For those who have been following interest rates closely.

You’ll notice that interest rates have come down quite a bit from their highs this cycle.

T-Bills went as high as 4.4% (in Dec 2022), but have since come down to 3.75%.

Fixed Deposits went as high as 4.2% (also in Dec 2022), and have since come down to 3.90%.

With that in mind I wanted to update the list of best fixed deposits in Singapore.

And answer these 3 key questions:

- Will fixed deposit interest rates go even higher from here (or have they peaked)?

- Should you lock in interest rates for 12 – 24 months here?

- Is it safe to put more than $75,000 in a foreign bank?

Best Fixed Deposit Interest Rates in Singapore yield 3.90% – Better than T-Bills or Singapore Savings Bonds for your cash investments? (April 2023)

The full list of Fixed Deposit Interest rates is set out below.

A lot of banks revised their fixed deposit interest rates down recently.

But I’ll just break it down for you.

If you are comfortable with a foreign bank:

- RHB Bank offers 3.90% for 6- or 12-month fixed deposit with a minimum of $20,000

- Maybank offers 3.90% for 12-month fixed deposit with a minimum of $20,000 (must go down to physical branch and there are some conditions)

If you prefer the peace of mind that comes with a local bank:

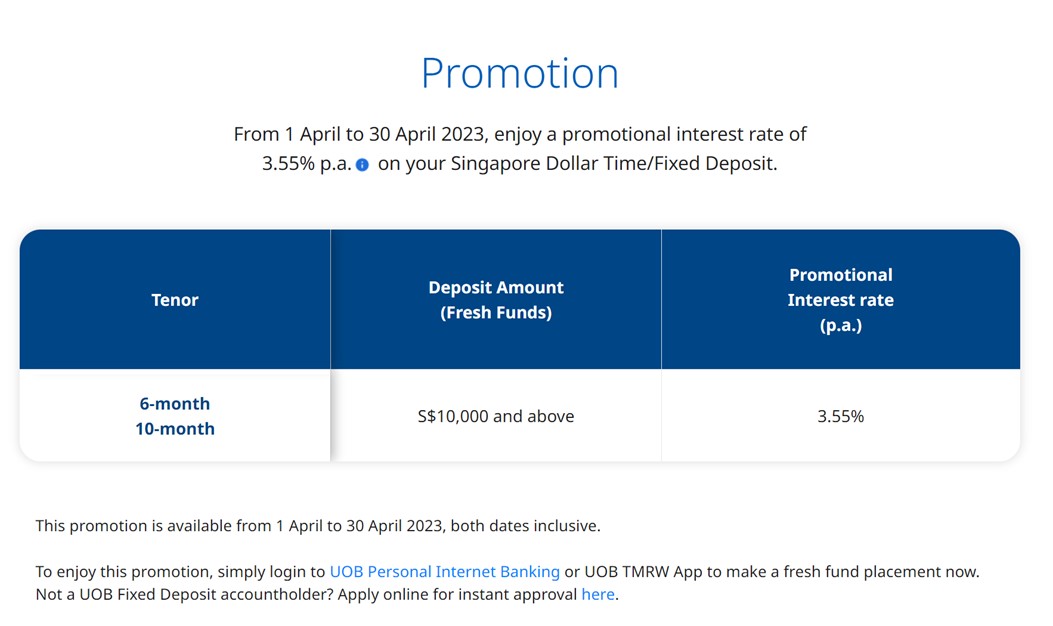

- UOB offers 3.55% for 6- or 10-months fixed deposit with a minimum of $20,000

- OCBC offers 3.40% for 6 months fixed deposit with a minimum of $20,000

Here’s the full list below:

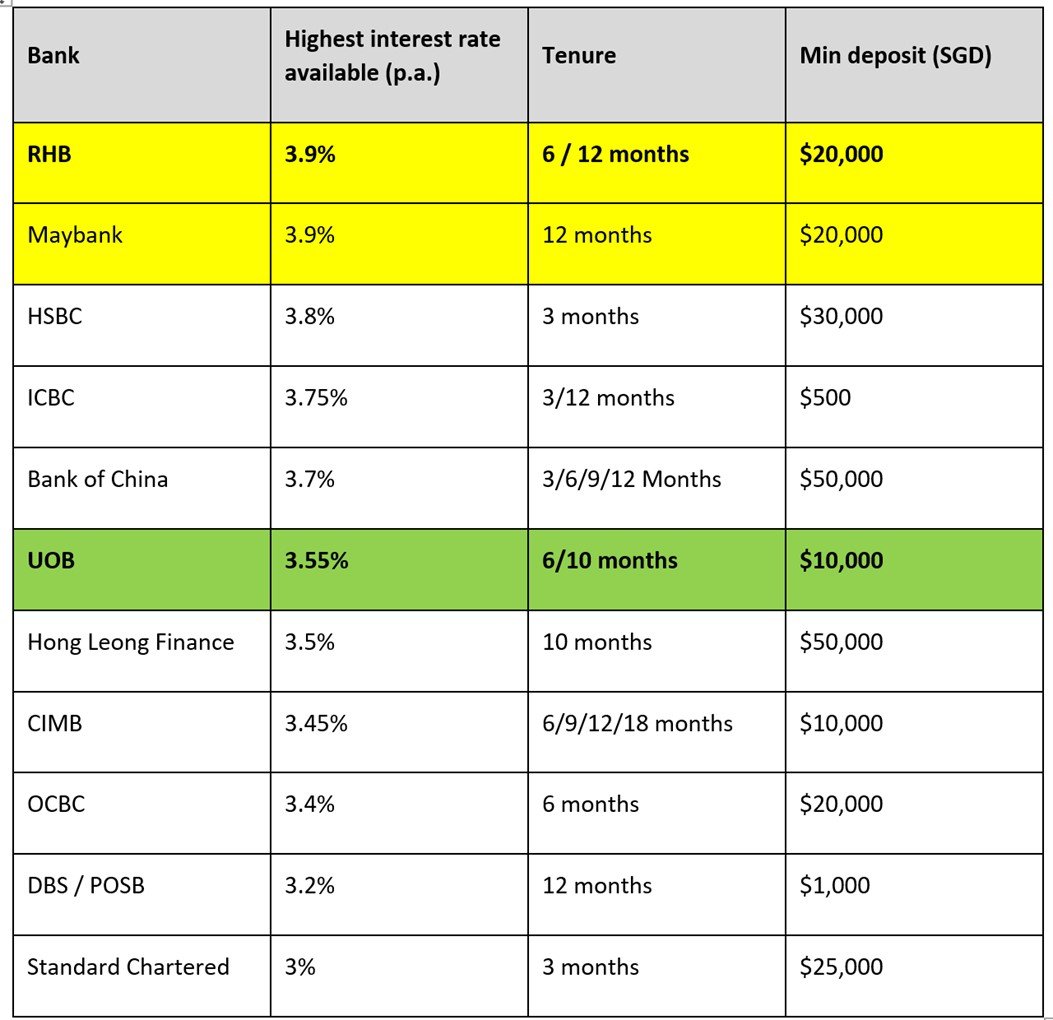

Here’s the same in a table form:

|

Bank |

Highest interest rate available (p.a.) |

Tenure |

Min deposit (SGD) |

|

RHB |

3.90% |

6 / 12 months |

$20,000 |

|

Maybank |

3.90% |

12 months |

$20,000 |

|

HSBC |

3.80% |

3 months |

$30,000 |

|

ICBC |

3.75% |

3/12 months |

$500 |

|

Bank of China |

3.70% |

3/6/9/12 Months |

$50,000 |

|

UOB |

3.55% |

6/10 months |

$10,000 |

|

Hong Leong Finance |

3.50% |

10 months |

$50,000 |

|

CIMB |

3.45% |

6/9/12/18 months |

$10,000 |

|

OCBC |

3.40% |

6 months |

$20,000 |

|

DBS / POSB |

3.20% |

12 months |

$1,000 |

|

Standard Chartered |

3.00% |

3 months |

$25,000 |

If you are comfortable with a foreign bank

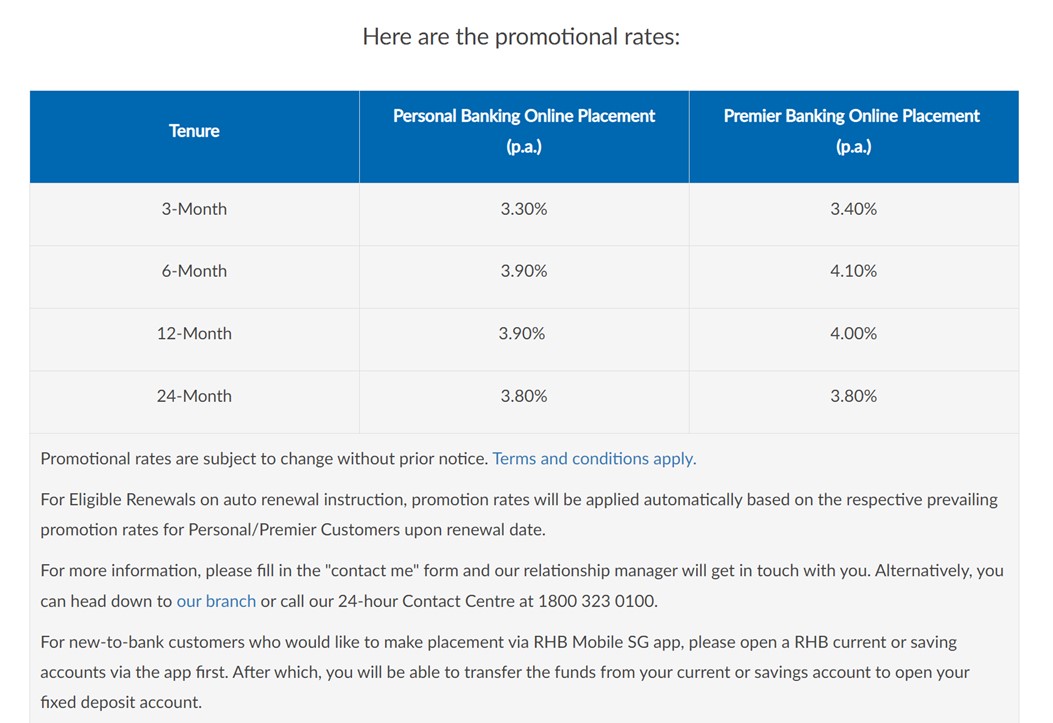

RHB Bank – up to 3.90% for 6 or 12 months (minimum $20,000 deposit)

RHB Bank is offering 3.90% for a 6 or 12 months fixed deposit.

Minimum deposit of $20,000.

Frankly quite a good deal.

Based on what I could find, this looks to be the highest Fixed Deposit interest rate in Singapore right now:

The big question then is whether one should be locking in a 6 or 12 month fixed deposit right now – given you can get 3.90% for both.

I don’t think there’s a right or wrong here, but I’ll share my personal views on the issue below.

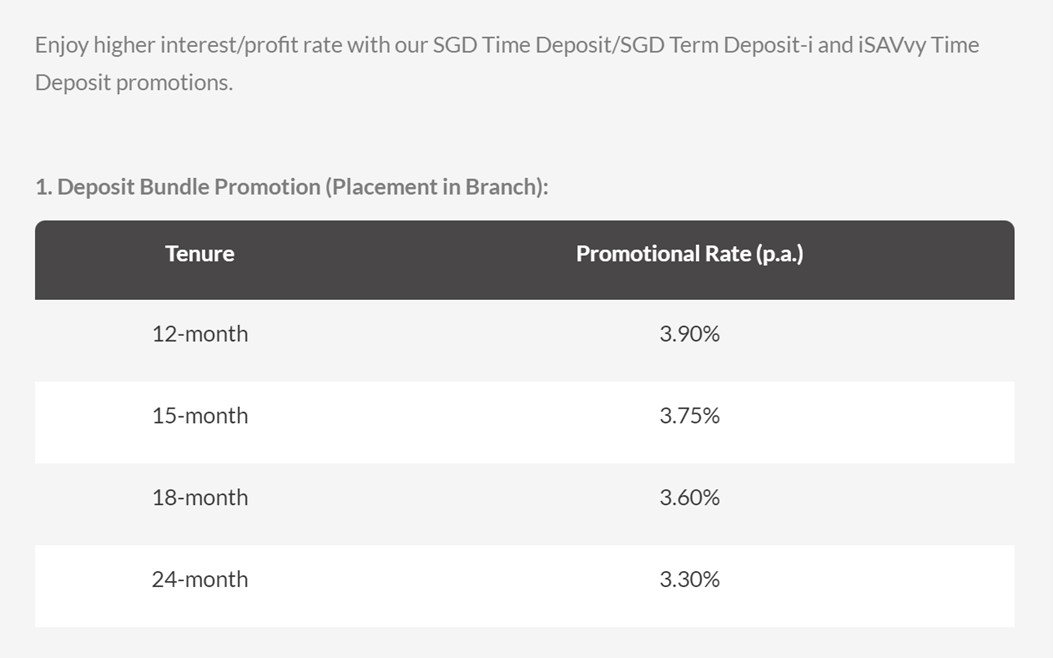

Maybank Fixed Deposit – 3.90% for 12 months (minimum $20,000) (must go down to physical branch)

For those that don’t like RHB Bank, or have already exceeded the $75,000 SDIC limit for RHB Bank.

Maybank is also offering 3.90% for a 12 months fixed deposit.

Minimum deposit of $20,000 too.

There is a catch though.

Firstly you need to the physical bank branch (in person) to place the fixed deposit.

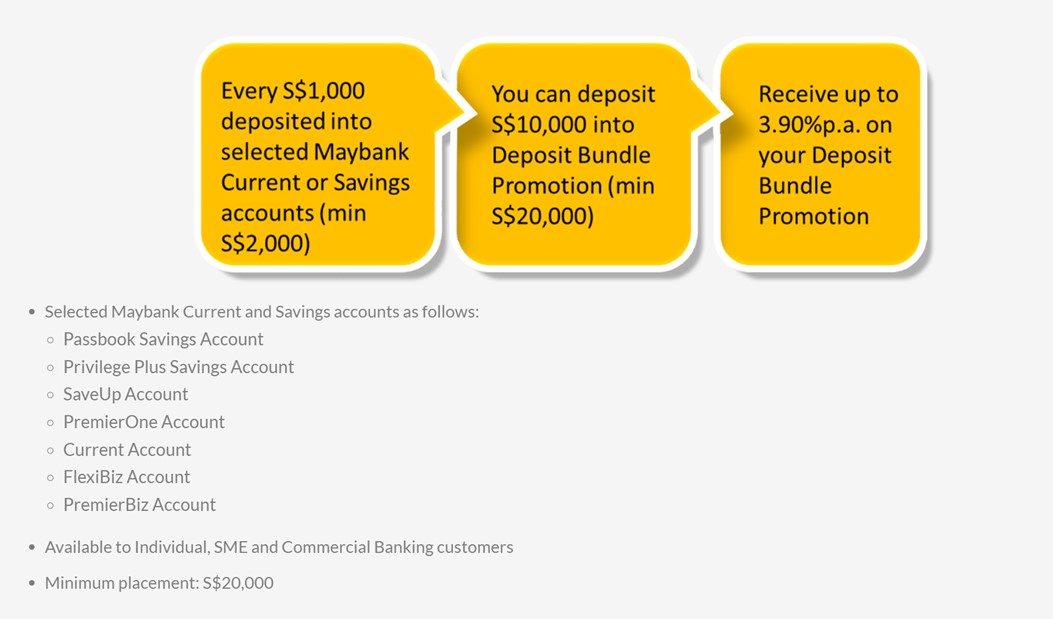

And secondly – you need to also place some cash into a Maybank account.

For every $1,000 deposited, you can deposit $10,000 into the Fixed Deposit.

It’s not a problem if you already have an account with Maybank that you use, but it might be annoying for new customers.

Do also note that this will bring the “effective interest rate” down to about 3.6% if you count the $1000 you need to deposit into the savings account.

If you want to stick with a local bank

I know some investors who prefer to deposit their money only with a local bank.

We’ll discuss this in further details below.

But for now – If you want to go with a local bank, UOB is probably your best bet.

UOB Fixed Deposit – up to 3.55% on 6, 10-month fixed deposit (minimum $10,000)

UOB offers 3.55% on 6 and 10 month tenures.

With a minimum deposit of $10,000.

Note that this is quite a big change from their promotion last month where they were offering 3.85% with a minimum deposit of $50,000.

And the 12 month tenor have been taken off the table as well.

So it does show that interest rates are starting to come down, and some banks are more reluctant to the same rates for longer term tenures.

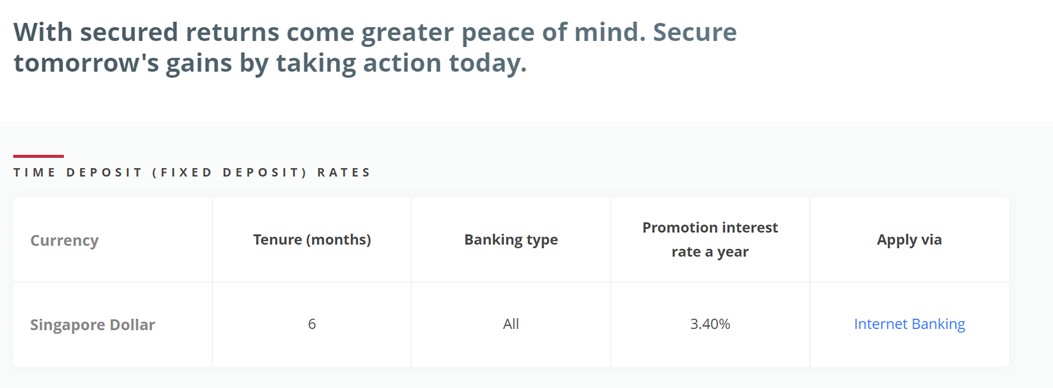

Alternatively, OCBC offers 3.40% on a 6 month Fixed Deposit

If you don’t want UOB for some reason.

The next best bet is OCBC.

OCBC was offering a 4.08% promo as recently as February.

Unfortunately that promotion is over, and it’s dropped to 3.40% now:

Minimum deposit of $20,000.

Fixed Deposit compared versus Singapore Savings Bonds and T-Bills – Which is a better buy?

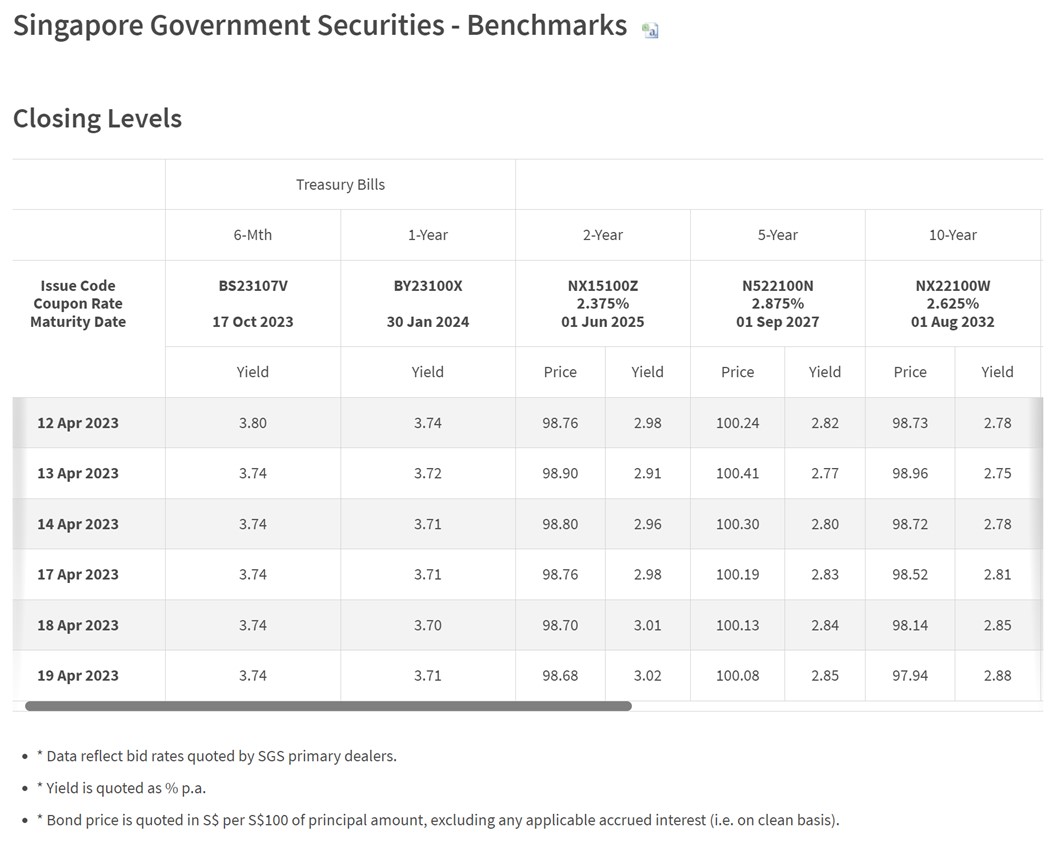

T-Bills

For the record, latest T-Bills interest rates are:

- 3.75% for 6 months T-Bill

- 3.58% for 12 months T-Bill

T-Bills don’t offer easy liquidity though, so it will not be straightforward to get your money back before maturity.

Given that Fixed Deposit interest rates are actually better than T-Bills, for cash investors you’re probably better off just placing the money in Fixed Deposit.

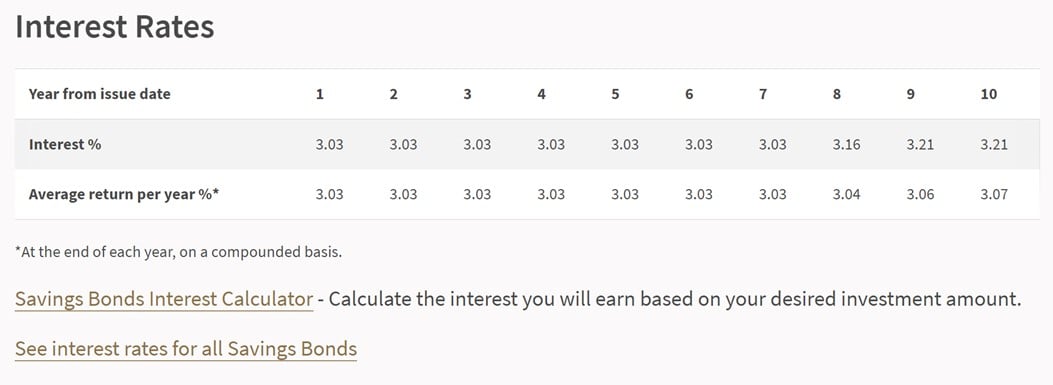

Singapore Savings Bonds

Singapore Savings Bonds on the other hand, are very interesting.

I plan to write more on this, but the long and short is that locking in the interest rates below for the next 10 years is not too bad as a hedge.

If interest rates do get cut drastically, you can hold for up to 10 years.

If interest rates stay high, you can redeem the full principal any time with accrued interest (no duration risk).

But of course, no denying that the 1 year interest rate of 3.03% is not as high as Fixed Deposit’s 3.90%.

That’s the price you pay for locking in rates for 10 years.

Next month’s Singapore Savings Bonds unlikely to be as good

Note that if you look at latest market interest rates, the interest rates on the next Singapore Savings Bonds are unlikely to be as good.

You’re probably looking at 2.8% interest flat for the first several years.

So for those who want to lock in money a bit longer, Singapore Savings Bonds are a decent alternative to fixed deposit.

With the uncertainty over where interest rates will go in the rest of 2023, not a bad idea to buy this month’s Singapore Savings Bonds if you are keen.

3 key questions that I want to discuss on Fixed Deposits

Okay, on to the more interesting stuff.

3 key questions to discuss:

- Will fixed deposit interest rates go even higher from here (or have they peaked)?

- Should you lock in interest rates for 12 – 24 months here?

- Is it safe to put more than $75,000 in a foreign bank?

Let’s discuss each of them.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Will fixed deposit interest rates go even higher from here (or have they peaked)?

Here’s what the market is pricing in.

1 more interest rate hike, and then the Feds to pause until late 2023 when interest rates get cut.

I think the market pricing is wrong on this

As shared previously, I just think the market pricing is wrong on this.

I agree that 1 more rate hike and we get a Fed “Pause”.

But I think the timing of the interest rate cuts priced in the market is too aggressive.

When exactly the Feds cut is the million dollar question – to which I have no easy answers to.

But I’ll be willing to bet that it is going to be later than what the market is pricing in above.

So FH… are Fixed Deposit interest rates going higher or not?

Based on the above.

If we only see 1 more interest rate hike, and a period of pause after that.

And where the uncertainty is more about the duration of how long rates stay here, rather than how much higher they go.

Then I don’t think bank Fixed Deposit interest rates will go much higher from here.

Of course, a big qualifier that fixed deposit interest rates are fixed by the bank, and only track market interest rates loosely.

So if banks have an urgent need for money (for eg. if depositors pull funds), it is possible that interest rates go higher.

Should you lock in interest rates for 12 – 24 months here?

If fixed deposit interest rates are unlikely to move up significantly from here.

And the risk is for interest rate cuts rather than interest rate hikes.

Then I suppose it doesn’t hurt to lock in a longer term fixed deposit (provided you don’t need the money in the short term).

You don’t have to put all your eggs in one basket…

Don’t forget you can ladder it to manage risk.

For example, you can put:

- 50% into a 6 month fixed deposit

- 25% into a 12 month fixed deposit

- 25% into a 24 month fixed deposit

To balance between liquidity needs while also locking in interest rates longer term.

Just in case market is right and interest rates are slashed in the second half of 2023.

What would I do? Lock in 6 or 12 months Fixed Deposit?

Up until now I’ve been mostly locking in 6-month fixed deposit / T-Bills.

This was because we were in an aggressive rate hike cycle, where the risk to interest rates was to the upside rather than downside.

But where we are today, it’s clear that we are very advanced in the rate hike cycle.

So I think the equation has skewed towards locking in a longer term duration.

So for my money that is coming due, I may actually consider switching to the 10 or 12 month Fixed Deposit for funds I don’t expect to be using so quickly.

But again, this is just me.

I leave it for each investor to decide the right balance between liquidity and yield.

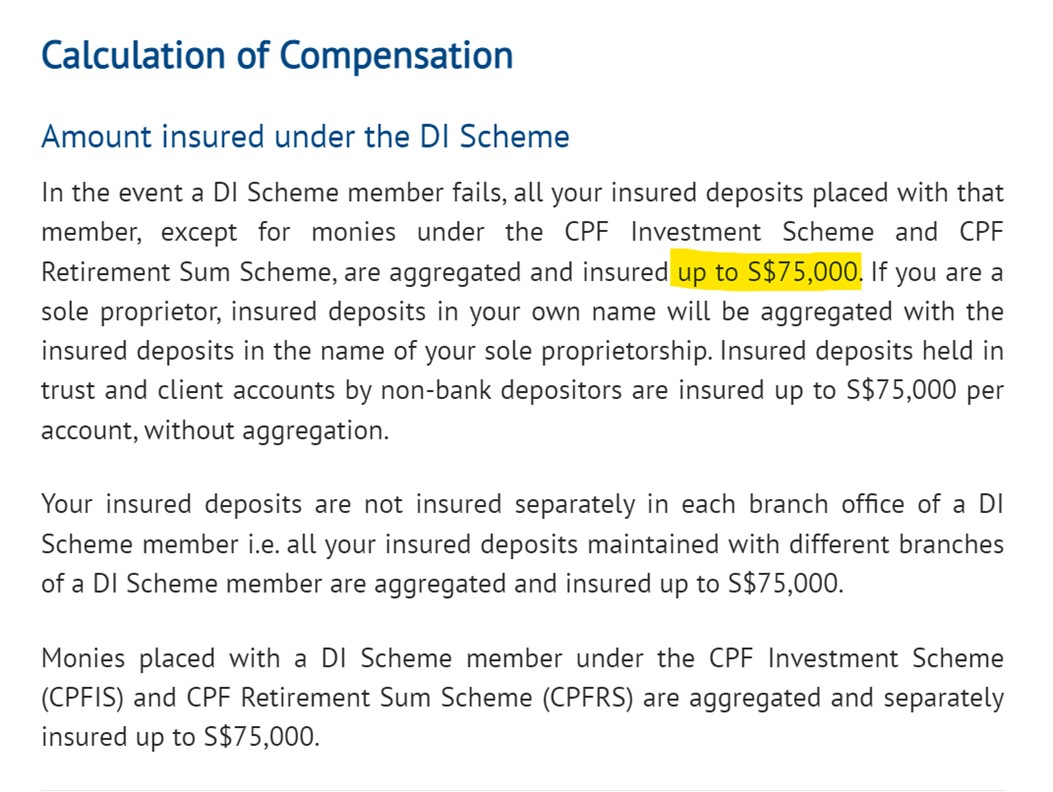

Is it safe to put more than $75,000 in a foreign bank? Especially after the failures of Silicon Valley Bank?

Do note that SDIC insurance only guarantees customer deposits up to $75,000 if there is a bank failure in Singapore.

This means that any amount above $75,000 with a bank in Singapore is technically not insured under SDIC insurance.

Ie. You are taking on counterparty risk, the risk that the bank goes under.

What is the risk of a foreign bank going under?

Let me just put it out there and say that I think the risk of a foreign bank going under in Singapore is low.

But hey – You never really know what you don’t know sometimes.

While the risk of a foreign bank in Singapore going under is low.

I wouldn’t say the risk is zero.

My Personal Views – Fixed Deposit with a Singapore bank or foreign bank?

I think if you’re holding up to $75,000 with a foreign or Singapore bank you don’t need to worry at all as it is SDIC insured.

Anything above $75,000, you do need to understand you are taking on counterparty risk of the bank.

For me personally I usually only hold amounts above $75,000 with a local bank.

Again, I know that the risk is exceedingly low, but it’s ultimately your call.

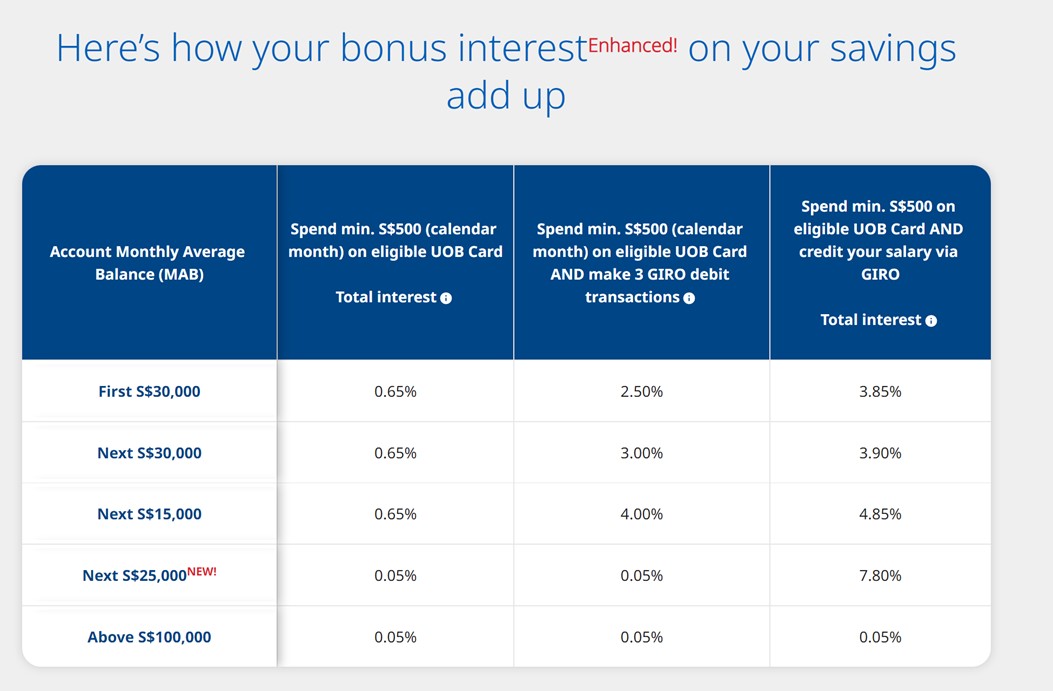

UOB One Account – up to 5% on $100,000

Just a final note that for those prepared to jump through a couple of hoops, the UOB One Account is a very fantastic deal.

If you spend a minimum of $500 on your UOB credit card, AND credit your salary via Giro.

You can get up to 5% effective interest on $100,000.

Don’t forget all this cash is fully liquid (can be transferred out any time with no lockup period).

And 5% is comfortably above latest T-Bill and Fixed Deposit interest rates.

Very good deal if you can hit the requirements.

This article is written on 21 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FH

Much appreciated your time in writing down to earth articles on money and investments that’s easy is clear and easy to understand .

????????????????

Thank you, appreciate the kind words. Do my best to help.

Thumbas up!

Thank you, appreciate the kind words. Do my best to help.

Hey FH! Given that we are this late in the rate hiking cycle, should we start to look at high quality fixed income funds rather than just holding cash?

Love reading your cash and equity strategies. Pls write on fixed income soon!

Ah I actually wrote a piece for Patrons on this. It’s a TLT play to bet on the falling long end due to a recession. But it will require call options to juice the trade (leverage) so it’s a bit more sophisticated than the usual long only plays I write on the public version of the site. With options you will need to consider timing and the option greeks as well.

But I get what you mean, let me see whether I can do something on the site for this.