2020 has been one hell of a year so far. January is barely even over, and we’ve already had a close shave with WWIII, Australian wildfires, Locusts in Africa, Kobe Bryant’s passing, and now the Wuhan Corona Virus. I’ve had enough excitement for the year, thank you very much.

And amidst all that chaos, comes Elite Commercial REIT’s IPO. I had a healthy dose of scepticism about Elite Commercial REIT when going through the preliminary prospectus (as evidenced in my original article here), but now that the final prospectus is out, I actually quite like this REIT.

Basics: What is Elite Commercial REIT?

Elite Commercial REIT is a small cap ($230 million aprox) REIT that holds commercial office buildings in UK. A total of 97 commercial buildings to be precise, scattered all over the UK, as set out below.

Gearing on launch will be 33.7%, and indicative yield is 7.1%, price to book is about 1.03x approximately.

Sponsor

Let’s start with the stuff that I don’t like about Elite Commercial REIT.

One of the big doubts I had in my original article was what the stakes of the sponsors would be like post-listing, and what the alignment of interest would be like.

Well, the numbers are set out below, and it looks a lot like the biggest unitholders are paring down their stakes, on a percentage basis.

The sponsors will collectively hold around 19% of Elite Commercial REIT post listing (assuming over-allotment option is exercised – which is likely given the small public offer). It’s a decent stake, but I would have preferred to see something much closer to 30%, along the likes of what CapitaLand and Mapletree do.

The cornerstone investors that will take up a huge chunk (23.4%), is private wealth, coming via UBS, Bank of Singapore (OCBC) and CIMB. I would have preferred to see big institutional names like Blackrock and the likes come in rather than private wealth, since greater ownership by private wealth typically results in greater volatility in share price.

But to be fair, given the small size of Elite Commercial REIT’s IPO, I can’t really fault the big boys like Blackrock for not wanting to come in.

Another thing to note is that this is the first REIT sponsored by Elite Partners, so we don’t have full clarity on their track record. A couple of the guys behind Elite Partners were from the original Viva Industrial Trust / Cambridge Industrial Trust (sold to ESR eventually). Both Viva and Cambridge Industrial did okay as a REIT, so hopefully that track record carries over here.

Forex Risk

Forex risk is another huge one here.

The underlying properties are located in the UK, so naturally they are denominated in British Pounds (GBP), as are the distributions.

The long term chart of the GBP against the SGD is set out below, and it’s not pretty.

IPO prices use the prevailing exchange rate of S$1.77 to 1 GBP, but frankly speaking, the exchange rates over the next 12 months can go anywhere. I’m not even going to bother trying to forecast where it will go because that’s how uncertain it is.

Sensitivity analysis is set out below. A 5% appreciation of the SGD against the GBP (S$1.68 to 1 GBP) drops distribution to 6.7%. Given that we were looking at S$1.65 to 1 GBP a year or two ago during the depths of Brexit, this isn’t completely out of the question.

Book Value

Now the portfolio of 97 properties was acquired by the Sponsor back in Nov 2018 for £282.15 million. And as many other investors have noticed, the fact that they’re IPO-ing them at £319.1 million now for a 13% paper gain looks pretty convenient.

To be fair to them though, November 2018 was the depths of the Brexit situation, and the forex was at $1.66 back then. The forex alone has appreciated 6.6% since then, which accounts for half of the valuation gain. To attribute the rest of the valuation gain to stabilisation in the political climate and forward outlook, is not completely out of the question.

If we accept the appraised value of the IPO portfolio, we’re looking at an IPO price of 1.03 times book value. If we use the price that this portfolio was acquired back in Nov 2018, we’re looking at a P/B of 1.16.

Personally though, I think the valuation gain is fair because of the improved Brexit situation, and most of the cap rates in the valuation reports range from 4% to 12%, which again looks reasonable. So I’m happy to accept the P/B of 1.03 times at face value. But you’re free to use the higher number if it makes you more comfortable.

Properties

So that’s all the stuff I don’t like about Elite Commercial REIT.

Now let’s move on to the stuff I actually like.

And what I really like, is the structure of this IPO portfolio.

To put it simply, the entire IPO portfolio is leased to the UK government (Department for Work and Pensions) on a long term 10 year lease. So in a way, the underlying distributions are backed by the creditworthiness of the UK government, for as long as the leases are in place. That’s just fantastic.

But how long are the leases are in place you ask:

“A majority of the Properties’ lease agreements are due to expire in 2028, and certain lease agreements contain an option for the tenant to terminate in 2023.

A majority of the Properties’ lease agreements are due to expire in 2028, and certain lease agreements contain an option for the tenant to terminate in 2023. Such Properties which have lease agreements that contain the option for the tenant to terminate in 2023 account for approximately 70.0% of the total Revenue of Elite Commercial REIT. As a result, Elite Commercial REIT’s Revenue may be adversely affected if the majority of these leases are not renewed or if Elite Commercial REIT is unable to source for suitable replacement tenants.

However, the Manager considers it unlikely for the UK Government to not renew its lease agreements for the majority of its Properties as the Manager believes that the IPO Portfolio is crucial public infrastructure for the provision of DWP services. Nevertheless, if the UK Government decides not to renew its lease agreements for the majority or all of the Properties, the Manager will seek to find suitable replacement tenants. The Manager believes that it will be able to find suitable replacement tenants as the (i) the Properties are well located (i.e. largely located close to amenities and public transportation), (ii) the Properties may be easily converted for other uses (i.e. other commercial uses of the Properties other than a job centre, call centre or back office) and asset enhancement opportunities are widely available, and (iii) the Properties are located across the UK and not concentrated in a single region.”

Long story short, most of the leases expire in 2028, with 70% having the right to terminate in 2023, but the REIT Manager thinks it unlikely the UK Government will terminate the lease agreements early. I’ve lived and worked in the UK for a bit, and from what I remember about British efficiency, I absolutely agree with the REIT Manager on this. I think the chances of the UK government terminating these leases early are terrifically low, but of course non-zero.

According to the REIT Manager, the properties are located in fantastic locations near bus stops and supermarkets. I haven’t been to any of them so I can’t comment on this. From what I remember about the UK, there are supermarkets and busstops at every street corner, so I’m not so sure how helpful this is.

Yield

Yield is also really attractive at 7.1% for FY2020, and 7.2% for FY2021.

The leases also have build in rental escalations that provide for embedded revenue growth:

In addition, the leases to the UK Government have in-built rental escalations every five years based on the UK Consumer Price Index (“CPI”), subject to an annual minimum increase of 1.0% and maximum of 5.0%. This provides the IPO Portfolio with a relatively predictable, embedded rental growth profile, with CPI forecast to increase at an average of 2.1% p.a. from 2020 to 2022

Given that the 10Y Gilt is trading at 1.1%, this is a mind-blowing 600 bps spread against the risk-free. In fact, I can see a lot of high net worth individuals using this as a leverage play, given the stability of the underlying cash-flows.

Fee Units

One interesting thing to note about the yield is that because the manager fees are paid in units, the cash yield is artificially juiced up. The sensitivity analysis is set out below, and if all fees are paid in cash, the distribution drops to 6.3%.

The way I see it though, I only care about actual cash in my hands, and as an investor, as long as I’m getting 7.1% yield I’m good. The impact from the fee units only starts to come in in the longer term. So I’m comfortable to accept the 7.1% yield as a headline number, while understanding that the natural yield is actually 6.3%.

Tax Expense

Another interesting thing about the yield is on tax treatment.

I’ve extracted this great segment below, but basically what Elite Commercial REIT is saying is that there will be a new law that reduces corporate tax to 17% on 1 April 2020, but Boris Johnson in his campaign speech said that they will undo this change and keep taxes at 19%. The numbers in the prospectus are based conservatively on 19% tax rates, so if Boris Johnson doesn’t actually go through with the changes, then there is potential upside here – distribution goes up to 7.2%.

That’s a nice to have.

Tax expense consists of current and deferred tax expenses. The current tax expense is based on the prevailing UK corporate tax rate of 19.0%. The deferred tax expense relates to the capital allowances claimed and fair value gains on investment properties and has been provided based on the UK corporate tax rate of 17.0%, being the enacted tax rate at the respective reporting dates as the UK Government had announced a reduction to the corporation tax rate from 19.0% to 17.0% with effect from 1 April 2020.

It should be noted that during the campaign for the 2019 UK election, the Conservative Party (which won the election in December 2019) had mentioned that it intended to maintain the UK corporate tax rate at 19.0% and did not intend to proceed with the planned reduction to 17.0% in April 2020. Such change, if any, is likely to be announced in the UK Budget which is due to take place in March 2020. Further details are set out in the section “Taxation”.

Borrowings

Borrowing is a single £120.0 loan facility, expiring in 2024 so no refinancing risk for the time being.

Interest rates are:

The Manager has assumed the average effective interest rate for Forecast Year 2020 and Projection Year 2021 to be approximately 2.30% and 2.29% per annum respectively, excluding the amortisation of debt-related upfront fee and transaction costs, and commitment fee.

Nothing out of the ordinary here.

What are you getting with Elite Commercial REIT?

Let’s sum up. What you are getting with Elite Commercial REIT, is a 7.1% yield in GBP, backed by the UK Government, that lasts until 2028. There’s the option to terminate in 2023, but it’s realistically quite unlikely. After 2028, Elite Commercial REIT’s preference will probably be to extend the leases with the UK Government, but that’s subject to negotiations, and also 2028 is heck of a far away so it’s hard to predict what happens there.

There’s some questions over alignment of interests, track record of Elite Partners as a sponsor, and future pipeline / growth of Elite Commercial REIT, but there’s not much we can do on that front other than to work it into the price.

Do I like it?

Personally speaking, I actually quite like Elite Commercial REIT. I like the stability of cash flows out to 2028 and I like the 7.1% yield. I don’t like the fact that it’s small cap, I don’t like the uncertainty over alignment of interests, and I’m not so sure how future growth will play out.

But hey, it all comes back to price right? And at 7.1% yield, I think the risk-reward could be pretty compelling.

Elite Commercial REIT v Wuhan Virus

There’s just one problem here. And it’s the Wuhan Corona Virus. I don’t see this impacting Elite Commercial REIT much given that these are UK properties and long leases to 2028, but I see this impacting the rest of the market. In fact, what I see is this impacting China and China related stocks really hard.

So short term that creates a problem for me. I’m already preparing funds to deploy into the market for when the China related selloff deepens, so any money I put into Elite Commercial REIT is money I’m not putting into my China warchest. The question then becomes one of opportunity cost. Will my China investments achieve a return in excess of 7.1% a year? If so, it becomes a no brainer and I skip Elite Commercial REIT.

If it doesn’t, then I might as well put some money into Elite Commercial REIT and spread out the risk, given how stable the underlying cash flows are here.

Closing Thoughts: Hey FH, are you subscribing?

It’s a really interesting dilemma. 2 weeks ago I would have put money into Elite Commercial REIT no questions asked, but right now, I’m not so sure.

In any case, I don’t have to decide yet. The offer closes at noon on Tuesday, 4 Feb, and given how rapidly the Wuhan Virus is playing out, I’ll be a fool to make a decision now. I’m going to let this play out more, and decide by Monday 3rd Feb if I want to commit some capital to Elite Commercial REIT. Public offer tranche is only 5.7 million units anyway, so they’re probably going to be hard to get.

I’m giving Elite Commercial REIT a 3.5 star rating because objectively, I think this is a pretty sound REIT. If you can put up with the small size, the uncertainty over future growth and sponsor treatment, there is a very solid 7.1% yield to be had here. There’s some forex exposure no doubt, but if you’re investing in UK properties, you want that exposure anyway.

For the guys who love to buy a flat in Central London, Elite Commercial REIT could be a great (and possibly safer) alternative.

For me though, I haven’t made up my mind on whether to put some money on this. I’ll still want to see how the China related stocks trade over the next few days.

Update (1 Feb 2020): I’ve decided to skip this IPO – you can check out my updated thoughts here.

What about you guys? Are you subscribing for Elite Commercial REIT’s IPO? Share your comments below!

*Reminder*

Back by popular demand, we’re launching a Chinese New Year promotion for the FH Course, at a discounted price of $288. The CNY promo ends this weekend! For those of you who missed the Christmas promo, now’s a great time to grab it!

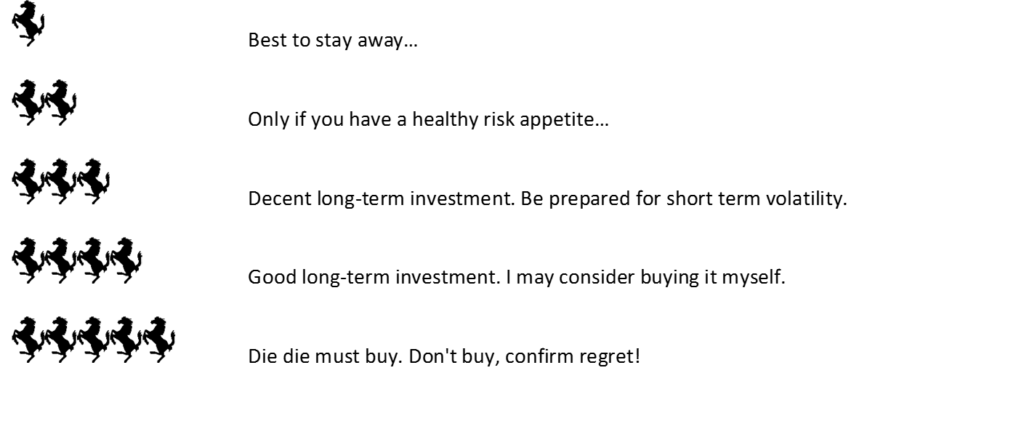

Financial Horse Rating – Elite Commercial REIT IPO

![]()

Rating Scale

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Like the Financial Horse Facebook Page and join the Facebook Group (Singapore Stocks) or Facebook Group (China/HK Stocks) to continue the discussion!

Sorry, may I know whether property owner has inflated valuation for 13% within 9 months (not 1 year & 3 months as mentioned)? Bought in Nov 2018 but date of valuation being 31 Aug 2019 according to Prospectus

Hi!

Valuation reports are as at 31 Aug but investors are buying in at IPO day using the IPO price. So the correct “inflation” will be original price on Nov 2018 against IPO day price, which is approx 13%+.

Hi FH, thank you for your detailed analysis. For me I feel that the brexit situation poses the most uncertainty. We have no doubt UK will be leaving the EU but can they leave on the terms they want? Given 11 months is unlikely to agree on a comprehensive trade deal between the EU and if Boris Johnson insists on not extending the deadline, here might be a no deal brexit happening which will impact the Sterling and affect local businesss(many of the bigger/international business had already moved operations or made preparations since the referredum).

Also, UK also faces the possiblitiy of it falling apart should northern Ireland leave or Scotland leaves.

I would wait closer till Nov-Dec 2020 then decide. But by then if the situation does really become better, then the gains would be much lesser. No risk, no gains.

Just my 2 cents: china may be better for now.

Thanks for sharing Fatty Finance, this was helpful for me in my decision making too. I agree that once the risk level drops with certainty over Brexit, the yield on these things should technically drop as well.

Yeah I think China is really interesting too, but for now I’m leaning towards putting some small money in this REIT and treating it as a long term UK bond. But we’ll see how things play out over the weekend.

Hi FH, thanks for the detailed writeup.

If I do participate, this would be my first time applying for an IPO denominated in a foreign currency. When it comes time to sell from CDP (e.g. using DBS Vickers, or OCBC), does this mean that I will have to set up an account denominated in pounds, for that particular bank?

Hi! No worries hope it’s helpful for you.

No the broker will automatically change the pounds into SGD and deposit the SGD into your CDP-linked account. 🙂

Hope that this helps!

Hi FH,

Have you made a decision if you are going to be subscribing to the IPO? or do you see China as a better opportunity given the reports of outbreaks of bird flu over the weekend?

Hi 🙂 Updated post here: https://financialhorse.com/elite-commercial-reit-ipo-update-why-i-decided-to-skip-this-ipo/