As you guys will be aware – the FH Stock / REIT watchlist went out over the weekend.

So my views on single stocks are in the watchlist.

In this article, I wanted to do a more high level survey on how I see the market generally today.

I’ll broadly split the article up into 2 parts:

- How do I see the market today?

- Where does value lie?

This is an FH Premium post written in Jan 2025, that I am making available to all readers.

If you find content like this helpful, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

How do I see the market today?

I came across a very interesting article from Bridgewater over the weekend.

Basically, Bridgewater discusses the 3 big markets of US, China and Europe, and shares their views on how they see the macro outlook for both, and how assets are priced relative to the outlook.

Full article here, and it’s worth the read if you have some time.

I’ll discuss each of the 3 markets below.

I’ll start with the Bridgewater summary, and then share my personal view.

US

Bridgewater’s views on the US?

Per the article:

In the US: Short-term cyclical dynamics are sustaining nominal spending at too-high levels, while the advent of mercantilist policy (e.g., tariffs, targeted fiscal measures, restrictions on immigration, stimulus in China) tilts the risks of inflation higher. To “have it all” (i.e., the currently discounted mixture of high profits, low inflation, high wage growth, and easing) against this backdrop requires sustained, high productivity growth, which an AI revolution makes possible but does not ensure. From a long-term debt cycle perspective, debt burdens have shifted from the private to the public sector and are once again manageable via interest rate cuts, leaving us in an interesting configuration where monetary easing and private credit creation can support growth, but the sustainability of fiscal spending is in question.

…

In terms of policy tools to navigate future downturns: monetary and fiscal policy are both available but are about one bad cycle away from exhaustion. From a standing start, there is no particular limit on either monetary policy or fiscal policy, but once they are utilized over time in one way or another, limits can be reached in terms of their usability. After 30 years of cutting interest rates from 1980 to 2010, the ability to use interest rates to stimulate in the US and other economies reached its limits because debt burdens were too high and rates hit 0%. That required a shift to what we refer to as MP2, i.e., QE, which during the pandemic by and large reached the limits of its effectiveness to stimulate growth. That led to the need for MP3 and fiscal policy to reflate the economy post-pandemic, which hit initial limits in the form of inflation and which, due to the expansion of government debts, are pulling forward the future limits of government debt sustainability. The good news is that the rise in interest rates that was required to fight inflation gives the US room to ease through interest rates again, and healthy private sector balance sheets may be more responsive to that easing than pre-COVID. But we are essentially one big easing cycle away from rates being back at zero. If at that stage fiscal sustainability becomes an issue, then, depending on the severity of the issues to be managed, a future downturn could require more drastic steps than fiscal stimulus, such as debt or monetary restructuring, to get the desired results.

In any configuration of future conditions, US assets face a significant hurdle to sustain outperformance. On an outright basis, the backdrop of easing, strong growth, and limited inflation is positive for US assets. What is more challenging is for US assets to repeat a decade of outperformance like they have just experienced. At their current level of global market capitalization, US stocks need to attract ~65 cents of every dollar that flows into stocks just to keep rising. And the pricing sets a high hurdle for these flows: in 2010, US earnings were discounted to grow modestly and at a similar rate to the rest of the world. The US then had an exceptional decade because its companies were more dynamic, had more supportive governance for shareholders, and operated against a more favorable policy backdrop. That’s all still true, but it’s also the case that US equity indexes and bond markets are extrapolating very fast earnings growth outright and versus the rest of the world, as well as stable inflation. The outcome that could square this challenge would be if the US captures the lion’s share of benefits of the AI revolution over time, both pushing back its structural inflationary limits via sustained high productivity and driving substantial profit growth. That outcome is possible but far from assured, and we’re tracking it closely in our AI research.

Bridgewater’s views on the US? – in Plain English?

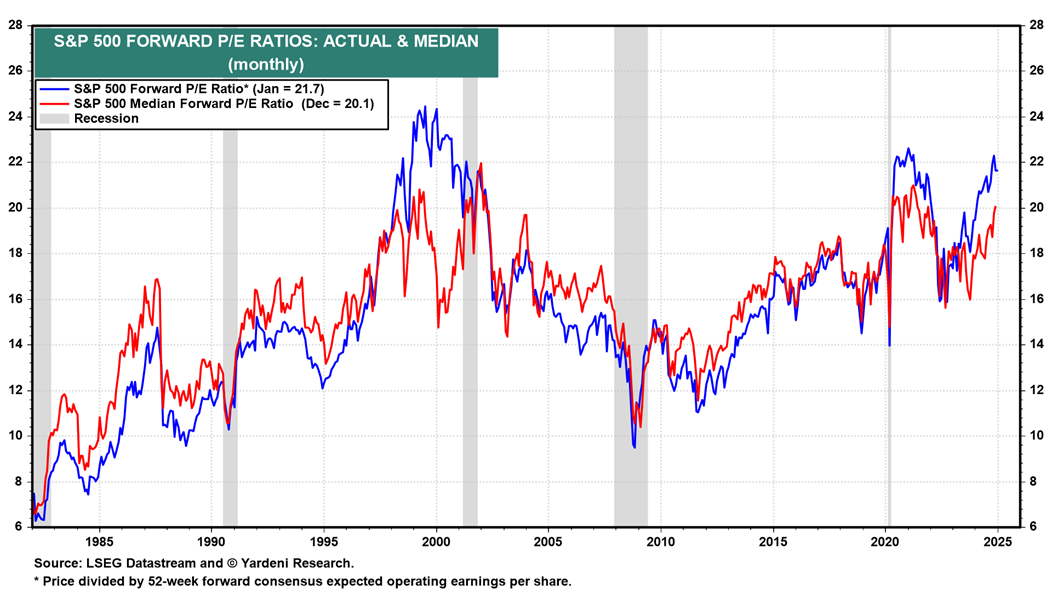

What Bridgewater is saying (which I have been saying as well), is that US assets are not cheap today.

US assets are pricing in a very optimistic macro future – which means that the future needs to be at least as good as what is priced in, otherwise there is downside risk.

Of course, this is not impossible, because:

- Under Trump you have a very pro-business president

- There is room to cut interest rates (if required)

- Private sector is not excessively overleveraged (unlike 2008)

- AI spending has the potential to create a new capex / productivity boom

At the same time, there are risks because if Trump goes too crazy with the fiscal spending, you could see resurging inflation (which will require higher interest rates from the Feds).

And if Trump goes too crazy with the tariffs, it could create a global economic distortion (in who wins and who loses).

And AI spending – well it remains to be seen if AI will indeed spark the productivity gains to justify the massive capex spending.

My views?

Generally speaking, I agree with most of the points above, and it’s what I’ve been saying for a while.

The nuance I would add, is that while US assets are expensively priced, it’s also at a point where if you don’t invest in the US – which other market today can offer as attractive potential returns going forward?

China has their own problems, as does Europe (we discuss both later), and Singapore is pretty much just banks and REITs.

My view is that ultimately investors today still have to allocate to the US.

But you have to go in with your eyes open.

Understand that US assets today are not cheap and price in a very optimistic outcome.

So size your position accordingly, and manage your risk with this in mind.

But I think it’s hard to say that as a global investor you run zero exposure to the US, because the US remains one of the most dynamic economies today (no doubt there are risks).

Follow Financial Horse to avoid missing any post!

Bridgewater’s views on China?

Per the article:

In China: Deflationary pressures from the long-term debt cycle are weighing on credit growth, leading to very weak nominal spending, which is too low by about half. Stimulus is needed to transition from what is now an ugly deleveraging, which is good for bonds but bad for just about everything else, to a beautiful deleveraging that stabilizes conditions and supports a movement of money from cash to assets. China has endured years of deleveraging because, in contrast to the US, it did not monetize unsustainable private and local government debts; instead, it used mercantilist production-side stimulus to support healthy industries and national champions. But now signs are emerging of more proactive central government fiscal support, which is needed more than ever as proposed tariffs threaten China’s export-driven growth model. Almost any stimulus is likely to support Chinese assets, as its stocks are discounting a depression and bonds are not discounting much easing. Exactly which assets will benefit, as well as the ripple effects for global spending, will depend on the effectiveness of policy choices.

…

China is still working through a long-term debt cycle deleveraging, and it’s ugly. China’s private sector and local governments are over-indebted, choking off growth. The interest rate lever by itself is not enough to drive spending sustainably above debt service, both because the burdens are large relative to incomes and because lowering rates may have undesirable consequences, such as increasing debt growth in the real estate sector or putting pressure on the renminbi. Most stimulus to date has come through “targeted” fiscal measures aimed at raising industrial production rather than broad demand, in view of the challenges above as well as policy makers’ stated desire to shift the composition of growth toward higher-value-add “new economy” sectors. The effect of this policy has been to capture manufacturing share from the rest of the world and raise political ire, but not to pull China out of its deflationary rut. The good news is that China’s central government, unlike its private sector and local governments, is not indebted, and policy makers have the ability to stimulate through that channel if there is the will to do so.

Nominal spending in China has been too low by half, necessitating more stimulation. China needs roughly 6-7% nominal spending growth but has been running nominal spending around 3.5%. That nets growth around 4% with intolerable deflation that is making economic problems worse, especially in the indebted real estate sector and by hurting corporate profits and sentiment, resulting in a self-reinforcing downward spiral. The path forward to sustained 6-7% nominal growth (i.e., the 5% real growth target plus acceptable inflation) is undefined at this point. But recently, the central government has made commitments to take additional steps to stimulate broad demand. It hasn’t said it will do “whatever it takes” to generate growth, although that is what is implied, and we’re tracking the scale and mechanics of stimulus announcements closely.

However policy makers choose to proceed, it is likely to be supportive for Chinese assets. In studying dozens of reflations across hundreds of years, we see that policy makers tend to get the conditions they want, and that getting there requires making assets attractive relative to cash. But which assets will do well over what timescale depends on the policy mix and the resulting economic conditions. In the US, the “beautiful deleveraging” policy mix used since 2008 created demand through a combination of monetary easing, QE, and fiscal stimulus. It was pro-growth without being too inflationary, contributing to an extraordinary rise in the stock market. In China, the approach of relatively restrained macroprudential policy, targeted fiscal policy, and some liquidity provision since COVID has resulted in low growth, grinding disinflation, and a substantial decline in the stock market but a huge bond rally. Looking forward, both Chinese stocks (which are discounting a depression) and Chinese bonds have the potential to benefit if policy makers stimulate vigorously.

Bridgewater’s views on China? – in Plain English?

Not to blow my own trumpet, but this is broadly in line with what I’ve been saying about China.

Namely – China is in a deleveraging cycle, that is threatening to descend into a deflationary spiral (like the US 1930s Great Depression).

The 2 ways out for them, to replace the real estate hole – are either (a) manufacturing / export growth, or (b) drive domestic consumption.

(a) has its limits in a post-Trump world, but no doubt China will push on it to the extent that is possible (and this is what we have seen the past few years).

(b) is what is truly needed, but it has implications for China’s manufacturing competitiveness (higher labour cost), and so far has not been undertaken to the extent required to offset the deflationary spiral.

My views?

But as the debts are RMB denominated, it is fully within the power of Beijing to stimulate – the only question is will they do it, when will they do it, and how will they do it.

But as Bridgewater puts it very succinctly – “Almost any stimulus is likely to support Chinese assets, as its stocks are discounting a depression and bonds are not discounting much easing. Exactly which assets will benefit, as well as the ripple effects for global spending, will depend on the effectiveness of policy choices.”

The contrast could not be more stark with the US.

Whereas in the US a lot of good news is priced into stocks. So you need a future that is better than priced in, for further upside.

Whereas in China, a lot of bad news is priced in. And you just need a future that is not as bad as what is priced in, for further upside.

Bridgewater’s views on Europe?

Per the article:

Europe remains in a state of long-term stagnation, losing the productivity and tech battle to the US and the manufacturing battle to China. While real growth looks stable around potential as ECB easing pumps growth into the periphery, replacing declining fiscal support, European powerhouses Germany and France face export stagnation and debt challenges, respectively. The risks to economic growth are tilted downward as we pencil out the likely impact of tariffs on the bloc and the challenges faced by Europe’s weak central institutions in formulating a domestic fiscal or international mercantilist response.

…

Europe risks stagnation unless it can better manage political constraints on economic policy. Europe’s deleveraging from the sovereign debt crisis depended on the strength of core economies like Germany and France, which benefited from export growth and increased fiscal spending, and ECB support to offset weakness in periphery countries and austerity throughout much of the bloc. Today, those conditions have turned on their head: growth in Europe’s periphery is moderate, but European conditions are weak overall because German exports have stagnated in the face of Chinese competition and France faces a debt reckoning. The ECB’s recent tightening cycle and Germany’s low government debt levels should in theory give policy makers room to maneuver and stimulate. But rapid, game-changing stimulus is unlikely given political constraints: at the country level, Germany has to contend with fractious politics and its “debt brake.” At the EU level, there is not enough pain to generate the political will that would be needed to reconsider the Stability and Growth Pact. The net of this: there is more inertia in Europe for events to take their course without meaningful policy intervention. That is worsening the dislocations that lost Europe the productivity battle to the US and the manufacturing battle to China over the last 10 years. The challenges created by this lack of coordinated policy making are worsening as global policy takes on a more mercantilist character and Europe faces industrial policy challenges from the US in addition to those it is already managing with China.

Bridgewater’s views on Europe? – in Plain English? My views?

The summary pretty much hits it on the head.

Effectively – Europe “remains in a state of long-term stagnation, losing the productivity and tech battle to the US and the manufacturing battle to China”.

There are structural challenges for the key markets of UK, Germany and France in declining productivity / competitiveness, while European leaders are not sufficiently competent to lead the bloc out of the current malaise, all while the superpowers of US/China are squeezing them on both sides.

Just look at the AI battle for an example.

While US and China are racing neck and neck to develop cutting edge models that will dominate the future industry (US is even restricting Chinese access to NVIDIA chips to blunt their advantage).

Europe is non-existent in this race, and instead market leader in regulating AI.

This structural long term stagnation makes Europe almost uninvestible in my view.

Save for certain key companies like LVMH, generally speaking I would stay away from Europe as a whole as the macro outlook is terrible.

What about Singapore?

Bridgewater doesn’t talk about Singapore specifically – but there was this reference to “Neutral” countries:

“In our studies, it tends to be the case that neutral countries do relatively well through conflicts, while the losers do the worst for obvious reasons and the winners tend to be a mixed bag, given the cost of waging even winning conflicts.”

So far at least, Singapore has done very well for herself by standing as a neutral player in between the two giants.

We continue to attract China capital and talent.

While remaining on the good books of the US, and receptive to capital / goods flow between the two.

Whether Singapore can keep up this precarious position as a “Neutral” player in an increasingly polarised world is the million dollar question, and much will come down to the ability of our leader.

But personally I think Singapore is well positioned, and I am mid – long term bullish on the outlook for Singapore.

Where does value lie today?

To sum it up – I view the key strategic markets for a Singapore investor to be:

- US

- China

- Singapore

US for the simple reason that you cannot afford not to be invested in the US today, but you have to go in with your eyes open and recognize that prices are not cheap.

China is one that can be skipped if you are not comfortable. But I continue to think China assets are pricing in a very gloomy outcome – which means upside if the outcome is less gloomy than what is priced in.

And Singapore because there are reasons to be structurally bullish Singapore, and as a Singapore investor you do need some investments at home as well.

This article has gotten very long, so I will break it up into 2 parts and discuss individual asset classes in Part II of the article (on FH Premium).

My full list of stocks / REITs I am keen to add is also shared on FH Premium.

This is an FH Premium post written in Jan 2025, that I am making available to all readers.

If you find content like this helpful, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly)

I have no dummfone, never touched fakebock, I have no idea what instagram or threads is, telegram either.

Seems: “The Matrix has you!” And isn’t it a US Matrix?

I wonder, if people who live a life of convenience loose touch with real stuff.

Or is it me? “I sometimes feel I am in a parallel universe. Maybe I am.” – Albert Edwards (Soc Gen)

The US stole the Russian ADR of all investors worldwide and you say she is top on your list? She vaxxed the world via operation Warp Speed. She is overindebted: 31 trillion in gov debt and 120 trillion in unfunded liabilities. US credit cards are maxxed out and people sold their eagles to survive. Others live on streets, sleep in cars even if they earn well. She wants to kick millions of Palestinians out and ignores the sins of Israel. She treatens little Denmark with war as she wants to take over Greenland. Then she puts taxes on her people via tariffs “on others”.

And you want to give her your money? By all means: Do it!

I agree with EUlandia. Where I am from and ran away when she forced us to injections. I would not feed her either.

So Singapore makes my no. one on your list because of relative freedom and security. She does not steal! This alone makes her such an exception these days.

Yes, there is a lot of stupidity like everywhere, but even I could write to MAS and the wonder happened. What would have happened to me with a yearslong dormant account in US? Same what happened to Russian ADR holders worldwide?

I live diet in February and I might be a little harsh without sugar and noodles, but (my) reality is the west has given up values. Values I hold dearly!

So do I invest in Sg REITS or banks? No, but I might asap my Sg bank sends me the TAN generator I am waiting for since 2011. Six letters brought no reaction. So foreign banks in Singapore are the way I use and over them I can steer my wealth.

Jim Grant’s famous “return of investment not return on investment” reigns my mind.

Mr Trump says, the US does not need anyone. I understand that.

Wow that’s a really interesting comment. Appreciate the sharing very much!

With the new president at helm, the only safe market we have right now is US and PRC. Sadly SG and Europe is as vulnerable as Canada or Panama whom he can shootdown overnight for something that goes against his will, thankfully that pain will last only another 3.5 years until he steps down. So my strategy is focusing on value and dividend play on the top 2 markets while working on long term’s covered call to increase the return.

Fair enough – appreciate the sharing!