The 4% rule says you can withdraw 4% of your retirement portfolio in the first year, then adjust that amount for inflation each year, with a reasonable chance it lasts about 30 years.

Which basically means that if your annual spending needs are $100,000 today, and you have a $2.5 million portfolio – that is enough to last you 30 years.

So quite a few of you have asked me whether the 4% rule actually works if you plan to retire in Singapore.

It’s a fair question, because almost everything ever written about safe withdrawal rates is American research, built on American market data, for American retirees.

In Singapore, the situation could not be more different.

So in this article, I wanted to answer 3 questions:

- Does the 4% rule actually work outside the US?

- What do Singapore’s structural advantages — CPF LIFE, zero capital gains tax, healthcare — actually add?

- What withdrawal rate should a Singapore investor actually plan around?

And I’ll say it upfront — the answer is not 4% (in my view).

What the 4% rule actually says — and where “fails 1 in 6 retirees” comes from

Quick recap of the mechanics.

You retire with a portfolio worth 25x your annual spending, withdraw 4% in year one, then adjust that dollar amount up for inflation every year — regardless of what markets do.

Bill Bengen’s 1994 study found this survived the single worst 30-year retirement window in US history (retiring in 1966, straight into a decade of stagflation).

The Trinity Study later popularised it, showing roughly 95–100% historical success on a 50/50 to 75/25 stock/bond mix.

But here’s the problem — both studies are 100% US market, 100% US inflation.

The “safety” of the 4% rule comes almost entirely from the fact that the US was the best-performing major stock market of the 20th century.

Which brings us to the number in the title — and it’s worth being precise about where it comes from.

In a paper titled “The Safe Withdrawal Rate: Evidence from a Broad Sample of Developed Markets”, four finance professors (Anarkulova, Cederburg, O’Doherty and Sias) rebuilt the whole exercise without the American luck baked in — roughly 2,500 years of asset-class returns across 38 developed markets, tested against realistic lifespans using mortality tables rather than a fixed 30-year window.

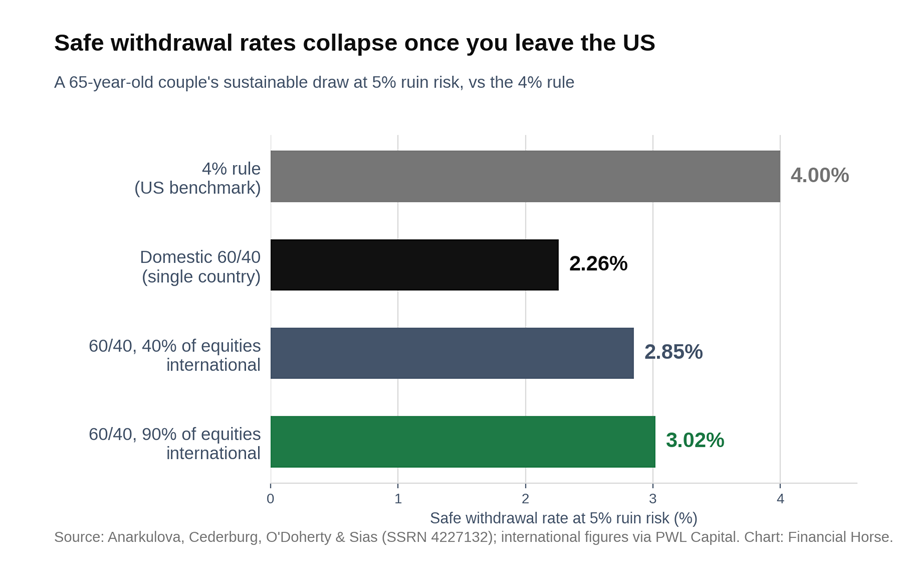

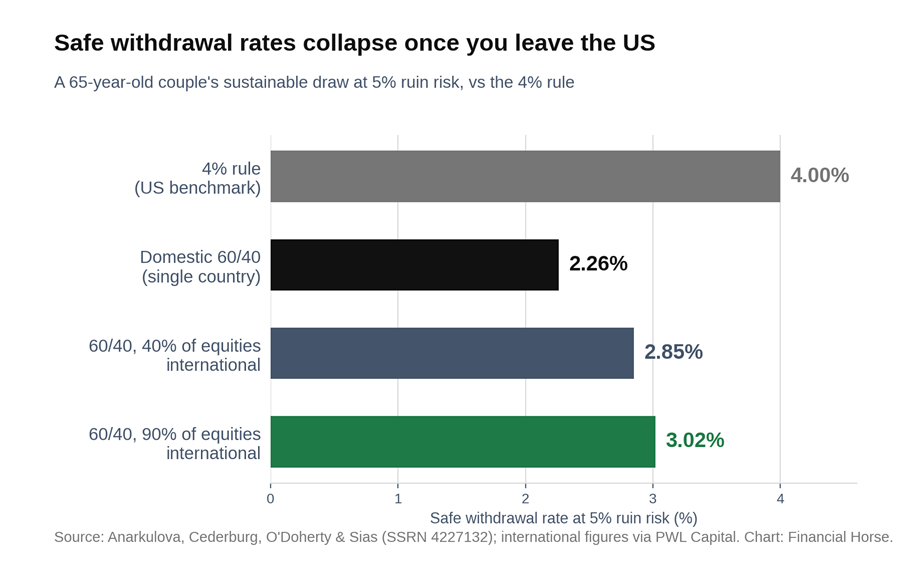

Their headline finding: a 65-year-old couple holding the classic 60/40 domestic stock/bond portfolio, following the 4% rule, has a 17.4% chance of depleting all assets before death.

That’s the 1 in 6 — and “fails” means exactly that: the money runs out entirely while you’re still alive, not merely a disappointing outcome.

And if that couple wants to keep their odds of ruin below 5%, the safe withdrawal rate isn’t 4%.

It’s 2.26%.

Diversifying globally helps meaningfully — Cederburg’s team puts the safe rate at 2.85% with 40% of equities international, and 3.02% at 90% international.

In plain English — America got lucky, and the 4% rule is what that luck looks like written down as advice.

Earlier work by Wade Pfau found the same thing from a different angle: across 20 developed countries, the withdrawal rate that survived the worst historical case reached 4% in only 5 of them.

A Japanese retiree in 1937 following the 4% rule ran out of money in 3 years.

And before anyone asks about running this study on the STI — you can’t (at least not reliably), because Singapore’s market simply doesn’t have a long enough independent history, and the market is heavily concentrated in 3 banks and a handful of REITs.

Long story short — the 4% rule is not a law of nature, it’s a side effect of backtesting on the American 20th century.

A retiree who bets their home market will be the next America is at risk of making exactly the bet that failed Japanese, Italian and German retirees.

The easy fix is global diversification – but that carries its own risks.

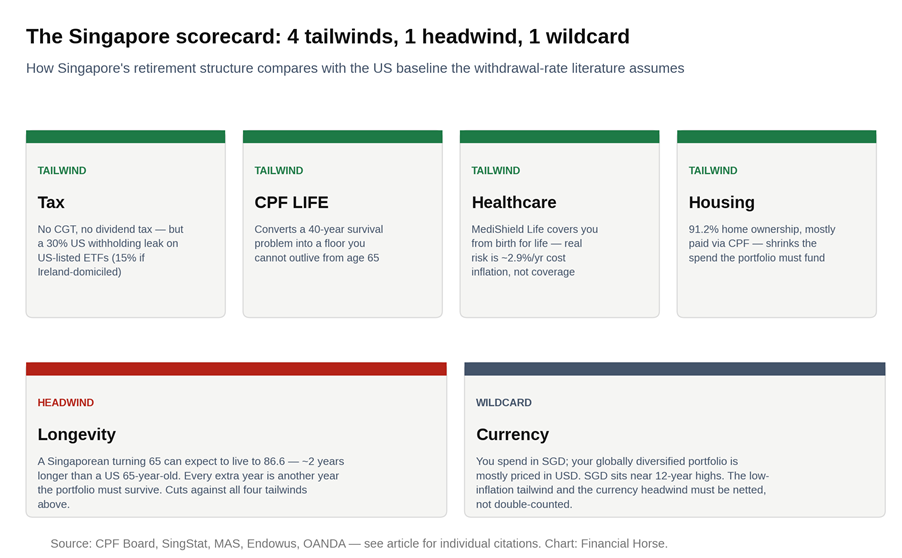

The 6 Singapore adjustments — 4 tailwinds, 1 headwind, 1 wildcard

Reasoning from first principles.

What are the differences between a US retiree, and a Singapore retiree?

A few big ones come to mind.

Tailwind 1 — CPF LIFE. The single biggest lever in this whole analysis

Probably the biggest one – CPF LIFE.

Here are the 2026 numbers for reference:

| Tier | 2026 sum | Monthly payout from 65 (Standard Plan) | Annualised |

| Basic (BRS) | S$110,200 | ~S$950 | ~S$11,400 |

| Full (FRS) | S$220,400 | ~S$1,780 | ~S$21,360 |

| Enhanced (ERS) | S$440,800 | ~S$3,440 | ~S$41,280 |

CPF LIFE solves the exact problem retirees are most afraid of: you cannot outlive it.

Once CPF LIFE starts, it keeps going, regardless of how long you live.

Practically this means that even if you run out of money in your portfolio, CPF LIFE provides a guaranteed floor income.

This has huge implications on asset allocation, as this single security layer is a massive security blanket.

Tailwind 2 — Singapore has no capital gains tax, and no tax on dividends

Singapore has no capital gains tax and no tax on dividends for individuals.

A US retiree pays capital gains and dividend taxes on the way out of their portfolio — we simply don’t, and that’s a real structural advantage.

But the popular “0% tax” framing misses a leak: Singapore has no tax treaty with the US, so US-listed ETFs (VOO, VTI, QQQ and friends) suffer a 30% US withholding tax on every dividend, deducted before the money ever reaches you.

On a global portfolio yielding ~1.5%, that’s roughly 0.4–0.5% of your portfolio lost every single year.

Ireland-domiciled UCITS ETFs (the CSPX/VWRA family) cut the withholding to 15% — roughly 0.2% a year — which over a 40-year retirement compounds into years of extra spending, not a rounding error.

And one more trap while we’re here — US-listed holdings above US$60,000 are potentially exposed to US estate tax of up to 40% on death for non-US persons, which is another point for the Irish-domiciled route.

I wrote more about estate tax recently, so check out the article if you are keen.

Tailwind 3 — Healthcare, the underrated one

The biggest hidden tail risk in the US retirement literature is an uninsured medical catastrophe, especially for anyone retiring before Medicare at 65.

A Singaporean is covered by MediShield Life automatically, from birth, for life — retire at 40 and you’re still insured.

The honest caveat: our real healthcare risk is cost inflation, not coverage — that ~2.9% a year compounds to ~77% over 20 years, and your spending basket tilts toward healthcare precisely as you age.

Tailwind 4 — Housing

91.2% of resident households own their home, typically paid down through CPF by retirement.

Many American retirees carry rent or a mortgage into retirement — their 4% has to fund shelter, ours mostly doesn’t.

The headwind — how long you live

The number that matters here isn’t life expectancy at birth — it’s life expectancy at 65, once you’ve already survived to retirement.

A Singaporean turning 65 in 2025 can expect to live to 86.6 on average — roughly 2 years longer than an American 65-year-old — and half will live longer than that.

Every extra year of life is another year the portfolio must survive — and if you’re FIRE-ing at 45, you’re asking it to survive 40+ years.

This matters, in a big way.

The wildcard — currency and FX risk

You spend in SGD, but your globally diversified portfolio is mostly priced in USD.

MAS runs a structural gradual-appreciation policy, and the SGD sits near 12-year highs against the dollar (around 1.29 as of mid-July 2026, its strongest since 2014) after gaining over 6% in 2025 alone.

In plain English — if the SGD keeps appreciating over time vs the USD, and your investment assets are mainly USD denominated, you’d better hope that your USD investment returns outpace the USD depreciation vs SGD.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

So… what is the “real” safe withdrawal number?

Which brings us to the million dollar question — what rate should you actually use?

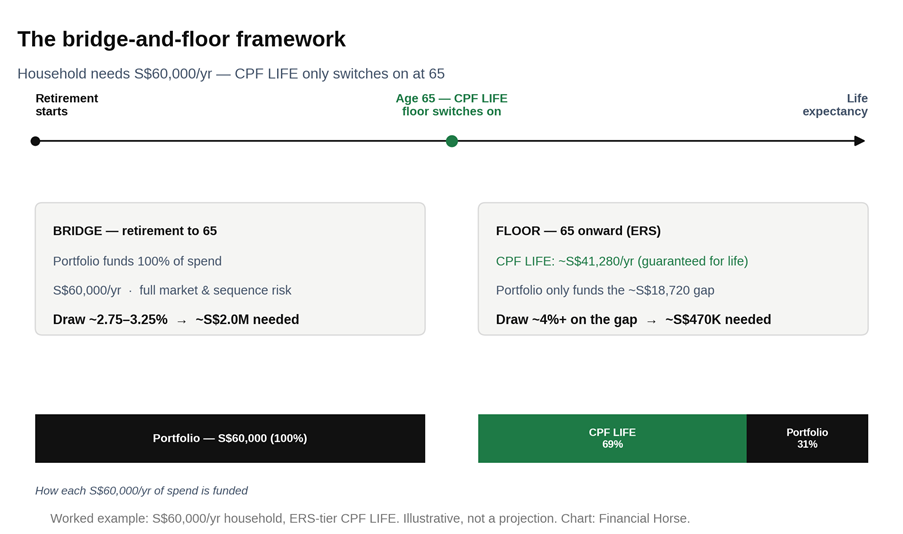

I don’t think a single headline number is honest, because a Singapore retirement has two distinct phases.

Phase 1 — The bridge (retirement to 65). Your portfolio is the only income source, carrying full market and sequence risk.

Starting from Cederburg’s globally diversified 2.85–3.02%, nudged up modestly for our zero tax drag (a judgment call on margin of safety), and nudged down for longer FIRE horizons and the currency headwind.

I would say a “safe” withdrawal rate for this phase is probably around ~2.75–3.25%.

And the longer this period lasts, the closer to the bottom of that range you should sit.

To be on the safe side.

Phase 2 — The floor (65 onwards).

After 65, CPF LIFE kicks in, and your portfolio only needs to fund the gap above it.

Because you now have a minimum safety income level in the form of CPF life, the residual-gap portfolio can safely run at 4% or above.

This is standard result in annuity research — adding a guaranteed income floor to a retirement plan is a huge improvement on the sustainable rate on everything else.

It’s insurance that allows you to take risk elsewhere.

In plain English – CPF Life is actually a pretty big gamechanger (in a good way), at least theoretically.

What does this mean in reality for retirees?

Let’s run the numbers on a household spending S$60,000 a year.

Assuming this person has the ERS CPF LIFE, these are the illustrative numbers:

| Pre-65 (bridge) | Post-65 (floor, ERS) | |

| CPF LIFE income | S$0 | ~S$41,280 |

| Portfolio must fund | S$60,000 | ~S$18,720 |

| At ~3% / ~4% draw | ~S$2.0M needed (using the lower end 3% draw) | ~S$470K needed |

CPF LIFE turns a 40-year survival problem into a 15-year bridge problem, and the bridge is where all the real risk lives.

Because once CPF LIFE kicks in, the risk across the portfolio is reduced.

That’s also why sequence risk does maximum damage — a bad first decade before 65 has no floor beneath it — so the bridge phase is exactly where you need to have some cash/bonds set aside to meet spending needs.

Stock markets in real life don’t deliver smooth 8% returns year after year, there are years where you may see a 20% drawdown, and if you don’t have CPF LIFE or cash set aside, that could be tricky.

Long story short – in my view, the 4% rule doesn’t survive the trip to Singapore intact.

A better way to think about it is to plan around ~3% while you’re bridging to 65, and let CPF LIFE do the heavy lifting after that.

And if you haven’t maxed out to ERS, this analysis is a strong argument for why you should think about it.

So that’s how I’m thinking about safe withdrawal rates in Singapore today.

Love to hear what you think — what withdrawal rate are you actually planning around?

This article was written on 17 July 2026. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

Why not build a dividend centric portfolio instead of depending on a withdrawal rate, and being forced to make withdrawals (sell) even in years where the market is down a lot?

In the scenarios where the market is down a lot (eg. 08, COVID), the dividends are likely to be cut too.

Enjoyed reading this, thanks for the article. 60:40 with 90% International is 3% but without the capital gain tax does that translate into slightly higher withdrawal rates? Also some suggests using dynamic withdrawal rule which can nudge the rate further higher. What do you think?

I think it’s one of those where you hope for the best, but prepare for the worst. If the portfolio pulls 5% – great. But stress test for a scenario where it does not – and can you survive a lower return.

I think you’re probably being a bit too conservative, but then nobody wants to contemplate the grim possibility of running out of money in retirement. Your points about CPF-Life are also well made. However, you failed to mention that, at the moment, the CPF is promising an extra 7% on your retirement account for every year that we delay starting to take withdrawals. I’m planning to do just that myself using my SRS for those 5 years between age 65 to 70.

Good point, appreciate the sharing!

Curious if you’ve read Bengen’s latest book where he arrives at 4.7% as an updated number. The only real historical headwind I can see is currency fluctuation which could become clearer over the course of the next US presidency (and US$ depreciation could also increase international inflow into their market and boost nominal value of their stocks). For core inflation, Singapore actually does very well on inflation due to a solid government and CDC vouchers – we’ve been much more stable than most of the developed world on essential goods inflation since Ukraine war. The other major potential headwind is a total change in market dynamics from potential AI developments, which I guess we’ll only know in a few years (i.e. be very conservative in 2026). Thirdly, if things really overheat here and/or the US$ depreciates another 10% over a decade then we’ll always have the JB/Thailand getout clause.

I guess I’m saying that other than AI rewriting the global equities system then I’d feel very comfortable with a well balanced global portfolio plus cash/bonds reserve delivering 4%.

Interesting. Have not seen the analysis, but 4.7% strikes me as a high number that may or may not survive the test of inflation. The path forwards looks to be very inflationary, which would be the biggest wildcard in my view.

Your recommendation is too general but slightly better than the 4% rule… Too many moving parts to determine whether $2.5M is sufficient or not, this figure maybe the liquid net worth of the top 5% of SG household, and if this figure is insufficient, than what is for common Singaporeans? But i have to agree that 2.5M in SSG or bonds will run out for sure based on 100K spending p.a. but it may last if they scale back expenses or life expectancy shorten for some….

Good point – appreciate the sharing!