I received this great question from an FH Premium subscriber, looking to invest to generate $150,000 a year in passive dividend income.

(some details have been amended to preserve privacy):

Dear FH,

I am seeking your insights on retirement planning. I’m a 59-year-old Singapore PR with $5 million in cash and stocks.

My goal is to retire in 5 years and maintain a comfortable lifestyle with an annual income of $150,000 from my investments.

The income will be supplemented by my wife’s and my CPF payouts.

My investment outlook centers on the following key points:

- I’m looking for a mostly passive investment approach, but I’d like to retain some flexibility to take advantage of market opportunities when they arise.

- I want to ensure the growth of my portfolio outpaces inflation.

- I want to avoid touching the principal to never outlive my resources, even if I reach 100 years of age

- I’d like to pass on as much as possible to my children and grandchildren.

- I’m keen on gaining some exposure to the US market due to its growth potential but am also mindful of foreign exchange risks.

I’d appreciate your guidance on the following:

- Asset Allocation: What would be a suitable asset allocation strategy for my situation, balancing growth, income, and risk mitigation while allowing for some tactical adjustments?

- Investment Vehicles: Which investment vehicles (e.g., index funds, ETFs) would you recommend for gaining exposure to both Singapore and US markets.

Thank you for your time and consideration.

How much risk do you need to take? To get $150k a year on $5 million of assets?

The first thing that struck me.

Is that if you have $5 million in investible assets.

And you need to achieve an annual dividend / return of $150,000 a year.

That’s a dividend / return of a mere 3% a year.

And if you know anything about portfolio retirement theories, you’ll know that most financial advisors advocate a 4% safe withdrawal rate:

The safe withdrawal rate helps you determine a minimum amount to withdraw in retirement to cover your basic expenses, such as rent, utilities, and food. As a rule of thumb, many retirees use 4% as their safe withdrawal rate—the so-called 4% rule

In other words, 4% is viewed as a fairly safe withdrawal rate to rely on in retirement.

And this investor only needs 3%.

Big picture wise, this suggests that you can afford to run a relatively low risk portfolio, and still be able to achieve your goals.

Asset Allocation I would use… if this were me?

Now for obvious reasons I don’t know anything about the investor beyond what was shared above.

In particular what his real estate ownership is like (does he own or rent), how many children does he have, does he plan on living in Singapore in retirement or migrating etc.

So I’ll stay big picture here, and please note this should not be taken as investment advice.

But if this were me?

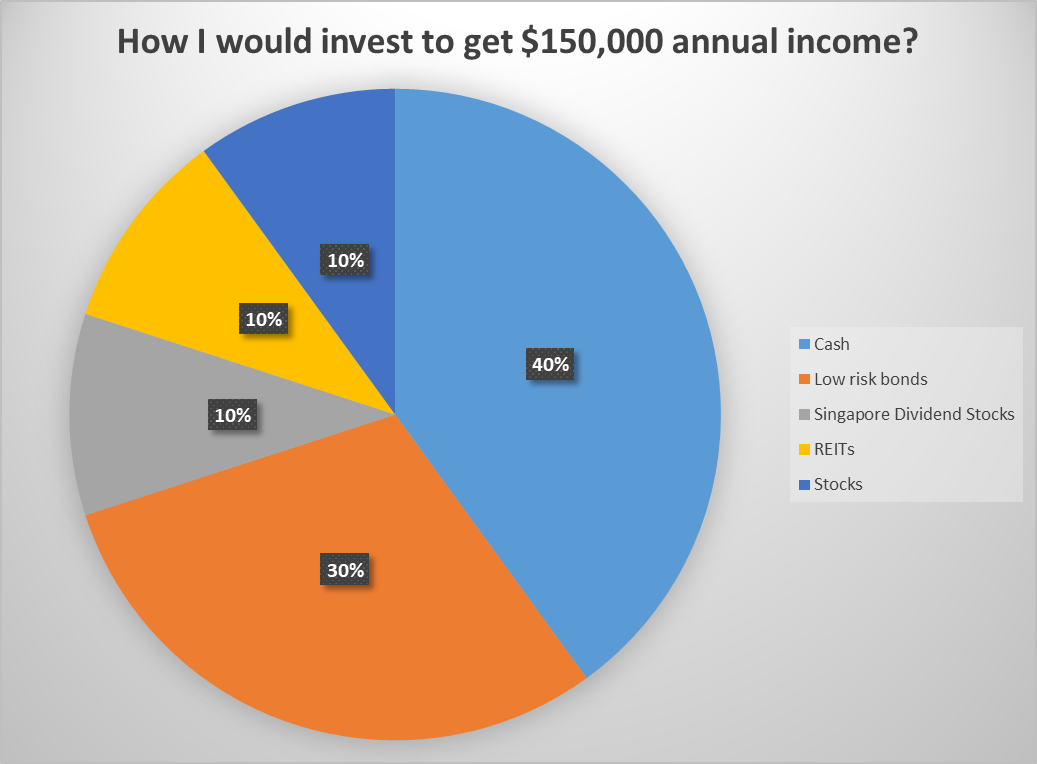

I think I might go with an asset allocation like the below:

| Asset Class | Amount | Yield / Investment Return | Dividend each year |

| Cash | 2,000,000.00 | 3.00% | 60,000.00 |

| Low risk bonds | 1,500,000.00 | 4.50% | 67,500.00 |

| Singapore Dividend Stocks | 500,000.00 | 5.50% | 27,500.00 |

| REITs | 500,000.00 | 5.00% | 25,000.00 |

| Stocks | 500,000.00 | 6.00% | 30,000.00 |

| Total | 5,000,000.00 | 4.20% | $210,000.00 |

Why so much cash/bonds?

Now of course you are going to ask – FH… why so conservative?

70% of the portfolio is in a mix of bonds and cash.

And I suppose my answer would be that hey this is my life.

If I have $5 million investible, and I can put 70% of that in a mix of low risk cash/bonds and still have $50,000 more than I need to get by.

Why take the risk?

Sure I can take on more risk and get $300,000 returns a year instead, but would that materially change my lifestyle?

Whereas if I take on more risk and something goes wrong, and say I suffer a 20% – 30% loss in the portfolio – now that could cause me a lot of undue stress in retirement.

Where are we in the business cycle? Is risk elevated?

Here’s what I wrote for FH Premium subscribers this week:

As shared, I think the Feds are slightly behind the curve on rate cuts here (especially due to monetary policy lag time), so once they start cutting they will have to cut fast and furious, so I generally agree with what has been priced in by the market [Update: As you can see the Feds cut 50 bps this week, in line with my thesis].”

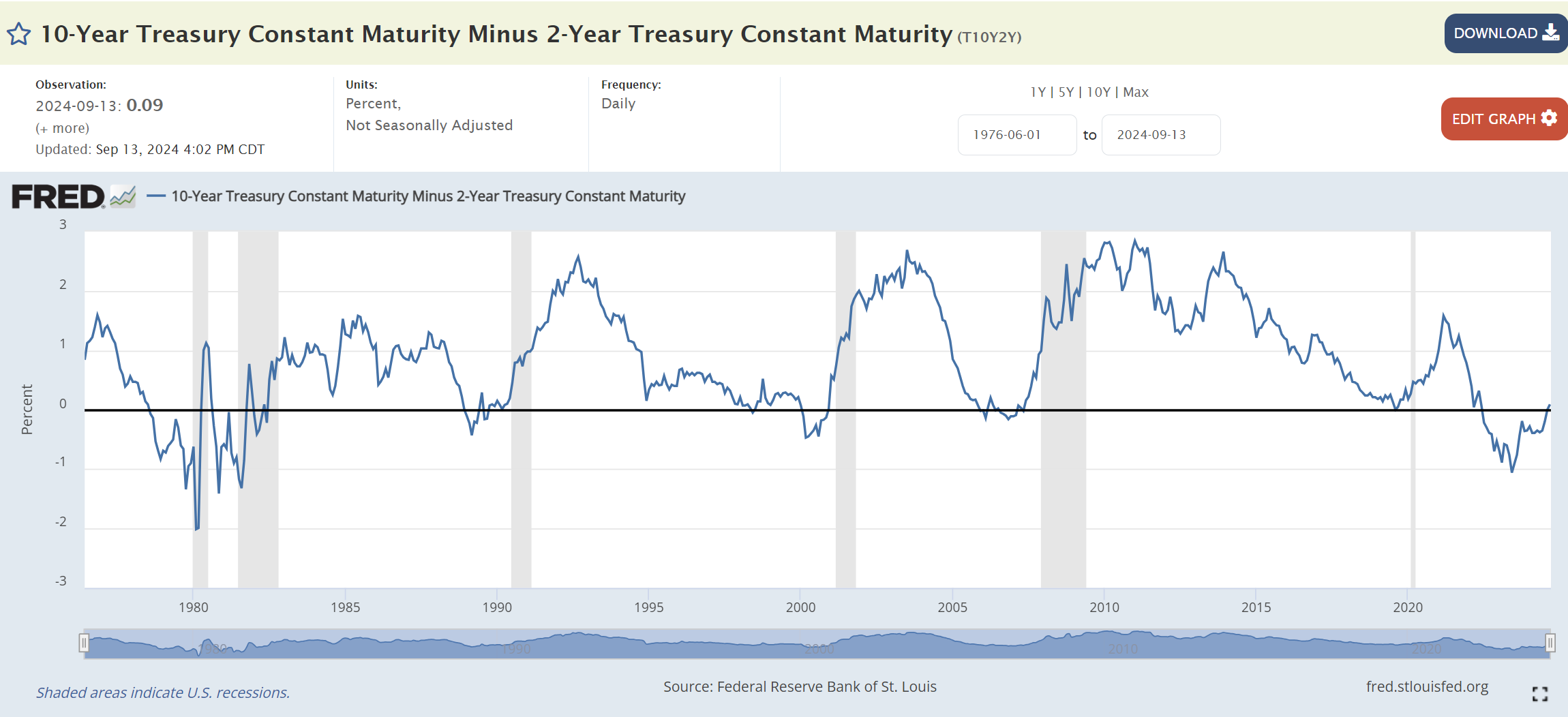

It’s worth noting that the 2s10s yield curve has recently uninverted, and this has happened before every recession in the past 40 years (and did not trigger in the 1995 soft landing).

Coupled with many other recession indicators like Sahm rule, it suggests elevated risk of US recession in the months ahead.

Of course, there are many reasons why pre-COVID indicators are no longer valid (it is possible that the structure of the economy has changed post-COVID), and only time will tell.

But big picture wise, there is no doubt that global economic growth is slowing.

The million dollar question now is whether Fed rate cuts + whoever wins the US election in Nov will be enough to reverse the slowdown in the US/global economy.”

There are no sure things in investing, and its possible most of the pre-COVID indicators are no longer accurate today.

But if I were a retiree in a situation like that, do I really need to take the risk?

I can sit on my $3.5 million in cash/bonds earning the yield.

And that buys a **** ton of tactical flexibility to take advantage of market opportunities.

What this investment portfolio does well in?

Coming back to the goals of the reader, I think this portfolio would achieve the following goals:

- I’m looking for a mostly passive investment approach, but I’d like to retain some flexibility to take advantage of market opportunities when they arise.

- I’m keen on gaining some exposure to the US market due to its growth potential but am also mindful of foreign exchange risks.

As shared above – when you’re running 70% or $3.5 million in cash / bonds, that’s a lot of flexibility right there depending on what happens next.

What’s the biggest risk with this investment portfolio?

Where the portfolio falls short, is on the following goals.

- I want to ensure the growth of my portfolio outpaces inflation.

- I’d like to pass on as much as possible to my children and grandchildren.

- I want to avoid touching the principal to never outlive my resources, even if I reach 100 years of age

In some ways the goals do conflict each other.

If you want growth, you do need to take on some risk.

And if you take on risk – well these are financial markets and there is always a risk you lose money.

So the question is how much risk are you prepared to take on.

But I do not deny that a portfolio with 70% in cash/bonds probably isn’t going to grow by a lot, and in some cases may fall short on these goals.

What if you want to focus more on growth?

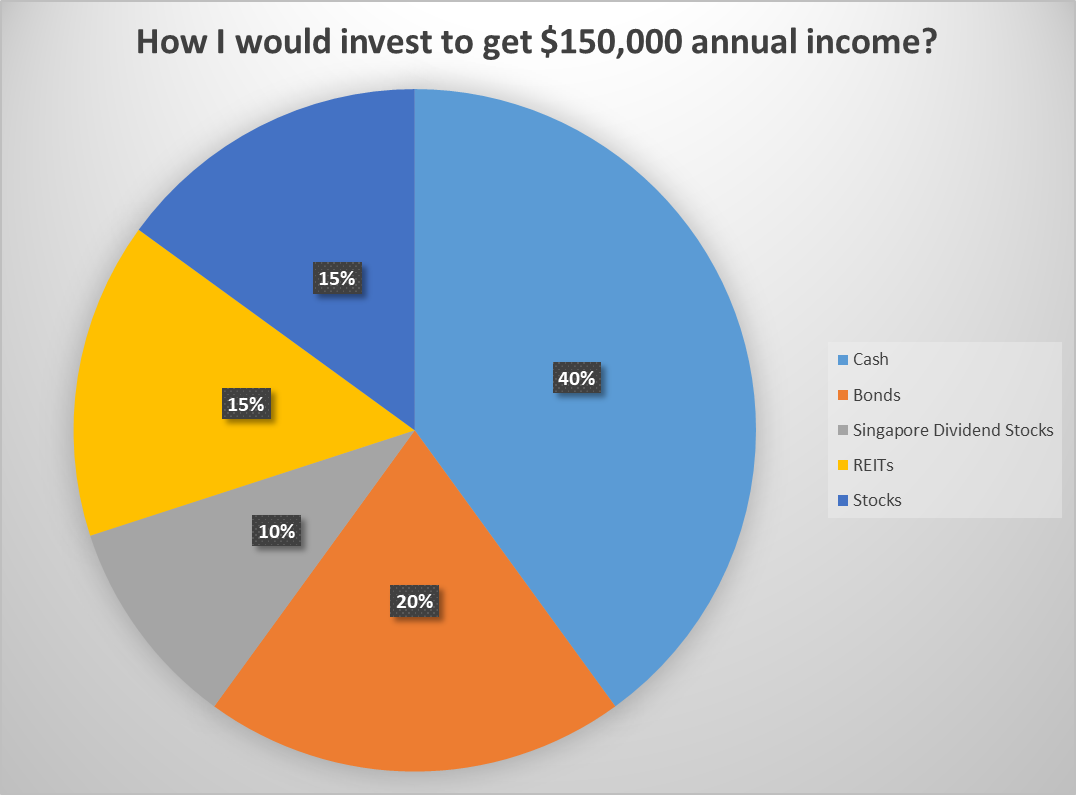

I suppose if you wanted to tilt the balance more towards growth, you could run something like the below.

| Asset Class | Amount | Yield / Investment Return | Dividend / return each year |

| Cash | 2,000,000.00 | 3.00% | 60,000.00 |

| Bonds | 1,000,000.00 | 4.50% | 45,000.00 |

| Singapore Dividend Stocks | 500,000.00 | 5.50% | 27,500.00 |

| REITs | 750,000.00 | 5.00% | 37,500.00 |

| Stocks | 750,000.00 | 6.00% | 45,000.00 |

| Total | 5,000,000.00 | 4.30% | 215,000.00 |

I would probably up the exposure to REITs and stocks slightly, to give more growth potential.

But frankly, this is a personal call on how much importance you place on each goal – capital growth vs capital preservation.

What I would add is that at this point in the business cycle, I probably want to dial back on risk slightly.

And if valuations come down or the macro turns favorable again, I would up the risk exposure.

What to consider buying for each segment of the portfolio?

Stocks

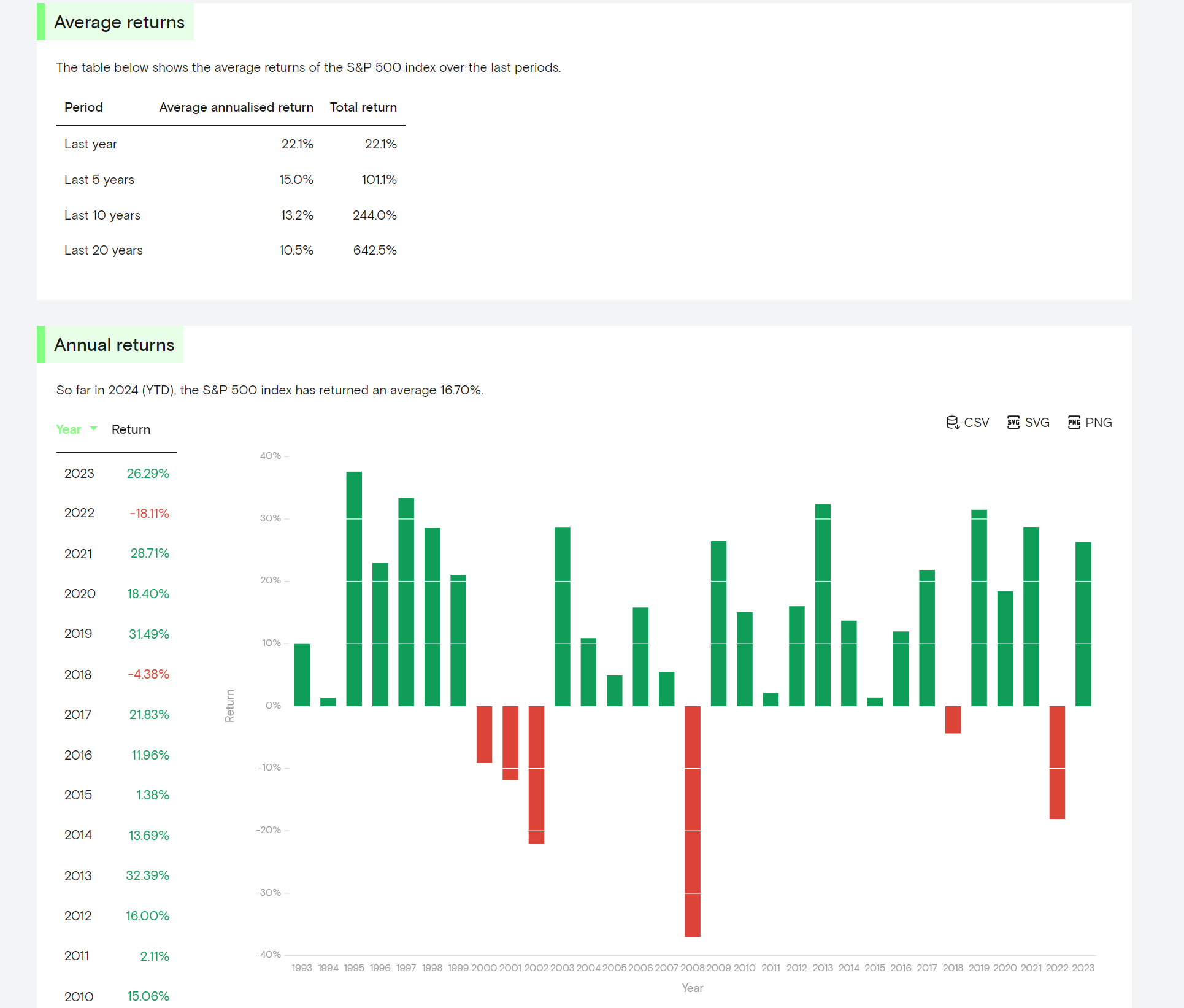

For stocks, I would say just go for a low cost S&P500 ETF.

As a Singapore investor, you want to use a LSE listed UCITS fund for more efficient withholding tax treatment.

iShares Core S&P 500 UCITS ETF USD (Acc) (LSE:CSPX) is one of those to consider.

20 year annualised return for the S&P500 is 10.8%, which is very strong.

That said – I know there’s a lot of criticism that US stocks are overvalued, the USD will depreciate, and that forward returns will not match the past 20 years.

Is FX a valid risk? Will the USD depreciate?

Over the past 20 years, the USD depreciated 24% against the SGD, which works out to 1% annualised loss each year.

So even after factoring in FX loss, you’re looking at 9%+ annualised return on the S&P500 the past 20 years.

Not too shabby.

But look closer at the chart, and you’ll realised that a huge chunk of this depreciation took place in 2002 to 2011.

During this period, the USD depreciated from 1.80 to 1.20, a whopping 33% move in FX in the span of less than 10 years.

Can the same repeat today?

I mean if you look at how the US government is spending today, the inevitable conclusion is that they need to do a lot of “money printing” going forward.

So I would not rule further USD depreciation.

Why the S&P500?

At the end of the day though – the US economy is probably the most dynamic and competitive market in the world.

Because of that, US stocks offer very strong potential returns, but at the cost of very high volatility, with FX risk.

I would say as a Singapore investor, you want some exposure, but you want to size it well based on your risk appetite.

REITs

I’ve been getting a lot of questions on REITs, and I wrote a long post for FH Premium subscribers this week (see a snippet of it here).

Simple answer is that if the Feds are going to cut as aggressively as what is priced in (and I think there is a chance they will given the weakening US labour market), there could be further upside for REITs.

I myself hold 30% of my portfolio in REITs mainly via stock picking, although I would not suggest that for a low risk passive portfolio like the one we are discussing today.

For a passive approach, something simple like a REIT ETF like NikkoAM-StraitsTrading Asia ex Japan REIT ETF (CFA) or Lion Phillip S-REIT ETF (CLR) or Syfe REIT+ would work.

Singapore Dividend Stocks

If this were me, I would actually just buy the 3 local banks (DBS, UOB, OCBC) in equal split and be done with it – netting a 5-6% dividend yield.

But the reader did ask for a passive approach, and this sort of ventures into the realm of stock picking.

An alternative would be to just go for the SPDR STI ETF (SGX: ES3).

I know the STI is not very well loved, but I think if your goal is to get broad exposure to the Singapore stock market as a passive investor, the STI is a decent enough option.

52% of the index is the 3 local banks, 16% is real estate / REITs, and the rest is a mix of the large blue chip or GLCs.

Dividend yield is about 3-4% though, and a fair bit lower than if you just buy the 3 local banks in equal weight.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Bonds

With $1 – $1.5 million in cash, you can technically become a private banking client select individual bonds to purchase.

But given this is meant to be a low risk passive approach, that probably entails a tad too much work.

In which case I would say just use a broad diversified bond fund.

Examples include Endowus Income:

Or Syfe Income Plus:

Some readers have mentioned Nikko AM SGD Investment Grade Corporate Bond ETF, but personally I’m not a fan.

This ETF only yields about 3.5% today, and the trading liquidity is abysmal.

I would say the bond funds are a better choice.

In fact if you’re so inclined, you can even pick individual bond funds on Endowus based on your maturity / geographical exposure / risk appetite.

A deep dive into bond funds is beyond the scope of this article, but let me know if you guys are keen and I can do a deeper dive.

Cash

For cash, you can refer to tomorrow’s article on the best place to park cash today.

I would say you want to get creative and use a mix of all the options available to you:

- Singapore Savings Bonds (don’t forget each family member has a $200,000 quota)

- T-Bills

- Fixed Deposit

- Money Market Funds

I assumed a 3.0% yield on cash which I think is still feasible today.

However given rapidly falling interest rates, it is possible that the yield on cash may drop below 3.0% going forward.

I did a simple sensitivity test, and you can see that even if the yield on cash falls to 2.0%, the overall portfolio still generates in excess of the $150,000 requirement.

Although the buffer is much smaller in that case, so it may require some rejigging around the portfolio (especially if there is a dividend cut / stock market sell off).

| Asset Class | Amount | Yield / Investment Return | Dividend / return each year |

| Cash | 2,500,000.00 | 2.00% | 50,000.00 |

| Bonds | 1,000,000.00 | 4.50% | 45,000.00 |

| Singapore Dividend Stocks | 500,000.00 | 5.50% | 27,500.00 |

| REITs | 500,000.00 | 5.00% | 25,000.00 |

| Stocks | 500,000.00 | 6.00% | 30,000.00 |

| Total | 5,000,000.00 | 3.55% | 177,500.00 |

Closing Thoughts – Do you want to get rich, or do you want to not be poor?

Now I hope the above has given you guys a rough idea of my thought process, and the instruments I would consider using in such a scenario.

But really the key theme for me is this:

Do you want to get rich, or do you want to not be poor?

To me, that’s really the most fundamental question you need to ask yourself as an investor.

If you’re 28 years old and you have $50,000 in investible assets, hey I would say you want to dial up the risk – because you are investing to get rich.

If you’re 59 years old and you have $5 million in investible assets, and you only need $150,000 a year to be happy, then hey maybe you have already achieved your financial goals, and you don’t need to risk losing everything to grow the pot further.

But fundamentally, this is a question that only you can answer.

I know many who would not be able to survive on $150,000 a year in retirement, so if you’re one of those maybe you want to continue investing aggressively.

While other may want to pass on as much as they can to their children, in which case you may want to increase risk exposure to grow the pot.

Frankly, there’s no right or wrong here.

I encourage investors to do some soul searching over the weekend, and answer this question for yourself.

Do you want to get rich, or do you want to not be poor?

This post is written on 27 Sep 2024 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Saxo Brokers – Trade the 100 most popular US stocks commission-free

Saxo is running a promotion where new account holders can trade the Top 100 US stocks commission free (more details).

Special account opening bonus for FH Readers:

- Sign up via the link: Saxo Brokers

Chocolate Finance- pays 4.2% yield on first $20,000

Chocolate finance pays 4.2% on the first $20,000, withdrawable instantly.

The funds are invested in a selection of bond and money market funds, and Chocolate Finance will top up any returns if they are lower than 4.2%.

I wrote a detailed review on Chocolate Finance (note not SDIC insured).

- FH invite link below:

https://share.chocolate.app/nxW9/ep4q7wxp

Stock Café – track your portfolio performance (including dividends)

I use StocksCafe to track my portfolio and dividend stocks (full review).

- FH x StocksCafe Referral Code:

https://stocks.cafe/user/tosignup?referral_code=financialhorse

Please do a deep dive for Bond Funds. Always talk about Reits and Banks is quite stale.

Haha ok!

Second that! Do a primer on bond funds for retail investors! Is it better to ETF or go with active managed? If active, which funds and which platform? Which geographies and high yield or investment grade? Any tax implications we need to take note of?

Ok! Will do!

The issue here is how to invest the bulk of the cash & bonds, and have it earn the stated returns with little to no risk. If a chunk of my funds are in CPF OA (eg $1million earning 2.5%), would you consider that as “bonds”? What would you recommend?

Ok I’ll do a deeper dive on this as part of the bonds article. CPF-OA at 2.5% I would classify more as cash rather than bonds, because of the lower interest and easier liquidity (in that it can be withdrawn for housing for eg.).