In Singapore, your home is likely to be an important asset.

How should you protect your home?

Not only can you protect your home from major accidents such as fire, you can also protect its contents.

You can even cover your pet if something happens to your home.

Let’s explore the types of home insurances that you can consider to protect your home.

This article was written by a Financial Horse Contributor.

1. Home insurance for HDB

For HDB owners, there are two compulsory types of home insurance:

- Home Protection Scheme (HPS)

- HDB Fire Insurance Scheme

The Home Protection Scheme (HPS) is a mortgage-reducing insurance that protects you and your loved ones from losing your Housing and Development Board (HDB) flat in the event of death, terminal illness, or total permanent disability. It insures members until they turn 65 years old, or until the housing loans are paid up, whichever is earlier.

In the unfortunate event of a claim, HPS will settle the outstanding housing loan, up to the sum insured, with HDB or the mortgagee directly.

The HDB Fire Insurance Scheme offers additional peace of mind from the cost of repair works in a fire.

The current appointed insurer for the HDB Fire Insurance Scheme is FWD Singapore Pte Ltd and the insurance is valid for a five-year period.

HDB fire insurance is compulsory for all flat owners who have an outstanding HDB loan. The insurance is valid for a five-year period and must be renewed once every five years.

Third-party insurance

In addition to HPS + HDB Fire Insurance Scheme, it is recommended to obtain extra home insurance for enhanced protection of your home contents.

For instance, AIA offers a plan for HDB home owners. The Enhanced Public Housing Contents Insurance (EPHCI) covers:

- Damage/loss due to fire, burst water pipes and more

- Personal liability cover

- Alternative accomodation

- Bill relief protector

- Complimetary home care services such as locksmith, plumber, electrician, aircon repair etc.

and more.

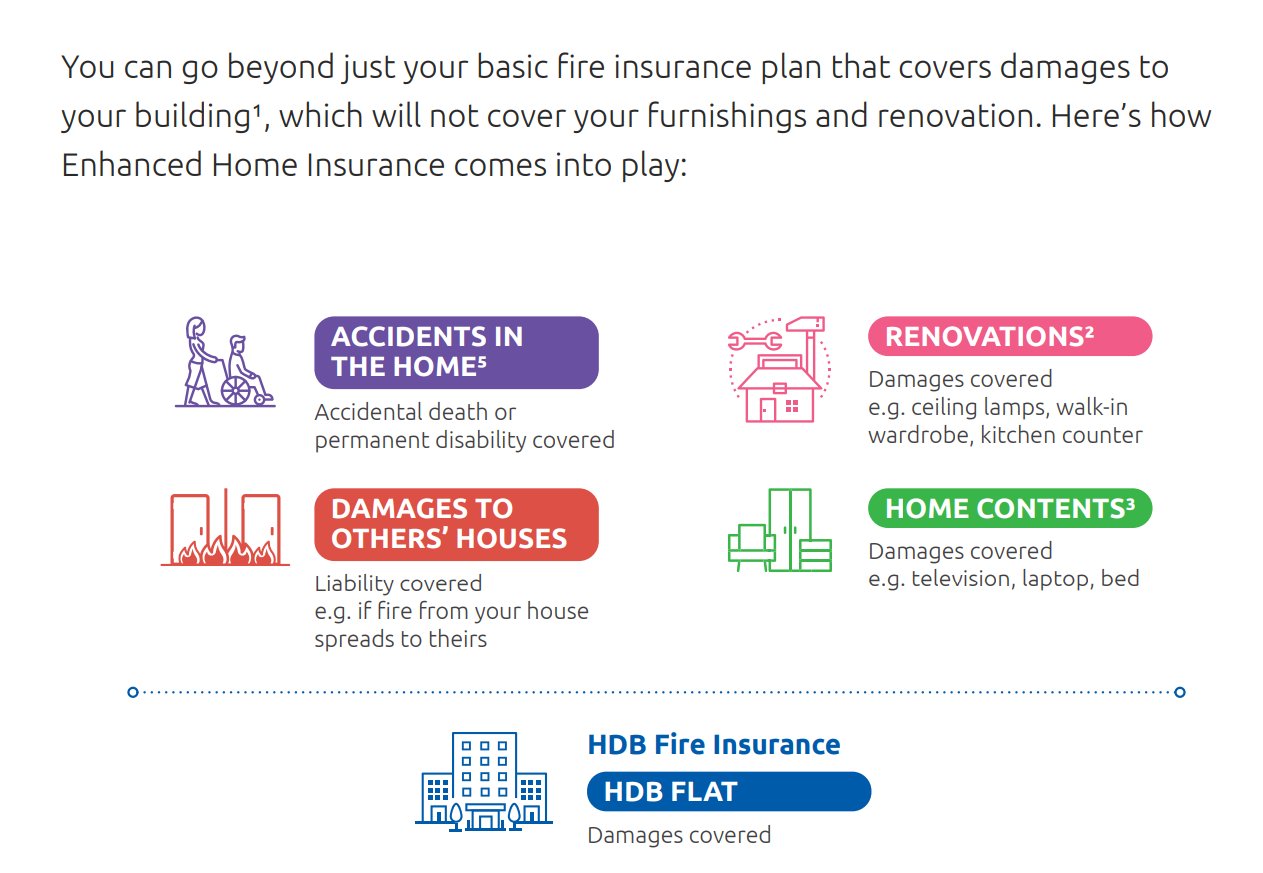

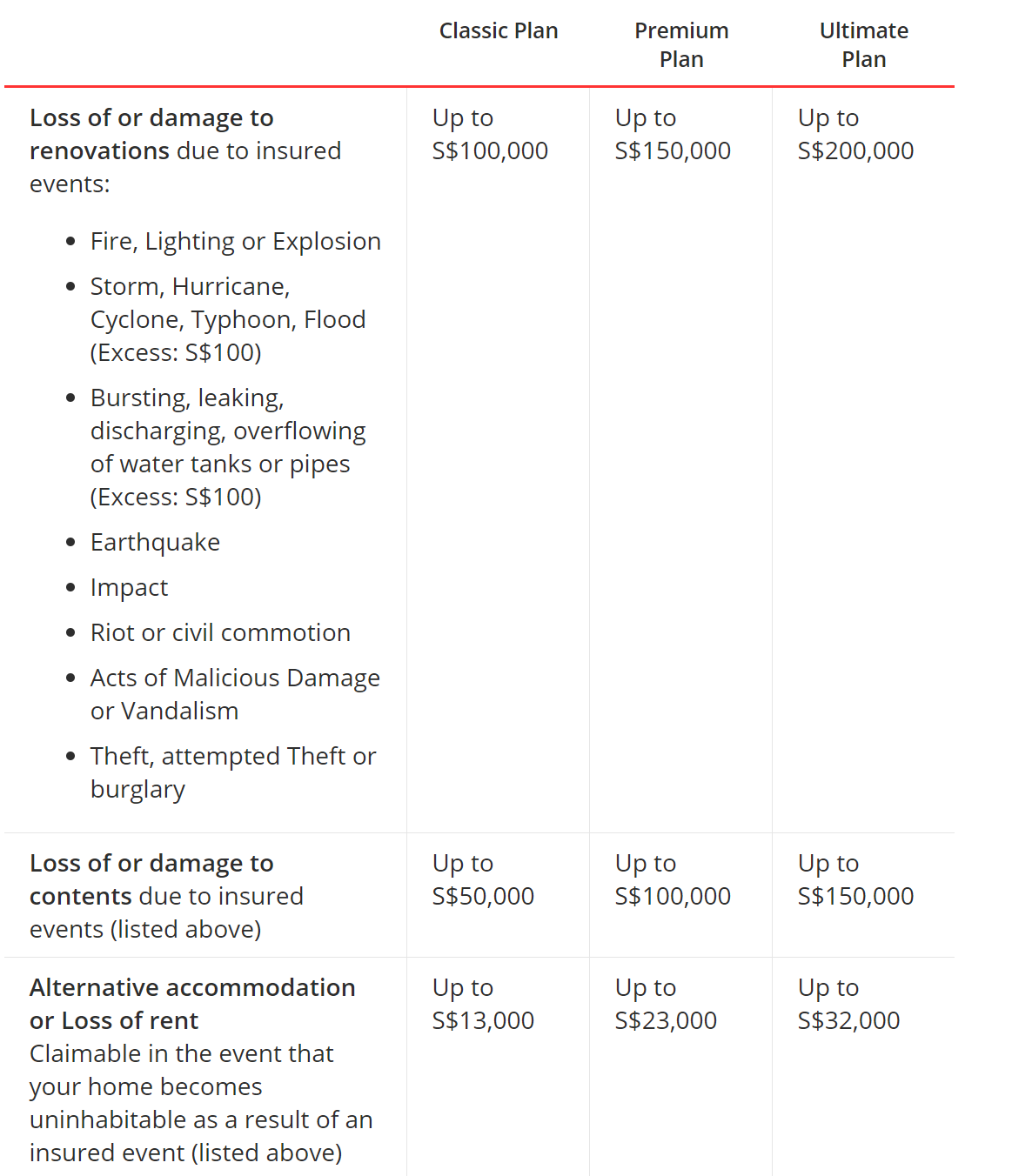

NTUC Enhanced Home Insurance provides flexible plans to protect your home, including the building, renovations and contents.

2. Unforeseen events

Home insurances typically cover unforseen events that cause damage to your home and its contents.

For instance, with Great Eastern’s HomeGR8 Essential, you can protect your home rom events such as fire, smoke damage, burglary, flood, bursting of water tanks or pipes.

- Household contents: any movable household items in your home or on the building (such as furniture, electronic appliances) and personal belongings (such as clothes);

- Renovations: Any fixtures, installation, addition, home improvement or decoration in your home (including the building) such as flooring, built-in wardrobes and air-conditioners.

- Building: the physical structure of your home (including renovations within your home).

- For HDB homes: Internal building structures, fixtures and fittings, as provided by HDB and/or its approved developer

- For Private homes: Building structure of the apartment or landed property that you own (including any garages, gardens, gates & fences situated within the landed property premises)

Insurance plans typically also even cover costs of alternative accomodation if you can no longer stay in your home.

For instance under DBS’ myHome Protect II, you can claim for loss of rent, or incurring costs for staying at an alternative accommodation.

3. Valuable contents

For home owners with a high amount of valuable items, it is also worth considering comprehensive coverage for your items.

HSBC’s HomeSure provides up to SGD 300,000 for renovations, movable household items and personal belongings.

You can get coverage for:

- home contents and renovations

- emergency home assist

- alternative accomodation

- temporary furniture storage

- removal of debris

- replacement of lock/keys

- accidental death of domestic pet

- loss of personal money due to burglary

- accidental breakage of fixed mirrors and glass

- deterioration of frozen food

- damage to security systems

and more!

If you have expensive watches, art or antiques, be sure to check the coverages of your plan.

Otherwise, you may only be able to recover up to a standard amount per item.

4. Renovation claims

Home insurance plans cover renovation claims.

This could include flooring, built-in wardrobes and kitchen cabinets.

5. Mortgage

You can also get insurance to cover mortgage payments.

eTiQa’s ePROTECT mortgage takes care of your remaining mortgage payments should untimely events happen to you

- Flexible policy term of 6 to 40 years, or up to 75 years old

- Pay only 90% and get covered for 100% of your policy term

Do note that these plans can be quite expensive, and you would need to do your own cost benefit analysis to see if such plans make sense for you.

6. Tenants

There are also home insurances for landlords and tenants.

For landlords, home insurances can cover loss of rent.

For tenants, while home insurance is not compulsory, you may wish to consider insurances to protect yourself.

For instance, under FWD’s plan, if you’re a tenant, you’re covered for loss or damage to the building renovations and home contents.

FWD even provides coverage if your pet dog or cat is stolen or is injured due to an insured event that happens at your home.