So I received this really great question on China recently:

Hi FH,

Happy new year!

There’s been a bunch of articles (on WSJ, BBG etc) that cautions China’s deflation problem and its risk of becoming another lost-decades Japan. I’ll put the links below. Let me know if you lack access.

I actually find myself largely agreeing with these.

There is also a big issue of demographics not even addressed, brought about by the 35-40 years of the One-Child Policy, that I don’t see any easy way they can resolve. By 2050, 40% of the population will be 60+ years old.

Some have also pointed to the dictatorship, censorship, and other undemocratic stuff being bear factors to the economy. I normally don’t agree with these being bad for a country – I think these are fine as long as you have a really really good leader (LKY wasn’t too dissimilar when in comes to these undemocratic attributes, and look at how SG succeeded). But if the dictator is a bad leader, boy it can really ruin a country for decades.

I’m already of the mind that China is at best a 1-2 year swing trade (mainly because they still have some ammo for stimulus), but as a long term multi-year holding, wow – I think China isn’t going to cut it, at least not when weighed against the “opportunity set” out there.

People tell me western media is biased, and I’m sure they are. But if you think about it – aren’t we a little biased as well here when we keep our faith in China? (because we’re Chinese by race, haha)

Keen to hear your views. Maybe you can challenge me here. And any thoughts on the demographics problem?

This is an FH Premium post written in Jan 2025, that I am making available to all readers (as many of you have been asking for my views on China).

If you find content like this helpful, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

Summary of the 4 articles

The four articles are a good read, and I’ve attached the full articles to this post for those who want a deep dive.

I’ve summarised my key extracts (emphasis in bold from me) below.

First Article: https://www.wsj.com/world/china/china-xi-debt-economic-plan-13aaeec1?st=WfZBSW&reflink=article_copyURL_share

People close to Beijing’s decision-making say that Xi views the economic challenges China faces as necessary pains in the process of replacing old growth drivers, including real-estate investment, with newer sources, such as high-value manufacturing including cars and chips.

…

And as exports are among the few bright spots in the Chinese economy these days, China needs to maintain its ability to sell to its major trading partners as much as possible to prevent another big hit to overall growth.

…

With a rematch of Trump vs. China coming, hopes are emerging among some Chinese economists that a new trade war will finally force the Xi leadership to shift its manufacturing-centric economic policy toward one more focused on empowering consumers. If Trump follows through with his promise to impose higher tariffs, they reason, Chinese exports would inevitably decline and Beijing would have to bolster domestic demand to keep the economy going.

But the world has changed since Trump’s first term. Both sides are more dug-in.

Evan Medeiros, a former senior national-security official in the Obama administration, said Xi’s leadership style will make it hard for China to manage Trump 2.0 effectively.

“I just don’t see Xi forging a grand bargain,” he said.

Second Article: https://www.wsj.com/world/china/china-economy-excess-debt-gdp-46c69585?st=U3y5ox&reflink=article_copyURL_share

China’s economy today is burdened with excess: Millions of empty or unfinished apartment blocks, trillions of dollars in debt straining local governments and ballooning industrial production driving an export surge that is igniting trade tensions worldwide.

China still has strengths: It dominates global manufacturing and has commanding positions in new technologies, such as electric vehicles and renewable energy. Policymakers have proven adept at handling past crises, and are readying bold new stimulus to support the economy.

Nonetheless, the scale of the excesses plaguing China’s economy underscores the perilous position Beijing finds itself in as a new trade war looms.

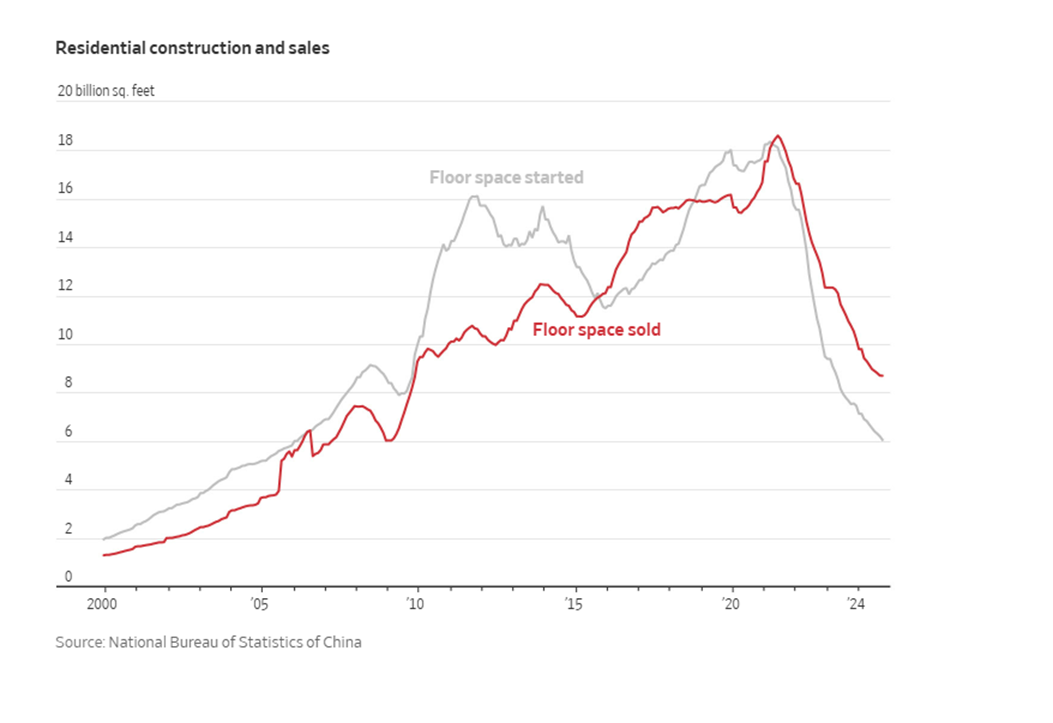

Some great charts below to illustrate what is happening.

Debt levels for China are very high – hence the need to deleverage:

While there is a massive amount of unsold residential stock that together with the fall in real estate prices – has led to a destruction of household wealth (and poor consumer sentiment):

China’s share of global manufacturing is massive – any increase in market share will come at the expense of others – not easy in this age of Trump and tariffs:

Third Article: https://www.wsj.com/world/asia/china-must-heed-lessons-of-japans-lost-decades-3a1491a8?st=FoeF5B&reflink=article_copyURL_share

Fourth Article: https://www.bloomberg.com/news/articles/2025-01-07/china-investors-sound-alarm-over-japan-style-deflation-as-yields-hit-record-low

“It’s a downward spiral that will keep getting worse if it’s not corrected,” said Xin-Yao Ng, a Singapore-based investment director at abrdn Plc, which oversees $494 billion globally. “There’s a psychological element to Japan’s lessons where the longer this persists, the weaker business and consumer confidence gets.”

…

“The bond market is already telling the Chinese people: ‘you are in balance sheet recession’,” said Koo, chief economist at Nomura Research Institute. The term, popularized by Koo as a way to explain Japan’s long struggle with deflation, occurs when a large number of firms and households reduce debt and increase their savings at the same time, leading to a rapid decline in economic activity.

It’s not that Chinese authorities haven’t taken action. A sweeping stimulus package rolled out since late September has given the struggling economy a lifeline, with President Xi confident the country has met its around 5% growth target for 2024. For this year, top officials have vowed bigger fiscal spending and made boosting domestic demand a top priority. Some say the economic slowdown is a necessity for China to transform into an advanced economy driven by high-tech industries, away from the debt-fueled model of the past.

The problem is that the policy prescriptions so far haven’t been nearly ambitious enough to reverse falling prices, with weak consumer confidence, a property crisis, an uncertain business environment combining to suppress inflation. Data due Thursday will likely show consumer price growth remained near zero in December while producer prices continued to slide. The GDP deflator — the broadest measure of prices across the economy — is in its longest deflationary streak this century.

…

To be sure, not everyone accepts the balance sheet warning, pointing to the big differences between China today and Japan during the late 1990s, particularly China’s lower average income — which gives it more room for growth.

Lower spending by households and corporations suggests only a “partial balance-sheet recession” in China, said Wang Yingrui, an economist at AXA Investment Managers. She said the spending power of the central government is helping paper over the cracks, at least for now.

The accumulation of stimulus and a possible bottoming out of the housing market could see the economy rebound in 2026, according to David Qu, an economist for Bloomberg Economics. The property sector’s drag on the economy may ease while new industries including electric vehicles will be playing a bigger role, he added.

…

But Japanification — if it really happens — will also create opportunities for investors. In several reports published last year, Chinese brokerage Haitong Securities Co. looked at the winners of Japan’s lost decades, pointing to opportunities in investments including high-dividend stocks, technology companies with room to grow and exporters with diverse revenue streams.

…

Some, like veteran emerging-market investor Mark Mobius, believe China has the tools to avoid following Japan’s fate. “Since the government has an outsized control over the economy, they have the ability to implement financial measures designed to reduce or even eliminate many of the negative elements,” he said.

Japan’s economy only started to respond positively once policymakers “finally began to directly transfer funds to the people’s pockets,” rather than plow money into infrastructure and companies, said Jesper Koll, an expert director at Monex Group Inc., who has been researching Japan for decades. It “took basically 20 years before politicians learned that lesson — I hope China’s leaders have learned this lesson and have the wisdom to boost the people’s purchasing power.”

My views – China no doubt has the tools to solve this – the question is whether they want to?

I know that’s a lot of information above.

So let me try to summarise below as simply as I can on how I am viewing the situation in China.

The fundamental problem here, is that China relied very heavily on real estate / construction spending the past 15 years.

That changed during the 2018 – 2021 period, when they stopped fuelling real estate / construction growth with debt.

And given that this sector amounted to about 30% of the China economy, once it started to slow, this left a big hole in the economy that needed to be replaced.

The way China tried to replace it, was via manufacturing / export growth – especially in new economy stuff like solar and EVs.

The problem of course, is that when your country is as big as China, you need huge export growth to move the needle.

And when China is already 30%+ of global manufacturing, it comes a point where any further gain in market share is going to come at the expense of someone else.

That someone else notably being the US, Japan, and Germany – all of which have reacted very warily to Chinese attempts to grow exports (this is a beggar thy neighbour strategy – as China’s export growth to US/Germany/Japan does not conincide with an increase in imports from US for example).

And it doesn’t take a genius to sense the shifting winds especially with Trump in office – if China keeps focussing on manufacturing / export growth, at some point other countries will react with tariffs.

So if your country is as big as China, and you cannot grow manufacturing to replace real estate, what are your options?

The only realistic option – is domestic consumption.

This is where things get tricky, for 2 reasons.

First is that because of the fall in real estate prices, consumer sentiment is poor (as a large percentage of Chinese household wealth is tied up in real estate).

Second problem, is that to raise domestic consumption, you basically need to raise household income levels.

And to raise household income levels, you need to raise wages.

And when you raise wages, this raises cost of production, which weakens China’s manufacturing price competitiveness.

Follow Financial Horse to avoid missing any post!

So you can see how there is a fine balance here for policy makers

The solution to this problem (real estate deleveraging) is (a) manufacturing and (b) domestic consumption.

But push on the manufacturing lever too hard, and other countries respond with tariffs.

Push on the domestic consumption level too hard, and manufacturing competitiveness declines.

What is the right balance between the two, and in what level to offset the real estate deleveraging, is the million dollar question here.

In a nutshell – that’s basically the dilemma facing China policy makers today.

But… China has the tools to solve it if they want to – but there will be consequences

The good news though, is that much of the debt is denominated in RMB.

And when the debt is denominated in RMB, it means that China has all of the necessary tools to solve the problem via money printing.

The only question is whether they want to or not.

When your country is as big as China, every move has consequences.

Depreciate the RMB and it releases a deflationary shockwave through the world (given how many countries import from China).

Even if you print money – it matters how you spend it.

Spend it to reinflate the real estate bubble and you benefit homeowners, but do nothing to solve the underlying structural problems with the economy (kicking the can down the road).

Spend it to give consumers to spend, and you inevitably raise production cost via higher wages (less competitive manufacturing/exports).

So yes – I agree with almost all the points that I extracted from the four articles above.

The question is what path will China policy makers take – when confronted with current constraints?

Demographics issue

The reader also asked a question on demographics, so let me share my views on this first because I go into investment implications.

Yes, no doubt China is facing a ageing population (as is almost every other developed country like Japan, Singapore, Korea etc).

The solution to this for China is simple – technology + productivity increase.

By and large, China’s labour today is not as productive as other developed nations on a per capita basis.

It’s simple math – when labour cost is cheap, there is little incentive to find a need to make labour more productive.

But once labour costs goes up – the need becomes apparent.

And you already see this in China with the transition towards use of robotics, and use of information systems / technology to improve worker productivity.

And look at companies like Bytedance, and it’s fairly clear that they have what it takes to become efficient and operate at the highest level.

This is a country with 5000 years of history, much of which operating at the top tier of human technology and ingenuity.

If you ask me whether they have what it takes to solve the current problems, my answer is a resounding yes.

To me the entire problem is less a question of capability, and more of desire + ability to enact the reforms to increase labour productivity.

Similar to the problem above with the economy.

They have the means to solve it, the problem is whether, and when, they will solve it.

What will China policy makers do

So in some ways the question comes back to what policy makers will do.

And boy that is not an easy one to answer.

One school of thought is that policy makers will do the bare minimum to avoid systemic risk, while continuing to allow the economy to deleverage and slowly transition into new areas of growth (like manufacturing).

Another school of thought is that post-Sep 24, policy makers will step in to do whatever it takes to rescue the economy, the only reason why they have not acted in a big way thus far is because they are waiting to see what Trump does.

Personally I’m somewhat in the camp that of “policy makers will do whatever it takes to avoid systemic risk, while continuing to allow the economy to deleverage and slowly transition into new areas of growth”.

But frankly, I don’t think it matters all that much what I think here.

You need to have a view, but you have to keep an open mind and be fully aware that your view could well be wrong.

But as an investor – it is risk-reward that matters

So that’s the 10,000 ft view.

Which is interesting from an academic perspective and all that.

But as investors – the question is how to make money.

There was a liner in the article that caught my eye:

But Japanification — if it really happens — will also create opportunities for investors. In several reports published last year, Chinese brokerage Haitong Securities Co. looked at the winners of Japan’s lost decades, pointing to opportunities in investments including high-dividend stocks, technology companies with room to grow and exporters with diverse revenue streams.

Looking at my China portfolio last year – it delivered a 27% return last year.

So yes you can say all you want about China’s economy being weak and all.

But hey my China portfolio still managed to make money last year.

With relatively low correlation to US/Singapore stocks.

So… are China stocks a good investment?

In my view, China stocks have very cheap valuations.

A lot of bad news is priced in at these levels, which means that if news turns slightly less bad, there could be upside.

This is in stark contrast to US / Singapore where generally speaking valuations are no longer cheap, and are pricing in quite an optimistic future.

This means that if the future turns out to be slightly less optimistic, there is downside risk.

I think if you look at the right places, and size well, I continue to think there is opportunity in China given the above.

But it’s also fairly obvious to me that China carries idiosyncratic risk.

If you’re not comfortable with China, just skip it, and invest in US / Singapore instead.

It’s really as simple as that.

The universe of investments is so big that there is literally no need to be in any investment you are not comfortable with.

And the way I see it, the bigger the sell-off in China stocks, the cheaper valuations get, and the more pressure on policy makers to respond, the more attractive the risk-reward.

But in investing, it’s always about risk management risk, returns second.

If you can’t stomach the risk, it’s a simple decision to just skip China.

For me at least, I’m running decent exposure to to China today, and you can see my full portfolio breakdown (and what stocks I use to gain exposure to China) on FH Premium.

This is an FH Premium post written in Jan 2025, that I am making available to all readers.

If you find content like this helpful, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly)

FH

As always, great sharing and very informative .

Always enjoyed reading your articles!

Thank you for the time and effort.

Best wishe

kk

Thanks for the kind words! Glad that it’s helpful.

Bull market rises from overly pessimism as always

Indeed!