Earlier this year, the story for cash was straightforward. Interest rates were falling, and the only real question was how quickly they would drop.

All that has changed.

The conflict in the Middle East has pushed oil and inflation higher and the Federal Reserve has shifted from cutting rates to signalling that its next move could be a hike.

For Singapore savers, the practical consequence is simple: cash yields have stopped falling, and may start rising going forward.

The 6-month T-bill has bounced off its lows, and the best fixed deposits have actually ticked up since February.

So this is a good time to revisit the question — where is the best place to park cash for yield today?

A few things I wanted to work through:

- The best risk-free rates available today?

- Why cash yields have stopped falling, and where they might go from here?

- Where I would park my cash today for yield?

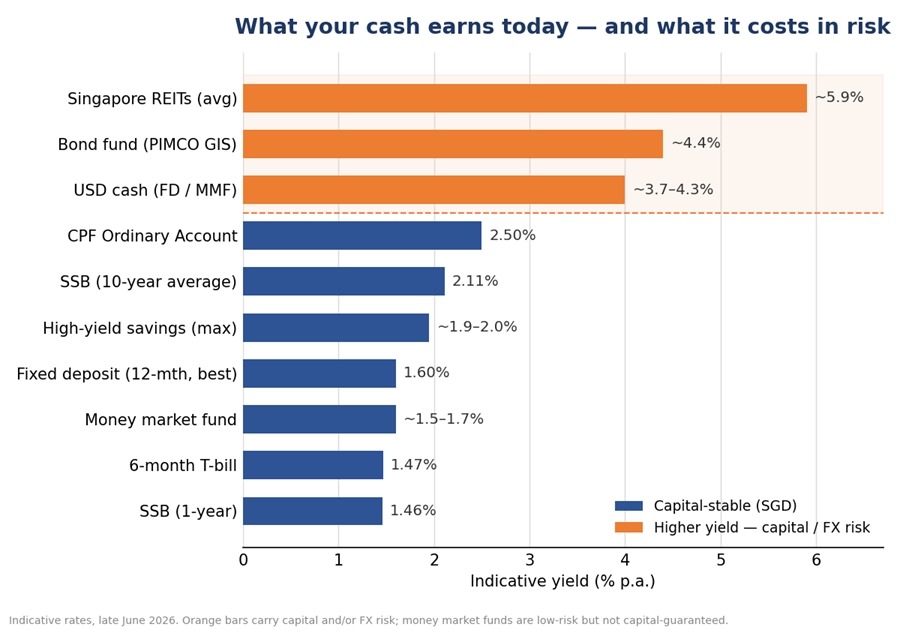

The short answer – Where is the Best Place to Park Cash for Yield Today?

The detailed comparison is further down, but here is the short version.

If your money needs to stay liquid, a money market fund or a high-yield savings account is the natural home.

If you can lock it up for six to twelve months, the best fixed deposits now edge out T-bills — and they come with deposit insurance.

And for money you genuinely will not touch until retirement, a CPF top-up at 2.5% is hard to beat on a risk-free basis.

And if you are comfortable with some risk, REITs, bond funds or USD money market funds offer even greater yields – but are NOT risk free.

The table below sets out the same options in more detail — the yield, whether your capital is guaranteed, how quickly you can get your money back, and whether it is covered by deposit insurance.

| Option | Yield (p.a.) | Capital guaranteed? | Liquidity |

| 6-month T-bill | ~1.47% | Yes (SG Govt) | Locked 6 mths; can sell early at market price |

| Fixed deposit (6–12 mths) | 1.50% – 1.60% | Yes | Locked for tenure; some allow penalty-free exit |

| Singapore Savings Bond | 1.46% Yr 1 / 2.11% 10-yr avg | Yes (SG Govt) | Redeem any month, no penalty |

| Money market fund | ~1.4% – 1.7% | No (very low risk) | ~1 business day |

| Cash mgmt – enhanced tier | ~2.5% – 4% | No (higher risk) | A few business days |

| High-yield savings (OCBC 360 / UOB One) | ~1.90% – 2.00% | Yes | Instant |

| CPF Ordinary Account | 2.50% | Yes | Locked till retirement |

| USD fixed deposit / MMF | ~3.7% – 4.3% | FD: Yes / MMF: No | Varies |

Why have cash yields stopped falling?

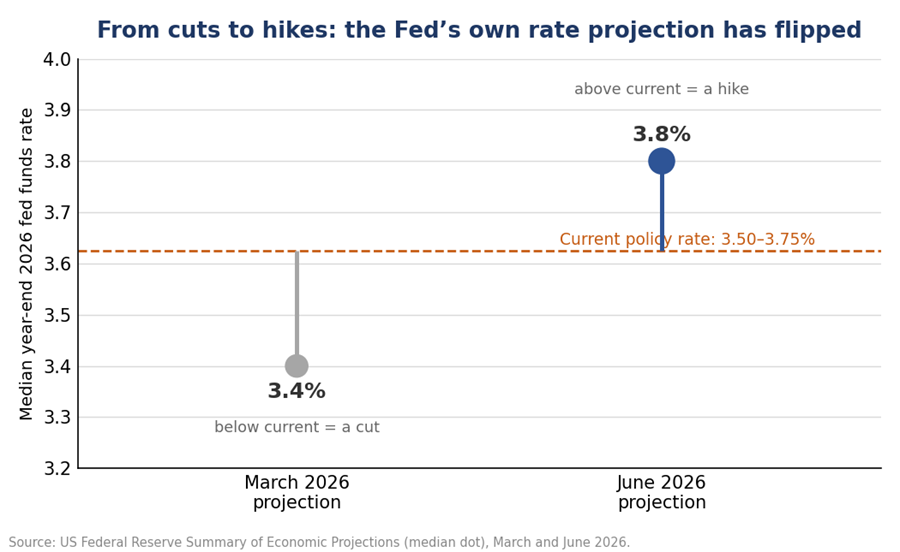

To understand where interest rates go from here, it helps to start with the Fed.

At its June meeting — the first chaired by Kevin Warsh.

The Fed dropped its forward guidance, and the median policymaker now expects rates to end 2026 higher than today.

In plain English, the markets went from expecting rate cuts in 2026 at the start of the year, to now expecting rate hikes

You can see the shift below.

The reason is simple – inflation due to the Iran war.

US headline CPI rose 4.2% in May due to higher oil prices, and the Fed lifted its end-2026 inflation forecast to 3.6%, from 2.7% in March.

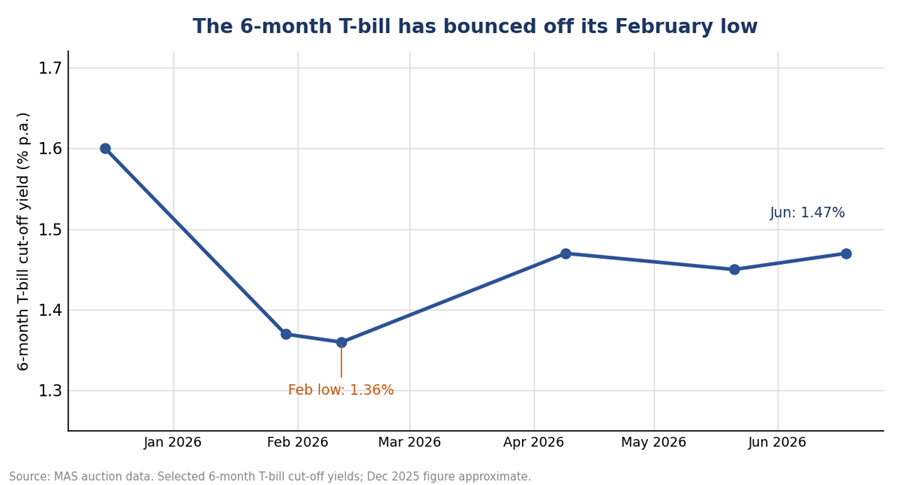

In Singapore you can see how 6-month T-bill has climbed back to 1.47% from a low near 1.36% in February

So the easy assumption that cash yields only fall from here no longer holds — and that changes how I would think about locking money up for the long term.

You do need to account for the possibility that interest rates could go up from here (this has implications for mortgages and stocks as well).

Fixed deposits — now the most competitive they have been in months at 1.6%

Start with the most familiar option.

The best mainstream fixed deposit rates today are around 1.50% for a six-month tenure (HL Bank and CIMB) and up to 1.60% for twelve months (GXS via its Boost Pocket).

Bank of China is running a higher 1.75% promotion, but only for larger placements of S$200,000 to S$250,000 in fresh funds, on eight- or eleven-month tenures.

Fixed deposits are insured by the SDIC up to S$100,000 per bank, which means that the best rates now sit above the 6-month T-bill.

That is a reversal from much of last year, and it makes fixed deposits the more sensible choice than T-bills for most savers right now.

The full list is below, with the standout rates in bold.

| Bank / Institution | Rate p.a. | Tenure | Min. amount |

| GXS (via Boost Pocket) | 1.60% | 12 months | S$100 (cap applies) |

| HL Bank | 1.50% | 6 months | S$10,000 (fresh funds) |

| CIMB | 1.50% | 6 months | S$10,000 (fresh funds) |

| State Bank of India | 1.50% | 12 months | S$50,000 |

| Singapura Finance | 1.48% | 12 months | S$50,000 |

| Bank of China (large placement) | 1.75% | 8 / 11 months | S$200,000 (fresh funds) |

| Bank of China (standard) | 1.35% | 3 months | S$500 |

| Bank of East Asia | 1.45% | 6 / 12 months | S$100,000 |

| RHB | 1.40% | 6 / 12 months | S$20,000 |

| Maybank (deposit bundle) | up to 1.45% | 9 / 12 months | S$20,000 + bundle |

| ICBC | 1.40% | Fresh-funds promo | S$200,000 (3-mth: 1.35%) |

| MariBank | 1.30% | 12 months | S$100 (max ~S$100k) |

| UOB | 1.25% | 6 months | S$10,000 (fresh funds) |

| OCBC | 1.20% | 9 / 12 months | S$20,000 (fresh funds) |

| HSBC | 1.18% | 3 / 12 months | S$30,000 (Premier Elite) |

| DBS / POSB | 1.00% | 9 / 12 months | S$1,000 (max S$19,999) |

Indicative promotional rates as at late June 2026, lowest tier and fresh funds unless stated. Rates change frequently — verify directly with the bank before placing funds.

6-month T-bills — yielding 1.47%, but no longer the best deal

The latest 6-month T-bill, auctioned on 18 June, came in at a cut-off yield of 1.47%.

That is up from a low near 1.36% in February, tracking the rebound in global bond yields.

At 1.47%, the maths no longer favours T-bills over fixed deposits. You are locking up your cash for 6 months, for a lower yield.

A fixed deposit at 1.60% is higher, comes with deposit insurance, and at most banks can be broken without penalty.

T-bills still have their place — particularly if you are deploying CPF or SRS funds, where the alternatives are more limited.

But for straightforward cash, I find it hard to argue for a T-bill over the best fixed deposit at today’s spread.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

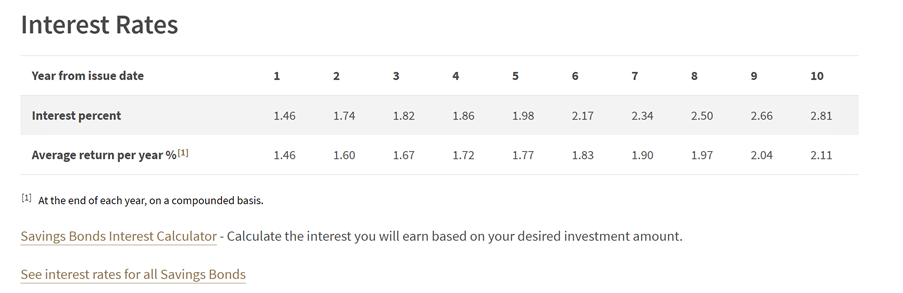

Singapore Savings Bonds — 2.11% over ten years, with full flexibility

The latest issue (SBJUL26) pays 1.46% in the first year, stepping up to an average of 2.11% per annum if held for the full ten years.

Each person can hold up to S$200,000 across all issues.

It’s slightly lower than fixed deposits, and given interest rates are rising going forward, I don’t think they are an amazing buy.

For what it’s worth, if you bought SSBs back in 2022 to 2024 when ten-year averages were above 3% (like I myself did), hold onto them — those are well above anything available today.

You can basically hold 2022 SSBs and earn 3%+ risk free, while borrowing from the bank at 1.4% today on a mortgage.

That’s a no brainer.

Money market funds and cash management accounts

For cash that needs to stay liquid, money market funds and cash management accounts can be looked at.

These products invest in short-term instruments — eg. T-bills and short-dated debt — and letting you withdraw 2 business days.

They are not capital-guaranteed and not SDIC-insured, but the lowest-risk versions are pretty low risk.

The pure money market fund options — the Fullerton SGD Cash Fund, MariBank’s Mari Invest SavePlus — are currently yielding in the region of 1.4% to 1.7% after fees.

If you are willing to take a little more risk, the “enhanced” tiers — Endowus Cash Smart Enhanced and Ultra, StashAway Simple Plus, and the bond-fund wrappers — reach higher yields by holding short-duration bonds.

But this does mean higher risk, and comes with mark to market volatility: the yield is higher, but the unit price can move based on interest rates.

| Product | Type | Indicative net yield |

| Fullerton SGD Cash Fund | Money market fund | ~1.4% – 1.7% |

| Syfe Cash+ Flexi (SGD) | Money market fund | ~1.6% – 1.7% |

| StashAway Simple | MMF + liquidity funds | ~1.5% – 2.2% |

| Mari Invest SavePlus | MMF + liquidity funds | ~1.0% – 1.5% |

| Endowus Cash Smart Enhanced / Ultra | Short-duration bonds | ~2.5% – 4% |

| Mari Invest Income (PIMCO GIS Income) | Global bond fund | ~4.4% (capital at risk) |

High-yield savings accounts

High yield savings accounts remain one of the better options for liquid cash — if you can meet the conditions.

OCBC 360 now pays an effective rate of up to 1.95% on the first S$100,000 when you credit your salary, save and spend; UOB One pays up to 1.90% on the first S$150,000 for card spend plus a salary credit or three GIRO transactions.

Both were trimmed in late 2025 and early 2026, but they still beat most fixed deposits — and the money stays instantly accessible.

Two things to watch.

First, the bonus interest only applies up to the cap; balances above S$100,000 (or S$150,000 for UOB One) earn close to nothing.

Second, if meeting the salary-and-spend conditions every month is a hassle, the effective rate falls drastically. So if you can’t meet the conditions, skip it.

| Account | Effective rate (realistic) | Bonus cap | Main conditions |

| OCBC 360 | up to 1.95% | First S$100,000 | Salary + Save + Spend |

| UOB One | up to 1.90% | First S$150,000 | S$500 card spend + salary / 3 GIRO |

| UOB Stash | up to 2.00% | First S$100,000 | Grow monthly balance (no salary/card) |

| Standard Chartered Bonus$aver | ~1.85% | First S$100,000 | Salary + card spend |

| DBS Multiplier | 1.80% – 4.10% | First S$100,000 | Income + transactions |

| CPF Ordinary Account | 2.50% (floor) | — | Locked till retirement |

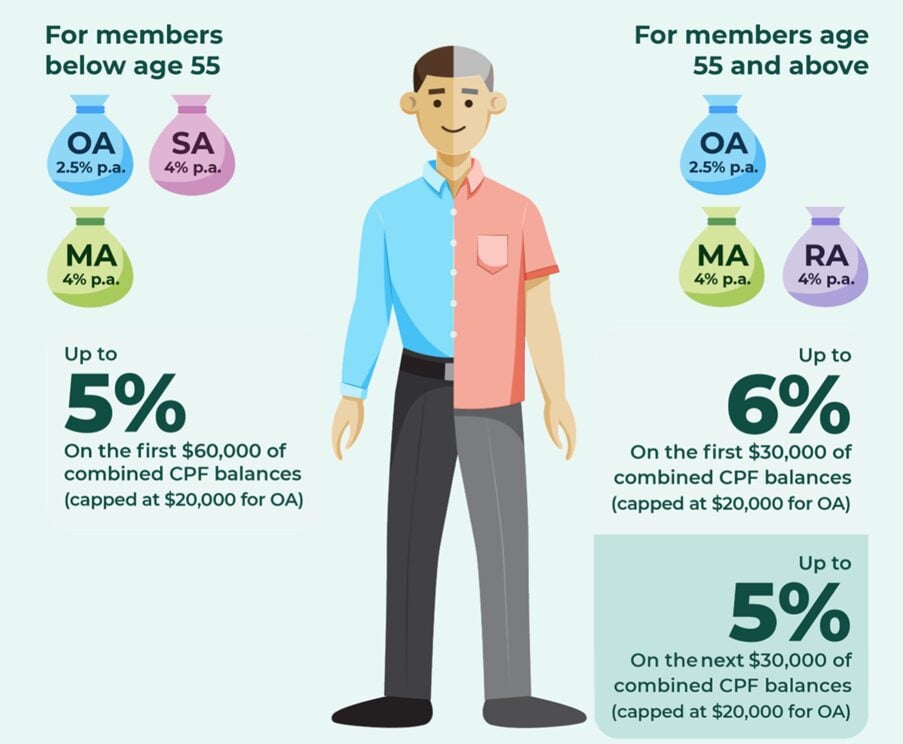

A 2.5% risk-free option hiding in plain sight — CPF

Don’t forget your CPF Ordinary Account, which earns a guaranteed 2.5% floor — now higher than every fixed deposit and most savings accounts on this list.

The catch, of course, is liquidity.

CPF monies are locked until retirement, and a voluntary top-up to your Special, MediSave or Retirement Account is irreversible.

So this is not a home for emergency funds or money you might need in the next few years.

What about USD cash?

The best USD fixed deposits are paying around 3.85% to 3.90%, and USD money market funds are in a similar 3.7% to 4.3% range.

That is more than double what you earn in SGD.

But there is no free lunch.

USD deposits carry foreign exchange risk, and they are not covered by the SDIC.

The Singapore dollar has been strong, and if it strengthens further, the currency move can wipe out the yield advantage when you convert back.

This only makes sense if you already hold US dollars, or have US dollar spending needs or the holding power to wait for a favourable exchange rate.

Personally I would not convert SGD into USD purely to chase the higher rates unless I need to use the USD.

Stepping out the risk curve — REITs and bond funds

Everything above is, broadly, relatively low risk.

If you are comfortable to take on real capital risk for a higher yield, then there are a lot more options.

A diversified basket of Singapore REITs yields around 5.9% today, with the main S-REIT ETFs (Lion-Phillip and CSOP iEdge) yielding around 5.4% to 5.9%.

Against a T-bill at 1.47%, that is a spread of roughly four percentage points — which is actually pretty decent.

The same logic applies to bond funds. Something like the PIMCO GIS Income Fund currently yields around 5%.

But to be clear — this is not risk free, so it should not be a replacement for cash.

Use these only if you can lock up the funds for a while, and you can tolerate capital loss.

So where would I park my cash today?

The way I think about cash is to match each pot to its time horizon and the risk I am willing to take.

- For emergency and near-term cash, I keep it liquid — a money market fund, or a high-yield savings account like UOB One.

- For money I can commit for six to twelve months, the best fixed deposit at 1.50% to 1.60% now makes more sense than a T-bill — higher, insured, and at some banks penalty-free. Of course if you hold 2022 Singapore Savings Bonds are 3% then hold onto them like they are gold.

- For money I can take some risk on and don’t need so soon, REITs or bond funds are an option to look at – but note they are not risk free.

Given the move from interest rate cuts to interest rate hikes, I don’t see a need to lock up money at the long end.

I would lean towards short duration and flexible instruments today, given the bias towards higher interest rates going forward.

So that’s how I’m thinking about parking cash for yield today. Love to hear what you think — where are you parking your cash?

This article was written on 26 June 2026. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

Which S REITs is good….any tips

you may start with CICT for SReits