Singaporeans love dividend stocks.

Myself included.

There’s nothing we love more than a stock that pays you a steady dividend every year, and slowly appreciates in price over time.

It’s the holy grail in Singaporean investing.

COVID-19 has decimated this industry as many companies have slashed their dividends, but I think there are still gems to be found.

In this article, let’s look at the Top 5 Singapore dividend stocks that will yield more than your CPF.

Rules for picking Singapore Dividend Stocks

Couple of rules to frame the discussion:

- Yield more than 2.5% – The yield has to be higher than CPF-OA at 2.5%.

- Stable yield – The focus is the dividend, so we want stocks where the dividend is stable and well supported by cash flows, and where there is little risk of a dividend cut.

- Capital gains ideally (or at least price stability) – The icing on the cake, will be if we can get dividend yield, and also capital gains. However, between the two, we’ll prioritize a stable yield, and capital gains is a bonus.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything.

Don’t forget also to join our Telegram Channel!

[mailmunch-form id=”928667″]

1. Netlink Trust

I first bought Netlink Trust back in 2018 and this stock has done really well for me since. I get that its not a company but a business trust, but the characteristics of the business are so close to a dividend stock that I thought it was apt to include it.

Netlink Trust owns the Fibre Networks in Singapore.

Each time we set up a new fibre connection for a new house, we have to pay an initial set up fee to Netlink. And of the $40 a month we may pay to Singtel, Singtel pay about $17 to Netlink Trust to “rent” the usage of the fibre network.

Dividend Yield Stability

That’s really as stable as it gets in this climate.

If the COVID recession gets really bad, you’ll cut back on your spending, but you’ll never cut back on the internet fee. In 2020, the internet connection has become like electricity or water.

Competition wise there’s unlikely to be a real threat, because the capex required to build an alternative fibre network to cover the whole of Singapore is too prohibitive.

5G is coming into play, but I see 5G as more for mobile devices, while home Wifi will still ride on fibre networks. And don’t forget that much of the 5G cell towers rides on a fibre backend as well, so this could actually be a tailwind for Netlink.

One thing to note is that the typical accounting life of the Fibre itself is 25 years, but according to Netlink they can last far longer – up to 50 years. Their repair and maintenance costs have been going up of late though, so perhaps the fibre requires more maintenance than expected. If so, this could materially impact yield, and is worth monitoring going forward.

Potential for Capital Gains

The problem though, is that there’s just not much growth in the business. The prices are regulated by IMDA (reviewed every 5 years), and it’s not in IMDA’s interests to ensure Netlink has good profits.

Longer term, growth will have to come from population growth – because with more people in Singapore, that’s more people to sign up for a fibre connection.

That said, I think there is the potential of capital loss for a stock like this. If the reflation trade starts to play out, and investors start betting on a big economic recovery, a stock like Netlink isn’t exactly the kind of stuff you want to own.

You’ll want to be owning the deep cyclicals that have sold off massively – the banks, energy, industrials, real estate. And I can see investors selling off stable yield plays like Netlink to buy cyclicals.

Rounding it up

At 5.1%, the yield on Netlink Trust is the highest on this list. It is also very stable, and I don’t see a big risk of a dividend cut.

But there’s not much growth in the business to be honest, and there is a risk of capital loss if the reflation trade starts to play out.

Could be perfect for certain kinds of income investors though.

Price: $0.975

Yield: 5.1%

Yield Stability – Good

Capital Gains potential (Long Term) – Low, with possibility of capital loss

2. CapitaLand

CapitaLand is an interesting stock where you either love it or you hate it.

Some people love holding property developers, while others swear by REITs. It’s a personal choice really, I don’t think there’s a right or wrong here.

Either way, CapitaLand holds very high-quality real estate, with 80% of the portfolio concentrated in 2 key markets: China and Singapore.

Post Ascendas acquisition, CapitaLand holds almost all asset classes – retail, hospitality, office, business park, data centers. And big stakes in all the REITs we know and love – CCT, CMT, CRCT, Ascendas REIT, Ascott REIT.

And it’s 51% Temasek owned.

What more do you want?

Dividend Yield Stability

It currently yields 4.3% at a 46.5% payout ratio.

Short term, cash flow and earnings are definitely impacted because of COVID-19, and the impact on rentals.

But a 46% payout ratio is nowhere near the 80% levels that companies like Singtel is pushing. 46% to me is more sustainable, and provides some headroom to buffer against the declining earnings.

The portfolio is also concentrated in Singapore and China, both of which are weathering the COVID crisis better than Europe or the US.

For now, I think the dividend is safe, barring of course a prolonged COVID recession.

Potential for Capital Gains

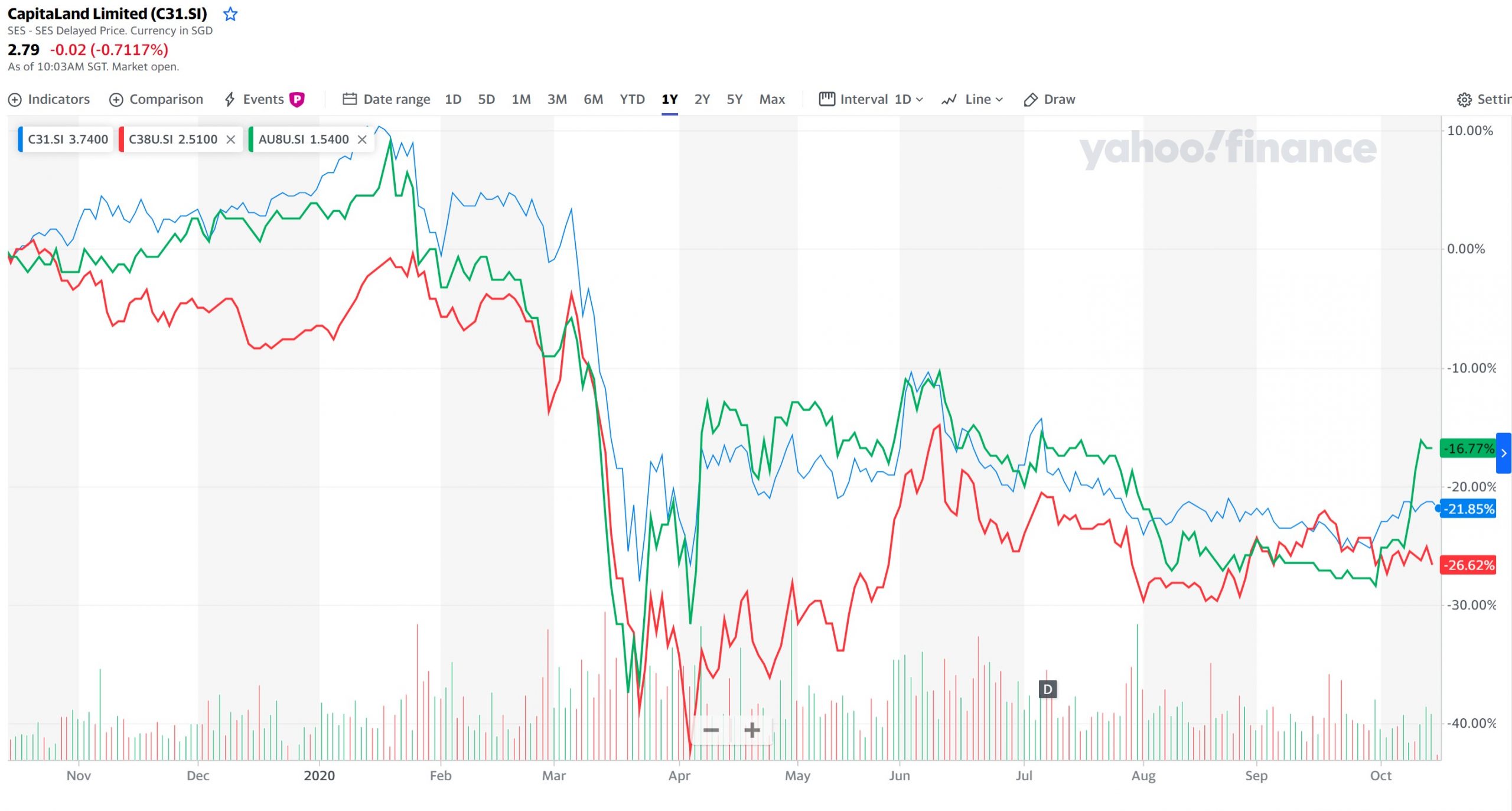

I’ve plotted CapitaLand’s share price (blue) against CMT (red) and CRCT (green) above.

Stock is down about 20% over the past year, in between CMT and CRCT.

At current price though, it trades at a 0.57x book value. Even in the good times, the stock trades at a 20% discount to book because of the conglomerate discount. It’s this concept where if you put too many businesses together, the stock market doesn’t value the sum as much as it views the individual parts.

CapitaLand suffers from this, so even if COVID goes away tomorrow, we’re probably looking at a 20-30% recovery in price tops.

Rounding it up

That said, the real estate is very high quality, and concentrated in Singapore and China, both of which are weathering the COVID crisis comparatively well.

Because of that I think the dividend should be safe, but it is definitely not ironclad.

I do like the potential of capital gains as well, given the high-quality real estate portfolio in play. As discussed previously, I think the next phase of the crisis (once we get through the insolvencies) will be inflationary, and I think high quality commercial real estate will perform well in such a scenario.

Price: $2.77

Yield: 4.3%

Payout Ratio 46.5%

Yield Stability – Average

Capital Gains potential (Long Term) – Good

3, 4, 5. DBS / UOB/ OCBC

I don’t think any Singaporean dividend investor can have a complete portfolio without an allocation to at least one of the 3 local banks.

Very stable businesses, in a very regulated environment. It’s about the cleanest way to bet on Singapore’s longer term economic growth.

Dividend Yield Stability

Post MAS dividend caps, the banks are sitting at about a 33% payout ratio, which is ridiculously low – even below that of CapitaLand.

We did a in depth analysis of DBS recently, and we found that the core business is still raking it in, which makes this kind of payout ratio look overly conservative.

In any case, current yield works out to about 3.4%, with very little risk of it being cut further unless we have a prolonged recession.

The government seems very committed to injecting fiscal stimulus to prop up the economy though. If that’s the case, it’ll be even better news for the banks because non-performing loans will stay low.

Potential for Capital Gains

I like the long-term prospects of the Singapore banks, especially at these prices.

Very cheap on a historical basis.

The problem of course, is that cheap can get cheaper.

Short term, I don’t think COVID is over just yet, so I do expect volatility in the share prices.

But longer term, the banks are really just about getting broad exposure to the Singapore economy, and if the Singapore economy does well, the banks should do well too.

One wildcard is the rise of the digital banks. I shared some thoughts on this in my DBS article, but the gist is that I am cautiously optimistic for the local banks – I think it’s harder to disrupt this business than one may expect.

Rounding it up

It’s a very solid business, in a very regulated climate, in an economy that I am pretty bullish longer term (Singapore).

There’s a lot to like about that.

At this kind of payout ratios, the dividend is likely to be incredibly stable, with very little risk of a cut unless there is a prolonged recession.

DBS:

Price: $21.21

Yield: 3.4%

Payout Ratio: 33%

Yield Stability – Good

Capital Gains potential (Long Term) – Good

UOB:

Price: $19.57

Yield: 3.5%

Payout Ratio: 33%

Yield Stability – Good

Capital Gains potential (Long Term) – Good

OCBC:

Price: $8.68

Yield: 3.6%

Payout Ratio: 33%

Yield Stability – Good

Capital Gains potential (Long Term) – Good

Bonus Mention: Big Oil as dividend stock / value play

Big Oil is not listed in Singapore, otherwise they would have likely made the list.

I think the Oil Majors are ridiculously cheap now.

Many of them are trading at 10- or 20-year lows, down 50% or more from their pre-COVID highs.

Now I do agree that the short-term outlook for oil is a complete disaster. Heading into the winter months, oil demand is just going to stay depressed for a while.

But 2 – 3 years out, I think demand will recover once COVID comes under control, and it’s not that easy to replace oil overnight. Most cars and planes still run on oil.

Post dividend cut, Royal Dutch Shell is trading at a 5% yield, and you can actually get RDS.B listed on the LSE with no dividend withholding tax for Singapore based investors. That’s a full 5% yield as you get paid to wait for the recovery. And if it goes back to pre-COVID highs, that’s more than a 100% price increase from here.

In the US, Exxon is trading at a 10% yield now. I think a dividend cut is all but a done deal at this point, but even then it’s still ridiculously cheap. The last time it was this low was in 2010 during the financial crisis.

That said, I do think that the best days for oil and gas may be behind us, so this isn’t a position I would want to be holding too long term. 3 to 5 years down the road, if I get a decent recovery in price, I’ll probably lock in my profits.

Closing Thoughts

To qualify – I think the macro environment we are currently in is incredibly unstable. So many people are just long a handful of tech names, and expecting that to continue the next 10 years. And everyone is short the USD and bonds.

I don’t know how it’s going to play out exactly, but history tells us it’s seldom that straightforward.

For some reason, the start of each new decade always seems to mark a new paradigm shift in investing where what worked in the past decade, no longer works in the new decade. 1990 (recession), 2000 (Asian Financial Crisis and Dot Com), 2010 (Lehman).

COVID in 2020 looks like it will be continuing this trend.

Personally, I think a broad diversified portfolio just makes the most sense for me right now. I definitely do not want to be going 100% long into any one asset class, whether it’s tech (or dividend stocks).

I own some dividend stocks, some tech, some REITs, and of course some gold / cash / bonds (for those who are keen, my full portfolio is available on Patron).

As the future starts to crystallise, I’ll rotate accordingly based on how it’s playing out. If I am right, this broader secular change in investing will not happen overnight, it will happen over years, so there’s no need to overcommit to a position until we see signs of it starting to move.

As always, this article is written on 16 Oct 2020 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

What other dividend stocks do you like? Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Is it right that RDS.B on NYSE is also free from witholding tax?

No you should be hit by withholding tax if you use the NYSE one. Has to be the LSE one.

I am holding RDS.B on NYSE. It is also free from witholding tax

I am not 100% sure on this but I think it depends on the broker you use. I own a Canada stock listed on NYSE, Canada dividend WHT is 25%, but Singapore has tax treaty with Canada such that the WHT I end up paying is 15%. So, in this case the WHT I pay is not the country of the listing (US 30%), nor country of incorporation (CA 25%), but as a Singapore tax resident 15%.

Yeah I agree with this. The broker you use matters a lot, esp their holding structure. So do check with your broker for the definitive answer on withholding tax.

Hi FH,

This is not really related to dividend stocks. But I would love to read your opinion on Wilmar. I suppose this should be quite a much mentioned stock recently, and hope you could do a piece on it. Thank you.

Sure, I will have a look. What makes you interested in Wilmar, just curious? 🙂

all depends on when you buy the socks.

I think there’s alot of interests recently because of its subsidiary YKA’s IPO. I think end of first day of trading last Thursday, YKA market cap was around ¥300B, which works out to be about S$60B. Wilmar owns 90% of YKA but its market cap is only S$27B. I think this is quite interesting.

Hi FH, BP vs Shell, which one is better?

They are very close to be honest, all European Oil majors. There’s a good article here that goes into the differences: https://www.suredividend.com/big-oil-supermajors/

It’s kinda like picking between OCBC/UOB/DBS in my view. Slight differences, but all within the same industry, and stand to benefit from the same tailwinds.

Just sharing my own experience. I own the exact same Canadian stock (listed on NYSE) with both OCBC and Standard Chartered (SCB). The WHT I pay on OCBC is 15%, but on SCB is 25%. My own guess is that OCBC being Singapore bank, my stocks custodied with OCBC probably enjoy the tax treaty and gets 15% WHT; and SCB is not, so I pay the standard canadian WHT rate 25%.

Hi FH, Shell or BP which one is better?

They are very close to be honest, all European Oil majors. There’s a good article here that goes into the differences: https://www.suredividend.com/big-oil-supermajors/

It’s kinda like picking between OCBC/UOB/DBS in my view. Slight differences, but all within the same industry, and stand to benefit from the same tailwinds.

Hi FH, which oil stocks will be more tax-efficient for SGrean?

The LSE listed European Majors. Shell (RDS.B listed on LSE) is one of those. 🙂

Maybe you can do a comparison on all the Oil majors since they are all selling at decade low discount.