As you guys know, I spend a lot of time thinking about asset allocation.

So I recently decided to cross check my thinking against AI, and see what inputs AI can bring to the picture.

So I asked AI to come up with the ideal asset allocation for a 35 year old Singapore investor (we discuss other age groups below don’t worry), with the following profile:

- Looking to invest to grow wealth aggressively

- However constraints as a Singapore investor are:

- Has to have at least 30% allocated to Singapore real estate (given high Singapore real estate prices)

- Has to have at least 10% in CPF, given mandatory CPF requirements on CPF-SA and Medisave

Unlock Your Financial Edge with FH Premium

Enjoy this exclusive FH Premium analysis—now free for all readers! But why stop here?

By subscribing to FH Premium, you’ll gain:

- Weekly Macro Deep-Dives

Understand where the global economy is headed—and why it matters for your wallet. - Regular Buy/Sell updates from my personal portfolio

See exactly what I’m adding to (or trimming from) my portfolio and act before the crowd. - Comprehensive Watchlists

Full stock & REIT watchlists, updated regularly with target prices, entry zones, and risk considerations. - My Personal Portfolio

Transparent tracking of every position I hold—and why—so you learn the “what, why, and how” of smart investing.

Join hundreds of savvy readers who’ve turned FH Premium insights into real returns. Ready to level up your investing?

Subscribe to FH Premium today and never miss a market-moving idea.

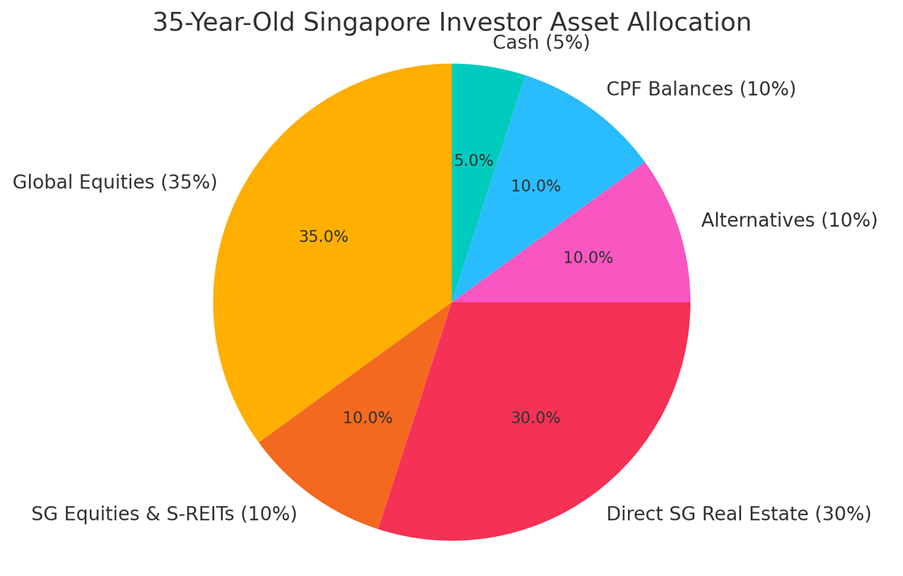

What is the Ideal Asset Allocation for this 35 year old investor (according to AI)?

Here’s the answer:

“Executive answer (3-liner)

- 45 % equities (35 % global, 10 % SG equities/REITs), 30 % direct SG real estate, 10 % alternatives, 10 % CPF balances, 5 % cash.

- Property sleeve captures continued but moderating price gains (URA Q1-2025 PPI +0.8 % q-o-q) while CPF earns a floor 2.5 – 4 % risk-free.

- Target long-run CAGR ≈ 7 % with ~-30 % drawdowns; review annually or if any sleeve drifts > ±5 ppt.

1. Updated strategic asset-allocation

| Sleeve | Target | Typical vehicles | Role / notes |

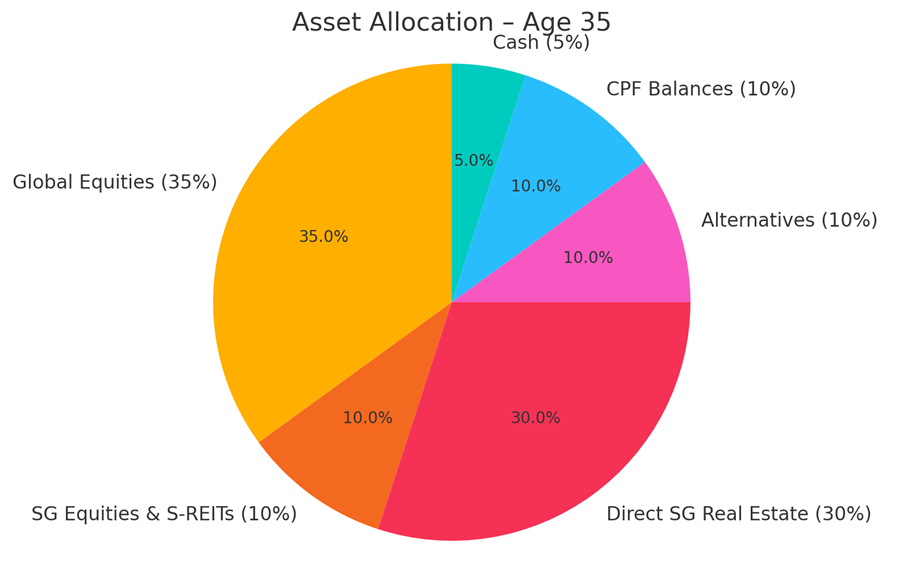

| Global equities | 35 % | CSPX (S&P 500 UCITS), IWDA (MSCI World), EIMI (EM) | Growth driver, FX diversification |

| SG equities & S-REITs | 10 % | ES3 (STI ETF), Lion-Phillip S-REIT ETF | Home-bias income, liquid proxy for SG economy |

| Direct SG real estate | 30 % | Primary residence equity, investment condo, private syndicates | Leverage rising land scarcity; PPI still +3.3 % y-o-y despite cooling |

| Alternatives | 10 % | Global commodity ETF (3069), PE/VC feeder funds, spot-Bitcoin ETP | Uncorrelated alpha, inflation hedge |

| CPF (OA + SA) | 10 % (min) | CPF-OA 2.5 %; CPF-SA 4 % | Government-backed “bond proxy”, retirement lattice |

| Cash / M-market | 5 % | High-yield SGD accounts, Fullerton SGD Cash Fund | Liquidity for rebalancing & emergencies |

2. Why this tilt makes sense now

- Real estate 30 %: Singapore private-home prices are still inching up (+0.8 % q-o-q Q1-2025) even after seven rounds of ABSD tweaks; keeping a third of net worth here recognises structural land scarcity and rental support from immigration-driven demand.

- CPF 10 % floor: OA/SA’s 2.5 – 4 % floor beats SGS 10-yr yield (~2.7 %); balances compound tax-free and can double as mortgage offset or T-Bill substitute.

- Equities trimmed to 45 %: Still majority growth engine but avoids over-risking once property leverage is counted.

- Alternatives kept at 10 %: Provides optionality to capture AI infrastructure, private credit and commodities up-cycles without over-diversifying.

3. Implementation checklist (bullet-style)

- Real-estate sleeve

- Cap total property exposure (market value minus outstanding loans) at ≤ 150 % of annual gross income to avoid over-leverage.

- If already own a home, treat its equity as part of the 30 %; any new buy should clear 3 % net rental yield stress test.

- Funding & leverage

- Fix mortgage rate if 3-yr packages < 2.6 % (current HDB-linked rate).

- Redirect spare CPF-OA cash to partially pre-pay loans > 3 % effective cost.

- Equity sleeve execution

- Weight CSPX:IWDA:EIMI at 60:25:15; add ES3 and Lion-Phillip S-REIT quarterly with DCA.

- Defensive & CPF

- Maintain S$15-20 k in high-yield cash for six months’ expenses.

- Keep SA untouched for 4 % compounding; shift excess OA > S$20 k into 6-m T-Bills only when cut-off > 3 %.

- Rebalancing rule: quarterly check; buy laggards when any sleeve deviates > ±5 ppt.

4. Key watch-points going forward

- URA PPI trend – a sustained negative print (> -2 % q-o-q) would prompt trimming property to 20 %.

- CPF policy tweaks – monitor annual Budget for interest-rate floor changes.

- Fed cycle & SGD NEER – sharp USD strength may cheapen foreign-equity entry points; hedge when USD/SGD > 1.38.

- Liquidity squeeze – if 3-m SIBOR > CPF-OA 2.5 %, accelerate mortgage repayment to lock risk-free spread.

(Not personalised financial advice; stress-test against your own cash-flow and tax situation before executing.)”

My Thoughts? Ideal Asset Allocation for this 35 year old investor?

And you know what?

I actually agree with about 80% of what AI came up with above.

The nuance is that you need to adjust the real estate / CPF component for each investor depending on financial circumstances.

For example those who are not married may be living with parents and have (or not have) investment property.

Those who are married with a family home and investment property may see real estate form a bigger portion of the net worth.

Those who choose to top up CPF-SA, or have not touched CPF-OA to buy property, may see CPF form a bigger portion of net worth.

And so on.

So you do need to apply some nuance to adjust the asset allocations for yourself.

But by and large I would say that I agree with the thought process:

- Think about how much you need in real estate and CPF – this forms the bedrock

- For the remainder, set aside what you need for emergency expenses / spending requirements in a mix of cash and bonds

- What is left after – the bulk should be invested in global equities and Singapore stocks/REITs (I would overweight the former assuming decent risk appetite – for higher potential returns)

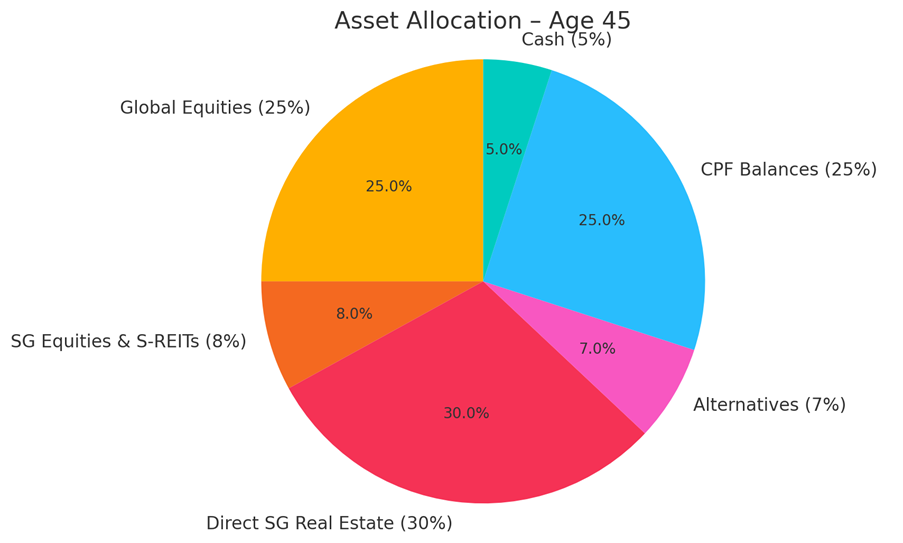

What about for an older 45 year old investor? Or a Younger 25 year old investor?

Now what if the investor is older (say 45), or younger (say 25).

These are the revised charts that AI gave me:

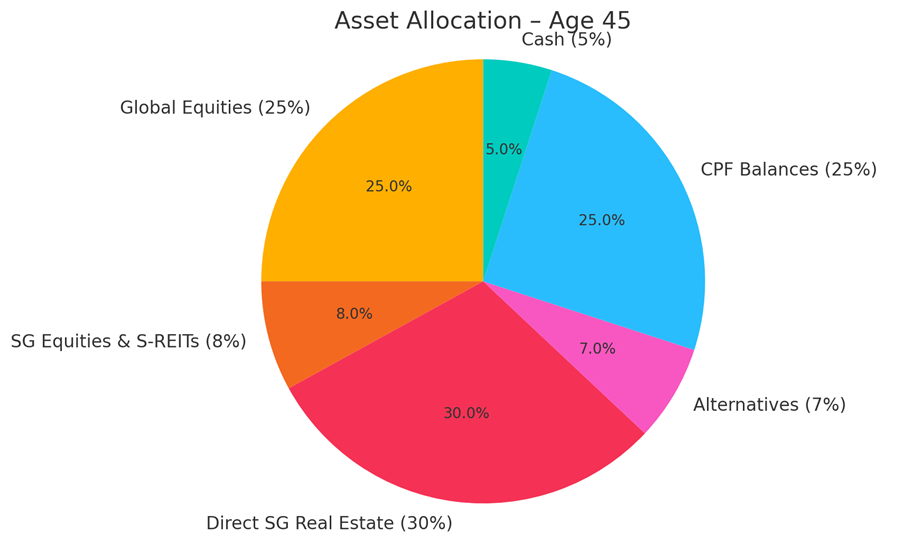

Ideal asset allocation for an older 45 year old investor?

The original asset allocation for a 35 year old for reference:

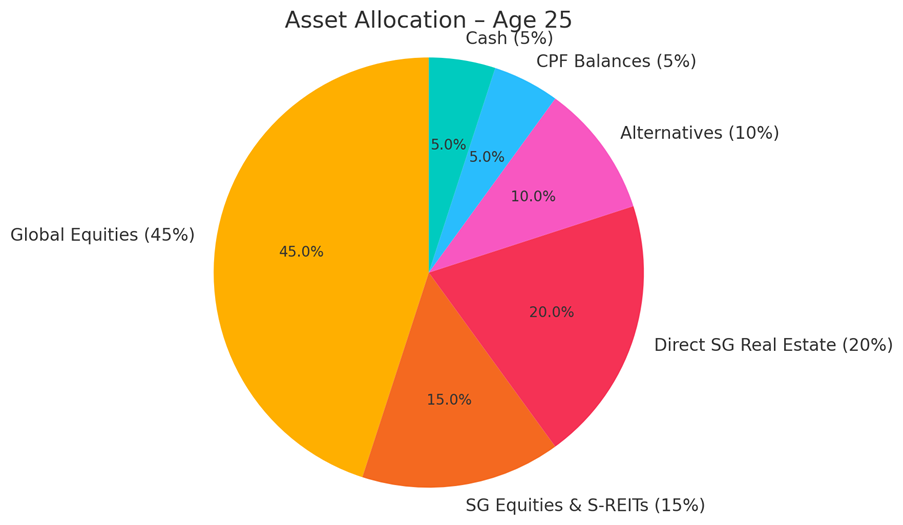

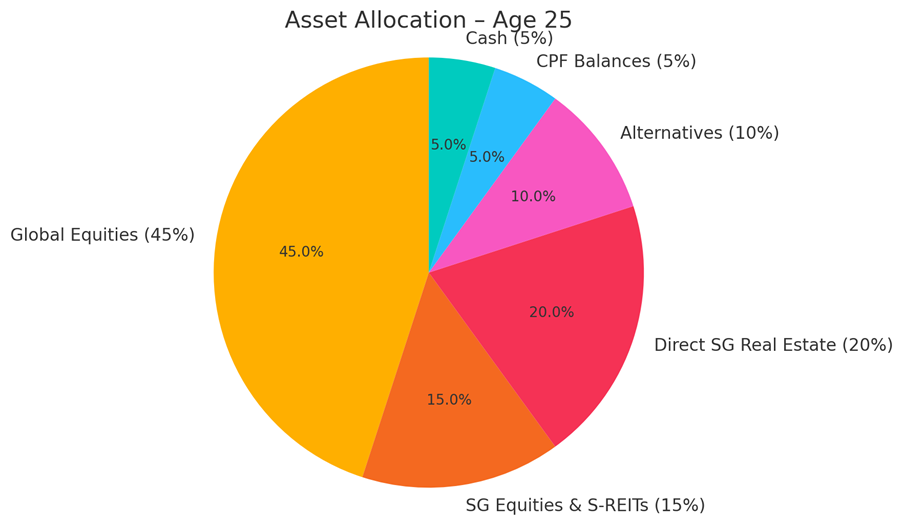

Ideal asset allocation for a younger 25 year old investor?

And the full thought process:

“Executive answer (3 – liner)

- Age 25: stay aggressive – equities 60 %, real estate 20 %, CPF only 5 %.

- Age 35 (baseline): shift to our prior mix – equities 45 %, real estate 30 %, CPF 10 %.

- Age 45: de-risk – CPF/“bond” 25 %, equities down to 33 %, real estate still 30 %.

1 . Side-by-side allocation comparison

| Asset class | Age 25 | Age 35 | Age 45 |

| Global equities | 45 % | 35 % | 25 % |

| SG equities & S-REITs | 15 % | 10 % | 8 % |

| Direct SG real estate | 20 % | 30 % | 30 % |

| Alternatives | 10 % | 10 % | 7 % |

| CPF balances (OA + SA) | 5 % | 10 % | 25 % |

| Cash / MMF | 5 % | 5 % | 5 % |

(CPF OA floor 2.5 %; SA 4 %. Q1-2025 URA PPI +0.6 % q-o-q)

2 . Thought process

- Human-capital glide-path: Younger investors have larger “bond-like” future earnings, so they can load up on equities (60 % at 25). By 45, human-capital duration shortens and market setbacks become harder to recover from, so equities fall to one-third.

- Property anchor: Singapore housing still trends modestly higher on land scarcity (URA 1Q 2025 +0.6 % q-o-q), and leverage is sticky; keep 30 % once a primary residence or investment unit is established, but start lower (20 %) when 25 if capital isn’t yet deployed.

- CPF as sovereign bond: Guaranteed 2.5–4 % real-SGD return substitutes for the traditional bond sleeve. Balances snowball with age and provide a volatility sink; raise to 25 % by 45.

- Alternatives 7-10 %: A steady sleeve for commodities, PE/VC, or Bitcoin ETP gives inflation and diversification upside without swamping core beta.

- Liquidity 5 %: Enough dry powder for job loss or tactical buys across life stages.

3 . Practical glide-path actions

- Age 25 → 35:

- Dollar-cost average into CSPX / IWDA / EIMI; channel bonuses into a first property only when the mortgage stress-test < 35 % DSR.

- Keep CPF OA for housing or T-Bills only when auction cut-off > 3 %.

- Age 35 → 45:

- Start voluntary CPF SA top-ups (tax-deductible, 4 % floor) to accelerate the secure sleeve.

- Shift 2 ppts of equities to CPF each year if equity gains exceed 8 % CAGR.

- Fix mortgage rates when SORA < 2.6 % to lock CPF-OA vs loan spread.

- Rebalance discipline: Quarterly check; trim/boost any sleeve that drifts > ±5 ppt.”

My views? Ideal asset allocation?

Here, I thought AI did not do such a great job, both for the 45 and 25 year old.

Let’s discuss each separately.

Never miss a market beat—ride with Financial Horse wherever you go!

Get timely insights, sharp analyses, and real-time alerts by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox, plus early access to special reports and FH Premium previews

My thoughts – 45 year old asset allocation

The big problem I see is the 25% allocation to CPF.

Frankly – just not sure how realistic this is for a 45 year old.

Assuming much of this has been drawn down to pay the property mortgage, I would expect CPF to form a much lower portion of the net worth.

The only scenario where this seems to make sense is if the investor did large CPF-SA top-ups, and did not really draw down CPF-OA in a big way.

But given that CPF-OA pays 2.5% today which is not all that attractive, I’m not sure how realistic this is (but of course I would love to hear your thoughts).

Personally if you ask me, I continue to think that the greatest threat for investors this decade is inflation.

As a 45 year old with 20 years to go till retirement (okay I know that may not be realistic in today’s more uncertain job market), and at least 30 – 40 years of spending left.

I would probably reduce the CPF / Bond allocation, and allocate that to either global equities or SG equities / REITs – to hedge inflation.

My thoughts – 25 year old asset allocation

Generally I think the thinking is right in that a younger investor should see a much bigger allocation to stocks.

That part is right.

What probably doesn’t make sense is the 20% real estate allocation.

As a 25 year old, unless you BTO-ed early, or have top up from parents to buy a private property, chances are the 25 year old would not own any Singapore property.

In which case the rest should go into bonds/cash (if saving up to buy property), or equities (if no immediate plans to buy property).

How to invest the Global Equities and Singapore Equities/REITs portion?

The next big question of course, is how to invest the “Global Equities” and the “Singapore Equities/REITs” portion.

But this article has gotten quite long with a lot to digest.

So I will cover this in Part II on FH Premium.

Unlock Your Financial Edge with FH Premium

Enjoy this exclusive FH Premium analysis—now free for all readers! But why stop here?

By subscribing to FH Premium, you’ll gain:

- Weekly Macro Deep-Dives

Understand where the global economy is headed—and why it matters for your wallet. - Regular Buy/Sell updates from my personal portfolio

See exactly what I’m adding to (or trimming from) my portfolio and act before the crowd. - Comprehensive Watchlists

Full stock & REIT watchlists, updated regularly with target prices, entry zones, and risk considerations. - My Personal Portfolio

Transparent tracking of every position I hold—and why—so you learn the “what, why, and how” of smart investing.

Join hundreds of savvy readers who’ve turned FH Premium insights into real returns. Ready to level up your investing?

Subscribe to FH Premium today and never miss a market-moving idea.

I am 55 yo. I am 35% in global and Singapore equities combined. The rest are in fixed income, cpf and cash. I did not include property. I thought it is pretty conservative until I saw your allocation for a 45 yo. Can you do a 55 yo profile?

Just curious, how would the numbers look like if you include property? Because I included 30% property for the 45yo allocation.

I would like to know how to have a similar allocation for retirees. They have lots of cash in their bank accounts but are not well informed about how to invest (see the high percentage of seniors at investment seminars?) Please help them

OK – let me think about this and see if I can write something.

I am 62 and have this unproven concept of investing like a younger person on the assumption that my son can take over my portfolio when I am gone. In essence, it is utilizing the time horizon of two generations to invest. I know the biggest factor is the assumption that my son has what it take to take over.

Very interesting viewpoint! And spot on on the assumption haha.