In case you’ve missed it.

Ascendas REIT today trades at 2.49.

The other times that it was this low?

Was in 2020 during the peak of COVID, and in 2022 at the height of the interest rate hike cycle.

Mind you this is Singapore’s largest industrial REIT, CapitaLand backed, and pays a 6.2% dividend.

So… is CapitaLand Ascendas REIT a good buy?

Ascendas REIT trades at COVID and 2022 lows

Here’s the weekly chart for reference.

Ascendas REIT at 2.49 is basically the same price the REIT was trading at in 2022 (the peak of the interest rate cycle when T-Bills were yielding >4% yield), and 2020 (when the world was closed due to COVID).

So that’s a very extreme pricing dislocation, considering the circumstances today are nowhere as bad as what we saw during COVID or the 2022 rate hike cycle.

Using the pro-forma DPU, you’re looking at a 6.2% dividend yield at this price, which for a blue chip Industrial REIT is actually pretty decent.

Meanwhile other REITs are near all time highs

And unlike in 2020 or 2022 where the entire REIT market was selling off.

Today the other REITs are nowhere near their lows.

Here’s Netlink Trust for example – trading at cycle highs:

CICT is down slightly from highs, but still way, way up from the cycle lows:

Likewise with Frasers Centrepoint Trust:

You may say that these are all retail and commercial REITs.

Fair point, but here is AIMS APAC REIT, an industrial REIT, and it too is trading near cycle highs:

Why is Ascendas REIT down so much relative to other REITs? Is this because of the recent equity fund raise?

So why is Ascendas REIT trading so poorly?

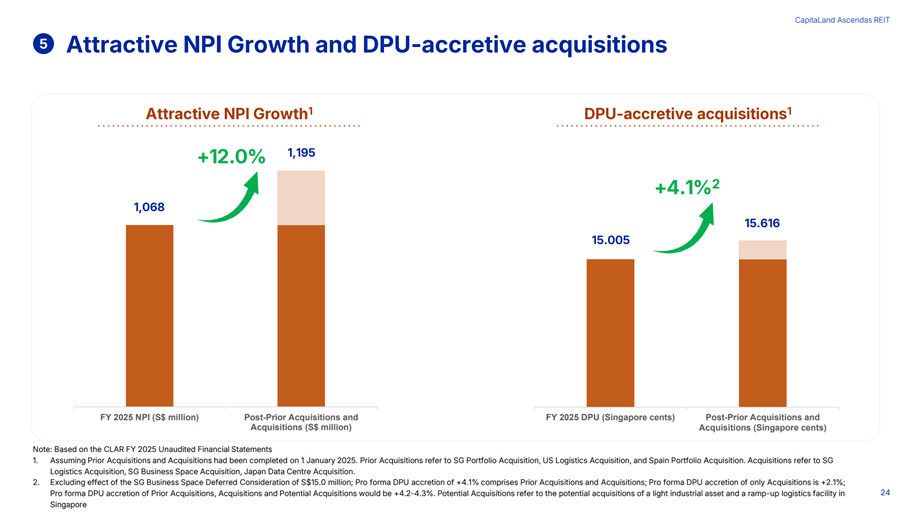

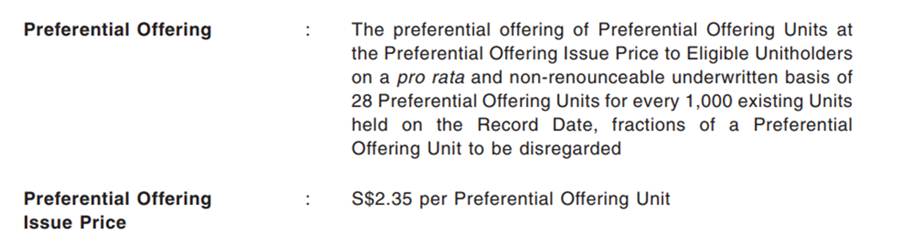

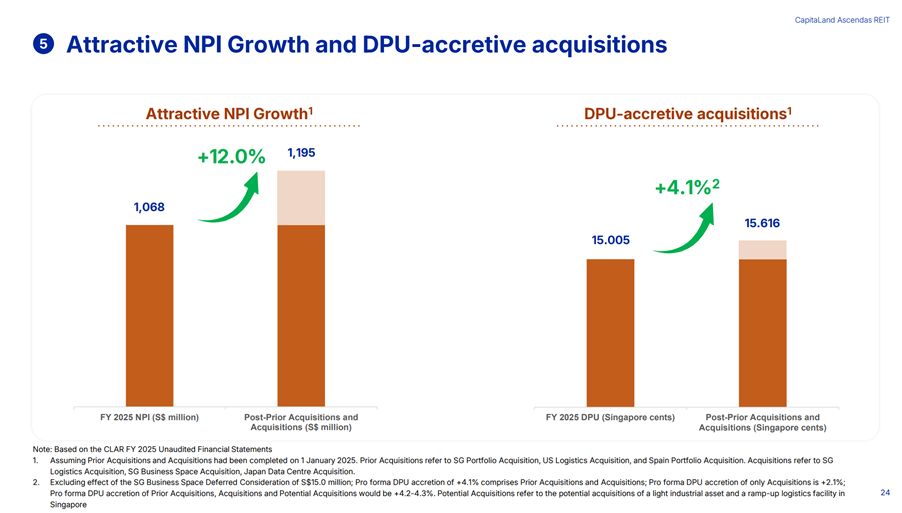

Some of you may say that this is because of the recent equity fund raise, where they did a preferential offering to finance the acquisition of properties in Singapore and Japan.

Frankly that was my initial reaction too.

But diving deeper into the numbers, actually the recent fundraise was not a big one – only 28 units per 1000 units.

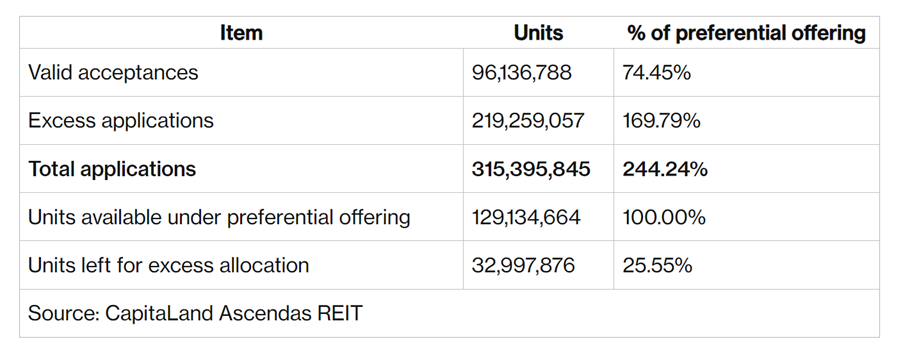

On top of that, the preferential offering was massively oversubscribed.

And when I mean massively – I mean absolutely overwhelming demand.

The preferential offering was 244% oversubscribed, which is by far the strongest showing I’ve seen from any S-REIT in a while.

And this was a DPU accretive acquisition as well, so it’s not like it was a dilutive deal.

So it’s hard to point to the preferential offering and say that this caused such a huge underperformance in the REIT.

You may argue that Ascendas REIT priced the preferential offering at a fairly large discount to the market price (2.35 vs market price of about 2.5).

So investors who applied and got their excess allocation are selling the REIT units on the open market to lock in their gain, creating short term selling pressure.

And you also need to adjust the share price to take into account the effect of the fundraise.

Sure that is one potential explanation, but my gut feel is that it wouldn’t explain all the underperformance.

So… why is Ascendas REIT trading so low? Iran war fears?

Another way to see it is that Ascendas REIT is a predominantly industrial and logistics REIT.

And industrial and logistics companies are likely to be the most impacted by higher oil prices from the Iran war.

So unlike other REITs like CICT where the underlying retail and office rentals are expected to remain resilient.

Ascendas REIT could be selling off due to fears over softness in underlying rentals going forward.

This is possible too, and I could get behind this theory.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

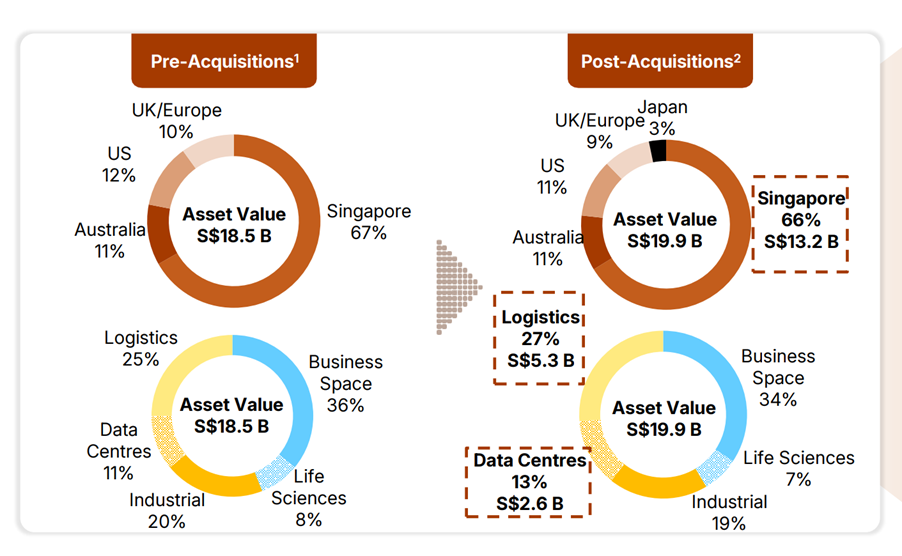

Good news is that the asset base is still predominantly Singapore after the acquisition

That said, the good news is that Ascendas REIT remains primarily Singapore assets even after the acquisition.

I’ve always said that in this post 2020 cycle I only want to hold Singapore real estate.

And Ascendas REIT with 66% Singapore assets certainly fits that bill.

With Singapore real estate I think that you can look through any short term rental weakness as the medium term rentals will likely recover due to controlled supply demand dynamics.

But with non-Singapore real estate I genuinely hesitate to say that, which is why post 2020 I no longer invest in REITs with predominantly non-Singapore real estate.

BUT – Short land tenure left on the industrial assets

I know a lot of investors dislike Singapore industrial properties because of the short lease tenure.

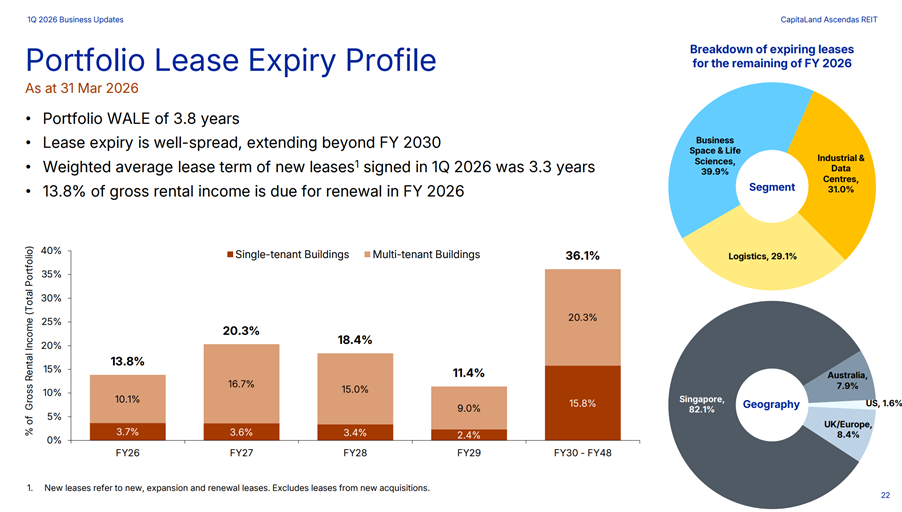

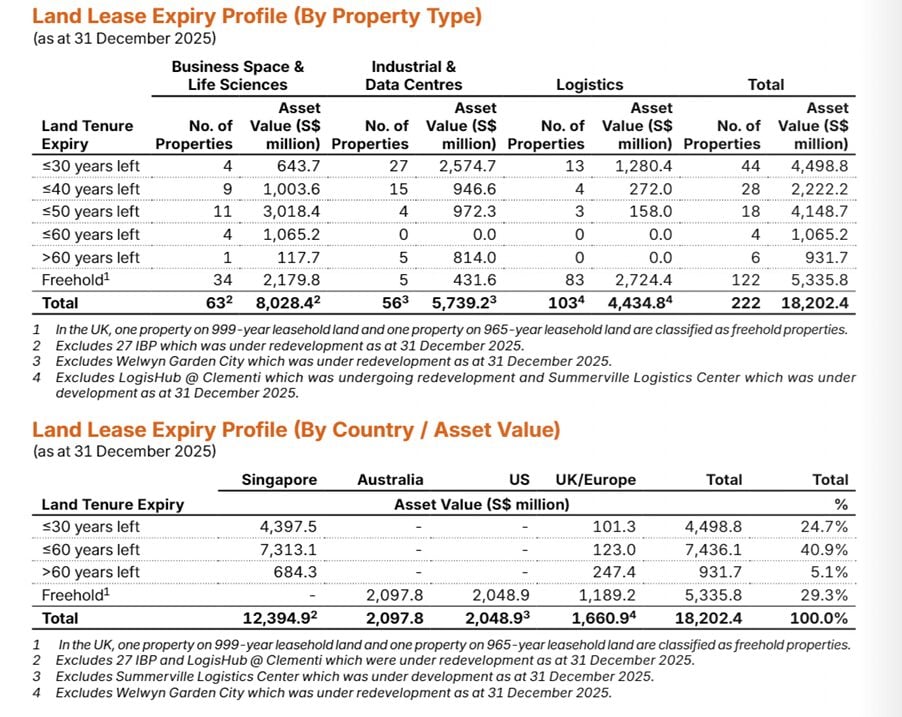

You can see how with Ascendas REIT – there is over $4.3 billion in real estate with less than 30 years left on the land tenure.

That’s a whopping 24.7% of the asset base.

To be fair, there’s nothing Ascendas REIT can do about this because this is the nature of industrial land in Singapore, where the lease tenures are shorter than retail or office space.

You can pull up any other industrial REIT and you’ll find the same problem.

So frankly this is industrial REIT wide problem.

You can dislike Ascendas REIT from a fundamental point of view because of this, but this alone does not explain why Ascendas REIT is underperforming other REITs.

It’s the same logic with higher interest rates from the Iran war – it should impact REITs across the board.

Ascendas REIT drops 15% in 2026 and pays a 6.2% dividend yield

At current prices, Ascendas REIT is down 15% from the January 2026 highs.

And pays about a 6.2% dividend yield.

How does that 6.2% dividend yield compare to other REITs?

Vs the 10 year SGS yield of 2.08%. that’s a massive 4.1% yield spread.

That’s one of the widest spreads I’ve seen Ascendas REIT trade at for a while.

Even at the 2022 low it was a 2-3% yield spread because interest rates were so high back then.

Benchmarked vs other industrial REITs:

| REIT | Fwd Yield | AUM |

| AIMS APAC REIT | ~6.8% | ~S$2.4B |

| Mapletree Industrial Trust | ~6.5% | ~S$9B |

| CapitaLand Ascendas REIT | ~6.2% | S$18.2B |

| Frasers Logistics & Commercial | ~6.1% | ~S$6.9B |

| Mapletree Logistics Trust | ~6.0% | ~S$13B |

| ESR-LOGOS REIT | ~7–8% | ~S$5B |

AIMS APAC REIT is significantly smaller than Ascendas REIT, there should therefore trade at a higher yield

Whereas Mapletree Industrial Trust is 50% US data centres, and they have been facing problems with the US data centres and are looking to sell a good chunk of those assets, hence again they should trade at a premium.

Meanwhile the fact that CapitaLand Ascendas REIT trades at a higher yield than Frasers Logistics & Commercial Trust (which is heavy on Australian real estate and significantly smaller) and also vs Mapletree Logistics Trust (which has heavy China and Hong Kong exposure which is weak) actually does suggest pricing may be attractive here.

Benchmarked vs other blue chip REITs:

| Name | Asset Class | Fwd Yield | AUM |

| CapitaLand Ascendas REIT | Industrial/business space | ~6.2% | S$18.2B |

| Frasers Logistics & Commercial | Logistics + commercial | ~6.1% | ~S$6.9B |

| NetLink NBN Trust | Telecom infra (business trust) | ~5.4% | ~S$4B |

| Frasers Centrepoint Trust | SG suburban retail | ~5.3% | ~S$4.2B |

| CapitaLand Integrated Commercial | SG commercial (retail + office) | ~5.0% | S$27.4B |

CapitaLand Ascendas REIT is again far ahead of the pack in terms of yield.

Yes there are risks with industrial assets as we discussed above including shorter lease tenure and potential for weaker rents going forward.

So the question is at current prices, to what extent has this already been priced in?

My gut feel is that prices are interesting here, but hey I could be wrong.

Will I buy Ascendas REIT? Are REITs a good buy once again?

Which brings us to the million dollar question.

Will I buy Ascendas REIT today, and are REITs today looking like a good buy again?

Full disclosure that I hold a position in Ascendas REIT.

Personally I see massive dispersion across REITs today.

You see names like Netlink Trust sit close to all time highs, while Ascendas REIT trades close to all time lows, and names like CICT, FCT, Lendlease REIT trade somewhere in the middle.

That’s a lot of opportunity for stock pickers.

Yes there are potential risks with Ascendas REIT as I flagged above.

But ultimately it goes back to risk-reward, and whether you’re being adequately compensated for the risk you’re taking on.

Personally I find Ascendas REIT interesting at this price.

But looking at the chart, it’s fairly clear this is a falling knife at the moment, which makes it hard to call a bottom.

And the fact remains that this is still a REIT.

Best case Ascendas REIT goes back to $3 which is a 20% return.

And throw in a yearly 6.2% dividend yield, you may be looking at 20-30% returns in 2 years in the bull case.

That’s okay returns, but this isn’t a semiconductor stock where you make 30% by next week.

So ultimately – there is an element of needing to understand what you’re buying.

An income play where capital gains are pure upside, Ascendas REIT could be worth a look.

A growth play where you have a chance to double your money in 18 months, this probably isn’t it.

Whatever the case, you can see my full personal portfolio, and the stocks / REITs I am keen to buy, shared on FH Premium.

If I decide to add to my position in Ascendas REIT, or if I change my mind on this REIT, updated thoughts will be shared on FH Premium.

Love to hear what you think though! Do you think Ascendas REIT is a good buy? Why do you think it has dropped so much relative to the other REIT?

Solid Div hold

Mapletree wants to sell US assets? Do you have source for this statement?

Sure here is the link

https://www.businesstimes.com.sg/companies-markets/mapletree-industrial-trust-divest-s600-million-north-america-assets-eyes-japan-and-europe-growth