I’ve been following the recent Hyflux saga with much interest. The fall from grace of one of Singapore’s homegrown companies, and the entire restructuring process, has been incredibly informative because it will likely serve as a template for future restructurings in Singapore where retail investors are involved.

I know that many readers here know at least someone who has personally invested their hard earned money in Hyflux, so I do hope that this could be helpful for fellow investors out there to decide on how they should vote.

Of course, this article shouldn’t be taken as investment or legal advice, so please note the disclaimer below:

The information contained in this article has not been independently verified. No representation or warranty expressed or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained in this article. Neither Financial Horse or any of its affiliates, advisers or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising, whether directly or indirectly, from any use, reliance or distribution of this article or its contents or otherwise arising in connection with this presentation. If you are in doubt as to the action you should take, please contact your financial advisor, stock broker, or legal advisor.

Better than nothing, but how much better?

In the original restructuring plan that I wrote about previously, junior creditors (ie. the retail investors who hold the perpetuals or preference shares) stood to receive about 10.7 cents on the dollar, of which 3 cents was cash, and 7.6 cents was shares. By contrast, senior creditors (banks and MTN bond holders) stood to gain anywhere from 24.5 cents to 38 cents on the dollar recovery.

Of course, this difference was way too large, and after retail investors kicked up a huge fuss, senior creditors eventually gave in. From the Straits Times (emphasis mine):

The change comes after unhappy perp and pref holders, represented by the Securities Investors Association (Singapore) or Sias, complained that they are not agreeable to the “paltry” recovery rate of 10.7 per cent on their original investment that Hyflux needs them to accept in order to return to solvency.

In comparison, Hyflux’s senior unsecured creditors, namely medium-term noteholders, unsecured banks and contingent claimants, are promised a minimum recovery rate of 24.5 per cent under the same scheme.

This second group gets to ride more upside because if none of the contingent claims are crystallised, 80 per cent of their proportionate compensation (which will be held in escrow) would have been distributed to noteholders and banks. The remaining 20 per cent would have been distributed to the managers of the projects for which the contingent claims were extinguished as “management payouts”, according to Hyflux’s Feb 15 court affidavit.

…

The difference now is that the management payout will be reduced from 20 per cent to 10 per cent of the cash allocated to any contingent claims that are extinguished. Hyflux confirmed that no member of the present board or senior management will receive any part of the contingent claim management payouts.

“All of these amounts will only be distributed to the project staff responsible for the extinguishment of the contingent claims,” Hyflux said. This is to incentivise project managers to complete projects on time, so that more claims will not be called.

Perp and pref holders will also receive a pro rata share of the remaining 90 per cent of the cash (but not equity) allocated to any contingent claims that are extinguished.

Hyflux said: “This means that when contingent claims under the scheme extinguish over the next two years, 90 per cent (up from 80 per cent) of the cash allocated to those extinguished contingent claims will be distributed among both the (perp and pref holders and senior unsecured creditors), rather than just being distributed among the (senior unsecured creditors).”

To break it down very simply, a portion of cash and Hyflux shares are set aside to repay contingent claims from creditors. These contingent claims are things like rental guarantees that are contingent on an event happening in future (eg. Hyflux failing to pay rent), so it’s impossible to know for certain how many would crystallise. If the contingent claims do not crystallise, whatever had been set aside would be used for distribution to creditors. Let’s call this the “contingent pot”.

Under the previous restructuring, 20% of the contingent pot would be used to pay Hyflux employees working on the restructuring, and the remaining 80% would be used to repay senior creditors. Junior creditors get nothing from this pot.

Under the new restructuring, 10% of the contingent pot would be used to pay Hyflux employees, and the remaining 90% would be used to repay senior and junior creditors on a pro rata basis. However, only the cash portion of the contingent pot will be split with junior creditors, and not the equity portion.

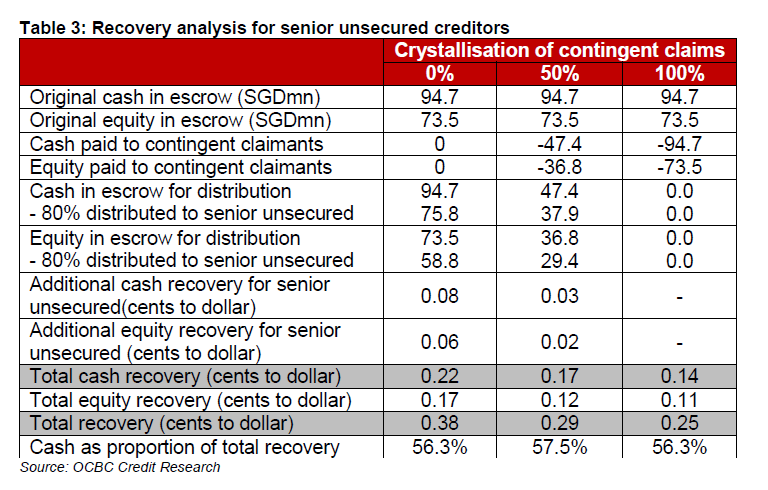

Let’s take a look at what this would mean. OCBC Credit Research kindly did the sums for the original restructuring, as set out below.

I ran the sums for the new restructuring (Note: Figures above have not been independently verified):

| 0% | 50% | 100% | |

| Senior Creditors (recovery – cents to dollar) | 18.5 cents cash

17 cents equity Total: 35.5 cents |

16.3 cents cash,

12 cents equity Total: 28.3 cents |

14 cents cash

11 cents equity Total: 25 cents |

| Junior Creditors (recovery – cents to dollar) | 7.51 cents cash

7.6 cents equity Total: 15.11 cents |

5.26 cents cash

7.6 cents equity Total: 12.86 cents |

3 cents cash

7.6 cents equity Total: 10.6 cents |

What this means, is that under the new restructuring plan, if none of the contingent claims crystallise, retail investors will get back 7.51 cents on the dollar in cash, and 7.6 cents on the dollar in shares. So for every S$10,000, they get back S$751 cash, and S$760 dollars worth of Hyflux shares. Of course, the actual value of the Hyflux shares is a big question mark, and we’ll touch on this later.

Assuming that 50% of the contingent claims crystallise, retail investors get back 5.26 cents on the dollar in cash, 7.6 cents on the dollar in shares.

It’s definitely better than the original restructuing, but the most obvious question to me, is why is it that only the cash portion of the contingent pot is split, and not the equity portion?

For discussion’s sake, I also ran the numbers assuming that the equity portion of the contingent pot is split equally with junior creditors:

| 0% | 50% | 100% | |

| Senior Creditors (recovery – cents to dollar) | 18.5 cents cash

14.5 cents equity Total: 33 cents |

16.3 cents cash,

11.75 cents equity Total: 28.05 cents |

14 cents cash

11 cents equity Total: 25 cents |

| Junior Creditors (recovery – cents to dollar) | 7.51 cents cash

11.1 cents equity Total: 18.61 cents |

5.26 cents cash

9.35 cents equity Total: 14.61 cents |

3 cents cash

7.6 cents equity Total: 10.6 cents |

The way I see it, this would lead to a far more palatable outcome for both junior creditors for 2 reasons:

Perception – The distinction between the cash and equity portion of the contingent pot is fairly arbitrary. I couldn’t think of any good reason why only the cash portion was shared with junior creditors. Sure, senior creditors may argue that the Hyflux shares are likely to be worth nothing post restructuring, but if that’s the case, why not just share it with the junior creditors, and increase the likelihood of the Scheme of Arrangement being approved? This one puzzled me.

Closes the gap between the senior and junior creditors – Under the original restructuring, in a best case scenario (0% crystallisation of contingent claims), senior creditors would get 38 cents on the dollar, while junior creditors get 10.7 cents. The different was just too stark. Under the revised proposal, senior creditors will get 35.5 cents on the dollar in a best case scenario, versus 15.11 for retail investors. If the equity portion of the contingent pot is split, that changes to 33 cents on the dollar for senior creditors, 18.61 cents on the dollar for junior creditors.

I must admit that I don’t have all the facts available to me here, but at first glance, I would think that the last outcome would be the fairest to all creditors. The senior creditors still get more than junior creditors, reflecting their higher priority in an insolvency, but at the same time retail investors are not hung out to dry, because a potential recovery of up to 18.61 cents on the dollar is better than nothing.

How likely are the contingent claims to crystallise?

OCBC Credit Research had an amazing bit of analysis on this:

Further upside potential from contingent claims if they do not crystallise

Background: The recovery amounts for the contingent claims (which we assumed to be SGD682mn) would be set aside in an Escrow Account. Such amounts would only be distributed to the contingent claimants when contingent claims get crystallised before the claim expiry date (2 years of restructuring effective date). Contingent claims are not existing claims and would only materialise upon some uncertain future event. As a recap, SMI’s investment is also conditional upon the full and final settlement of continent claims and in our view, setting aside monies and equity stake upfront caters for the possibility of a future unknown claim which reduces SMI’s investment risk in HYF.

Not all contingent claims are likely to crystallise: Based on the currently available disclosure, contingent claims include those relating to TuasOne, legal disputes, corporate guarantees, bankers guarantees, performance bonds and those in relation to two rental agreements with landlords. While some of these contingent claims could be crystallised, we think there is a good chance for a significant amount of contingent claims not to crystallise eventually (eg: rental related) post-restructuring, should the company emerge as a going concern post-restructuring.

In other words, OCBC seems quite optimistic on recovery from this contingent pot!

Really bad (or good) timing by PUB

Depending on how you see it, PUB also suddenly became a major player in the restructuring last week, for better or worse. From Channel News Asia:

With just about one month to go before a crucial vote on its restructuring plan, embattled water treatment firm Hyflux has found itself served with a notice of default by local authorities – the latest complication to an already-challenging restructuring journey, said observers.

PUB on Tuesday (Mar 5) said it has issued a default notice to Hyflux’s wholly-owned subsidiary Tuaspring Pte Ltd (TPL) for not fulfilling various contractual obligations, such as keeping Singapore’s largest desalination plant “reliably operational”, under a 25-year water purchase agreement.

When pressed for details, the national water agency would only say that Tuaspring “failed to provide plant capacity as required on multiple occasions”. It declined to say more, citing “confidentiality obligations”.

“PUB has been in talks with TPL regarding its defaults all this while,” a spokesperson told Channel NewsAsia on Thursday. “As much as possible, we have allowed TPL time to resolve its operational and financial defaults but our concerns have been growing.”

The default notice, while not exactly unexpected, poses “huge implications” for Hyflux’s restructuring, said the president of the Securities Investors Association Singapore (SIAS).

“It is not a surprise because the company is now clearly insolvent,” said Mr David Gerald.

Hyflux’s latest financial accounts showed net liabilities of S$136 million for the first nine months of 2018, after taking a hefty S$916 million impairment on the carrying value of Tuaspring and other project receivables.

Given that the end of 30-day default cure period falls on the same day as the creditors’ meetings on Apr 5, the SIAS chief sees PUB’s notice as an “ultimatum” for Hyflux to get its scheme passed.

“I don’t know if it’s a coincidence but only with approval from the shareholders then can the company go back to PUB to say it now has S$530 million on the table and it can continue with Tuaspring.”

“If restructuring fails and Tuaspring is taken over by PUB, the company will be in dire straits because the white knight will walk away and there are no other white knights in sight,” added Mr Gerald. “It is now all in the hands of the investors.”

OCBC summarises it further in the following note:

The Public Utilities Board (“PUB”) has issued a default notice to Tuaspring Pte Ltd (“Tuaspring”) requiring Tuaspring to remedy certain defaults associated with contractual obligations in the Water Purchase Agreement between PUB and Tuaspring. These defaults relate primarily to operational reliability as well as demonstrating ongoing financial ability to continue running the plant.

- In a separate release by HYF confirming receipt of the default notice, the default cure period end date is 30 days from 6 March which is 5 April, the date of the scheme meeting. Importantly, the notice also states that this date could be extended “as may be reasonable for Tuaspring to consult with PUB”.

- Both releases confirm that should the defaults remain unresolved by the default cure period end date, then PUB has the sole discretion to terminate the Water Purchase Agreement and takeover Tuaspring. As terms of the agreements between PUB and HYF are non-public, it is unknown if any compensation would be paid on the takeover.

- This development follows the recent release of updated unaudited financial information by HYF as at 30 September 2018 which indicate a significant write-down in asset values including Tuaspring. We find total book value of common equity (ie: excluding perpetual and preference shares) to be negative SGD1.0bn as at 30 September 2018, with the company’s liabilities exceeding assets. In contrast, total book value of common equity was SGD112.8mn as at 31 March 2018 based on 1Q2018 unaudited financials and SGD120.2mn as at 31 December 2017 based on 2017 audited financials. This though is not the only factor in the default notice, with operational issues that were previously undisclosed now also apparently plaguing Tuaspring. Operational issues were reported by the media to have started since 2017.

To simplify matters, Hyflux had signed a contract with PUB regarding the supply of water, that included certain obligations as to their operational reliability, and financial standing. Given that they are now technically insolvent, they have breached these obligations. As it turns out, PUB has a right under the contract to takeover Tuaspring if Hyflux fails to comply with these obligations.

And PUB just served Hyflux with a notice of default this past week. Interestingly enough, the date to remedy the breach ends on 5 April, the date of the Scheme Meeting. In other words, if the Scheme of Arrangement is not approved, PUB may have the right to takeover Tuaspring.

So what are the implications of this? OCBC has another good note:

- In our view, if the instances of operational issues at Tuaspring are merited, PUB is well within their rights in issuing a notice of default. The existence of clauses spelling out private party defaults are normal in public-private-partnership agreements to protect offtaker rights and ensure continuity of service delivery, hence PUB’s actions could be merely a matter of process at this stage in reserving their rights to takeover Tuaspring should the Scheme collapse as soon as practical and in accordance with current agreements.

- This announcement comes at a difficult time, as HYF now must deal not only with creditors under the Scheme Arrangement (as well as creditors at the asset level) but also PUB to ensure the overall restructuring can be completed. This is because the restructuring agreement with SM Investments Pte Ltd (“SMI”) is conditional on Tuaspring remaining within HYF’s corporate structure. Should Tuaspring be taken back by PUB, then SMI is entitled to walk away from the Restructuring Agreement hence leading to a collapse of the Scheme. Another complication is the rights and reaction of Maybank (sole secured lender of Tuaspring), whose recovery values are now increasingly uncertain in the face of PUB’s notice of default to potentially takeover the asset. As a recap, terms of the agreements between PUB and HYF are non-public and we are unable to determine the compensation levels (if any) to creditors and equity investors of Tuaspring (ie: HFY).

- In our view, the likelihood of liquidation has increased as a result of this announcement. Even if PUB can be assured that the defaults can be cured, the reputational damage is likely to have lasting impacts on HYF’s ability to win future projects hence diminishing the potential future value of the equity provided for in the proposed restructuring scheme. This means the decision making process will be more driven by short term recovery considerations rather than longer term ones. In the context of our conclusions in our Special Interest Commentary dated 21 February 2019, we think the Scheme is now harder to reject for bondholders. Conversely the impact for perpetual security and preference share holders depends on the reliance on the proportionately larger component of equity as part of total recoveries. In our view, apart from a more compressed timeline and higher urgency towards negotiating a better outcome, those that already saw little recovery value in the proposed terms are unlikely to view their position as diminished versus before.

- We think in a best case scenario that PUB will need to extend the default cure period on the assumption that operational issues can be resolved but that PUB will need to wait on the results of the Scheme to assess if HYF’s financial issues are resolved. Other scenarios are difficult to hypothesize given the multiple interested parties and their divergent stance. (OCBC, PUB, Company).

For the record, I absolutely agree with OCBC credit research (and I am very impressed by their analysis and generous commentary on this topic).

PUB is fully within their contractual right to serve this notice. And if I were PUB, I would definitely do so, because it reserves me the right to takeover Tuaspring if anything goes wrong with the restructuring.

For everyone else however, this is a huge problem, because Tuaspring is just about the main (only?) asset of value left in Hyflux. If PUB takes over Tuaspring, there’s really no saving the company, and creditors may get close to nothing.

The way I see it, the best way out for creditors, may be to agree to split the equity portion of the contingent pot with senior and junior creditors, and for all creditors vote in favour of the restructuring. Of course, being able to renegotiate the split of assets between senior and junior creditors (ie. the minimum 25 cents recovery for senior vs 10.7 cents recover for junior) would be the best case, but given where we are in the restructuring process, I would be less optimistic on such an outcome.

And all this has to be negotiated before voting on the Scheme of Arrangement, because if the vote on 5 April fails, the chances of liquidation have gone up due to the PUB notice.

Closing Thoughts: What will be the value of Hyflux post restructuring?

Given that so much of the recovery to retail investors comes in the form of Hyflux shares, it’s also helpful to take a look at how much these shares will be worth post restructuring.

The Straits Times has this to say:

Hyflux has taken a $916 million impairment for the nine months ended Sept 30, to adjust for a fall in carrying value of the Tuaspring water and power plant and other write-downs.

…

The impairment has put the Hyflux group in a net liability position of $136 million, indicating that the group is insolvent. Mr Gerald said: “Hyflux will thus be valueless if no restructuring is done.”

However, if creditors consent to haircuts under its proposed restructuring scheme, Hyflux will return to a net asset position of $1.1 billion, according to the group’s pro forma calculations. Mr Gerald said: “This means that the company may have positive value post restructuring.”

Post-restructuring, Hyflux’s pro-forma net tangible assets (NTA) per share would be 4.2 Singapore cents, based on an NTA of $815.3 million distributed across an enlarged share base after an equity injection and various debt-for-equity swaps.

Indonesia’s Salim Group and Medco Group had earlier agreed to give Hyflux a $400 million equity injection in exchange for a 60 per cent stake in the company post-restructuring. Effectively, Salim-Medco is buying into Hyflux at 3.4 cents a share.

If the Salim-Medco deal goes through, Hyflux’s debt securities holders and senior unsecured lenders will be cleaned off the balance sheet.

One thing that we’ve learned from this whole saga, is that Hyflux is essentially a water company, that was, and is, betting its entire existence on electricity prices. After oil and gas prices fell in 2015, electricity prices fell, and Tuaspring became a loss generator, that coupled with crippling debt, eventually took the company down. If in the near future oil and gas prices go back up, and electricity prices go back up, the plant would be raking in the dough once again. So interestingly enough, the future of the Hyflux’s shares, depends to come extent on the price of oil / gas.

Of course, Hyflux’s future also depends on its ability to launch and build new projects. After this entire saga, would anyone in Singapore still trust them with a large infrastructure project?

Then there’s the intentions of SMI. The fact that SMI is willing to step in and bail out Hyflux for a 60% stake in the company, indicates to me that SMI finds that there is value in the company post-restructuring. What is uncertain though, is SMI’s plans for the company going forward. Do they intend to run Hyflux as a going concern post-restructuring, given all the hit to Hyflux’s brand name? Or do they intend to break up the company and sell it for parts?

There’s just a lot of uncertainty over the value of the Hyflux shares going forward.

Till next time, Financial Horse, signing out!

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!