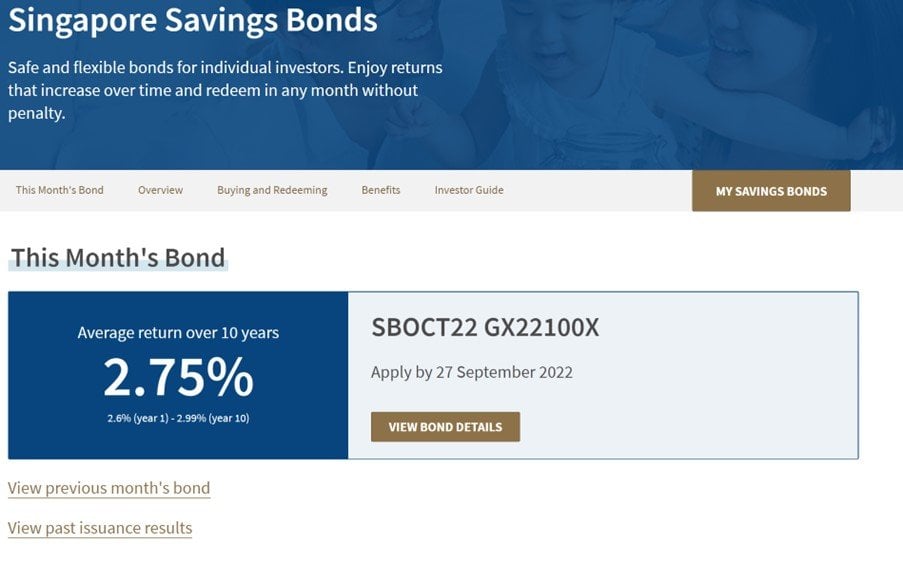

So the latest Singapore Savings Bonds (October) are out.

Interest rates are below, and at 2.75% over 10 years it’s actually lower than last month’s (2.8%).

I’ve been getting some questions on why Singapore Savings Bonds interest rates are going down despite a rising interest rate climate.

I’ve also been seeing a lot of discussion on how T-Bills or fixed deposit are a better place to park your cash.

So I wanted to share my views in this article, including why I’m still buying the Singapore Savings Bonds (instead of T-Bills or Fixed Deposit).

Latest Singapore Savings Bonds yield 2.75%

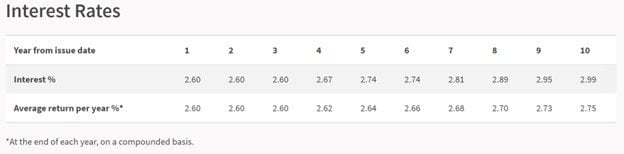

Interest Rates for the latest Singapore Savings Bonds (October) are below.

To sum up:

- 1st year interest rate of 2.6% (which stays flat for 3 years)

- 10 year interest rate of 2.75% (annualized)

For the record, this was last month’s Singapore Savings Bonds (September), where:

- 1st year interest rate was 2.63% (stepping up to 2.71% in year 2 and 3)

- 10 year interest rate was 2.8% (annualized)

So… last month’s Singapore Savings bonds was *slightly* better than this month’s.

Very slight difference only though.

Better allocation of Singapore Savings Bonds this month?

For the record, the maximum allocation for last month’s Singapore Savings Bonds was $13,500 per person.

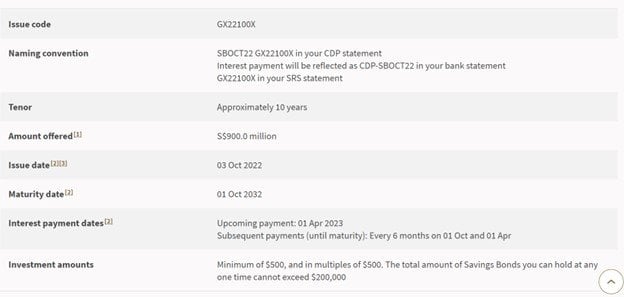

Issuance size this month is exactly the same as last month (S$900 million).

And since this month’s Singapore Savings Bonds have a lower interest rate, it stands to reason they would be less popular.

Which means we might get even bigger allocations this month – bigger than $13,500.

Why are interest rates on Singapore Savings Bonds going down?

Quite a few of you have reached out to ask why are interest rates on the Singapore Savings Bonds going down, when US interest rates are going up relentlessly.

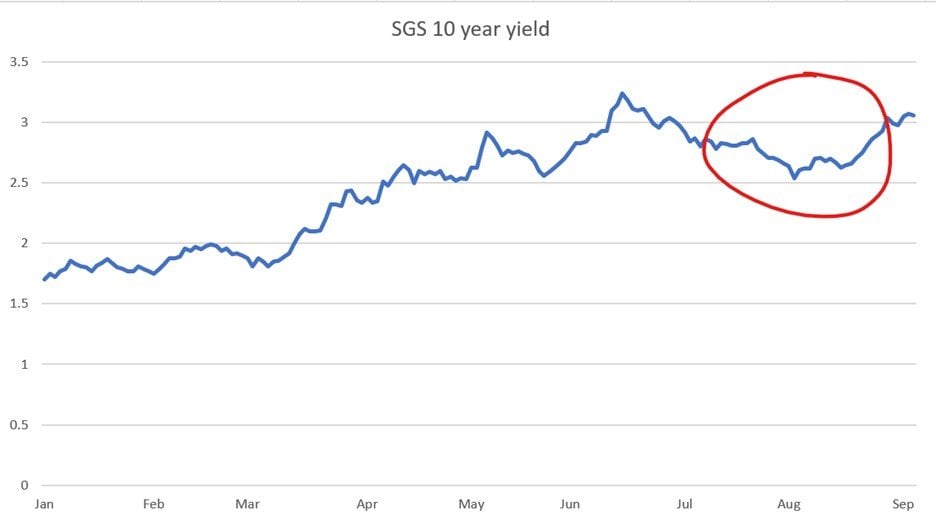

The short answer, is because bond prices went up in August – so bond yields went down.

Singapore Savings Bond yields track the latest bond yields, and so the Singapore Savings Bonds yield went down.

Here’s the 10-year Singapore Government Security yield in 2022, you can quite clearly see the part circled in red where yields went down in August.

Now the slightly longer answer, is that nothing goes to hell in a straight line.

Just like how in a bear market for stocks, you get multiple vicious rallies on the way down:

Well, it’s the same with bonds, and interest rates.

Interest rates are going up, and the market is pricing in a peak of 4.5% Fed Funds Rate this cycle.

But that doesn’t mean bond yields are going to go from 1.5% to 3.5% in a straight line.

There are going to be rallies along the way, where bond yields go down.

Exactly what we saw in August:

Will interest rates continue going up?

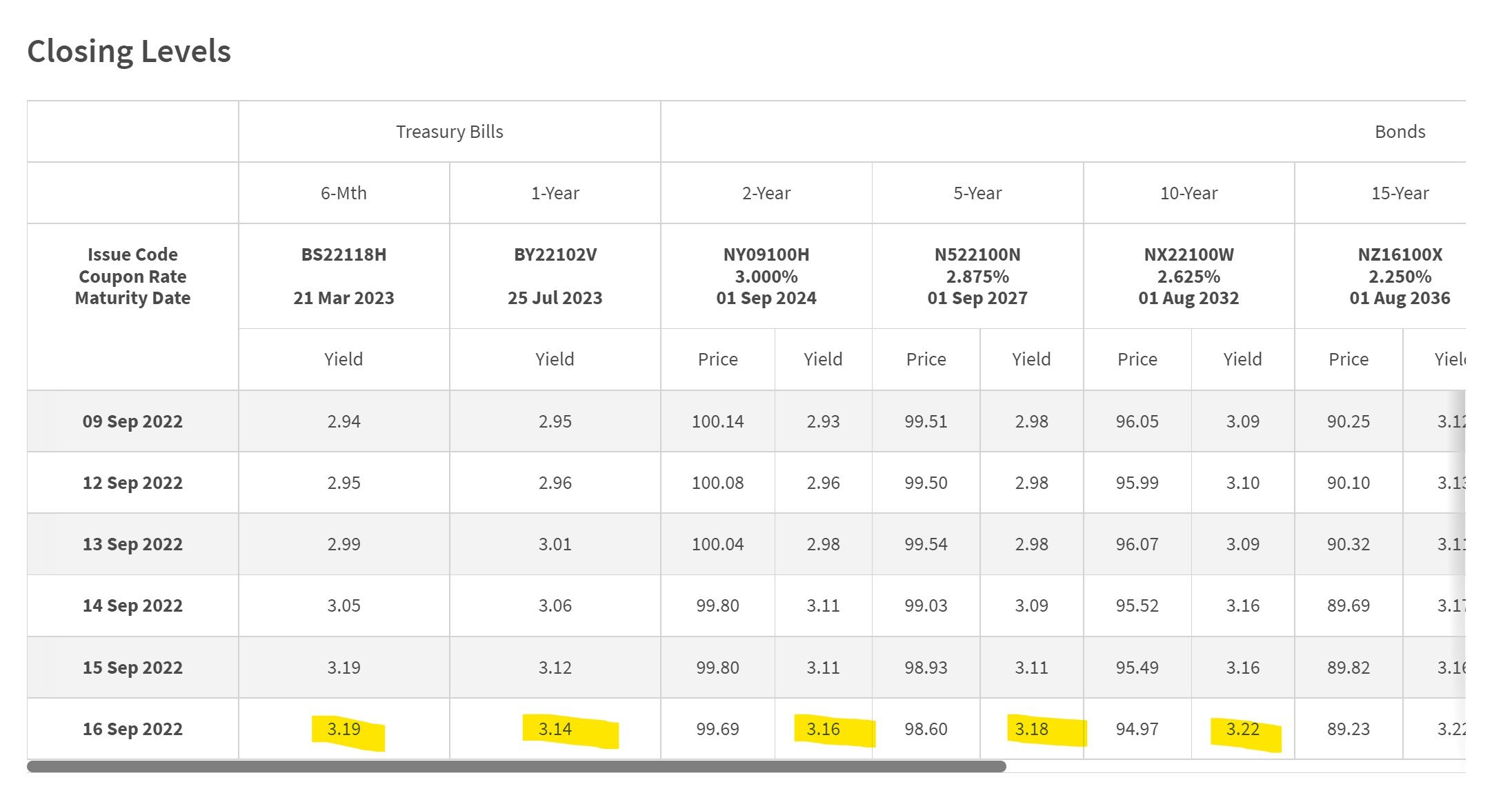

For the record, interest rates have already gone up.

Here’s the latest SGS pricing, where the 10 year has already broken past the 3% (sits at 3.22% now).

If things stay this way, we’re going to see next month’s Singapore Savings Bonds look much more attractive than this month’s.

Where will Singapore Savings Bonds yield peak this cycle?

Now I’m just going to venture out on a branch here because quite a few of you have asked.

For obvious reason, nobody knows how the future is going to play out, so this is just going to be a wild guess from this horse.

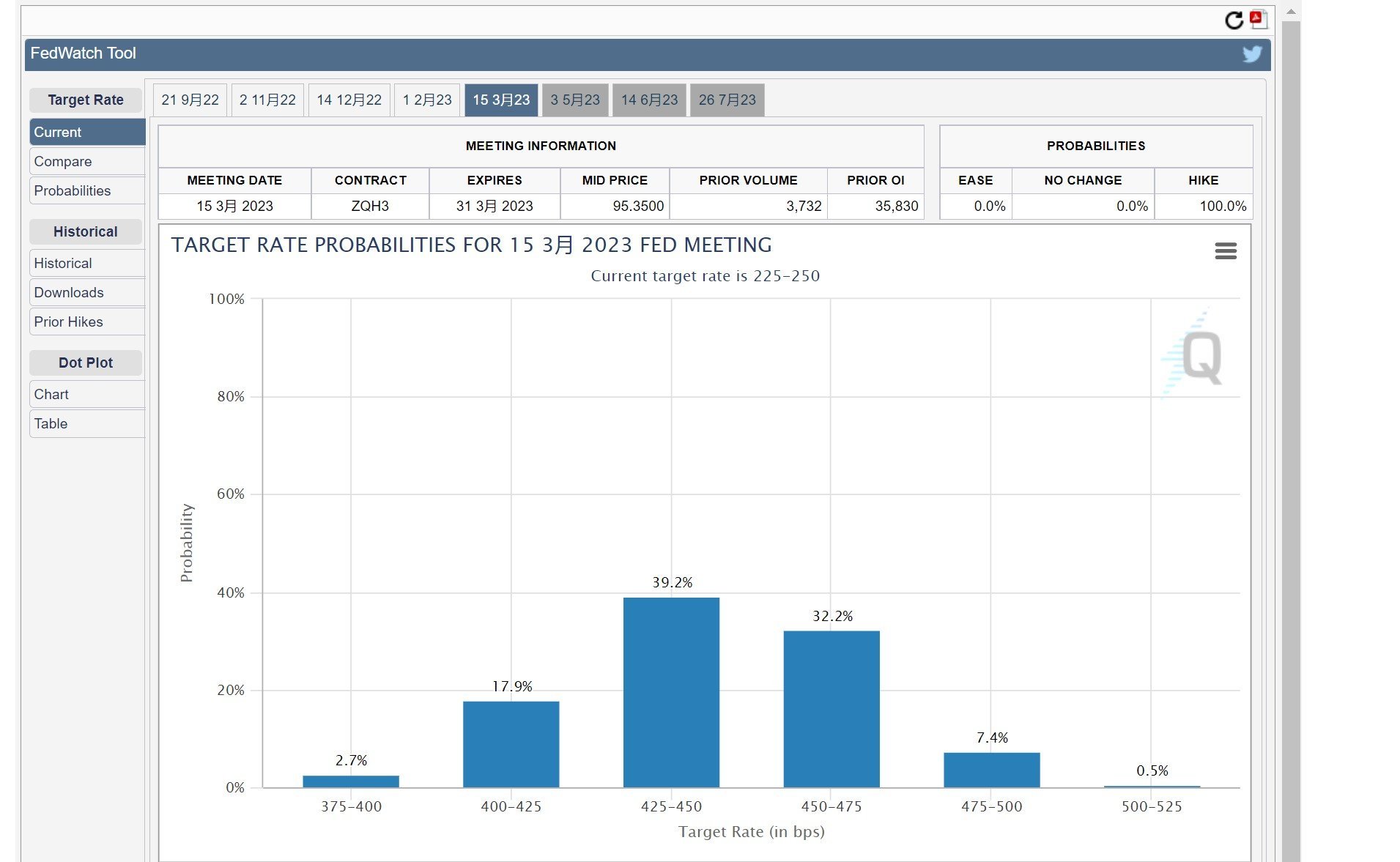

With the latest CPI print out this week, it looks short term interest rates (ie. Fed Funds Rate) for the US will top out at the 4.25% – 4.75% range.

This isn’t just this horse being hyperbole – after the past week the futures market is pricing in peak Fed Funds Rate of 4.5% by March 2023:

Now the US 10 year yield is determined by market forces, so it’s not so straightforward to call.

Based on what we know today, I think a US peak 10 year yield of 3.75% – 4.25% is reasonable (we could even go higher depending on how tight liquidity for treasuries gets).

Because of SGD strength, let’s be conservative and assume a slightly lower peak in the 10-year Singapore Government Security.

I think you could see the 10 year SGS (and Singapore Savings Bond) peak at 3.5% – 4.0% this cycle, give or take.

Of course, many things can go wrong, so do take this with a pinch of salt.

If the economy absolutely collapses in 2023, the Feds could cut interest rates very rapidly, and we never go near the 4.0% Fed Funds Rate.

If inflation stays sticky, like the data the past week shows, we may go even higher than the numbers above.

Based on what we’re seeing though, the economy is still holding up for now, so talks of a Fed pivot are still a bit too early.

Will I still be buying Singapore Savings Bonds?

Short answer – yes, I will.

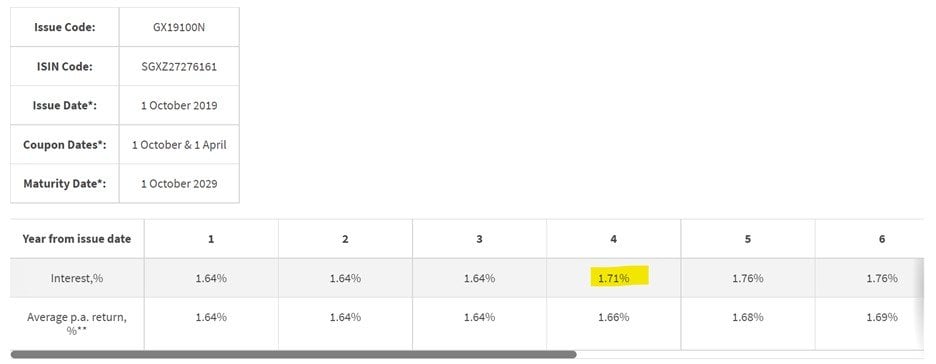

I have a bunch of Singapore Savings Bonds back from 2019.

Even though we’re moving onto the 4th year now, they still only pay 1.71% interest:

So it’s almost a no brainer to redeem the 2019 Singapore Savings Bonds and rotate them into these new 2022 Singapore Savings Bonds that pay 2.6% first year.

Almost a full percentage point higher.

Of course, based on what I shared above I think the Singapore Savings Bonds may headed higher to the 3.5% – 4.0% range.

But Singapore Savings Bonds can be redeemed any time, so if (when) that happens, I’m free to just redeem and reapply then.

In any case, the problem for now is trying to get a meaningful allocation given the hot demand for Singapore Savings Bonds, so I’m just going to try and get whatever amount I can get my hands on for now.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Will I buy T-Bills or Fixed Deposit?

I know many of you like T-Bills or Fixed Deposit.

The best Fixed Deposit pays 2.85% for 12 months, absolutely risk free.

The latest T-Bills pay 3.3%+ for 6 months, again absolutely risk free.

That said, I still prefer Singapore Savings Bonds.

There are no free lunches in investing, but the Singapore Savings Bonds is as close as it gets.

The 2 main advantages for Singapore Savings Bonds for me are (1) Liquidity, and (2) Locked in interest rates.

Liquidity

I think that some time in the next 12 – 18 months, there is a good chance something will break in the global economy or financial markets.

When that comes, I want to be hoovering up risk assets.

Sidenote that you can see my full stock and REIT watchlist on Patreon, together with target prices.

To buy assets in a crash, you need cash.

So in times like this, liquidity is king.

With a Singapore Savings Bond you can get your cash back anytime with accrued interest. The maximum wait time is 1 month, if you are really unlucky and pull them at the start of the month.

T-Bills

With T-Bills – yes I get that the interest rates are higher than Singapore Savings Bonds.

But just try selling a T-Bill.

Close to impossible.

This means that with T-Bills you’re sacrificing the liquidity for the higher yield.

That may be okay for some investors, but that’s not okay for me.

Fixed Deposit

Fixed Deposits are slightly better though, in that you can get the money back if you really need, after paying a small penalty fee (in the form of lower accrued interest).

So I suppose if I really wanted a place to park my cash, it would go into Fixed Deposit.

Locked in Interest Rates

The other point – is that with Singapore Savings Bonds you have the option to continue holding on for 10 years.

Let’s say I’m completely wrong on the interest rate outlook.

Let’s say in January 2023, the economy completely collapses, and the Feds cut back to zero interest rates.

With your T-Bills and Fixed Deposit, once they mature you are going to be rolling into rock bottom interest rates.

That’s interest rate risk right there for you.

Whereas with the Singapore Savings Bonds, worst case if I am absolutely wrong on interest rate outlook, I’ve already locked in these rates for the next 10 years.

And there’s a lot of value in that.

Of course, the problem with Singapore Savings Bonds is that allocations are very poor, so I guess maybe there is no free lunch in this world after all.

Does it make sense to wait for higher interest rates before applying for Singapore Savings Bonds?

For what it’s worth, it’s a good question.

Do you apply for the October Singapore Savings Bonds, despite knowing full well that interest rates are likely to head higher in the months ahead?

I think the answer ultimately needs to depend on the individual.

If you don’t have a lot of cash lying around, and don’t want to go through the hassle of applying and redeeming, you could probably just wait for higher rates.

But if you do have a lot of cash, then your primary worry would be about allocation. Because even at $13,500 allocation size, it will take many months to hit your full $200,000 allocation.

And you may want to seriously consider T-Bills or Fixed Deposit as an alternative for your cash, so you can enjoy some interest in the interim.

Whatever the case… I will be applying for the October Singapore Savings Bonds

In any case, I’m going to applying for the Singapore Savings Bonds again.

For the reasons shared above, I like these Singapore Savings Bonds over T-Bills and Fixed Deposit.

The low allocation numbers are a real bummer, but hopefully with slightly lower interest rates this month we’ll get more meaningful allocations.

Let’s see!

Timeline for Application / Redemption of Singapore Savings Bonds

Timeline for application and redemptions are set out below.

Don’t forget to submit by 9pm on Tuesday, 27 September if you want to apply (or redeem)!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

There’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I did the same for my own mortgages and found it pretty useful.

Do give it a try .

As always, this article is written on 18 Sep 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with , a zero commission broker.

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.