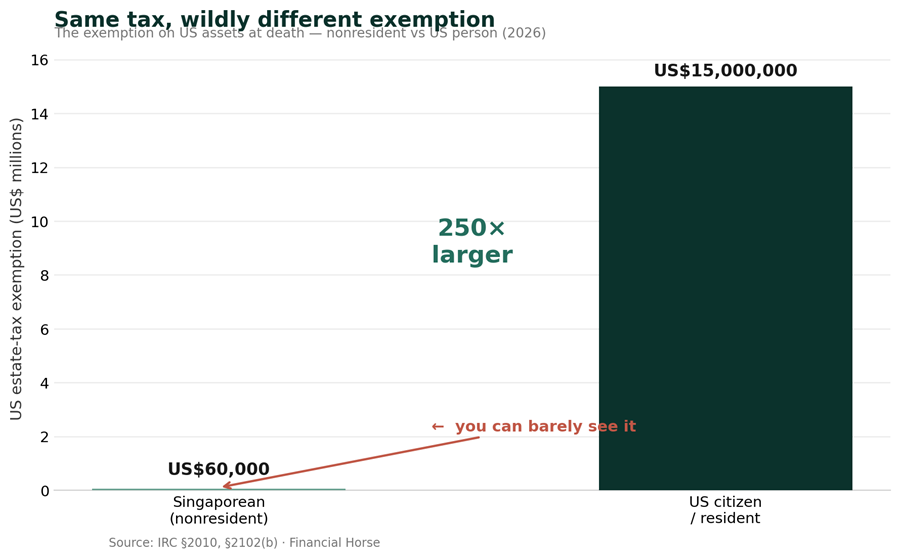

Start with the exemption — and how small it is

A US citizen can die with US$15 million in assets before the estate tax bites.

A Singaporean gets US$60,000.

In plain English, the US hands its own citizens an exemption 250 times larger than the one it gives you.

You can see just how lopsided that is below.

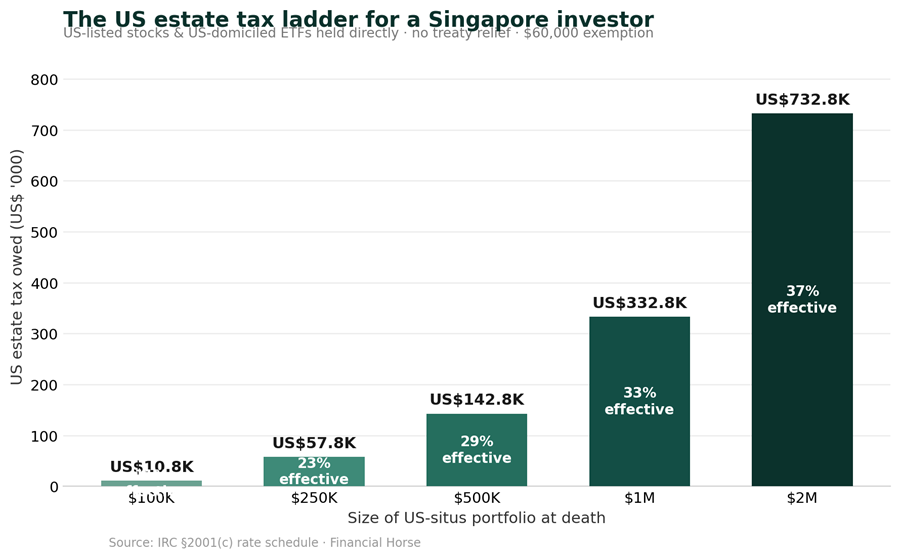

Above that US$60,000, the tax is graduated from 18% up to 40%, and the top 40% rate hits everything above US$1 million of taxable assets.

The 40% headline gets quoted a lot, but the effective rate is what actually comes out of the estate, and it climbs with the portfolio.

Run the numbers on a US$1 million US stock portfolio and the estate tax works out to about US$332,800 — an effective rate of 33%.

You can see how the effective rate scales as the portfolio grows below.

Table 1 — US estate tax by portfolio size (Singapore investor, no treaty)

| US-situs assets at death | Estate tax owed | Effective rate |

| US$100,000 | US$10,800 | 10.8% |

| US$250,000 | US$57,800 | 23.1% |

| US$500,000 | US$142,800 | 28.6% |

| US$1,000,000 | US$332,800 | 33.3% |

| US$2,000,000 | US$732,800 | 36.6% |

Assumes the whole estate is US-situs and no treaty applies. The $60,000 exemption is delivered as a $13,000 credit against the graduated tax (IRC §2001(c) schedule).

If you take one thing away from this article, it should be this:

Die holding $2 million in US stocks, and you’re paying $732,000 in taxes to the US government, that your descendants won’t get a cent of.

The one thing that fixes this is a tax treaty — and this is where Singapore loses.

The US has estate tax treaties with around 15 countries, and residents of those countries can claim a share of the full US exemption.

A UK resident, for instance, gets the same multi-million-dollar exemption a US citizen would.

Singapore has no such treaty, so there is no relief — you get the US$60,000 and nothing else.

Does using IBKR, Tiger or moomoo protect you? No.

This is the most common misconception I hear.

The logic goes: my broker is in Singapore, so my shares are Singapore assets.

That is wrong.

US estate tax follows the underlying asset, not the custodian.

Apple shares are US-situs whether you hold them through IBKR, Tiger, moomoo, Saxo or a US account — situs is set by where the company is incorporated, not where your brokerage sits.

So the platform makes no difference to your exposure.

And the same logic applies to US shares bought through your SRS account — the wrapper is Singaporean, the asset is not.

What matters is what you hold.

Table 2 — What’s exposed, and what isn’t

| Counts as US-situs (exposed) | Not US-situs (safe) |

| US-listed stocks (Apple, Nvidia, Tesla…) | Irish / other non-US-domiciled ETFs (e.g. CSPX) |

| US-domiciled ETFs (VOO, SPY, QQQ) | Cash in a US bank deposit account |

| Cash sitting in a US brokerage account | Most directly-held US Treasuries (portfolio-interest debt) |

| US retirement accounts (IRA / 401(k)) | Non-US and SGX-listed shares |

| US real estate | Non-US real estate |

The part that turns this from theory into a real problem is enforcement.

When a US custodian is notified that the account holder has died, it freezes the account.

Before releasing anything to your heirs, it requires an IRS transfer certificate (Form 5173) — which the IRS only issues once the estate’s tax position is settled.

The custodian is personally on the hook to the IRS if it releases assets early, so it will not do your family any favours.

That process routinely takes 6 to 18 months.

Whether the IRS actively chases small estates is genuinely debated — but the liability is real, and it’s your executor and your family who carry it while the account sits frozen.

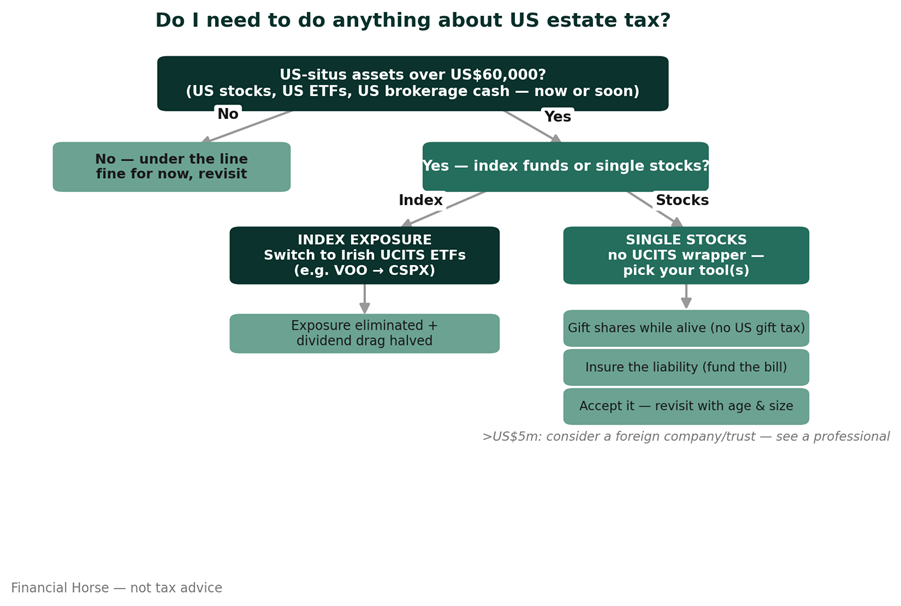

How can Singapore Investors “solve” this?

Now to be absolutely clear – none of this should be taken as financial / tax advice.

But let’s explore some potential ways around the problem.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

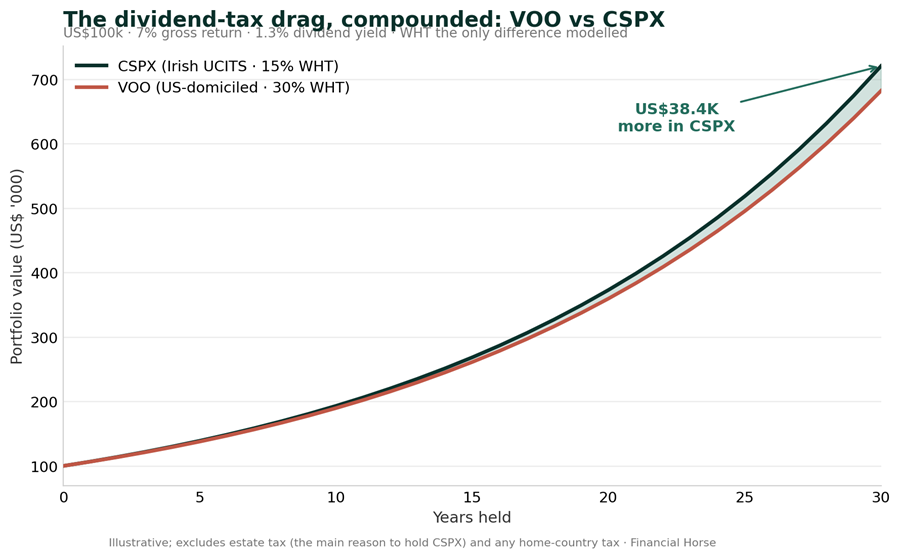

1. For index exposure — just use Irish-domiciled UCITS ETFs

This is the cleanest fix, and for most people it solves the problem outright.

An Ireland-domiciled ETF is not a US-situs asset, so it sits completely outside US estate tax — at any portfolio size.

If you hold VOO for S&P 500 exposure, the direct swap is CSPX, the iShares Core S&P 500 UCITS ETF, domiciled in Ireland and listed in London.

There’s a second win here.

Because of the US-Ireland tax treaty, dividend withholding inside an Irish fund is 15%, not the 30% a Singaporean pays inside a US-domiciled ETF.

So moving from VOO to CSPX takes your estate tax exposure to zero and halves your dividend tax drag.

Table 3 — VOO vs CSPX

| VOO (US-domiciled) | CSPX (Irish UCITS) | |

| Domicile | United States | Ireland |

| US estate tax exposure | Full (US-situs) | None |

| Dividend withholding | 30% | 15% |

| Total expense ratio | 0.03% | 0.07% |

| Listing | NYSE Arca (US) | London SE |

| Dividends | Distributing | Accumulating |

And that drag compounds.

On US$100k over 30 years, the 15-point difference alone works out to about US$38,000 — and it scales with the size of your portfolio.

You can see the gap widen below.

For anyone whose US exposure is mostly index funds, this is a no brainer.

The trade-off is slightly higher fees, and slightly poorly liquidity.

But for 90% of Singapore investors, I would say it’s worth the trade-off.

2. The underused one — gift the shares while you’re alive

Note that a Singaporean’s gift of US shares is not subject to US gift tax — at all.

US stocks count as intangible property, and a nonresident’s gift of US intangibles falls outside the US gift tax entirely — there isn’t even an annual cap the way there is for tangible US property.

So the same shares that would be taxed at up to 40% if you die holding them can be transferred to your children during your lifetime, tax-free.

That’s a genuine planning tool, especially for older investors sitting on large, appreciated US positions.

The catch is that the gift is irrevocable — you give up control, and the exposure doesn’t disappear, it transfers.

Your children now hold the same US-situs assets with the same US$60,000 exemption — just with, hopefully, several more decades before it matters.

And don’t try to be cute and do a trust structure where your children legally own the shares and you hold beneficial interest – that could immediately trigger the entire tax bill.

It has to be a genuine gift, that you give it away entirely before death.

3. Stay under US$60,000 — fine when you’re starting out

If your US-situs assets never cross US$60,000, there’s no tax and no filing.

That works if your portfolio size is small, but it doesn’t work for a serious portfolio — so treat it as a phase, not a plan.

4. Life insurance — to fund the bill, not dodge it

Death benefit payouts are generally outside the US estate.

This doesn’t remove the liability — it gives your estate the cash to pay it without a forced sale of your holdings.

Useful once the exposure is large and you’d rather not restructure everything.

But doesn’t truly solve the problem.

5. Foreign companies and trusts — the >US$5 million tools

Holding US assets through a foreign company or trust can move them out of your US estate.

These work, but they’re costly and complex, and not a DIY job — if you’re at that size, see a cross-border adviser, and get a proper tax and legal consultant.

One thing that doesn’t work: joint accounts

This is the fix people assume works, and it doesn’t.

For non-spouse joint holders, the IRS presumes the entire account belongs to the first to die unless the survivor can prove their own contributions — so joint tenancy defers paperwork, not tax.

And don’t count on a spousal exemption either — the unlimited marital deduction only applies when the surviving spouse is a US citizen.

Here’s a simple flowchart to summarise the thought process (again not tax advice).

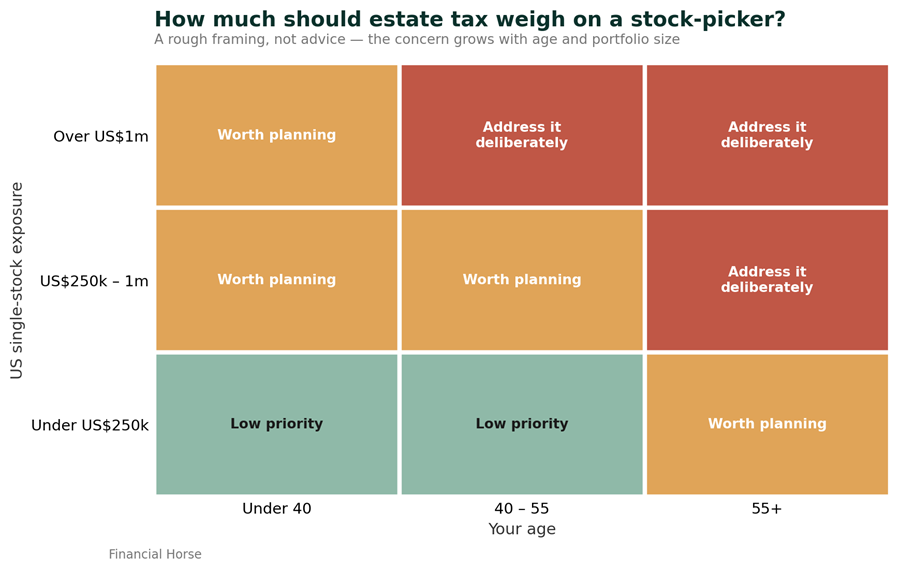

The hard case — what if you pick your own stocks?

Everything above is easy if you only hold index funds.

It gets harder the moment you want to own Nvidia, Google or Berkshire directly — because there is no Irish UCITS wrapper for a single stock.

If you’re a stock picker, the ETF fix is off the table, and you’re left with three tools: gift during your lifetime, insure the liability, or simply accept it.

I’d frame this the way I frame any asymmetric risk.

The tax only bites in one scenario — death — and for a healthy investor in their 30s or 40s, the odds of that in any given year are low (touch wood).

In plain English – the risk of holding US single stocks is small while you’re young, and it rises as you age and as the portfolio compounds.

This is a planning problem that grows with you, and you should think about it the older you gety.

You can see roughly where it starts to matter below.

The trap I’d avoid is letting the tax tail wag the investment dog.

If your edge is picking US single stocks, giving that up to save a tax that may be decades away — and that you can plan around later — is a bad trade.

But the calculus flips as you get older and richer.

Past a certain size and age, the expected cost stops being trivial, and that’s the point to gift down, insure, or restructure deliberately.

So the honest answer is: don’t panic-sell, but don’t ignore it either — revisit it every few years as the umbers move.

Love to hear what you think though!

How are you handling US inheritance tax — or is this the first you’re hearing of it?

This article was written on 3 July 2026. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

Do we need to pay Estate Duty tax for our Australia property investment and stocks holding when we die as a foreigner who is a Singaporean ?

Same question for China Stocks holding ?

Ok this should not be taken as tax advice. But my understanding is that Australia does not have estate tax, but it has capital gains tax. China stocks via A Shares and H Shares do not have inheritance tax, but the US listed China stocks will have the same problem as that set out in this article.

I understand that US listed China stocks which are legally registered as foreign corporations (predominantly Cayman Islands Variable Interest Entities, or VIEs), their shares constitute non-US-situs assets and not subject to the US estate duty tax?

I took a closer look at this, and yes you are right. But best to do a check on a per stock basis, as it really depends on how the legal structure for the VIE is set up.

Term Insurance solves the problem. You basically need to bear the cost of premium. This is much lower than incremental fund charges in Ireland. The US authorities can deduct the 40%, whilst Insurance pays that to the estate.

This works for young investors. But once you get more advanced in age the premiums are too expensive.

I am a citizen of UK but live and work here. how does this affect me?

This goes well into the realm of tax advice, it will depend on your specific situation – for eg. how many days you spend in SG, whether you are SG or UK tax resident etc etc.

From what i have experienced, brokerage accts are not automatically considered part of your estate, aka if undeclared it can remain in limbo forever.

My FIL passed away and for convenience, we sold his shares and transfer the money to his bank acct (and subsequently transfer out) to skip all these issues. Worked though.

This is a loophole in enforcement by the IRS (because they don’t know about it)… it does not necessarily mean it is legal…

Thanks for the article. My questions are:

Will tax apply if the US stocks are held in a singapore incorporated company; and

is discretionary managed portfolios subject to US tax? I am assuming that the investor is dead.

It will depend on the legal holding structure. Not easy to advice without knowing the full details.

If I give in advance the password of my account to my family, will my family be able to avoid paying the tax? Is this doable? I have prepared all the passwords in a file including bank accounts just in case.

Okay I am not a tax advisor. But if you do this intentionally, this goes well into the realm of potential tax evasion.

for an Australian citizen but residing in Singapore as a permanent resident and using platforms like Moomoo, Tiger, IBKR will I be subject to Australia-US tax treaty or Singapore-US tax. Also how to gift shares as they are under street name?

This will depend on your personal circumstances – whether you are Australia/SG tax resident etc.

Sorry what do you mean by under street name. It sounds stupid but the easiest way to gift the shares is usually to sell them, and gift the cash proceeds…

Thanks for the great article. I noticed you mentioned “ When a US custodian is notified that the account holder has died, it freezes the account.”

May I know whether this means if one has an IBKR account with only Irish domiciled ETFs, the account will also be frozen and will require IRS transfer certificate before the family can touch the account?

To my knowledge, if the custodian is not specifically notified, they actually won’t know if someone is deceased. So it goes well into the realm of estate admnistration after death. Like some other commenters have said, if the IRS doesn’t know about it they can’t collect the tax, but then again that would be tax evasion.