It’s funny how life turns out. Just last week I added CapitaLand Limited onto the FH Stock Watch, because I thought it was starting to look interesting as a long term investment. And today, CapitaLand announced that they would be buying over Ascendas-Singbridge from Temasek, in what is probably going to be the largest Singapore M&A deal this year.

Basics: Who is buying who?

There’s a lot of misinformation going around, so I’m just going to summarise quickly what’s happening (the full announcement and slides are here).

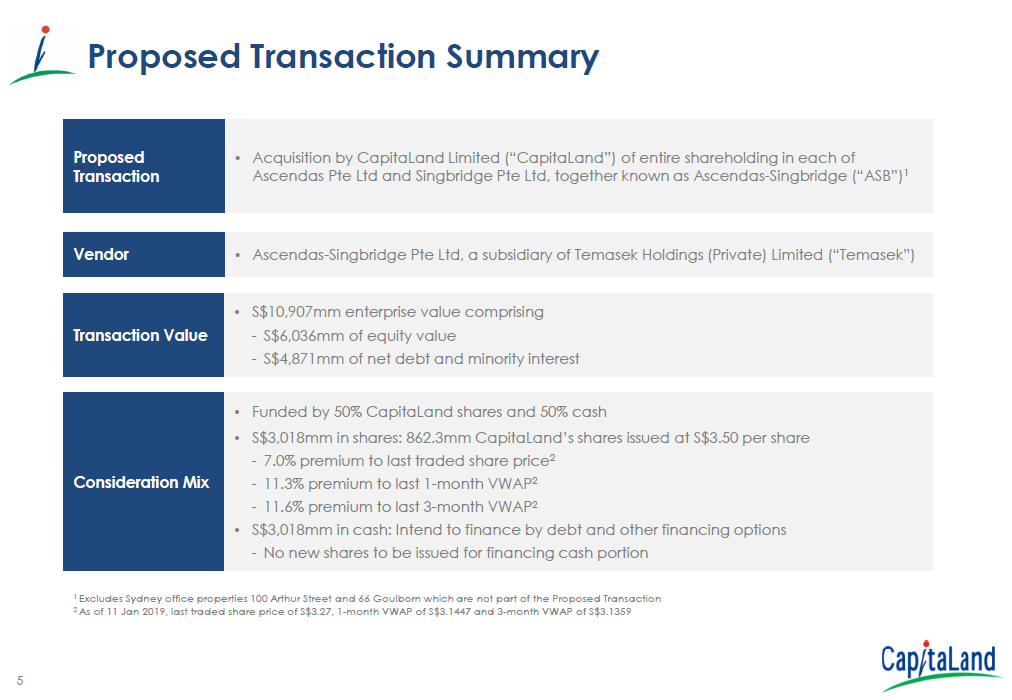

CapitaLand Limited is a property developer that is about 40% owned by Temasek. CapitaLand is the sponsor of 5 different REITs (CapitaLand Mall Trust, CapitaLand Commercial Trust, CapitaLand Retail China Trust, Ascott Residence Trust, CapitaLand Malaysia Mall Trust), and holds about a 30 to 40% stake in each of them.

Ascendas-Singbridge is a property developer that is 100% owned by Temasek. Ascendas-Singbridge is the sponsor of 3 different REITs (Ascendas REIT, Ascendas Hospitality REIT, Ascendas India Trust), and also holds about a 30 to 40% stake in each of them.

Today, CapitaLand has agreed to buy Ascendas-Singbridge from Temasek at an enterprise value of S$10.9 billion. But because S$4.8 billion of this enterprise value is debt in Ascendas-Singbridge (that CapitaLand will assume when it buys over Ascendas), the actual amount that CapitaLand will pay Temasek is S$6.0 billion.

So that’s S$6.0 billion that CapitaLand has to cough up, which is not exactly spare change. This will be funded by:

- 50% (S$3 billion) will come in the form of CapitaLand shares issued to Temasek. These shares are issued at S$3.50 per share.

- 50% (S$3 billion) will come in the form of cash. This will be funded via debt or other means (but no rights issue or preferential offering).

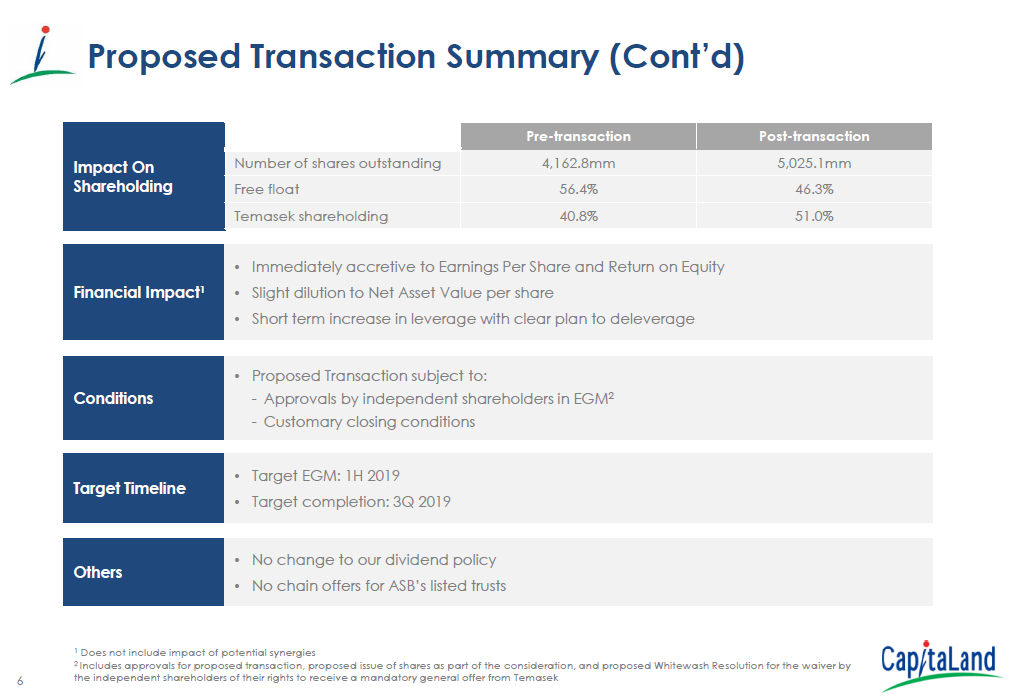

And because this is an interested person transaction (Temasek is a controlling shareholder of CapitaLand), it will be subject to shareholder approval at an EGM, where Temasek is unable to vote. So it’s time for the small guys to shine ;).

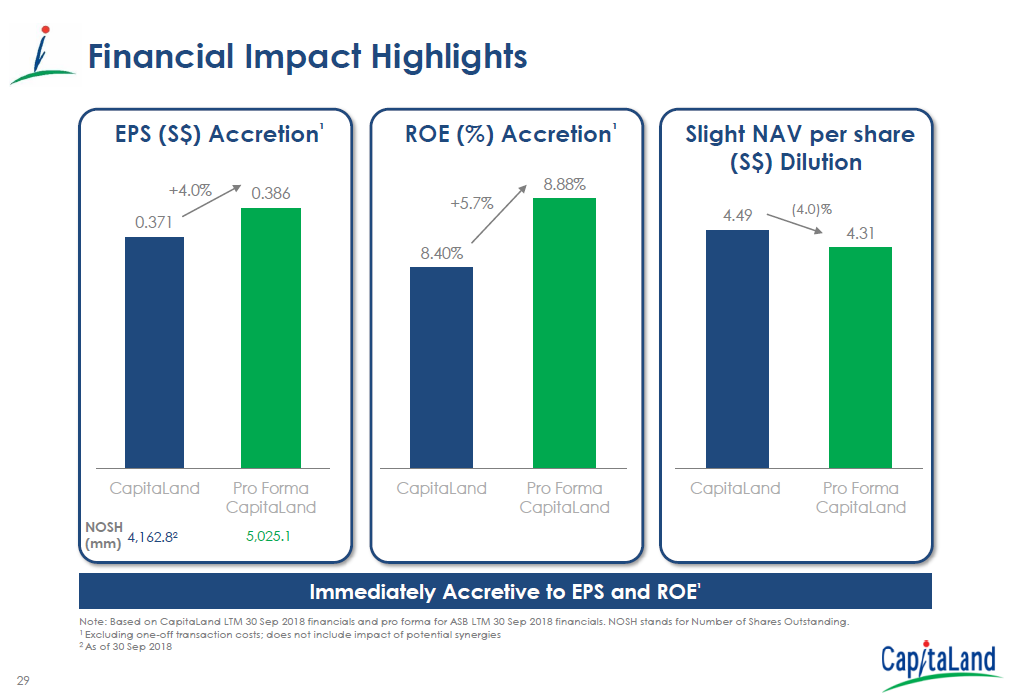

1. Consideration shares look dilutive in the short term

The most immediate reaction, is that this deal may be dilutive for existing CapitaLand shareholders in the short term, because of:

- Price – CapitaLand’s NTA per share is S$4.34 as at Sep 2018, and the new shares are being issued to Temasek at S$3.50 each. The S$3.50 issue price is a nice 7% premium to its current market price, but when compared to the book value, it does seem less attractive.

- Volume – CapitaLand’s current market capitalisation is S$13.6 billion, and issuing S$3 billion worth of new shares is not something to be trifled with.

As shown below, CapitaLand’s NTA as at 31 Dec 2017 was 4.20 per share, and post acquisition it will drop to 3.88, which does illustrate this dynamic.

So in the immediate term at least, there may be a mild sell-off as the market digests this information.

2. What is the right price for Ascendas-Singbridge?

In the medium term though, the overriding concern is going to be this: Is CapitaLand buying Ascendas-Singbridge at a good price? Ascendas-Singbridge is 100% owned by Temasek. As a private company, it doesn’t have to report its financial performance, and there’s no publicly traded shares for us to get a sense of the true price of Ascendas-Singbridge.

We will get more information in the circular to be released, as well as the IFA (Independent Financial Advisor) opinion, but until then, it’s just not very clear whether CapitaLand is overpaying, or getting a good deal here.

3. In the long term, the only thing that matters is execution

The only thing that matters in the long run though, is execution. Whether CapitaLand can properly integrate Ascendas-Singbridge into its fold, and reap the operational synergies that have been promised, will determine whether this transaction will prove to be a success. Don’t forget, CapitaLand itself was created in 2000 by a merger between DBS Land and Pidemco Land, and look how far they’ve come. If they’re able to repeat the same thing here, the current share price is going to look like a bargain.

Historically and statistically speaking though, evidence tends to indicate that when large conglomerates make a large M&A deal, they tend to overvalue the company being purchased, and overstate the cost efficiencies that can be reaped. Such acquisitions never end well. There’s no way of knowing for certain what will happen here, but one hopes that with Temasek being involved, Temasek would have done its best to ensure a sustainable, long term growth path for the new CapitaLand.

4. Is it too late in the cycle for a game-changing acquisition?

The timing of this acquisition is interesting. It comes at a time when the global macro environment has become a lot more uncertain, with a slowdown in China (especially in real estate), and the Federal Reserve seemingly nearing the end of its interest rate hike cycle. At the same time, real estate prices globally are still at record valuations. It does raise questions of whether CapitaLand is making this acquisition at a top in real estate prices.

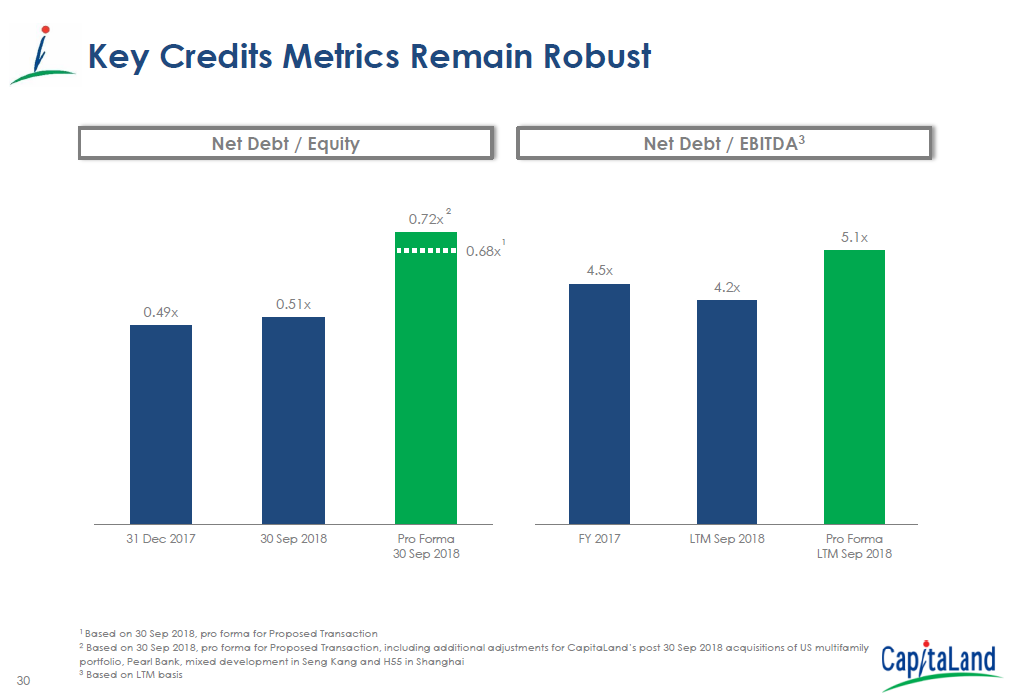

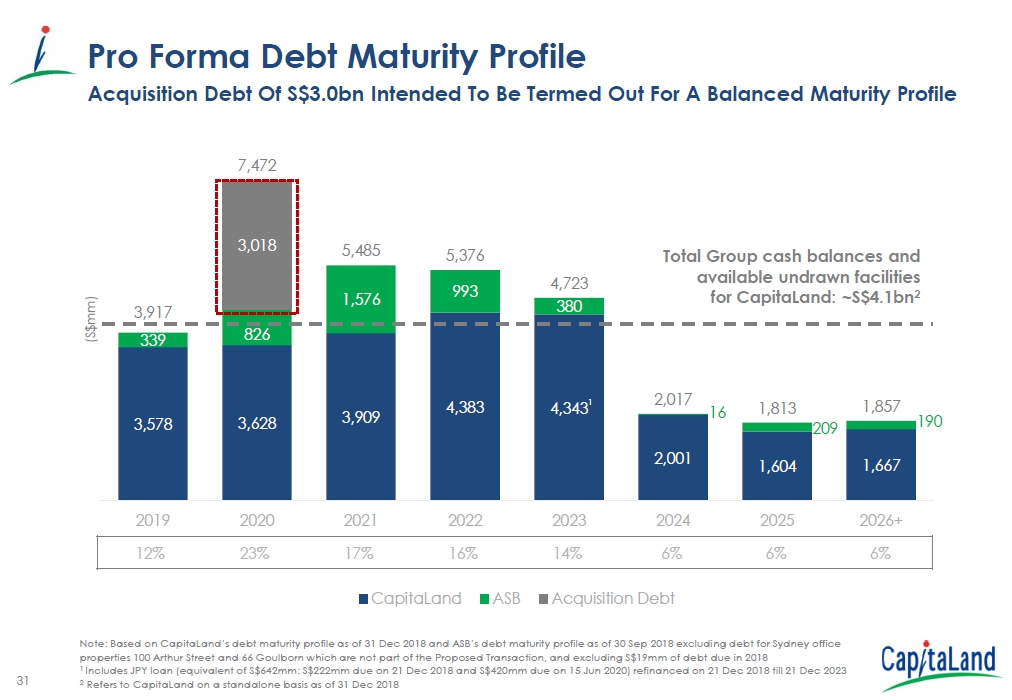

Don’t forget they’re taking on a lot of debt to make this happen (gearing ratio goes up to 72%), and there’s a large amount of debt coming due in 2020. If the market cycle does turn, there could be some challenges here.

Of course, as management you can’t just sit around all day and wait for a market crash, so I fully understand why this acquisition is happening. In any case, even with its elevated gearing, I don’t see any situation where CapitaLand runs into financial difficulties even in a recession. After all, Temasek holds 51% of the “new” CapitaLand. 😉

5. Good news for Singapore Inc

What I will say for certain though, is this. This move is a fantastic one for Singapore Inc. With the newly formed CapitaLand-Ascendas-Singbridge, Singapore will have the largest property developer in the whole of Asia, and one of the top 10 property developers in the world. This puts us on a level playing field with the truly big boys such as PGIM and Blackstone. And in the real estate market today, size, and scale mean everything. Scale allows you to raise financing more cheaply, attract big name institutional investors, have more bargaining power, more access to the juiciest deals, and basically have a seat at the table. As a Singaporean, I’m definitely proud of this move. Well done!

Although that said, I wonder how Mapletree would react. They’ve done amazingly well in recent years, but this CapitaLand-Ascendas merger would place the new CapitaLand on totally different league in terms of AUM size… Interesting times indeed!

Till next time, Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy!

[mc4wp_form id=”173″]

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Currently, temasek owns 51% of Ascendas Singbridge and JTC owns the remainder.

You’re right, thanks for the correction.

Am vested at quite a low price but not excited. Because i think CapLand has over paid (dilution) and bringing in more debts. Pity those who bought at $8 some years ago and still holding and hoping. Uncles and aunties would remember the hype about GLCs then. Many retail lost big thinking GLCs is safe and bao jiat. Good luck. 🙂

Thanks for sharing your thoughts. I personally think that property developers are less “sexy” these days, as one can simply buy the REITs to get access to the best in class properties. But the market is cyclical, perhaps in time developers will be attractive once more.

Cheers.

Nowadays, the ‘meat’ is in the S-REITs 🙂

Developers are under pressure due to the property-cooling measures.

Haha yes I do agree with this. REITs are looking more attractive than developers these days, although that said the S-REITs have rallied quite a bit and are looking pretty pricey right now.

Will capital land share going up or down due to this news.

Logically speaking it should have gone down near term. But on the same day China did a large liquidity injection into the Chinese economy that lifted the share price. That’s how unpredictable day to day price movements are. 😉

Hi FH, insightful thoughts there and I’ve learnt alot from your analysis.

I’m a beginner investor and intend to stock up on Capitaland for the long term, but at a good price(I like the Singapore Inc story too! 😉 )

I was just thinking how to achieve my goal, and I wondered if it is also a tenable strategy now to invest in the ASB related entities (A-REIT, A-HTrust etc.), and then sell these off after the EGM, assuming that:

-Shareholders approved of the deal

-I feel that Capitaland is not overpaying for ASB

-The offer price for the related entities are acceptable to me

Because I understand that in past M&As, historically a target company’s stock usually rises because the acquiring company has to pay a premium for the acquisition. So based on this premise, I foresee that Capitaland is likely to pay a good premium too for ASB post EGM, and therefore more investors are likely to want to buy ASB-related stocks between post EGM announcement until the actual exchange of shares and cash to complete the acquisition. That’s when I intend to sell these ASB stocks.

My grand plan is to then plough the profits back into Capitaland during the mild sell-off that you mentioned.

And even in the unlikely scenario that the deal falls through, I feel its still a gain to me as I’ve been eyeing A-REIT and A-HTrust REITS for sometime now, and wanted to buy these REITS anyway and the prices now are still not too high.

Do you think this is a workable strategy?

Hi there!

Apologies for the delayed replies as I was tied up with other matters. My thoughts below:

(1) The deal is an acquisition of ASB, technically speaking, the listed REITs under ASB shouldn’t move in prices significantly. Of course, market sentiment is a lot harder to predict, but personally I don’t think the ASB REITs will be affected too much by this deal.

(2) I think the chance of this deal is incredibly unlikely, given how these kind of institutional deals are usually done.

(3) In the short to mid term, what might affect CapitaLand/REITs share price even more is likely going to be the macro environment, whether the Feds raise rates, whether the China trade war is resolved etc. You could get the acquisition completely right, but the share price could still move in the other direction because of global macro events beyond your control. So do be aware of that kind of uncertainty when making short term trades.

Not sure if this addresses your questions, feel free to reply with a comment if I didnt!

[…] https://financialhorse.com/capitaland-ascendas-singbridge/ […]