Okay so quite a few of you have asked me about UOB this week.

And I get why.

UOB’s share price jumped almost 10% in 1 week, including a 4.7% gain in a single session — without any earnings result.

For a stock I bought in the low S$33s when everyone hated it, this has been a satisfying ride.

But all-time highs force a decision.

Is UOB — still the cheapest of the 3 Singapore banks — finally catching up to DBS and OCBC?

Or is this a momentum move that changes nothing about why UOB trades at a discount in the first place?

In plain English — should I buy more UOB at S$44, or stick with OCBC and DBS?

I want to cover 3 things:

- Why all 3 Singapore banks rallied this week?

- Whether UOB’s valuation discount is justified?

- What I am doing with my UOB position today?

All 3 bank stocks rallied this week

It was not just UOB.

DBS and OCBC also hit all-time highs this week.

Here are the 1-week returns:

- UOB (candles) — 9.8%

- OCBC (orange) — 8.1%

- DBS (red) — 5.2%

Zooming out to year-to-date returns tells a slightly different story:

- OCBC Bank (orange) – 37%

- UOB Bank (candles) – 26%

- DBS Bank (red) – 24%

All 3 banks have comfortably beaten the STI (16.7%), but OCBC remains the clear winner for the year.

My biggest position is OCBC, followed by UOB, and I do not hold DBS today.

So looking at the chart makes me think I did something right.

But the chart is history.

The key question is what happens next — and which of the 3 banks will outperform from here.

Why did the 3 banks rally this week? And why are analysts split on UOB?

The immediate trigger for the rally was a Citi note raising target prices across the Singapore banking sector on a loan-growth recovery thesis.

SORA has fallen roughly 2.7 percentage points from its peak and appears to be bottoming near 1%, while Citi expects a combination of stabilising interest rates and stronger loan growth to drive about 10% sector earnings growth in 2027–2028.

I broadly agree with that view.

With markets no longer expecting aggressive Fed rate cuts, the worst of the interest-rate downcycle for bank margins may be behind us.

This is also why US financial stocks have performed well recently, and why I added to my OCBC position 1 or 2 months ago, as shared with FH Premium readers.

But here is the nuance.

Citi remained neutral on UOB despite being bullish on the banking sector.

The reason is simple — UOB’s wealth and loan-growth trajectories still lag DBS and OCBC, so its lower valuation may be fair rather than an opportunity.

On the flip side, Macquarie looked at the same setup and upgraded UOB, citing further re-rating potential.

So who is right here?

Is UOB actually cheap? Yes — but that’s the wrong question

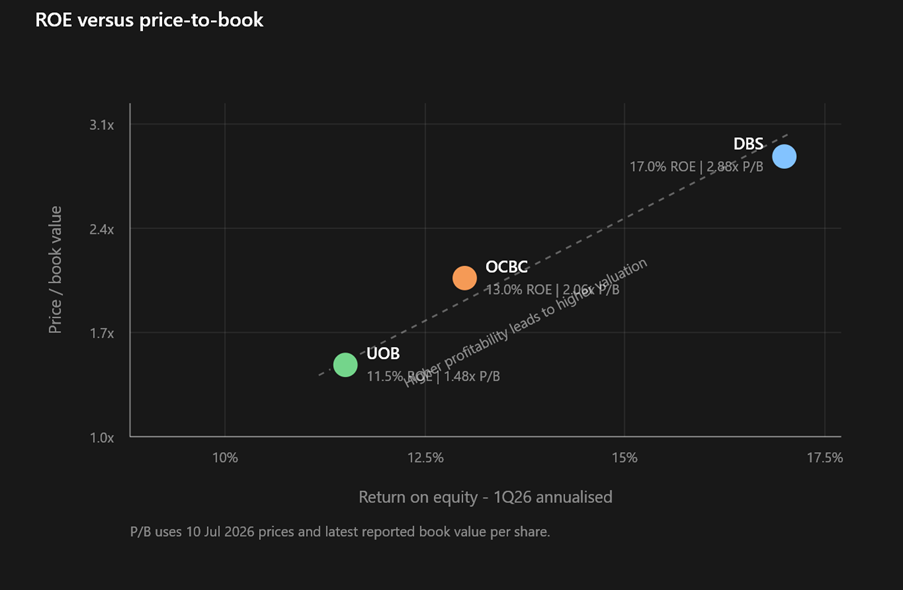

I’ve summarised the valuations of the 3 banks below.

| Metric | DBS | OCBC | UOB |

| Trailing P/B | 2.88x | 2.06x | 1.48x |

| Forward FY26 P/B | 2.79x | 1.75x | 1.36x |

| Approx. NTM P/E | 16.7x | 15.5x | 12.5x |

| ROE, 1Q26 | 17.0% | 13.0% | 11.5% |

| Group NIM, 1Q26 | 1.89% | 1.76% | 1.82% |

| NPL ratio | 1.0% | 0.9% | 1.5% |

| CET1, reported | 16.9% | 17.0% | 15.3% |

| CET1, fully phased-in | 14.8% | 15.2% | Not separately highlighted |

| Forward cash yield | ≈4.6% incl. capital return | ≈3.6% | ≈3.9–4.1% |

You can see that UOB is the cheapest bank whether you use P/B or P/E.

But its ROE is also by far the weakest.

That matters because a bank earning an 11.5% ROE should not trade at the same valuation as one earning 17%.

A lot of readers have pointed this out to me — UOB is simply not as good a bank as DBS or OCBC today, and that this is not going to change, therefore UOB deserves to trade at a discount.

I think that is broadly correct.

But I wanted to discuss more on the “that is not going to change”.

The “right” question – Can UOB close the gap vs DBS and OCBC?

For the discount to close sustainably, UOB’s ROE needs to catch up with DBS and OCBC.

Is that realistic?

And here is the problem — UOB’s own guidance points the other way, at least in the near term.

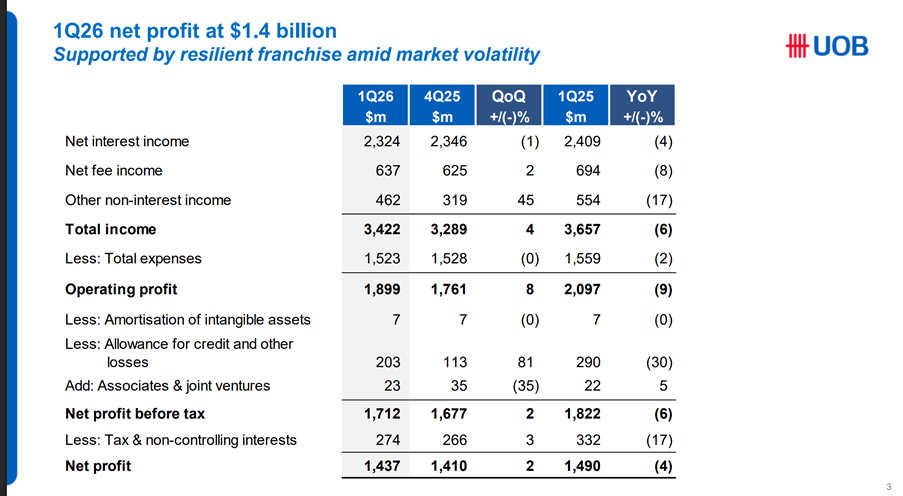

1Q26 net profit fell 4% year on year as lending margins declined, while management guided for FY26 NIM of 1.75%–1.80%, below the 1.82% reported in the first quarter.

Management expects margins to keep compressing this year, not recover.

The genuine long-term ROE story is the Citibank ASEAN integration, which is now largely complete.

Management wants to monetise 8.5 million ASEAN customers and double wealth income by 2030.

The early numbers look promising — trade loans grew 19% in 1Q26 and wealth income rose 6%, suggesting that the strategic logic of the Citi acquisition is finally showing up in the results.

But 2030 is a long way away.

And “doubling wealth income” is exactly the kind of promise I would rather pay for after I see results, not before.

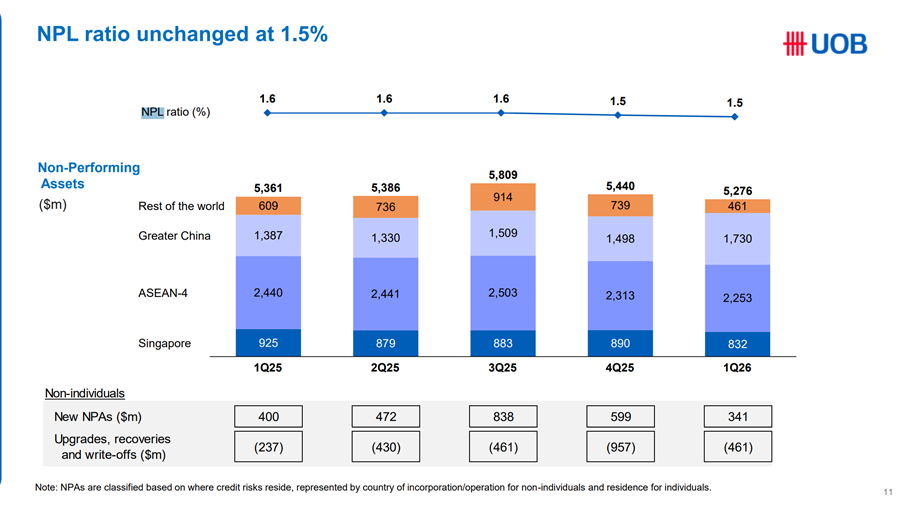

Then there is asset quality.

UOB’s 1.5% NPL (non-performing loans) ratio is the highest of the 3 banks, while Greater China real estate remains management’s explicitly flagged watchpoint.

This is the same roughly S$48 billion exposure behind the S$600 million pre-emptive provision that sent the stock lower last year.

If Hong Kong commercial property takes another leg down, the ROE gap widens rather than closes.

That is the central risk.

So on fundamentals alone, I agree with the readers who pushed back on UOB — and with Citi.

There is nothing in the fundamental results to suggest that UOB is on the same level as DBS or OCBC today.

Why the UOB trade works anyway

Here is the thing.

I can run all the valuation analysis I want, but UOB still outperformed both OCBC and DBS this week.

So I think a more practical view is required.

From a fundamental perspective – UOB does not need to re-rate to OCBC’s valuation for the position to work.

Book value can compound at roughly 8% a year through retained earnings, while the shares pay a dividend yield of about 4% at today’s price.

The valuation multiple has already moved from roughly 1.25x to 1.4x without any meaningful ROE convergence.

Even if the multiple holds from here, earnings / book-value growth plus dividends can still produce a low-double-digit annual return.

If the Citi ASEAN wealth strategy delivers and NIM bottoms in 2027, that is upside on top.

And then there is the trend.

Regular readers know my framework — buy uptrends, never average into downtrends, and remember that the crowd is right about 80% of the time.

When I first covered UOB in November, the stock was below every key moving average and I passed.

When the S$33 support held on rising volume, I changed my mind and bought, and then I added when it broke above key moving averages.

But I always hesitated from adding to the position in huge size because unlike DBS and OCBC, UOB stock was going sideways.

This week resolved that uncertainty.

UOB has now printed 5 consecutive all-time highs on volume.

In plain English, UOB has gone from “cheap but going sideways” to “cheap and trending up.”

That is a meaningful change and should not be underestimated.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

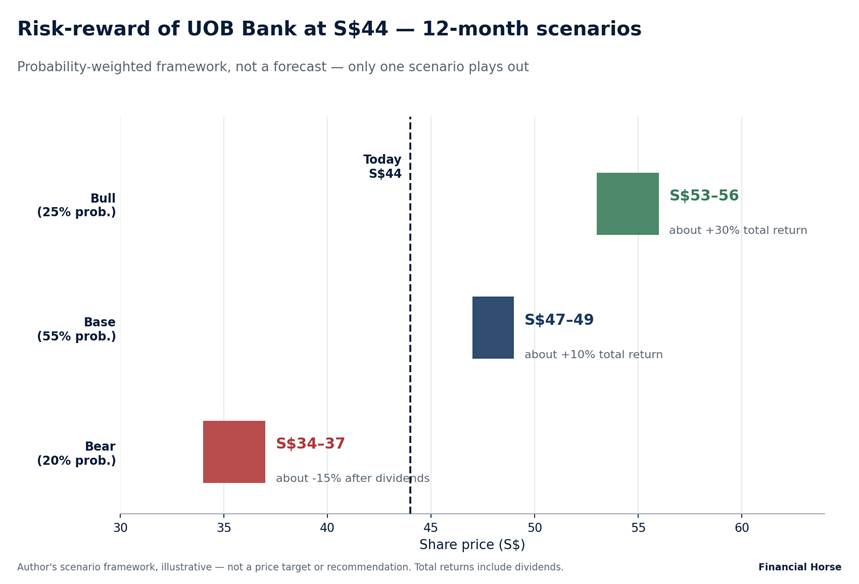

Risk-reward of UOB Bank at S$44

That being said – this stock has run 17% in 1 month.

Chasing a vertical move is how you turn a good position into a bad entry.

Here’s how I would think about risk-reward the next 12 months:

Bull case (25%) — UOB executes well, the sector re-rates and the share price reaches the mid-S$50s, producing about a 30% total return including dividends.

Base case (55%) — earnings and book value grow, but the valuation multiple stops expanding; the share price reaches the high S$40s, producing about a 10% total return including dividends.

Bear case (20%) — a recession or further deterioration in Hong Kong real estate sends UOB back to the mid-S$30s, producing about a 15% loss after dividends (potentially more depending on the severity).

For what it is worth, this is consistent with what I told FH Premium readers in May: Singapore banks are no longer an easy asymmetric trade at these prices.

The easy money — buying UOB at S$33 with a yield of about 6% — has been made.

What remains is a trend trade with a valuation cushion, and this week showed that there is still money to be made from that.

What I’m doing with my money – will I buy (or sell) UOB Bank?

Which brings us to the million-dollar question.

I bought UOB in the low S$33s as a speculative position and added when it broke above the 200-day moving average.

I have a decent-sized position today, although it is still about half the size of my OCBC position.

My instinct after 5 straight all-time highs is to take profit.

Regular readers know that this is my most expensive bias — I sold some of my AI positions before the parabolic run this year and had to buy Micron back at double my exit price.

Selling winners too early has cost me far more than holding losers too long.

So I am consciously doing the opposite of my instinct – I’m letting my position in UOB run.

My exit is mechanical, not emotional.

If UOB breaks below key support levels and starts printing lower highs and lower lows, I will trim the position and reassess.

Would I buy more UOB at S$44?

That’s much more tricky.

My combined positions in UOB and OCBC already give me meaningful exposure to Singapore banks, and adding at all-time highs would increase my downside if the sector reverses.

The parabolic 10% rise in the span of a week also suggests potential for a pullback.

But at the same time, the charts for the 3 banks very bullish and suggest more gains ahead, and the fundamental macro picture is supportive (interest rates have bottomed, no signs of imminent recession).

It’s clear to me that I will hold my UOB position.

Whether I will add at this price, I have not made up my mind yet.

I will share latest updated views on FH Premium as and when I make up my mind on this, whether to add to UOB Bank (or take profit).

You can also see my full portfolio shared on FH Premium.

Love to hear what you think though – do you think UOB is a better buy than OCBC and DBS bank going forward?

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

As a trade, UOB would be great for reversal of sentiment and just overall change in mood for banks

For long term hold, I think you answered it as it’s relatively weak among the 3

Excellent research. It seems logical to take some profits at this point given the fundamentals. One of the great things about equities is that we don’t have to sell the entire holding, and the transaction costs are minimal. Furthermore, in Singapore there’s no capital gains tax to worry about. Longer-term all three still banks look good.

Hi FH,

https://sgwealthbuilder.com/2026/07/18/dbs-group-share-price-to-hit-80/

In my view, two major catalysts are driving this massive surge in the DBS Group share price. The first is the highly anticipated prospect of a special dividend. Looking closely at the bank’s SGX filings, an interesting data emerges: DBS conducted its last share buyback on 11 July 2025—nearly a full year ago.

What makes this intriguing for retail investors is that the bank has only utilized roughly 12% of its massive $3 billion share buyback mandate so far. It is highly probable that management intentionally pulled the brakes on buybacks because the soaring share price made accumulating DBS shares less value-accretive. Given that the leadership remains fiercely committed to returning excess capital to shareholders, they aren’t just going to sit on that cash pile. Instead of buying back expensive shares, there is a very strong likelihood that DBS management could dish out special dividends over the next few quarters to make good on their capital return promise.

Evidently, the big boys are buying heavily into this narrative. According to SGX market data, DBS was among the Top Ten Institutional Net Buy counters, with big institutional players net buying a massive $102.3 million worth of shares in the week of 6 July 2026 alone.

https://sgwealthbuilder.com/2026/07/18/dbs-group-share-price-to-hit-80/