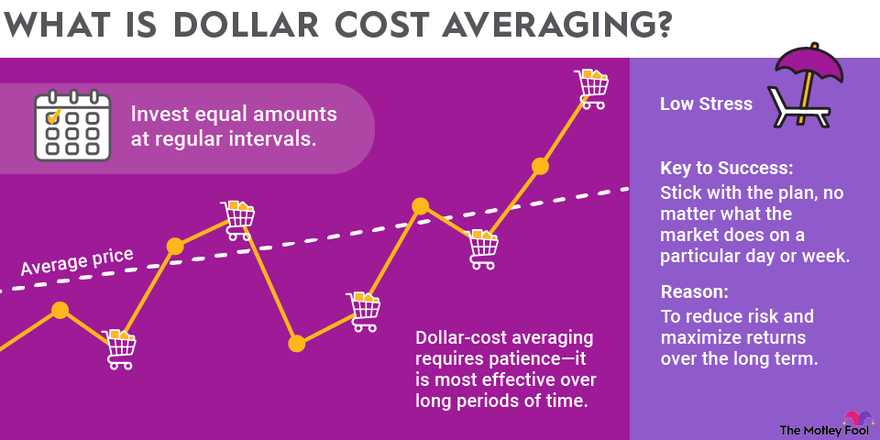

Dollar-Cost Averaging (DCA) is a popular investment strategy that is often recommended to investors.

How does it work?

An investor invests a fixed amount of money at regular intervals, regardless of the stock price.

The goal is to reduce the impact of volatility. DCA style of investing can potentially lower the average cost per share over time.

However, is DCA is the best way to buy stocks? Let’s explore.

This article is written by a Financial Horse Contributor.

Advantages of DCA

DCA helps to reduce emotional decision making when it comes to stockis.

Since DCA involves automatic, regular purchases, it helps investors avoid the temptation to time the market or make emotional investment decisions based on market fluctuations.

DCA smoothens out the effects of market volatility, which can reduce the risk of investing a large lump sum during a market peak.

It encourages a long-term, disciplined investment approach, making it easier for individuals to stick with their investment plans.

While there aren’t many high-profile investors publicly credited with making fortunes solely through DCA, the strategy has shown consistent success for ordinary investors over long periods of time.

S&P 500 Historical Success (Over Time)

One of the best illustrations of the success of DCA comes from the performance of the S&P 500. Historically, the S&P 500 has averaged around 8-10% annualized returns over long periods (after inflation).

Example: An investor who regularly contributed $500 per month to an S&P 500 index fund from 1980 to 2020 would have experienced massive growth, especially due to compounding returns. Even through market crashes like the dot-com bubble, the 2008 financial crisis, and COVID-19 pandemic, the long-term growth trend would have allowed them to accumulate significant wealth.

DCA is also the backbone of most retirement savings strategies, particularly in employer-sponsored plans like 401(k)s in the USA. In these plans, workers contribute a fixed amount of their salary regularly, usually into diversified funds. Over decades, these contributions grow significantly through compounding returns, even if the market experiences short-term volatility.

Disadvantages of DCA

Missed Opportunities in Bull Markets

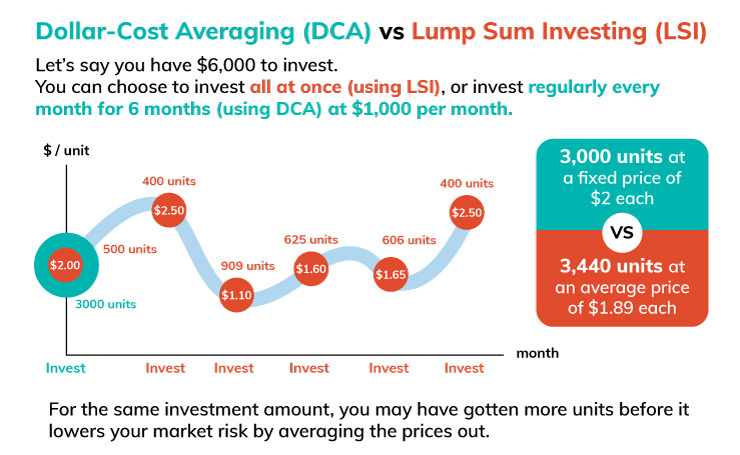

In a steadily rising market, lump-sum investing (putting all your money in at once) might outperform DCA because you’re investing less as prices continue to rise.

One of the biggest risks with DCA is the potential opportunity cost during a long-term bull market.

-

Lump-Sum vs. DCA: In a rising market, a lump-sum investment (investing all at once) often outperforms DCA. If you spread out your investments over time while prices are consistently rising, you end up buying fewer shares at higher prices compared to investing a lump sum early on when prices were lower.

Example: If you had $10,000 to invest at the start of a bull market, lump-sum investing could have delivered better returns compared to spreading the investment over, say, 12 months, because stock prices would likely be higher each month.

DCA reduces risk during periods of volatility, but if the market experiences a prolonged bear market or a flat market, returns can be suboptimal.

Example: During the “lost decade” of 2000 to 2010, the S&P 500 experienced almost zero growth due to the bursting of the dot-com bubble and the 2008 financial crisis. An investor using DCA during this period may not have seen much growth, as the market stagnated for a long time.

Slower Capital Deployment

If you have a significant amount of money to invest, DCA can result in a slow deployment of your capital, which may lead to missed opportunities in strong-performing markets.

Impact of Transaction Costs

Frequent investments can lead to increased transaction costs, such as brokerage fees, which may erode investment gains over time. It’s crucial to consider these costs when implementing a DCA strategy, as they can offset the benefits of regular investing.

False Sense of Security

Investors may develop a false sense of security with DCA, believing it completely shields them from market volatility. While DCA can mitigate some risks, it doesn’t eliminate the inherent uncertainties of investing, and investors may still experience losses, especially in prolonged bear markets.

Types of investors that best suit DCA style of investing?

Beginner Investors

New investors who are just starting and may not have a large sum of money to invest. DCA allows them to contribute smaller amounts over time.

Risk-Averse Investors

Those who are wary of market volatility and prefer a steady, measured approach to building their portfolio.

Long-Term Investors

People with a long-term investment horizon, such as retirement savers, who can benefit from the compounding effect of regular investments over many years.

Investors who do not have time or energy to track markets

Those who don’t have the time or interest in following daily market fluctuations but still want to invest regularly.

Types of investors that may not suit DCA style of investing?

When markets are steadily rising

DCA underperforms lump-sum investing in a rising market.

When you have a high-risk tolerance

DCA is not designed to maximize returns. It’s more about minimizing risk, which might not appeal to investors who are willing to take on more risk for potentially higher rewards.

When markets are flat or inflation is high

In a stagnant or high-inflation environment, DCA might not be as effective.

Types of stocks that suit DCA?

- Broad Index Funds (e.g., S&P 500): DCA works well with index funds and ETFs that track the broader market, as it allows you to capture long-term market growth while mitigating short-term volatility.

- Dividend Stocks: Regular investments in dividend-paying stocks can allow you to reinvest dividends and take advantage of compounding over time.

- Large-Cap and Stable Companies: Blue-chip stocks of well-established companies, which are less prone to extreme volatility, are often ideal for DCA.

- Growth Stocks: Stocks with strong long-term growth potential, though volatile in the short term, may benefit from a DCA strategy as it allows you to buy during dips.

When DCA may not be ideal?

In a strong bull market…

If the market is experiencing a prolonged upward trend, a lump-sum investment might outperform DCA.

For experienced traders…

Those who have a deep understanding of market timing and trends might prefer a more active, strategic approach to maximize returns.

Plus, you can always do both!

A mixture of a DCA style of investing for certain types of stocks, and a more active component for other types of stocks that capitalize on your area of expertise can certainly work as well.

Overall, DCA is particularly well-suited for long-term investors, those who want to reduce risk and stress from market timing, and those investing in diversified, stable assets like index funds or blue-chip stocks.

Do you adopt a DCA style investing for your own portfolio?