As some of you will know, there is a new REIT IPO coming.

NTT DC REIT – a data centre REIT sponsored by NTT.

It’s the first big name REIT (or rather any big stock listing) listing on the SGX for years.

So I was pretty keen to cover this REIT.

I was actually looking at NTT DC REIT over the weekend, and the final pricing just came out today.

So here’s my updated views, including latest IPO pricing.

Unlock Your Financial Edge with FH Premium

Enjoy this exclusive FH Premium analysis—now free for all readers! But why stop here?

By subscribing to FH Premium, you’ll gain:

- Weekly Macro Deep-Dives

Understand where the global economy is headed—and why it matters for your wallet. - Regular Buy/Sell updates from my personal portfolio

See exactly what I’m adding to (or trimming from) my portfolio and act before the crowd. - Comprehensive Watchlists

Full stock & REIT watchlists, updated regularly with target prices, entry zones, and risk considerations. - My Personal Portfolio

Transparent tracking of every position I hold—and why—so you learn the “what, why, and how” of smart investing.

Join hundreds of savvy readers who’ve turned FH Premium insights into real returns. Ready to level up your investing?

Subscribe to FH Premium today and never miss a market-moving idea.

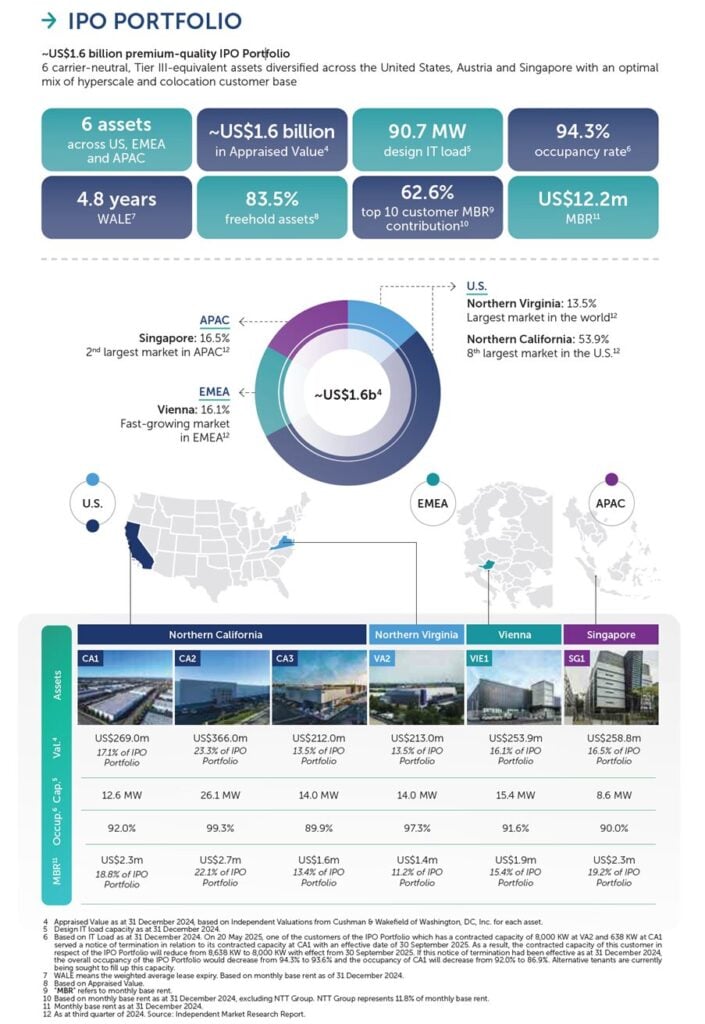

Summary of NTT DC REIT IPO Portfolio

High level summary of the NTT DC REIT IPO property portfolio:

- NTT DC REIT’s seed portfolio consists of six carrier-neutral data centres:

- four in the USA (Ashburn VA and three in Sacramento CA),

- one in Vienna (AT)

- one in Singapore.

- ¥240.7 bn (US$1.57 bn) agreed transfer value.

- Assets span completion years 2001-2023, giving a balanced mix of mature cash-flowing facilities and a brand-new European flagship.

Portfolio snapshot

- Geographic mix by IT load: USA 72 %, Europe 17 %, Singapore 9 %.

- Weighted-average building age: ~12 years (young relative to global DC peers).

Long story short – it is a primarily US focused data centre portfolio, with assets in Europe and Singapore as well.

| Location | Year built | Net data floor (m²) | IT load (MW) | Occupancy* | Notes |

| Ashburn, Virginia, USA | 2016 | 7,204 | 14.0 | 97.3 % | Part of NTT’s VA campus in the world’s largest DC market |

| Sacramento, California, USA | 2001 | 7,718 | 12.6 | 92.2 % | Legacy facility; recently upgraded power & cooling |

| Sacramento, California, USA | 2011 | 8,249 | 26.1 | 99.4 % | Campus anchor; highest-capacity asset in seed lot |

| Sacramento, California, USA | 2015 | 6,018 | 14.0 | 89.9 % | Expansion phase completed 2020 |

| Vienna, Austria | 2023 | 8,317 | 15.4 | 91.5 % | Brand-new Tier III+ facility; strategic EU gateway |

| Serangoon North, Singapore | 2012 | 5,040 | 8.6 | 90.0 % | Edge node serving APAC hyperscalers |

*Occupancy rates as of 31 Dec 2024.nttdata.com

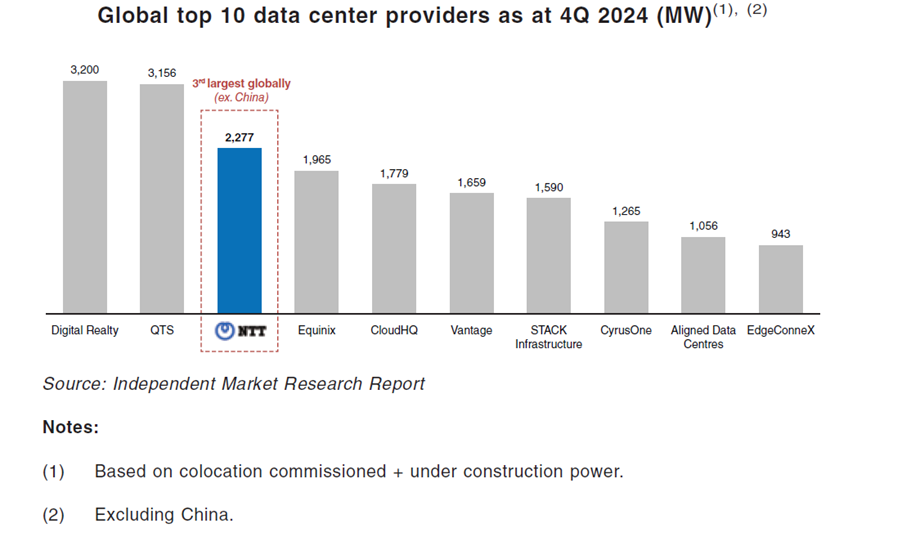

Who is NTT? Are they a solid sponsor?

Now one of the most important things we look at when considering whether to buy a REIT, is to look at who is the sponsor.

The sponsor of NTT DC REIT is NTT.

Which is Japan’s incumbent telco and the world’s #3 colocation operator, running 150 + data centres in >20 countries via NTT Global Data Centers (GDC).

You can see the charts below, and they are a big player:

| Dimension | Key facts | Why it matters |

| Corporate strength | • Nippon Telegraph & Telephone Corp. (NTT) FY24 revenue ≈ ¥13.4 tn (~US$84 bn) • Credit ratings: A-/stable (S&P), A3 (Moody’s), AAA (JCR). | Investment-grade parent lowers counter-party risk and can backstop funding if needed. |

| Data-centre expertise | • NTT GDC operates >150 DCs / c. 1500 MW IT load across Americas, EMEA & APAC; targets +1 GW by 2028. | Scale, engineering depth and purchasing power support uptime, procurement and ESG capex. |

| Sustainability commitment | • Net-zero by 2040; 51 % renewable usage (non-IT load) in FY23. | Aligns with MAS/SGX push for green disclosures; future-proofs energy-intensive assets. |

| ROFR / growth pipeline | • Continual land banking (e.g., 174 ac Mesa AZ; 53 ac Milan IT; 32 ac Tochigi JP). | Provides NTT DC REIT with visible acquisition optionality without third-party sourcing. |

NTT already sponsors NTT UD REIT in Tokyo (listed 2002).

Generally speaking, the track record for the Tokyo listed NTT UD REIT is decent.

With two decades of asset-recycling, 96 % occupancy and steady external growth.

- Alignment: NTT routinely sells mature assets to the J-REIT below replacement cost, signalling willingness to seed growth.

- Governance: 20-year listing history with no major related-party controversies.

I know some of you will argue that the same may not apply to the SGX listed REIT.

But frankly – no way of knowing for certain until the REIT develops a track record in Singapore.

Alignment of interests of Sponsor?

NTT as Sponsor holds 25% of NTT DC REIT post listing – which I think is an acceptable number.

What I like about NTT DC REIT

You’re getting exposure to data centres which is probably the hottest real estate asset class right now.

With a strong sponsor pipeline.

Backed by a decent sponsor.

35% gearing is on the low side:

And 70% fixed rate loans provide protection in the event of any sudden jump in interest rates:

A fuller table setting out what I like about NTT DC REIT:

| Driver | Why it matters | Evidence |

| Secular demand for DC capacity (AI, cloud, edge) | Sustains occupancy & pricing power across cycles | Market overview; NTT GDC’s 2.2 GW portfolio & global footprint |

| Sponsor ROFR “double-up” pipeline (130 MW in 5 yrs, >2 GW long-term) | Embedded external growth; could more than triple AUM without third-party sourcing | |

| Geographic diversification – US, Singapore, Austria (3 Tier-1 markets) | Mitigates single-market regulatory or demand shocks | IPO portfolio disclosure |

| Low starting leverage (~35 %) with headroom to statutory 50 % | Provides debt capacity for accretive acquisitions before equity dilution; conservative balance sheet | |

| 70 % debt fixed/hedged; all-in cost 3.9-4.0 % | Shields earnings from near-term rate spikes; optional upside if rates fall |

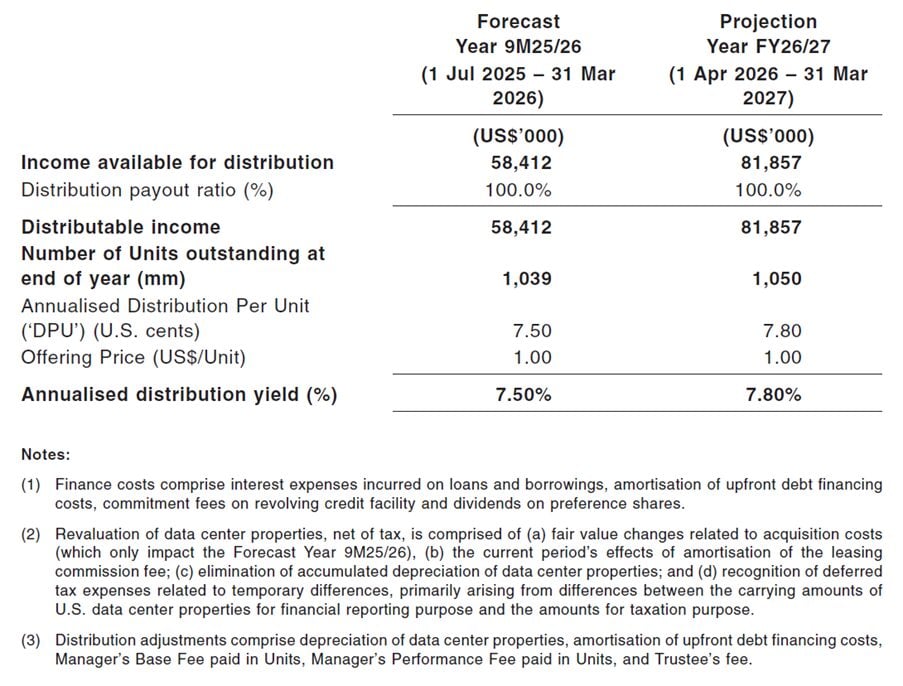

Pricing / Dividend Yield of NTT DC REIT

But probably the most attractive point in my view – is the pricing / dividend yield.

NTT DC REIT is marketing its IPO at:

- 7.50% – 9M25/26 distribution yield

- 7.80% – FY26/27 distribution yield.

That is pretty attractive, because among data centre REITs:

- Keppel DC REIT trades at ~4.4 % annualised yield

- Mapletree Industrial Trust (MIT) offers ~6.4 % annualised yield.

NTT therefore carries a c. +300 bp yield premium vs. Keppel DC and c. +120 bp vs. MIT.

| REIT | Asset focus | Forward yield* | Trailing-12M yield | Leverage (latest) |

| NTT DC REIT (IPO) | US 72 %, EU 17 %, SG 9 % | 7.0 – 7.8 % (prospectus FY 25/26 range) | n/a (new listing) | ~35 % post-listing |

| Keppel DC REIT | Asia-Pac 81 %, EU 19 % | 4.4 % (annualised 1Q 25 DPU) | 4.1 % | 38 % |

| Mapletree Industrial Trust | 54 % DC / 46 % hi-spec industrial | 6.4 % | 6.9 % | 40 % |

| Digital Core REIT (for context) | US DC (wholly USD) | c. 5.9 % | 5.9 % | 38 % |

*Forward yields are broker/issuer projections annualised to March- or December-year-end as disclosed in the cited sources.

Before you add, yes I know Keppel DC REIT is a largely Singapore data centre portfolio which deserves a valuation premium, while Mapletree Industrial Trust is only 50% data centres.

But personal view is that even factoring in the above factors, I think NTT DC REIT at current pricing, it decent risk-reward.

Never miss a market beat—ride with Financial Horse wherever you go!

Get timely insights, sharp analyses, and real-time alerts by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox, plus early access to special reports and FH Premium previews

Key risks of NTT DC REIT

To sum up the key risks:

| Category | Specific risk |

| Macro / markets | Recession, high inflation & energy prices squeeze power-intensive DC margins and dampen demand; FX swings (USD/EUR/SGD) affect NAV & DPU |

| Tenant concentration & competition | Hyperscalers may self-build or renegotiate; industry consolidation could reduce customer base |

| Operational resilience & cybersecurity | Outages, security breaches, or power failures (e.g. CA1 generator event 2022) can trigger SLAs, reputational damage & churn |

| Power-supply dependence & cost pass-through | Rising wholesale electricity prices and third-party supply failures directly hit NOI |

| Acquisition & integration execution | Overpaying, capex overruns, or inability to embed assets efficiently erodes accretion |

Why did Digicore REIT fall so much post IPO? Will the same repeat here?

But frankly – to dive a bit deeper into the biggest risk I see.

Is to look at the case study of Digicore REIT, which soared 15% on listing.

Before having an almost 70% drop in share price.

Will the same repeat here?

What exactly drove the crash?

To summarise the sequence of events for Digicore REIT:

| Event (chronology) | Share-price impact |

| Dec 2021 – IPO at US$0.88; closes first day at US$1.01 | +15 % debut pop |

| Apr 2022 – Sungard Ch 11 (5th-largest tenant) | stock down to c.US$0.70 |

| 2022 – Fed lifts rates 525 bp | higher discount rate across S-REITs |

| Nov 2022 – final US IRC §1446(f) withholding rules on PTPs | brokers restrict US-asset REIT trading; incremental selling pressure |

| Feb–Jun 2023 – Cyxtera credit-downgrade & bankruptcy (22 % rent) | panic low US$0.37 on 10 Jun 23 |

| Nov 2023 – Cyxtera assets sold / leases restructured | rebound to US$0.50s |

| FY 2024 – higher unit base & disposals | muted |

What drove the crash for Digicore REIT?

To break down what caused the big drop in share price:

| Trigger (2022-23) | Impact on DCRU | Root cause |

| Tenant bankruptcies (Cyxtera 22 % rent; Sungard 7 %) | 63 % price draw-down | Over-reliance on two speculative-grade tenants |

| Rapid Fed hiking – SOFR +525 bp | DPU cut ≈12 % | 100 % floating debt, minimal hedges |

| Section 1446(f) tax & liquidity squeeze | Retail broker lock-outs, widening spreads | All-USD asset base |

Will the same repeat here?

A Digital-Core-style price collapse looks unlikely but not impossible for NTT DC REIT: the IPO starts with lower gearing, broader tenant spread and 70 % fixed-rate debt, reducing the main triggers that sank Digital Core.

The biggest tail-risks are power-cost/FX shocks and any single hyperscaler exceeding 20 % of rent; neither is presently at that threshold, but both need monitoring.

Near-term downside is more macro- than idiosyncratic; a repeat crash would require simultaneous tenant distress and rate/power spikes, a lower-probability combo versus 2022-23.

But that being said, look at the list of Top 10 customers and there is some concentration risk right at the top.

Like I said, lower risk – but not impossible.

That being said, there is no investment with zero risk, it’s about taking measured risk.

Will I buy NTT DC REIT IPO?

All that said and done.

Would I buy this REIT?

I think the answer is going to be yes.

It just comes down to pricing for me.

Yes no doubt there are risks associated with the REIT.

But when you benchmark NTT DC REIT against comparable data centre REITs on the SGX.

Even after adjusting for the risk profile.

I think the 7.5% – 7.8% forward yield is attractively priced.

| REIT | Asset focus | Forward yield* | Trailing-12M yield | Leverage (latest) |

| NTT DC REIT (IPO) | Global DC (US 72 %, EU 17 %, SG 9 %) | 7.0 – 7.8 % (prospectus FY 25/26 range) | n/a (new listing) | ~35 % post-listing |

| Keppel DC REIT | 100 % DC (Asia-Pac 81 %, EU 19 %) | 4.4 % (annualised 1Q 25 DPU) | 4.1 % | 38 % |

| Mapletree Industrial Trust | 54 % DC / 46 % hi-spec industrial | 6.4 % | 6.9 % | 40 % |

| Digital Core REIT (for context) | US DC (wholly USD) | c. 5.9 % | 5.9 % | 38 % |

Note that the public offer size is miniscule

That being said – note that the public offer size is miniscule.

Public Offer is 30million units, which works out to US$30 million.

Which is frankly miniscule.

So I don’t expect to get a large allotment (if at all).

And if we get a decent pop in share price on IPO, I may just sell the position entirely, as holding a small position is not really meaningful for me.

Sidenote that GIC is taking up 9.8% of the REIT post-listing, which I think is not too bad as GIC is known as being long term investors in the real estate space.

How to apply for NTT DC REIT IPO?

The public offer opened on 7 July 2025, at 9pm.

And will close on 10 July 2025 at 12.00 p.m.

That’s only 2.5 days, which is quite a short offer window.

So don’t forget to get your bids in if you’re keen.

Application is via the usual ATM, internet banking, or mobile banking of the local banks.

Love to hear what you think!

Will you apply for NTT DC REIT IPO?

Unlock Your Financial Edge with FH Premium

Enjoy this exclusive FH Premium analysis—now free for all readers! But why stop here?

By subscribing to FH Premium, you’ll gain:

- Weekly Macro Deep-Dives

Understand where the global economy is headed—and why it matters for your wallet. - Regular Buy/Sell updates from my personal portfolio

See exactly what I’m adding to (or trimming from) my portfolio and act before the crowd. - Comprehensive Watchlists

Full stock & REIT watchlists, updated regularly with target prices, entry zones, and risk considerations. - My Personal Portfolio

Transparent tracking of every position I hold—and why—so you learn the “what, why, and how” of smart investing.

Join hundreds of savvy readers who’ve turned FH Premium insights into real returns. Ready to level up your investing?

Subscribe to FH Premium today and never miss a market-moving idea.

Just a note: the 7.5% are possible due to a payout ratio of 100% for the first two years. Afte that it will be reduced to 90%.

I guess I will wait a bit and see how it develops.

Yeah that’s a fair comment. So the natural yield is closer to low 7ish. But after the post-IPO drop it does bring the yield up nicely though. Assuming no other big fundamental problem.