A month or two back, I wrote an article on the Top 5 Stocks / REITs on my watchlist for 2020. Of the 5 stocks, one was SBS Transit.

It generated a lot of great discussion at the time, and the ultimate conclusion reached was that SBS Transit could be a good stock – at the right price.

So in this article, I wanted to do a deeper dive into SBS Transit.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything. Sign up below (you get a free guide when you sign up):

Basics: What is SBS Transit

SBS Transit makes money in 3 ways:

- Bus Services (Basic Bus Services • Chinatown Direct Bus Services Express Bus Services • Nite Owl Bus Services City Direct Bus Services)

- Rail Services (• North East Line • Downtown Line • Sengkang Light Rail Transit System Punggol Light Rail Transit System)

- Other Services (Advertising Services (those billboards you see in the MRT station and on buses) and leases of space at the station)

And that’s really all there is to it.

It’s a simple, easy to understand, old school business. This is the kind of company that your textbook corporate finance and valuations work on, not those new world stuff like Facebook and Tencent.

There are a couple of nuances to SBS Transit that we need to cover to fully understand the business

Bus Contracting Model

The rail service is straightforward. SBS Transit runs the North East List and Downtown Line, and it makes money from the fares paid by commuters.

Buses though, operate on a Bus Contracting Model that came into force in 2016.

Today has a good summary on this:

Under the model, operators bid for a package of routes through competitive tendering. The Government owns all fixed and operating assets and retains fare revenue while bus operators earn a fee for running services.

Bus operators also have to meet service standards set by the Land Transport Authority (LTA).

This is a departure from the previous privatised model where operating assets, such as depots and buses, were owned by both the Government and the two incumbent operators, SBS Transit (SBST) and SMRT.

The bus operators kept all the fare revenue which they used to pay for operations and operating assets.

This model, said the Government, did not incentivise operators to expand their capacity ahead of demand or improve service levels.

So the old system was like rail, where SBS Transit owns the bus, and it makes money from the fares. But this system created poor service standards, because operators were incentivized to provide the minimum level of service to maximise profits.

Under the new Bus Contracting Model, SBS Transit will be paid a flat fee for each bus service run, with incentive fees if it meets certain standards. All the fares collected by SBS Transit will then be paid to LTA. This way, SBS Transit can focus on providing the level of standard required by LTA at the minimum cost possible to maximise profits, and consumers benefit because a certain minimum level of service is guaranteed.

The Bus Contracting Model is key, because before this, SBS Transit was generating negative free cash flow. After it came into force in 2016, everything changed, leading to the “modern era” where SBS Transit is now viewed as a cash generating monster.

Commercial Sensitivities surrounding operational metrics

This was discussed at one of the AGMs:

Before opening the floor for questions at the 2019 SBS Transit AGM, Chairman Lim Jit Poh reminded shareholders not to ask questions related to the breakdown of revenue by rail or bus; the management does not disclose the details due to commercial sensitivity. SBS Transit has to bid for bus tenders under the new bus contracting model (BCM) and publishing their operating margins may give clues to how much the company could bid for their next contract. Therefore, the information is deemed to be highly sensitive. By keeping their margins confidential, this helped SBS Transit win two out of four contracts at the first open tender exercise when the BCM came into effect.

So unfortunately, we’re not able to see margin or revenue breakdown by rail or bus segments because it is commercially sensitive.

60% Market Share for Bus

Taken from the Fifth Person:

SBS Transit has around 60% market share in Singapore from running nine out of 14 bus packages in 2018.

These made up 222 bus services with a total fleet size of 3,417 buses, an increase of 225 buses from the year before. The company employs around 6,600 bus captains to run the bus services. SMRT is the second largest bus operator in Singapore with market share of around 25%. The other two bus operators, Tower Transit and Go-Ahead (both UK-based), split the remaining market share with approximately 8% and 7% respectively. According to CEO Yang Ban Seng, market share is estimated using the total number of bus services in Singapore.

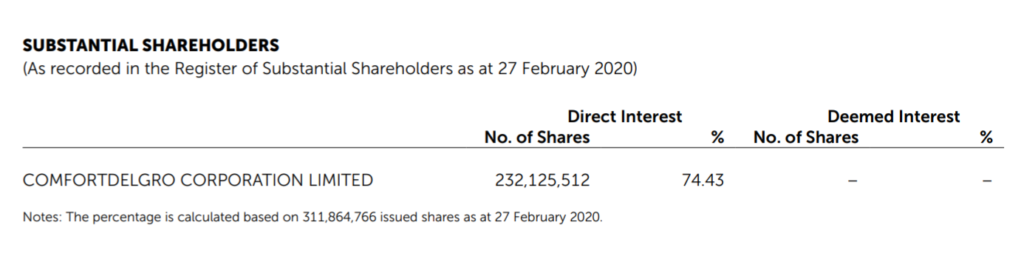

Shareholder

The largest shareholder is Comfort Delgro which owns about a 75% stake.

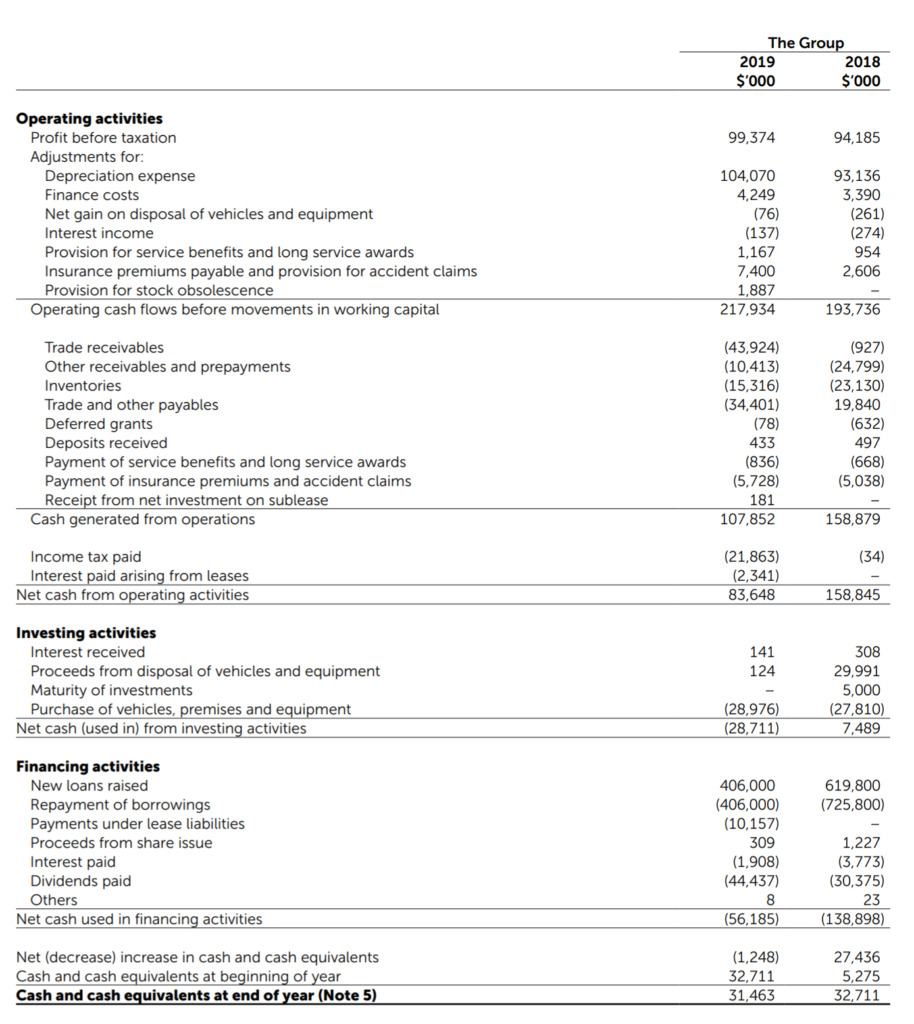

Financial Statements

A quick look at the latest Financial Statements:

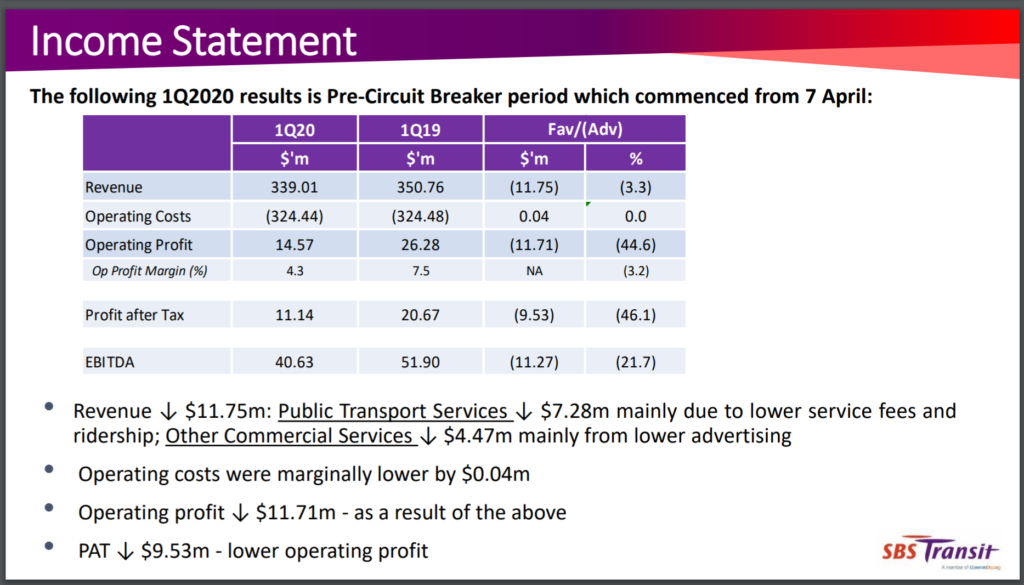

Income Statement

Q1 Revenue (Jan to March 2020) saw a 3.3% drop in revenue, and a 44.6% drop in operating profit. This shows how tight the business is – profit margins are measured in single digits. A small drop in revenue can trigger a massive fall in profits.

This was before the circuit breaker, so Q2 is going to print a massive loss, but it will gradually recover from Q3 onwards.

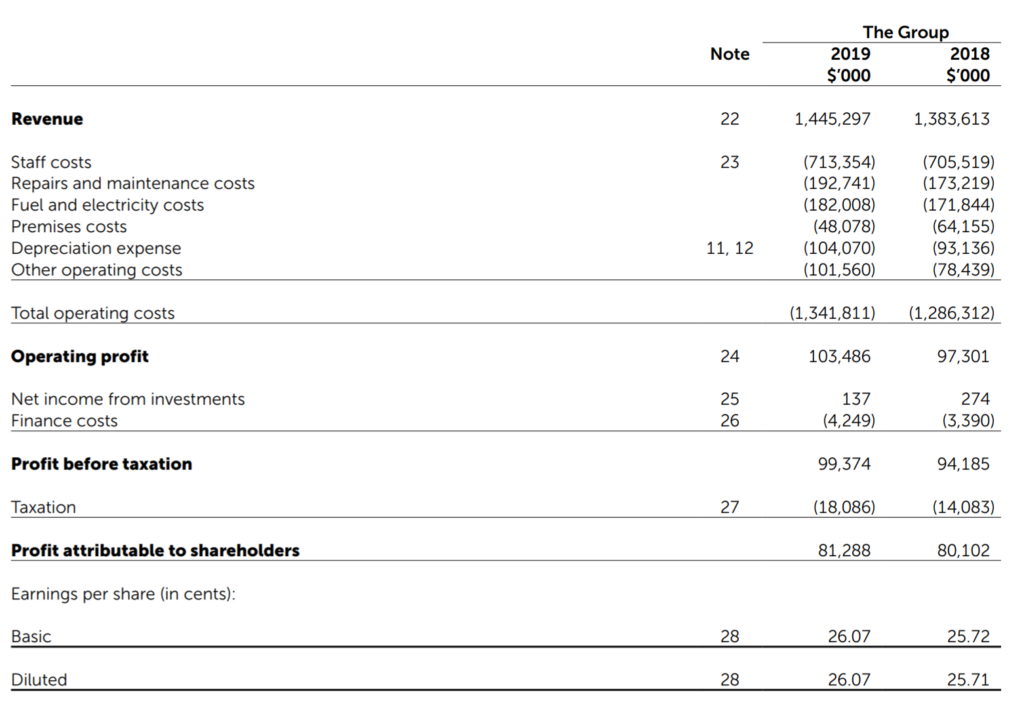

2019 and 2018 income statement shows that stabilized profit before taxation before COVID19 is around $95 to $99 million range. After tax is approximately $80 million.

Balance Sheet + Cash Flow

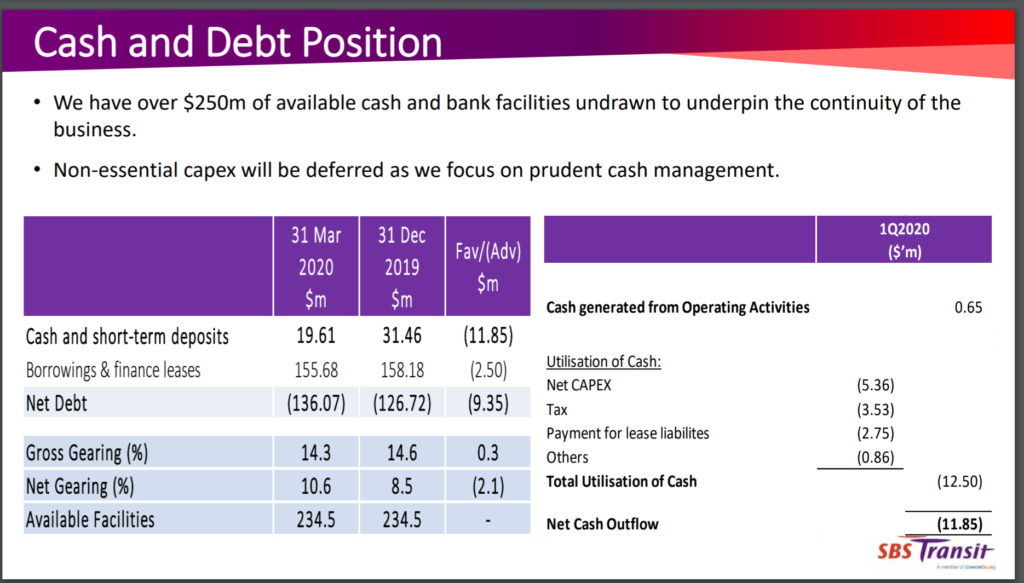

Source: COVID19 Update from SBS Transit

Current net gearing is a low 10.6%, and there are $250 of cash and committed bank facilities that can be tapped on.

Net cash outflow in Q1 was approximately $12 million, and capex will be cut going forward to cut down on cash burn. If we assume conservatively $15 million cash burn a quarter, that still another 16 quarters worth of cash, so solvency shouldn’t be a big issue for SBS Transit.

Valuations and Dividend Yield

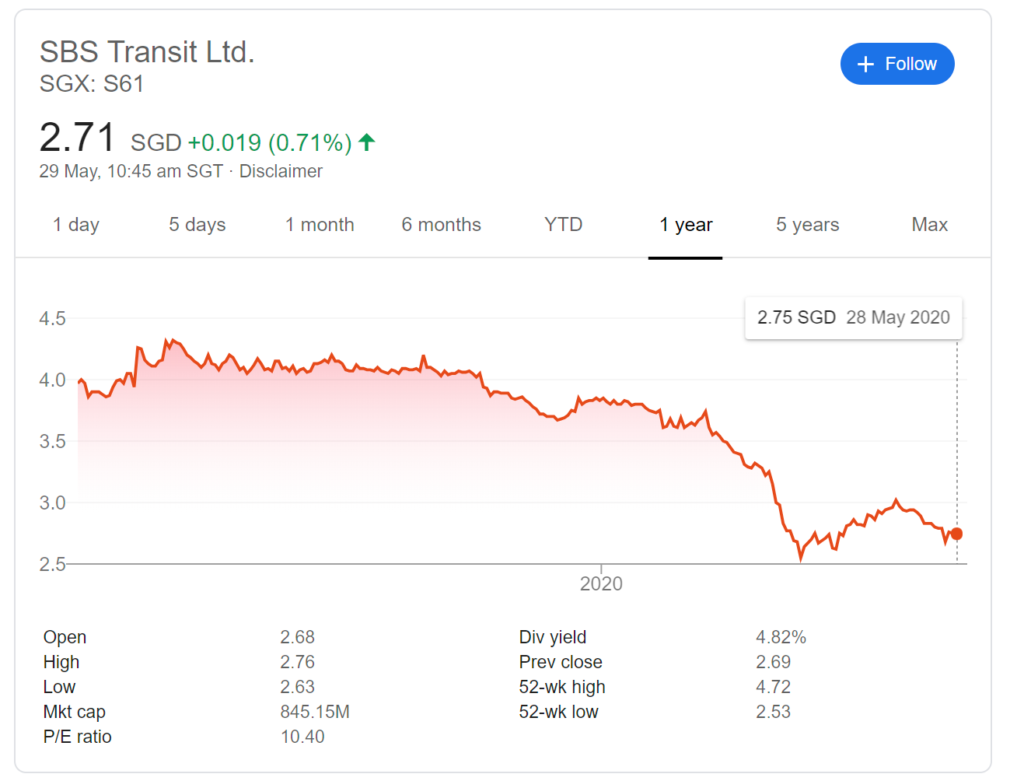

Note: Calculations are based on share price on 29 May 2020 of $2.69

Valuations are really tough to run because we have no idea what earnings will look like going forward. 2020 is going to be a completely meaningless year, so we’ll just skip it entirely and look at 2021.

Stabilised earnings last year was $80 million, so if we assume a 20% drop in earnings to about $64 million, that gives us 13 times P/E.

Management has committed to a 50% payout ratio, so that’s a $32 million in dividend payout, works out to 10.24 cents per share, a 3.8% yield for 2021.

I wanted to test if there’s any way to increase the payout ratio, and it doesn’t look so straightforward because of the capex expenditure. In 2018 and 2019, capex took up approximately $28 million a year in cashflow.

If we kept this capex, and assume the same 20% drop in earnings, that leaves around $36 million a year in cash. If management paid out 90% of that cash flow, that works out to a 32.4 million, which isn’t much more than the 32 million (based on a 50% payout ratio) we modelled above.

The crux of the issue then, is that earnings is key. If we’re going to see a 20% drop in earnings in 2021, then the company just isn’t a great investment.

But if 2021 can match 2019 in earnings, that’s $80 million profit after tax, $40 million in dividends, and a 4.75% yield, with spare cash left over.

How stable are earnings in 2021?

So the 2021 earnings are going to be critical to set the stage going forward.

But hand to my heart, there is absolutely no way I can think of to give an accurate estimate of 2021 earnings. Any kind of estimate will require a judgment on what the government does, and the status of COVID19 next year, which could just turn out to be completely wrong.

Q1 2020 was before the circuit breaker, but it had a bit of overhang from COVID19 in China where people cut down their travel. And Q1 saw a 3.3% drop in venue and 46% drop in profits. If this holds true in 2021, that 46% drop in profit is way more aggressive than the 20% drop we’ve modelled above to get the 3.8% yield.

Whichever way you look at it, there’s just going to be a lot of uncertainty about 2021’s earnings.

Offline Advertising and Leasing

I’m also pretty wary about the “Other Services” of Offline Advertising and Leasing of spaces at the stations. Short term, there’s just going to be big headwinds for both.

Lots of reports about offline ad spending migrating to online ad spend, and we all know how retail leases are going to play out this year.

How stable are earnings in the longer term?

So that’s the short term. Longer term, there are 2 main threats: Changes to the Bus Contracting Model, and competition from other bus operators.

Changes to Bus Contracting Model

Today has a good analysis on the Bus Contracting Model:

One year into the model’s implementation, operating expenditure for buses alone, which consists of the contract with the winning bus company as well as the upkeep of assets among others, was S$979 million.

The expenditure was supported by S$423 million in grants, as well as S$513 million in operating income.

Since then though, the operating expenditure for buses has shot up to S$1.925 billion. Of this, government grants made up S$1.024 billion while fare revenue rose to S$834 million.

This essentially means that less than half of the operations for buses here are supported by revenues from fares, with the majority coming from Government subsidies instead.

With public transport ridership increasing at a pace of about one to two per cent each year over the last four years, fare revenue collected has not increased in tandem with operating expenditure of buses.

This makes sense in a way.

Public transport fares are too low to maintain the current service levels if left to market forces, so the Bus Contracting Model allows LTA to “subsidize” public transport while allowing market forces to improve efficiency.

It’s a really good model, and personally, I don’t see big changes going forward. It’s a really good balance between maintaining service levels and keeping market forces in play.

Competition

There are 4 bus operators in Singapore: Tower Transit, Go-Ahead, SBS Transit and SMRT.

SBS Transit holds about 60% of the market, so any gain in market share by the others will be a drop in earnings for SBS Transit.

The contracts are for 5 years each, and some are coming due in 2021, so this is another threat.

The rail business has far less competition of course, but unfortunately we don’t know the breakdown between rail and buses.

Putting it all together

So in SBS Transit, we have an operator that runs North East Line and Downtown Line, and about 60% of the bus services in Singapore, and sells ads on all of them, and leases out some space in the stations.

We have a big question mark as to earnings over the next 1 to 2 years.

We have uncertainty over earnings in the longer term due to competition for bus contracts.

And we also don’t have significant capital gains because most of the assets owned by SBS Transit are depreciating in nature (eg. Buses) – unlike REITs.

And the million dollar question then – what price would SBS Transit be attractive?

The share price has already dropped about 30% from its high of $4, and there’s some longer term support at the $2.5 range.

At the $2.5 range, a 20% drop in earnings is a 4% yield, and a full recovery to 2019 earnings will work out to a 5% yield.

That’s actually not super attractive, given all the uncertainties in play. Netlink trust trades at a 5% yield now, for a lot less uncertainty. And with a blue chip REIT you can get maybe 4+% yield, but good potential for capital gains down the road.

So in a way, I don’t see SBS Transit as a compelling buy at the current price. At this price, there really isn’t a sufficient margin of safety to compensate me for the risk being taken on, especially with all the uncertainty over COVID19 recovery.

But we still have a long way to go in this crisis, and as earnings continue to fall as 2020 plays out, I wouldn’t be surprised to see SBS Transit continue to drop.

And at some point, if it drops enough, it could become a compelling buy.

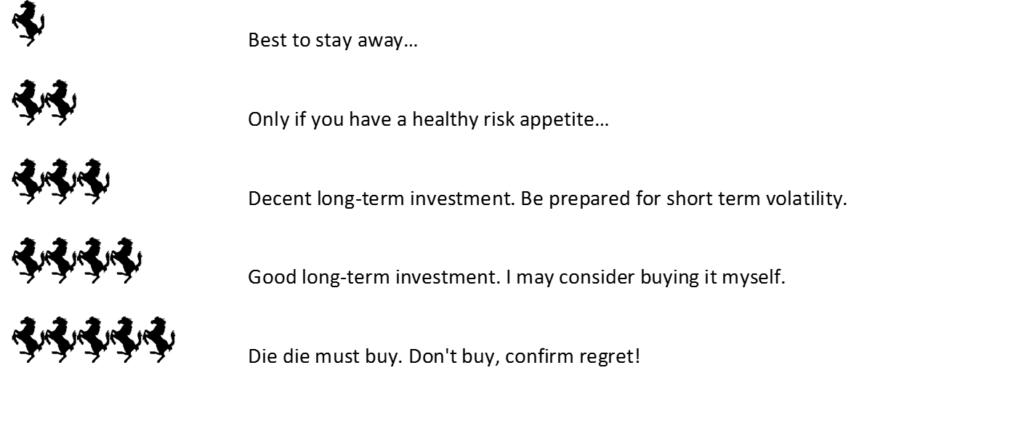

I’ll give SBS Transit a 3 Horse rating at its current price. It’s a decent stock, but because of all the uncertainties in play, and short term headwinds, it’s just not an amazing buy right now. But I’ll definitely be watching this closely going forward.

As a reminder, this article is written on 29 May 2020 and will not be updated going forward. My updated thoughts (and personal stock watchlist) are available on Patron.

SBS Transit – Financial Horse Rating (3 Horses)

Financial Horse Rating Scale

Share your comments below!

Support the site as a Patron and get market and stock watch updates.

Do like and follow our Facebook Page. We share great links and infographics there.

Join our Facebook Group to continue the discussion, we have a great community of investors who want to help each other become better investors. Everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Hey FH. Good article overall. You just need to factor in the DTL licence charge and your analysis will be complete. The fixed charge started in 2019 and increases by S$5m p.a. The variable charge is unlikely to come in until the DTL turns profitable, which is probably… a long time away.

Thank you for raising this! Appreciated.

Not sure at least in the near term, how covid 19 will change the capacity of public transport ? Reduced capacity = reduce revenue, perhaps for pple who are wary of the virus, will choose not to crowd out in public transport.

Just a hypothesis, Im just thinking will some people buy cars instead for transportation ? ( since the car industry is badly affected by the crisis, and maybe car prices / coe will plunge ? Pple who bought cars in 2009 when coe plunge, didnt lose much at all for private cars. Those with cars already, may also choose to renew coe , given the dire economic conditions here.

More private , less chances of transmission of disease.

Im actually thinking Vicom might be a good alternative defensive stock as well, and has very good dividends as well. Monopoly business, with high level barriers of entry for competitors and has a big market share as well.

Will you be considering doing an article on Vicom ?

It really posted way better financial results than sbs transit and comfort delgro.

One of the interesting lessons from China was that after lockdowns lifted, people went out to buy cars, because they were afraid of public transport!

It’s different in Singapore though, because of the cost of a car, and COE artificially restricts the supply of cars.

I probably won’t do on Vicom, but I might do one on Comfort Delgro.

SBS’ public transport capacity will return to 100% going into June. Since the public scheduled buses are on the BCM framework, they do not have fare box risk and hence earnings are independent of ridership. Unless of course, you foresee LTA reducing service frequencies as a result of more people working from home. Only then will the service fees for buses decline. It’s the Rail business that has fare box risk, whose earnings will be impacted by lower ridership. Not that it makes money anyway. That said, the government has stated it is looking to revise the current rail framework, which could see positives emerge. The losses on DTL are substantial and reduced SBS’ bus net profit by about one-third if you use 2018 as reference. So what you see on the headline is after losses from rail. Imagine if you reduce those losses to zero…

VICOM looks ok for now, but don’t forget that slightly over half of the business comes from non-vehicle testing. It’s a segment that people often forget about. That segment will likely take a hit in coming quarters, as flagged in their trading update. They have clients in the Aerospace, Oil & Gas and Construction sector, all of which suffered lower activity in 2Q20. So, you should expect non-vehicle earnings to come off going into 2Q20 and then mirror the economic recovery going into 2H20.

Yeah I agree that the rail business is the big question market. Unfortunately we don’t know what the breakdown between the two are like. I think either way, there are near term headwinds at least for the rest of this year, but 2021 onwards perhaps we may see a recovery.

So it really all goes back to pricing again.

NEL is also in the red.

These single stock / investment posts are great! Been awhile since the FH rating was last seen!

Haha will try to do more of these going forward then! 🙂