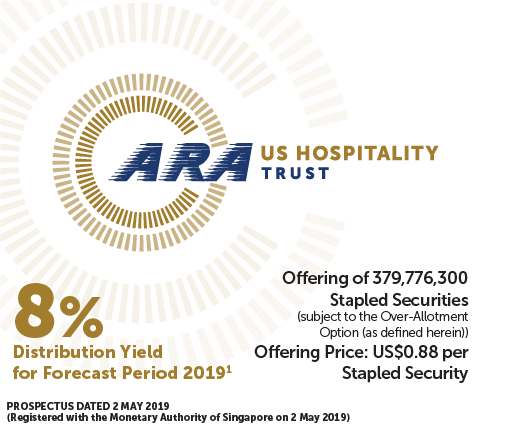

It’s been a while since we had a SGX mainboard IPO, so boy, does it feel good to go through the ARA US Hospitality Trust prospectus.

Basics: ARA US Hospitality Trust

ARA US Hospitality Trust is a stapled trust consisting of ARA Hospitality REIT, and ARA Hospitality Business Trust. It’s a fairly common structure for hospitality REITs, where the REIT component holds the asset, and the business trust component serves as a tenant and operator of last resort, in the event that the REIT can’t find an operator to run it. For ARA US Hospitality Trust, the business trust component is active on day one (so it effectively leases to itself and runs it), but the day to day property management is handled by a third party manager.

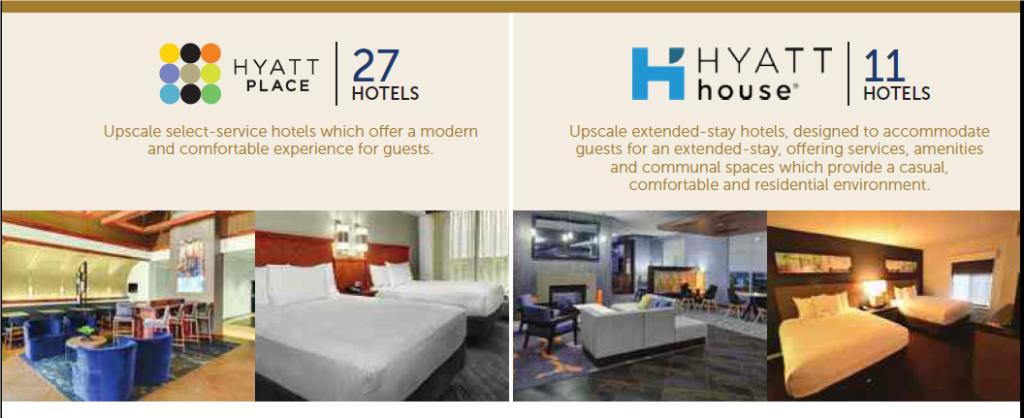

The REIT holds 38 properties in total, 27 from Hyatt Place, 11 from Hyatt House. They’re all part of the Hyatt group, but it’s not the fancy high end Hyatt we’re used it, these are the more mid-range Hyatt hotels.

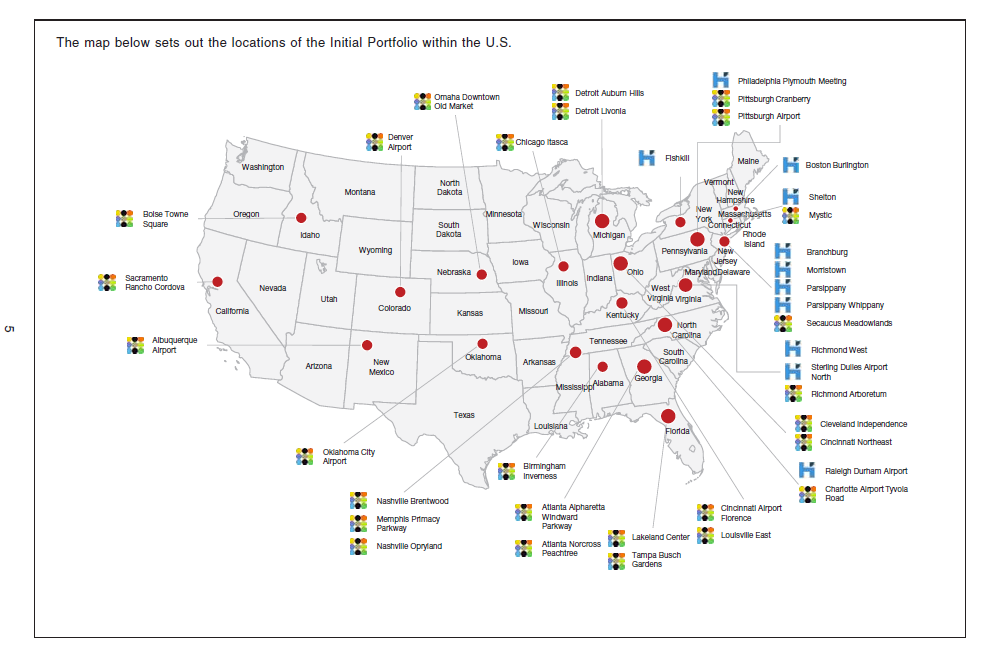

The hotels in question are split all over the US, with a concentration on the East coast.

There’s some interesting bac kground to this portfolio of assets that was dug up by another blogger (Probutterfly):

kground to this portfolio of assets that was dug up by another blogger (Probutterfly):

“These 38 assets were first acquired by ARA Group back in December 2018 from Lone Star, a Dallas-based private equity group for US$700.0mil. Given that the proposed IPO currently values the assets at US$719.5mil, ARA Group would have clocked a gain made a 2.8% gain in 5 months or 6.7% on an annualised basis.

Lone Star in turn had purchased these assets directly from Hyatt Hotels Corp. back in November 2014 for US$590.0mil. As part of the deal, Hyatt will enter into franchise agreements with Lone Star, with all hotels maintaining their existing Hyatt Place and Hyatt House branding.”

So the portfolio in question has changed hands a couple of times in the past few years, and each time it did the valuation has gone up. So we’ll probably want to be extra careful with this REIT, nobody wants to be the last guy caught holding the bag.

For this article, I generally adopted the Financial Horse framework for analysing REITs that I wrote about previously, so do check that out if you want more background.

Valuations

ARA US Hospitality Trust is going to be quite a small-cap REIT when it first lists, in the range of 500 to 600 million SGD. It will be the first pure play US hospitality REIT, so there’s no real comparison on the SGX today. Anyway, I benchmarked it against a couple of other pure US REITs (Keppel KBS US REIT, Manulife) and hospitality REITs (Ascott, CDLHT).

| Yield | Price/NAV | |

| Keppel KBS US REIT | 8.0% | 0.955 |

| Manulife US REIT | 6.7% | 1.07 |

| Ascott Residence Trust | 5.92% | 0.861 |

| CDL Hospitality Trust | 5.75% | 1.05 |

| Eagle Hospitality Trust | 8.0% (Indicative) | 0.91 |

| ARA US Hospitality Trust | 8.0% (Indicative) | 1.02 |

Interestingly, the yield of all 3 US REITs, Keppel KBS US REIT, Eagle Hospitality Trust, and ARA US Hospitality Trust are at an 8 percent yield. Manulife is slightly lower at 6.7%, but to be fair they’re also a fair bit larger in terms of market cap and slightly more diversified. Based on these numbers, it’s hard to draw any conclusions on yield alone.

On Price/NAV, ARA US Hospitality Trust is the highest, with a slight premium to book value, while the other 2 US REITs are all below book value. It looks like they aligned the forecast yield, as opposed to using Price/NAV.

The comparison vs the other hospitality REITs (Ascott and CDLHT) is not a fair one because the latter group is far more diversified and larger in size, so the latter is technically less risky. But they’re useful as a benchmark, and it generally seems there’s a 2% yield premium for this smaller and riskier ARA US Hospitality Trust.

Sponsor

Let’s face it, ARA Realty is not a big player in the US property market. And I’m not saying that as a bad thing, because even the other big boys like Mapletree or CapitaLand are not big players in the US. The US property market is incredibly vibrant and liquid, and unless you’re someone like Blackrock or PGIM, it’s hard to really make a dent.

What this means though, is that there’s not going to be a ready pipeline of assets from the sponsor ready to be injected into ARA US Hospitality Trust. Future growth is likely to come from third party acquisitions.

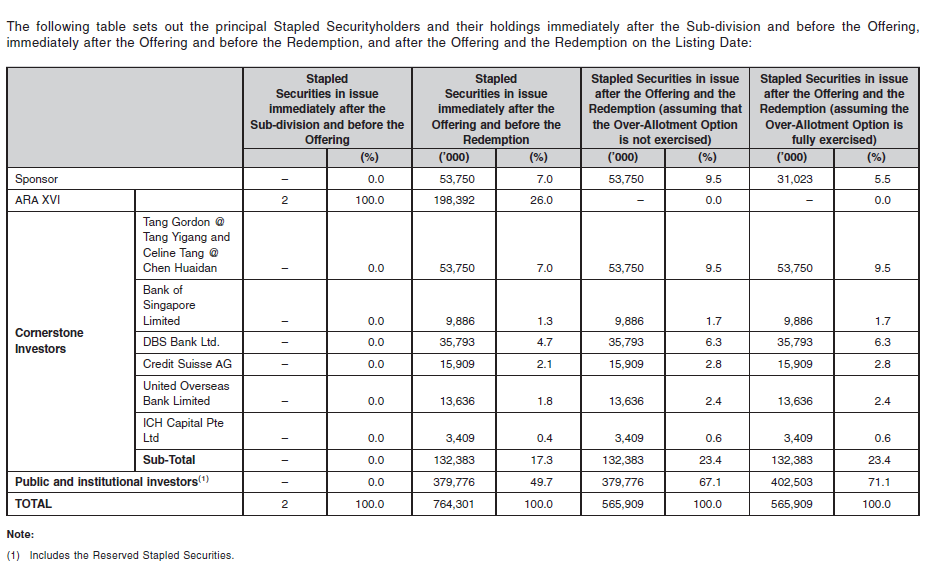

Because of tax reasons, no single unitholder can hold more than 10% of a US REIT, otherwise it destroys the tax transparency status. The result of this is that post listing, the Sponsor is only going to have a small stake of about 9.5% or 5.5%, depending on whether the Over-Allotment is exercised.

I understand why it has to be done in this case (tax transparency), but I still never like it when the Sponsor holds such a small stake post-listing. Despite all the corporate governance in place, it always felt to me that this low stake could raise the possibility of conflicts of interest, because the economic interests of the sponsor and the REIT are as aligned as they would be as if the Sponsor held a 40% take. But to be fair, every US REIT that you buy on the SGX will have the exact same issue, so it’s hard to fault them on this.

The cornerstone investors are also interesting, mainly because there are no big institutional players taking up the cornerstone tranche. You know, the likes of Blackrock or the Norwegian wealth funds. The cornerstones here are mainly private wealth (ie. the private banking clients from the banks). There could be other reasons in play here, but I never like it when there aren’t any big institutional guys taking up a large cornerstone for an IPO.

Because of the small market cap of ARA US Hospitality Trust (500 to 600 million SGD), and because its post listing gearing is going to be around 35%, any future acquisition is likely to be funded by equity offerings. That’s also tricky because with a small REIT like this it can be hard to raise meaningful equity without diluting existing investors (take a look at the Keppel KBS recent offering for an indication of what can go wrong). My gut feel is that if you buy into ARA US Hospitality Trust, you should be prepared to cough up cash for future acquisitions when they do an equity offering.

Book Value

The NAV of ARA US Hospitality Trust on listing will be US$0.86, so at US$0.88 you’re buying in at about a 2.3% premium to book. When you look at the other US REITs on the SGX that are going at below book value, this looks to be slightly on the high side, but I guess they aligned the forecast yield instead of book value.

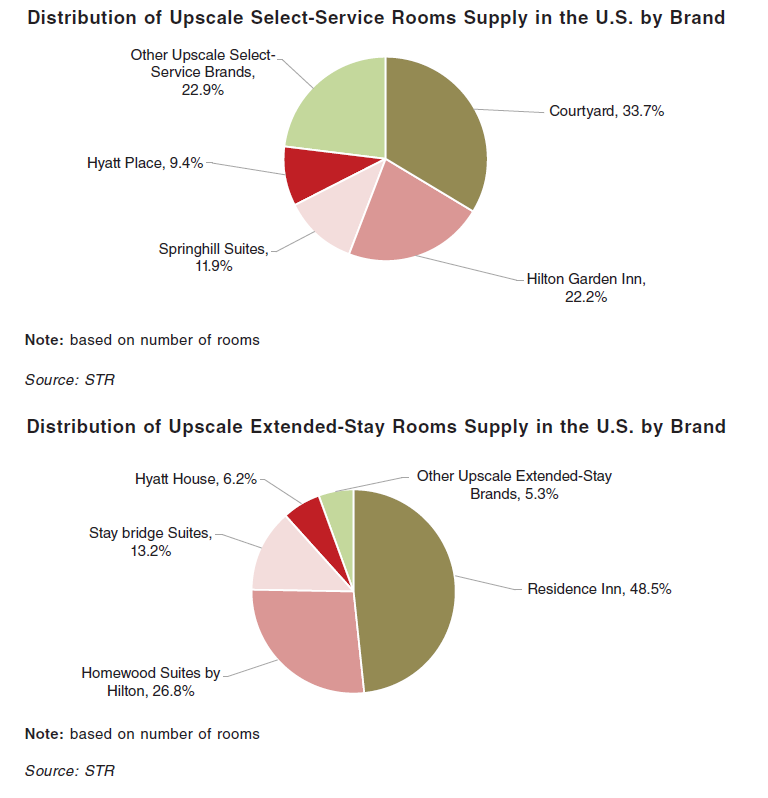

Sector / Geographical Allocation

ARA US Hospitality Trust is a mid-range US Hospitality play. Because these are not the premium, high end Hyatt Hotels, what concerns me is potential competition from the Airbnb style players going forward.

The US market is incredibly competitive, as is the hospitality industry. And hospitality isn’t like commercial (office) or retail (shopping malls) where having a good property in a good location can work wonders. With hospitality, things like branding, the “feel” of the building, customer loyalty, all play a part in attracting and retaining customers. And in hospitality, scale does matter.

And when we look at the kind of market share that Hyatt Place and Hyatt House have, they seem to be in a weird place where they don’t really have scale, neither are they a true boutique players (market share generally below 10%). We’ll take a closer look at the operating numbers later, but for now, business competition from other hospitality chains in the US concerns me going forward.

Of course with a US REIT where earnings are in USD, there will be forex risk. ARA US Hospitality Trust borrows in USD, so there is some natural hedging, but it’s not like some other REITs where they hedge a portion of their foreign earnings. Personally I think this is an acceptable risk, because with a small US REIT like this I would want to get the USD exposure if I buy into it, and in any case USD seems to be the only currency of strength in the near future.

Quality of Assets

Property Manager

The assets are managed by an external third party property manager, Aimbridge, which is basically a large hotel manager in the US:

Aimbridge is the largest third-party hotel management company in North America and the Caribbean with a portfolio of approximately 800 upscale, independent and branded hotels, with more than 100,000 rooms across the U.S., Canada and the Caribbean. With a history of 16 years of operation, Aimbridge has approximately 30,000 employees and maintains records of the permits and licenses required for and held by ARA US Hospitality Trust’s operation of the hotels.

That fine because Aimbridge probably knows what they’re doing, but I sometimes like it more the Sponsor themselves run the property, like what you get with CapitaLand and Ascott REIT. I sleep a lot easier when I know that the Sponsor has a huge hospitality business and is worrying about the hotel business themselves, instead of outsourcing the property management to a third party.

Rent structure – mostly variable

What is also interesting about ARA US Hospitality Trust, is that the rental income is largely variable. Business Times describes this well:

Two-thirds of EHT’s rental is fixed, protecting it from downside risks. The remaining variable rent is pegged to gross operating revenue and gross operating profit, which combined together, give the REIT stability and growth. This is, perhaps, more significant to the hotel industry than other sectors, given that “leases” can be as short as one night for hotel dwellers.

ARA US Hospitality Trust, on the other hand, has a largely variable cost structure. One could argue that unitholders get to enjoy the full upside in good times, but the reverse is also true when the market is down.

With other hospitality REITs, the rent tends to be a mix of fixed and variable rental. For example with Ascott REIT, it’s about 50% fixed rent that is paid regardless of what happens to property income, and a 50% variable rental pegged to income from the property. Because the hospitality industry is highly cyclical, this structure smooths out the earnings, and gives the REIT greater rental income stability. With ARA US Hospitality Trust, the rent is mainly variable in nature. So when times are good, you get to enjoy all the upside, but when times are bad, there’s no one to really “guarantee” a minimum income. It’s a high risk high return structure, and I’m not so sure if I like it, especially given the risky nature of the underlying assets.

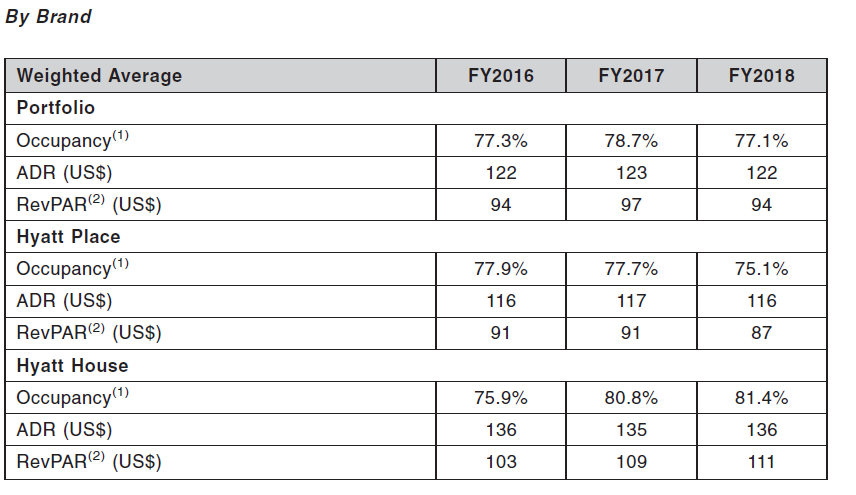

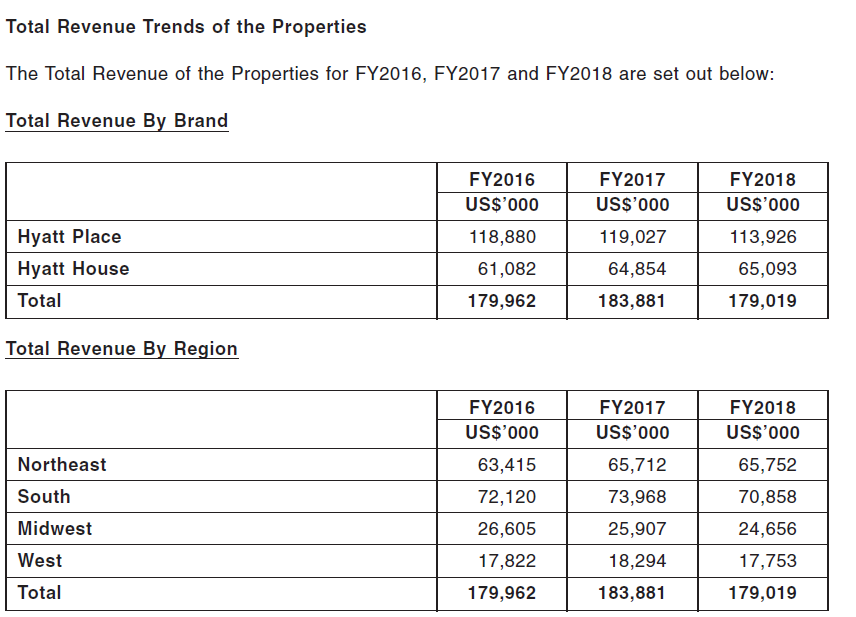

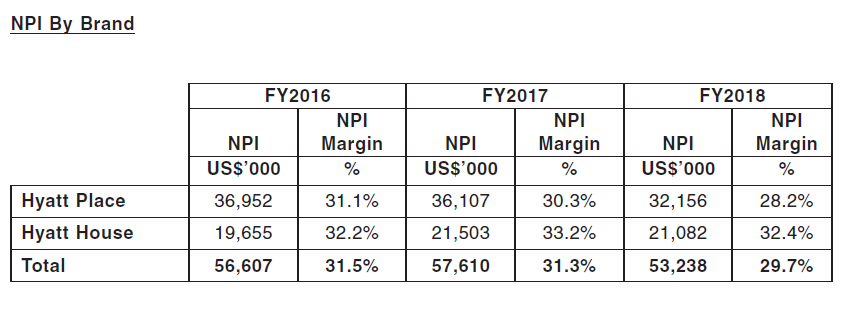

Operating Performance

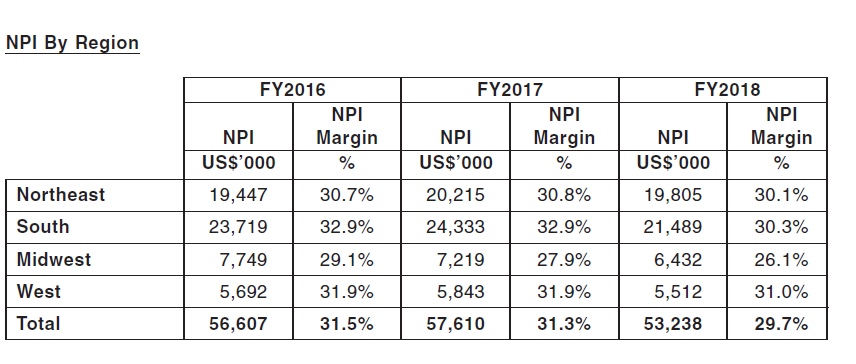

Anyway I took a closer look at the operating figures, which are extracted below:

Across just about every operating metric, it seems that revenue, occupancy, ADR etc are all flattish from FY2016 to FY2018. NPI margins are especially bad, and show a consistent downtrend from FY2016 to FY2018. The drop in revenue from FY2017 to FY2018 is particularly troubling as well.

This is what ARA US Hospitality Trust has to say about it:

“During FY2018, the Initial Portfolio was globally marketed for sale by the previous owner, which was disruptive to the operational performance of the Properties. In addition to running the day-to-day business of the Properties, the on-property management team was required to conduct property tours and inspections, answer questions from consultants and potential investors, and staff had to be redeployed to accommodate the various requests. As such, the on-property management team’s efforts to secure bookings were adversely affected, leading to a loss of Occupancy from FY2017 to FY2018.

Certain markets experienced substantial increases in new supply, diluting demand temporarily and resulting in Occupancy decreases, particularly in the Midwest, South, and West Regions. The dilution in demand is often temporary as new supply eventually gets absorbed. New hotel entrants in markets such as Oklahoma City Airport, Atlanta Alpharetta, Cincinnati Airport, and Denver Airport expanded room inventory and also created downward pricing pressure as they offered introductory rates during their absorption period. Existing hotels such as the Hyatt Place Properties in those markets experienced a decline in Occupancy and RevPAR.”

In other words, FY2018 sucked because the owner / operator was too busy trying to sell the asset, and getting a good price for the sale. It was also bad because of new supply in certain markets, and they believe that this will eventually be absorbed into the market.

It’s hard to comment on the accuracy of this statement because we don’t have that kind of in depth knowledge of the US hospitality market that the property manager would have. We also don’t have access to the Q1 2019 results to see if there was indeed an improvement. So for now, we’ll just have to take management’s word for it.

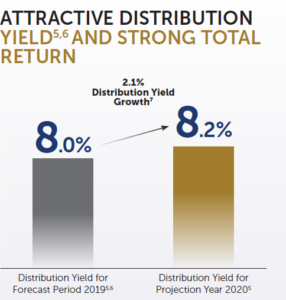

Distribution Yield

Annualised Distribution Yield for 2019 is projected at 8.0%, and 8.2% for 2020.

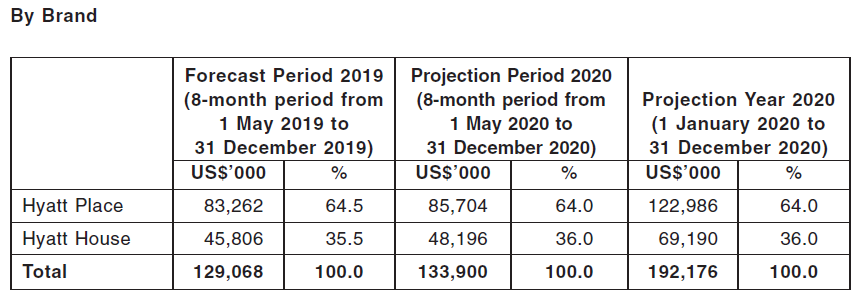

The forecast revenue figures that they use, are set out below.

Taking a look at the FY2018 results, what this means it that they are projecting an 8% increase in revenue from FY2018 to FY2019, and for low single digit growth from FY2019 to FY2020.

Again I don’t know enough about the mid-range US hospitality space to comment intelligently on this, but when I look at the revenue trend over the past 3 years, and look at all the competition from Airbnb, and question marks over the strength of US economic growth, it does get me thinking whether these projections will hold up.

Closing Thoughts: I’ll probably skip this one

Investing is about risk-reward, and for ARA US Hospitality Trust, there are just too many question marks for my liking.

Things that concern me include the lack of clear pipeline going forward, the possibility of a big equity offering to fund acquisitions down the road, the lack of a big institutional cornerstone, the lack of clarity over revenue growth and the risk of competition from other US hospitality players, just to name a few.

Even if we take the forecasts at face value, and assume 8.0% and 8.2% yields, that’s just in line with what Keppel KBS US and Eagle Hospitality Trust are offering.

I’ll give ARA US Hospitality Trust a 2 Financial Horse rating, because while I don’t like it personally, if you’re bullish on the US hospitality space, or if you have inside knowledge on how amazing these assets are, this could still be a good buy. After all, the rental structure allows for plenty of upside if the underlying assets perform well.

For me though, I bought Keppel KBS US REIT at about a 10.3% yield in December 2018 that I’m still holding on to, so if this REIT ever trades in that kind of range, I probably would be interested. At an 8% yield and with all the uncertainties around future performance though, I’m probably giving this a miss.

Will you be taking up this IPO? Share your thoughts in the comments section below! I respond personally to all comments!

Financial Horse Rating – ARA US Hospitality Trust

Financial Horse Rating Scale

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

perhaps you could also analyse a bit the tax structure, how it manages (or not) to escape the US income and withholding tax, and whether such arrangement is a trick/loophole waiting to be plugged. Did you realize the entire income for the reit is in a form of “interest payment” ?

Yep it’s structured as an interest payment for tax reasons. The structure used is market standard for all US REITs listed in Singapore. There was a huge debate recently on wh ether this loophole would be plugged, but it seems that the conclusion for now is that the US will leave it alone, at least for the near future. Any change would affect all the other US S-REITs (Keppel KBS, Manulife) equally, so it’s not a risk that’s unique to ARA.

Hope this helps!

[…] after going through the prospectus, it turns out that Eagle Hospitality Trust is similar to ARA US Hospitality Trust in many ways. So a lot of my comments in the review on ARA Us Hospitality Trust will hold true here […]

[…] after going through the prospectus, it turns out that Eagle Hospitality Trust is similar to ARA US Hospitality Trust in many ways. So a lot of my comments in the review on ARA Us Hospitality Trust will hold true here […]

[…] after going through the prospectus, it turns out that Eagle Hospitality Trust is similar to ARA US Hospitality Trust in many ways. So a lot of my comments in the review on ARA Us Hospitality Trust will hold true here […]