I was reading the DBS 2Q 2019 Investment Insights recently, and one of the points really caught my eye:

“Barbell – the winning strategy

Build barbell portfolios with exposures at two ends of the risk spectrum. Seek secular growth themes like Digitalisation and Millennial consumption on one end; income-generating assets like REITs and corporate bonds on the other.

…

Maintain a barbell strategy

In 1Q19’s CIO Insights “Tug of War”, we advised investors to adopt a barbell strategy in the way a portfolio should be constructed. We reaffirm this approach.

To recollect, a barbell strategy refers to being heavily-weighted at both ends of the risk spectrum. This means overweighting high-growth stocks on one end of the portfolio, while loading the other end with stable and income-generating ones.”

To be honest, I have never in my life heard of a “Barbell” strategy until this DBS article, so for those of you who are new to this, we are in the same boat.

Basics: Barbell Strategy

Essentially, what this investment strategy says is that you should split your investment portfolio into two. On one end you will have safe, dividend yield plays like REITs and corporate bonds. Let’s call this the yield barbell. And on the other end you will have growth stocks for the capital gains. Let’s call this the growth barbell.

Catchy name aside, the idea at its core is a very powerful one. It creates a portfolio that is heavily exposed to growth stocks (that perform well when the economy is good), and is also exposed to stable, yield stocks (that are more resilient when the market is bad). Sounds like a win win right?

My own investment strategy?

My exact investment portfolio (on a % basis) is disclosed on Patron, but it’s broadly split into high yielding Singapore REITs and stocks, and US growth stocks.

Which coincidentally, is very similar to the “Barbell” investment strategy that DBS talks about. And needless to say, this strategy has performed well the past 12 months due to the Fed changing their mind about rate hikes (pushing up yield stocks), and the significant global rerisking since early 2019 (pushing up growth stocks). So perhaps DBS is on to something here.

How will it perform going forward?

DBS did some backtesting on the “Barbell” investment strategy:

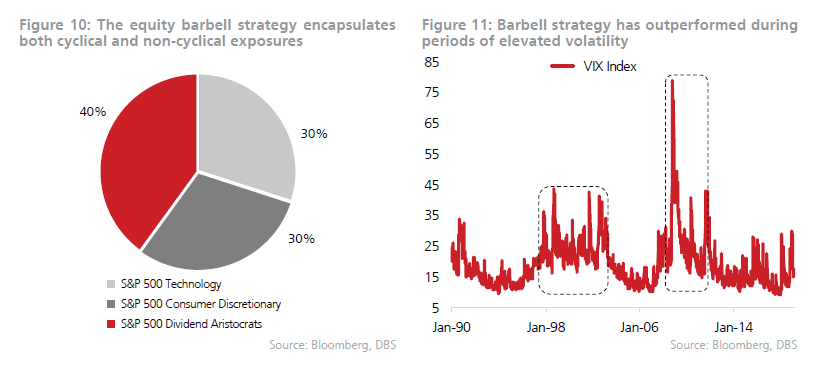

Our research shows that this strategy has historically resulted in substantial outperformance during periods of elevated volatility. We applied and tracked the performance of this strategy in the US equity market. For this analysis, our “US Equity Barbell Portfolio” comprised (Figure 10):

- S&P 500 Technology: 30% weight

- S&P 500 Consumer Discretionary: 30% weight

- S&P 500 Dividend Aristocrats (an index consisting of companies that followed a policy of increasing dividends every year for at least 25 consecutive years): 40% weight

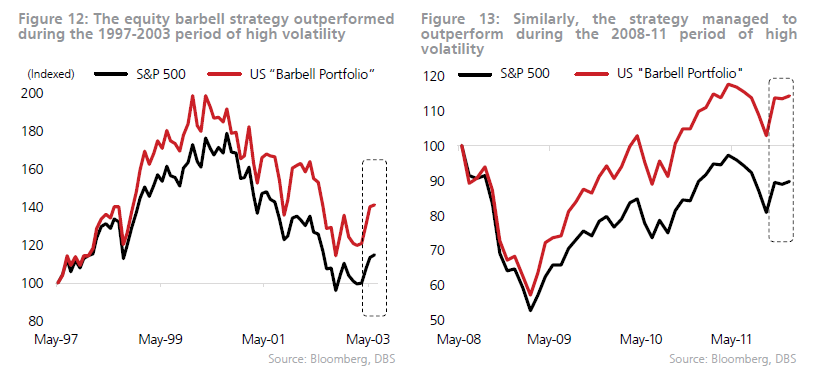

We tracked the performance of this barbell portfolio during two periods of elevated volatility over the past 28 years (Figure 11):

- Jun-97 to Jun-03 (a period where the CBOE SPX Volatility Index (VIX) Index averaged 25.2, vs the long-term average of 19.3)

- Jun-08 to Dec-11 (a period where the VIX Index averaged 28.2, vs the long-term average of 19.3)

For the Jun-97 to Jun-03 period, average monthly returns for the S&P 500 was 0.3% while average returns for the “barbell portfolio” was 0.7%. On a cumulative basis, the S&P 500 gained 14.9% during the period while the “barbell portfolio” surged 41.1%, constituting an outperformance of 26.2 percentage points (Figure 12).

Similarly, for the Jun-08 to Dec-11 period, the S&P 500 registered monthly losses of 0.1% while the “barbell portfolio” saw monthly gains of 0.5% on average. On a cumulative basis, this translated to a 10.2% loss for the S&P 500 and a 14.3% gain for the “barbell portfolio”, constituting an outperformance of 24.5 percentage points (Figure 13).

In other words, it does well in periods of high market volatility, like the one we are going through currently. How it would perform going forward though, is anyone’s guess.

Given how much this investment strategy tracks my own portfolio, asking me to justify it is probably like asking the Chef whether his food is good.

The way I see it though, one main reason why I adopted this strategy is for ease of execution.

When you live in the US and have access to the biggest and most competitive companies in the world, and an incredibly deep and competitive REIT and bond market, you’re free to pick from almost any asset class. When you’re a Singaporean investor though, and you’re confronted with a home exchange (SGX) that comprises mainly bank and property related stocks, it really forces you to get creative. The way I approached it, was to focus on what Singapore and the SGX is good at: Yield stocks and REITs. So I bought up all the yield stocks, REITs and blue chip GLCs that I loved on the SGX.

But at the same time, I knew that if my portfolio is comprised purely of yield stocks, it’s going to underperform in certain economic climates. So I wanted to get exposure to growth stocks as well, for the capital gains.

And because one of the defining events of our lifetime is the rise of technology and its impact on old world industries, I wanted to get exposure to the big tech disrupters like Google and Amazon as well.

And let’s face it, these guys don’t list on the SGX. So I had to go the US exchanges for these.

How to execute this?

There are a couple of nuances to this strategy in my opinion:

Yield plays need to be stable – The yield plays absolutely need to be stable one. There’s no point loading up on a high risk yield play like HPH Trust or Starhub and think you’re done with the yield barbell, because such stocks should belong in the growth barbell.

You really need to find stocks with a sound business model that is less vulnerable to disruption, and that will not be significantly affected by market volatility or macroeconomic shifts. Easier said than done I know.

Picking the right growth stocks – There are growth stocks, and there are growth stocks. Anything from Jumbo to Uber to Meituan Dianping will count as a growth stock, but the returns for each going forward can be very different. And growth stocks by their very nature are unpredictable, because their “growth” basically depends on customers liking their future business model. You can make an educated guess, but you’ll never know for certain how many new customers Uber will get in the next 5 years until it actually happens.

One easy way out, is to just do it via an ETF. This gives you broad exposure to the asset class a whole, and you can then add in one or two stocks that you really like. But of course, the returns will not be as amazing as if you pick a couple of stocks, and turn out to be spot on in your picks.

Picking the right geography – Increasingly, there’s starting to be a split between the western, US based tech companies, and the newer Chinese based tech companies. As we go forward, I expect this distinction to become more pronounced. The rise of China is another defining theme of this century, and picking the right geography to allocate to can have huge implications on future returns.

Which Stocks would I Pick?

Anyway, as a simple thought exercise, I also wanted to imagine how I would construct such a portfolio if I were a beginner investor today. I set a couple of ground rules for myself:

- 5 stocks maximum – As a beginner investor, I wouldn’t have a large amount of funds. Ideally, the number of stocks should be kept to a minimum to minimise transaction costs like brokerage fees. Having less stocks also makes it easier to monitor the portfolio and rebalance.

- Minimal intervention required – Not everybody wants to look at their portfolio everyday. As a beginner investor, my goal is really to build up financial knowledge while also working on my career and growing professionally. The investment portfolio shouldn’t become a full time job.

Here are my 5 picks, split into the “Yield” and “Growth” barbell:

Yield Barbell

Mapletree Commercial Trust –MCT has had a huge run-up recently and is now trading at a 4.9% yield. But if there were only one REIT I could own, MCT would still be very high up on my list. I wrote about MCT many times in the past, and I still love this REIT for the great sponsor, the great exposure to Singapore retail, office and business parks, and the fantastic growth pipeline (MBC Phase II).

There could be some price volatility going forward, but as a yield play, I think the distribution is as solid as it gets.

Netlink Trust – Even after the recent run-up, Netlink is still trading at about a 5.5% forward yield, which is pretty decent. I wrote about Netlink in the past, and I just don’t see any material disruptions to the business model moving forward. 5G is coming online soon, but 5G isn’t going to replace Fibre for home connections, and a lot of 5G networks will need to run off a fibre backend.

DBS Bank Ltd – This one’s quite a controversial one, so if you’re risk adverse, feel free to skip it. But I included DBS because it’s trading at a nice 4.4% yield, and it gives you broad exposure to the financial services industry. Also, no Singapore portfolio is complete without exposure to at least one bank. It trades at 1.4 times book value now so it’s definitely not cheap, but out of the 3 local banks, DBS is my pick for their digitisation efforts.

Growth Barbell

NASDAQ ETF (QQQ) – This is an ETF that tracks the NASDAQ 100, which includes companies like Apple, Amazon, Microsoft, Facebook etc. This gives you broad exposure to the tech space in the US.

S&P500 (SPY) – I also included the S&P500 for greater flexibility. This is an ETF that tracks the S&P500, which are the 500 largest companies by market capitalisation in the US. It’s less volatile than the Nasdaq ETF, so potential returns are lower, but if you don’t want to take on so much risk, S&P500 is a good choice.

With these 5 stocks, I can then play around with the asset allocation to achieve my desired balance between growth and yield. My personal portfolio is probably in the range of 60% yield 40% growth, but feel free to mix it up as you like based on your risk profile. Of course, if you’re a more advanced investor, you’ll probably add in even more stocks, and have a total portfolio consisting of 10 to 15 stocks.

Closing Thoughts: How does this compare vs the All Weather Portfolio?

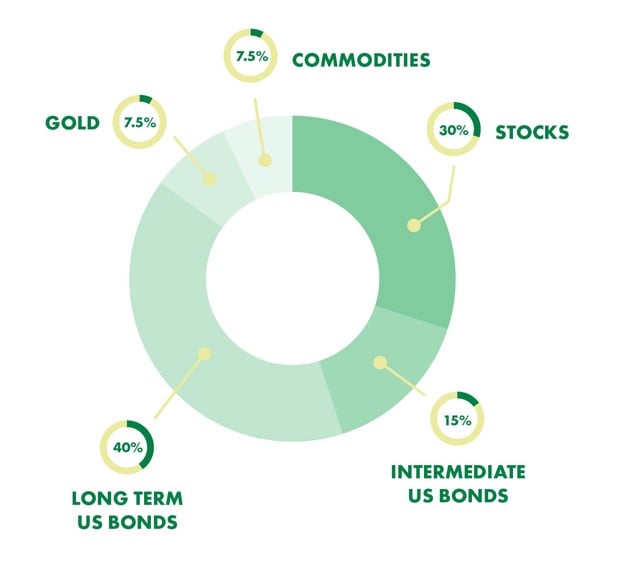

I wrote about Ray Dalio’s All Weather Portfolio as an asset allocation tool in the past. The broad allocation is set out below.

The way I see it, these two strategies are actually complementary. The All Weather Portfolio teaches you how to organise your entire net worth holistically. The “Barbell” strategy teaches you how to allocate your stock portfolio specifically (ie. the 30% portion in the picture above).

For Singapore investors using the All Weather Portfolio, Intermediate US Bonds can be replaced with Singapore Savings Bonds, and Long Term US Bonds can be replaced with CPF-OA or CPF-SA. Unfortunately, the All Weather Portfolio doesn’t factor in property, which is something you’ll need to do if you’re a Singaporean (because all Singaporeans own property right?). I’m still collecting my thoughts on how property affects asset allocation, so that’s an article for another day! If you have any thoughts, I’d love to hear them below.

Leaving all that aside, I do believe that if you pair the All Weather Portfolio with the Barbell strategy, you’ve like got a great starting point from which you can allocate your net worth as a Singaporean.

Till next time, Financial Horse, signing out!

Enjoyed this article? Do consider supporting us and receiving additional exclusive content. Big shoutout to all Patrons for their generous support, and in helping keep this site going!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Great article. Coincidentally I was designing the same. I had a heavy SG and EU exposure. So readjusting. Also yields are tax free in SG and capital gains are tax fee whether you accrue it in the US or in Singapore.

Which Chinese ETF or Chinese Tech ETF would you recommend and why.

Thanks for your advice.

I’m new to investment, do you think it is recommended to invest my investable amount quaterly in just the 5 picks you mentioned over a 30 years period? With 20% amount going into each picks.

30 years is a long time. I think the 5 above are great for the next few years, but over time things change so the individual stock picks may be less relevant if the business case changes.

The S&P500 and Nasdaq100 are probably good for 30 years though, because the index refreshes itself over time according to market capitalisation.

Yes great point. The tax regime also favours this approach as well, for the reasons you mentioned.

Unfortunately I haven’t located a Chinese ETF I really like. The Hang Seng doesn’t give strong exposure to China A shares, and something like the China A50 index will have really high management fee (70 bps). I’ve primarily played China through China proxies thus far, things like Hang Seng, US listed China stocks like Alibaba, or Singapore listed companies with strong exposure to China.

[…] Given how the trade war has escalated once again and the STI is headed back to 3100, opportunities should start emerging in the market place. As you may know, I’ve shifted my investment strategy from an all growth no yield strategy last year to a half yield half growth strategy as part of my hope to reduce the volatility of my portfolio. What I didn’t know was that this is referred to as a “barbell strategy”. You can read more about this strategy from this article by Financial Horse. […]

I understand that the DBS Barbell Strategy is a flop after its launch. It is flat. And market is volatile and is up 6 percent. It is hardly a good idea. But a sales gimmick.

Haha I think the underlying idea is sound, it’s just about timing and execution. 🙂

“For the Jun-97 to Jun-03 period, average monthly returns for the S&P 500 was 0.3% while average returns for the “barbell portfolio” was 0.7%. On a cumulative basis, the S&P 500 gained 14.9% during the period while the “barbell portfolio” surged 41.1%, constituting an outperformance of 26.2 percentage points”

I suppose the bank DBS purposely research and fit the time. One should be honest, and set from June 1997 to latest period. I am too suspicious of such style. I believe in investing in established fund managers not a bank

I receive the bank’s idea, no comparison to timing. It is not said timing is that important.

Haha thanks for sharing your thoughts, I guess there is a bit of “fitting” of the data here. But objectively speaking, I do think the underlying concept of having a growth + dividend portfolio is sound, because it is a mix of fast growing businesses (growth) together with more mature businesses (dividend), which gives you good exposure to the economy.

The devil as always, is in the details, and things like execution and timing are important as well.

I must thank the commentators that highlighted the pitfall of investing in the DBS Barbell idea. My colleague yesterday cut at 20% loss…. After the DBS High Notes saga, oil & gas saga, you can’t trust DBS especially they have the worst CIO in town. Do own research & don’t trust their investment counsellors!

I think the core theory is sound, it’s the execution that will make or break the performance. Apply the underlying theory, but pick your own stocks to form the barbell. I’m doing that and the performance has been good.

Financial Horse can you show us how the Barbell worked for you? Did you make money on this crash? I am actually skeptical. I follow your blog closely, no comments until now. I agree with some of the commentators. The current DBS CIO is inferior to the former one. Lucky for me, I exit the market last December. Miss a bit but miss the current crash!!!!!!!

Hi Angie,

Good to hear from a long time reader! 🙂

I think the key about Barbell is to understand the underlying strategy – that in a secular low growth environment, the key areas that will do well are growth and yield. That’s all the Barbell strategy is.

I agree that DBS’s execution of the strategy is flawed. For me personally, I used US stocks for growth exposure, and Singapore stocks or REITs for yield.

And this barbell was only the equity portion of my portfolio. I also layered it with bonds, cash, gold, real estate etc to create a balanced portfolio.

So yes, I think the idea is sound, but the execution needs to be well thought out.

My full portfolio breakdown is available on Patron if you’re interested! 🙂

https://www.patreon.com/financialhorse

Hope this helps!

Hi FH,

Thanks, always enjoy reading your articles.

I am fairly comfortable in deciding my allocation across asset classes, but have some trouble within asset classes. For example, within stocks, what is a systematic process to decide how much should be allocated to each geography?

Great question, we actually built an entire lesson in the REITs Masterclass on this haha.

I would say look at:

1) Risk appetite – more to EM if you’re high risk

2) Level of knowledge – favour those you have strong informational advantage

3) Stage of macro cycle – macro matters, eg. for now we’re probably seeing inflationary busts in EM (esp commodities exposed) play out over 2020, so less to those etc

It’s not a tick the checkbox kind of exercise. I would say look at the 3 factors above, and decide what works for your own investing situation. Everybody’s answer is unique.