In this week’s FH Premium article, I shared my views on whether bank stocks or REITs are a better buy today.

Banks are the strong momentum play, while REITs are the mean reversion play.

This led to a great question from a subscriber:

Amongst the three banks, which one would be the most interesting buy right now based on your analysis? If you were to add more. Thank you.

So I wanted to take a closer look at the 3 bank stocks.

Share price performance of DBS compared vs UOB and OCBC

This is the year to date performance of the 3 local banks.

DBS is the candles, green is UOB, and blue is OCBC.

You can see how the year to date performance (excluding dividends) is:

- OCBC (18%)

- DBS (10%)

- UOB (7%)

Now OCBC is my biggest bank position today, so I am understandably very pleased with this performance.

But let’s zoom out to the 1-year chart.

Here the performance is much more stark:

- OCBC (46%)

- DBS (41%)

- UOB (7%)

Over the past 1 year, both OCBC and DBS have been standout performers – but the bulk of OCBC’s return came over the past half year.

While UOB has just gone sideways for a 1 year.

Why is OCBC share price beating DBS and UOB Bank in 2026?

If you ask me, it’s down to 2 factors:

- Strongest earnings growth – driven by wealth management

- More reasonable starting valuations

Strongest earnings growth – driven by wealth management

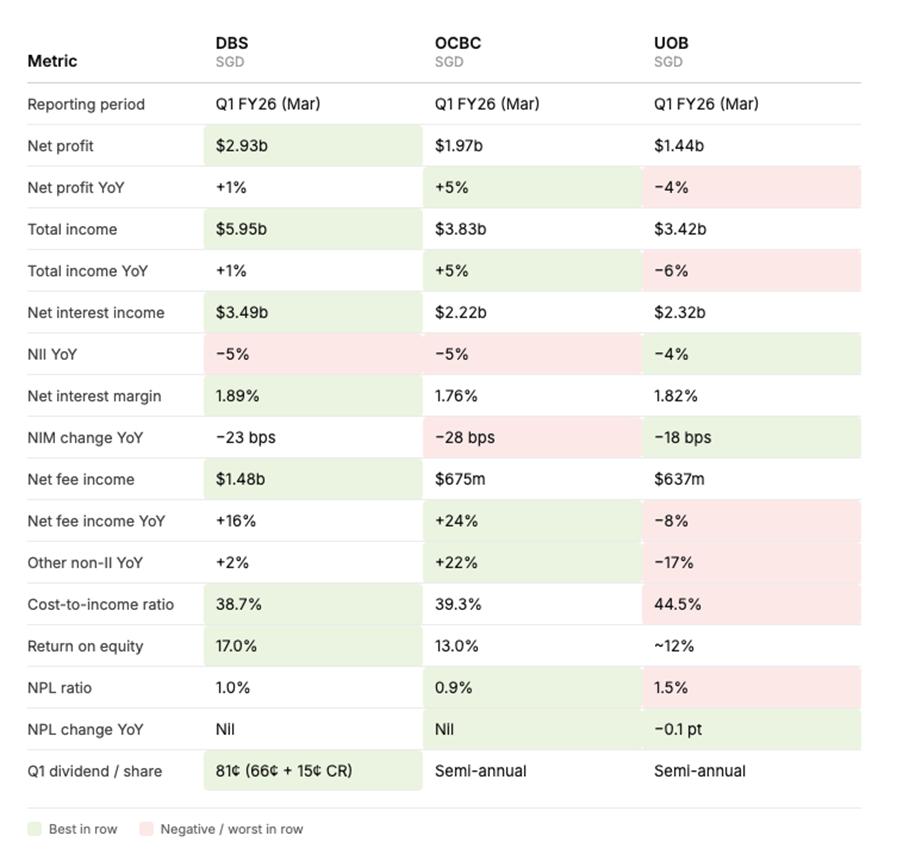

I came across this great chart below that compares the operating performance for the 3 local banks.

If you zoom in on the year-on-year net profit line item.

The performance is obvious:

- OCBC (+5%)

- DBS (+1%)

- UOB (-4%)

OCBC demonstrated the strongest earnings growth in the recent quarter – it’s no wonder their share price is outperforming.

The better question of course, is what is driving this outperformance?

You can see net interest margin for the 3 banks is generally similar around 1.8%, so none of this outperformance is coming from the lending business.

The outperformance rather, is coming from the fee income business.

OCBC is showing 24% growth in net fee income, which handily beats that of DBS and UOB.

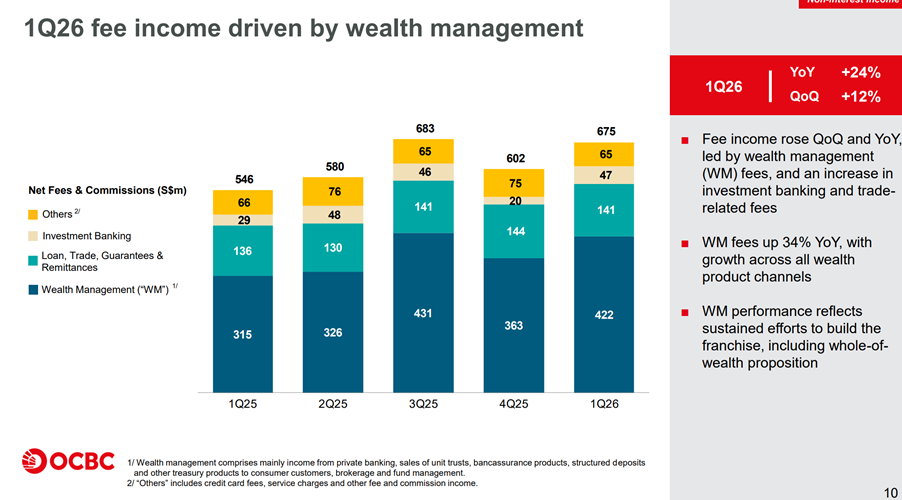

Broken down below – the bulk of the growth is coming from wealth management, with a massive 34% year on year growth.

Bottom line is that because of the lower interest rate climate, all 3 banks are facing pressure on the core lending business.

The difference then becomes who can deliver strongest growth on wealth management.

DBS showed they could deliver on wealth management in 2025, hence the market rewarded them.

In 2026 OCBC showed that they too could deliver on wealth management, hence their recent outperformance.

More reasonable starting valuations

The other point – is valuations.

Latest Price/Book of DBS and OCBC below.

Even after the recent rally OCBC sits at 1.7x book, a significant discount to DBS’s 2.5x book value.

Yes, I get that DBS has best in class 17% ROE.

But at 2.5x book, a lot of that strong performance is already priced in.

Whereas OCBC at around 1.5x before the rally, had “more room to run”.

In plain English – OCBC outperformed vs market expectations, whereas DBS delivered more in line with market expectations.

Hence OCBC’s stock price is stronger of late.

| Bank | Share Price | NAV per share | P/B | ROE (latest) | 10-yr avg P/B |

| DBS | S$61.43 | S$24.38 | 2.52x | 17.0% | ~1.5x |

| OCBC | S$23.33 | S$13.38 | 1.74x | 13.0% | ~1.1x |

| UOB | S$37.79 | ~S$30.5 | ~1.24x | ~11% | ~1.1x |

Which is the best bank stock to buy today?

But that said.

Nobody buys a stock for where it is today, you buy a stock for where it will be in 18 months.

Both points we discussed above are historical – backward looking.

To evaluate which bank is best to buy today, we need to be forward looking.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Technical Analysis

Let’s start with the charts, because sometimes technical analysis gives us useful clues that we can back up with fundamental analysis.

The charts are unequivocal.

Both DBS and OCBC are in strong uptrends – with OCBC having the arguably better chart.

UOB on the other hand – is a lot more mixed.

It’s not to say the chart is terrible because you could argue the stock is forming a base, and the key $33 support at which I picked up the stock is still holding.

But no uptrend at the moment.

Which bank has the strongest business in 18 months? That is not already priced in?

Anecdotally, most of us would think that in terms of the best execution today, they would be ranked as follows:

- DBS

- OCBC

- UOB

And frankly, that’s exactly what we see reflected in the chart as well.

But in investing, we also need to ask to what extent has this been priced in.

DBS is the best performing bank, but at 2.5x book value it sits very close to a global best in class bank like JP Morgan.

How much more multiple expansion can we see at these kinds of valuations?

And if there is no multiple expansion, then growth has to track earnings growth or inorganic growth, both of which are execution dependent.

Whereas with OCBC and UOB, if they can prove that they can deliver on the same extent as DBS, there could be further room for multiple expansion.

| Bank | Share Price | NAV per share | P/B | P/TBV | ROE (latest) | 10-yr avg P/B |

| DBS | S$61.43 | S$24.38 | 2.52x | ~2.55x (minimal goodwill) | 17.0% | ~1.5x |

| OCBC | S$23.33 | S$13.38 | 1.74x | ~2.5x¹ | 13.0% | ~1.1x |

| UOB | S$37.79 | ~S$30.5 | ~1.24x | ~1.5x¹ | ~11% | ~1.1x |

| JPM | US$303 | US$128.38 | 2.36x | 2.78x | 19% | ~1.6x |

¹ Tangible book adjustments for OCBC/UOB reflect ~S$4.4bn (OCBC) and ~S$4.0bn+ (UOB) of goodwill/intangibles from past acquisitions (BoS, Wing Hang, ING, Citi ASEAN).

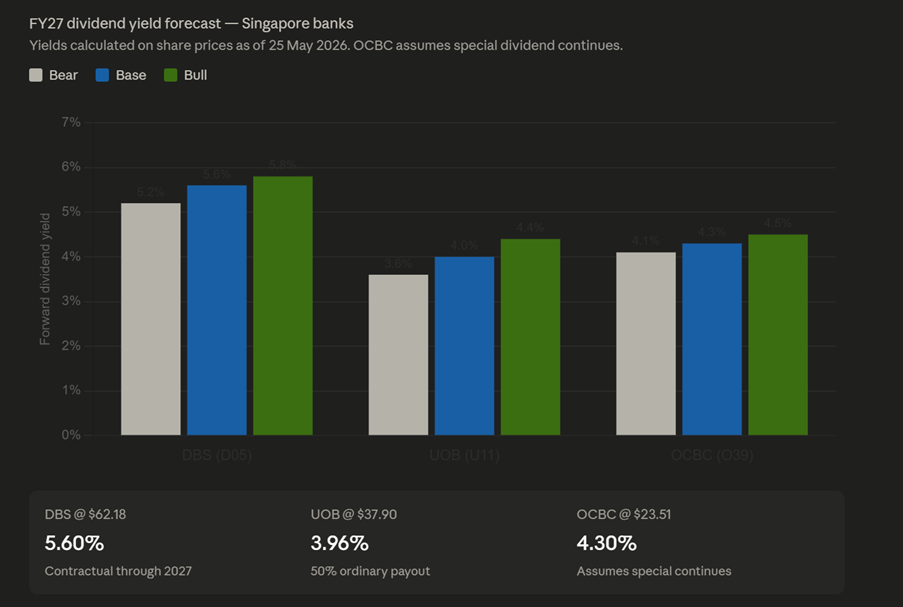

DBS offers the highest dividend – due to capital return dividend

Comparing the forward dividend yield of the 3 local banks:

- DBS (5.6%)

- OCBC (4.3%)

- UOB (4%)

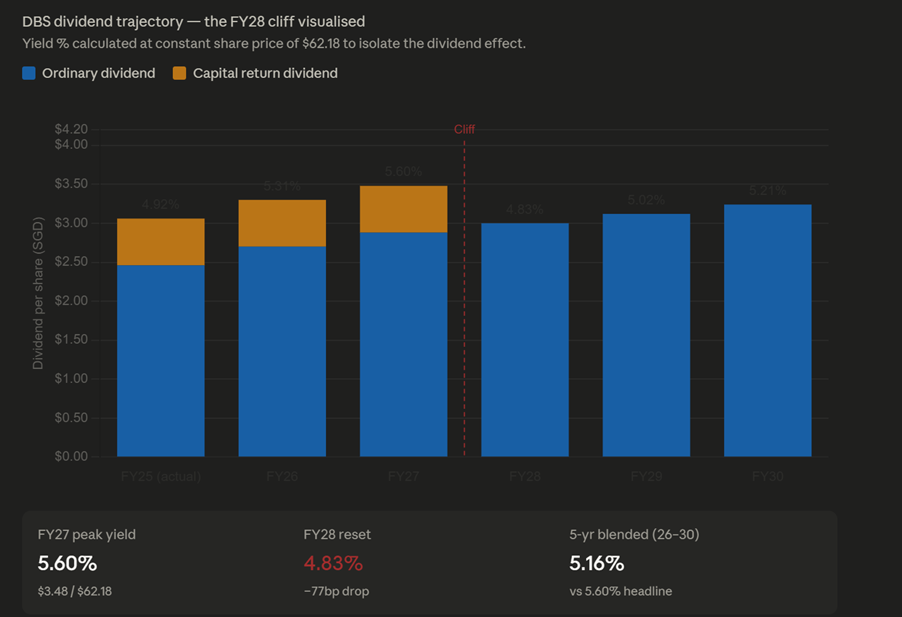

There is a nuance to this, because DBS’s dividend is artificially “juiced” because of its capital return dividend.

To explain in plain English, bank dividends are split into 2 components.

The first is the ordinary dividend, which is usually paid out of 50-60% of the bank’s profits.

The capital return dividend, is an additional dividend on top of that – a return of capital.

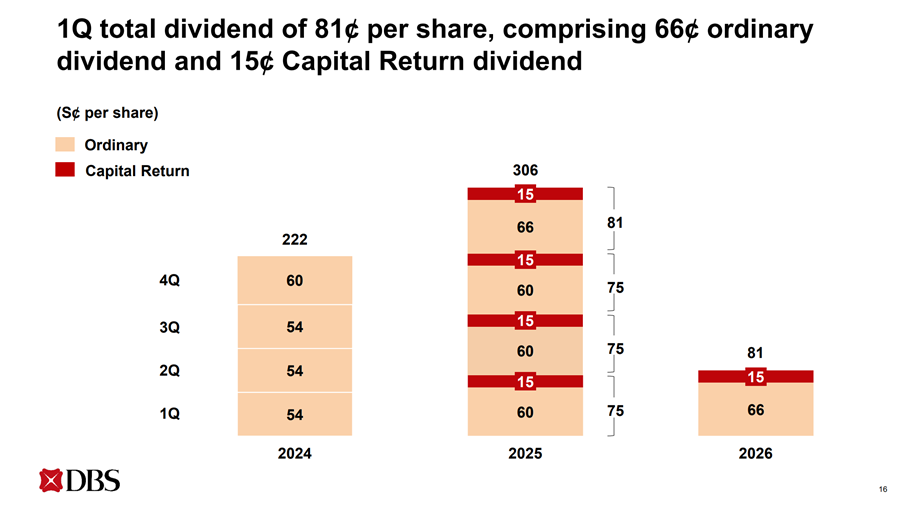

DBS accumulated CET1 well above target (peaked at ~17%, target ~13–14%) from years of retained earnings plus integration of LVB and Citi Taiwan.

Rather than letting that excess capital sit idle and drag ROE, management committed to giving it back over a fixed 3-year window:

- $8B total programme (2025–2027): $5B via the $0.15/qtr capital return dividend + $3B via share buybacks

- The $0.15/qtr × 4 quarters × 3 years × ~2.84B shares ≈ $5.1B — that’s the maths backing the schedule

Because this is a capital return dividend funded by excess capital – mathematically it means the dividend will end once the excess capital is fully paid out.

And that date is end-2027.

Charted below – you can see how DBS’s dividend will drop in F28 once the capital return dividend ends.

Meanwhile, OCBC has approximately S$800 million remaining under its S$2.5 billion two-year capital return plan, which runs through end-FY2026.

Management (CFO Goh Chin Yee, 1QFY2026 briefing) has stated that any unutilised balance will be returned as special dividends, with CEO Tan Teck Long expressing a personal preference for this route.

Sell-side (DBS Research) flags this as a potential re-rating catalyst.

It’s never easy to interpret the impact on share price, but one way of seeing this is that OCBC has added optionality going forward, and a potential re-rating catalyst if they do a similar capital return plan like DBS.

Whereas for DBS this is already priced in at this point, and the capital return dividend will fall off by the end of next year.

Which of the 3 bank stocks would I add today?

From a Dr Wealth article I came across (to be absolutely clear – not my view):

“The short-term outperformance of OCBC is entirely justified. It is the result of brilliant capital management, an aggressive share buyback scheme, and a fundamental earnings beat driven by wealth management. For income investors seeking deep value and the potential for late-2026 special dividends, OCBC remains a strong favourite for the short term.

However, DBS remains the long-term structural winner. While you have to pay a premium valuation to own it, DBS’s industry-leading ROE, dominant digital infrastructure, and 74.6% dividend payout ratio make it the ultimate compounding machine.

If your timeline is 6 to 12 months, ride the OCBC capital-return wave. If your timeline is a decade, DBS is still the king of the hill.”

If you ask me, I think it’s a bit more nuanced.

All 3 local banks today benefit from the structural tailwinds of Singapore as an Asian financial center.

Significant amounts of capital are flowing into Singapore, which is why you see the wealth management arms performing so strongly.

So all 3 banks give you that kind of macro exposure.

Within that framework, no doubt DBS has been the strongest execution wise, followed by OCBC which is catching up recently, and UOB still a distant third.

The problem is that to a large extent, much of this is already priced into the stock.

For DBS to outperform going forward, you need DBS to outperform vs fairly optimistic expectations.

For UOB to outperform going forward, you just need UOB to outperform vs fairly pessimistic expectations.

So it’s all going to come down to how the management team executes vs expectations.

For investors who don’t want to stock pick and just want the broad macro exposure, there’s a good argument to just buy all 3 banks, and if you think DBS outperforms maybe you overweight DBS.

If I absolutely had to pick one?

Frankly I don’t think any of the 3 banks are a fantastic deep value buy today, as I see them as fairly valued.

If I absolutely had to pick on?

I might marginally lean towards OCBC for their strong momentum, and optionality from the capital return plan.

And I also find UOB interesting because if they can surprise execution wise, there could be plenty of upside at current valuations.

But frankly, this is not a view I have a great deal of confidence in.

Like I said, I find all 3 local banks fairly valued today, and it’s going to come down to execution.

Love to hear what you think though.

Full disclosure that I hold positions in OCBC Bank and UOB Bank.

My full personal portfolio, including stocks I buy/sell, are shared on FH Premium.

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

I would say buying the ES3, with 55% in banks and 25% REITS, is a prudent way of naturally hedging at this market level first. Any further drawdown can be utilized to buy individual stocks

That’s my plan for now

I would not buy now as the prices of DBS/OCBC are currently at peak for the year, would wait for price retracement to decide the long position, Both DBS and OCBC are in my watch list now