So I received this really interesting question:

Hey FH, thanks always for the content you put out, I have a question for you that may be outside your core content but nonetheless I would greatly value your opinion. I have a newly TOPed property that I initially planned to sell. However, it is in the CCR region (D9) and prices there are quite depressed as of late due to govt cooling measures (foreigner ABSD in 2023) and the decreasing number of MNC expats in SG.

Current offer would only net me 80k in net profits after subtracting accrued interest, agent fees and stamp duty. Being in CCR, the demand is very low with only 2 transactions so far this year, with high supply (over 50 2 BR listings for sale) from it’s new TOP status

My current thoughts are to either:

- Sell to unlock cash to invest in US equities as valuations drop over the next few months.

- Hold and rent out in hopes that economic instability causes a rotation into safe haven assets like SG real estate or some form of rate cuts buoy real estate volume here (is this wishful thinking?).

I am 70% likely to go with the first choice but want to hear your thoughts as well.

Thank you as always for your keen insight!

This was an FH Premium post written for subscribers only.

I am making this available to all readers in case it may help others out there.

If you find content like this helpful, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

There are a lot of things I don’t know about the investor…

For obvious reasons, there are a million things I don’t know that should influence the decision, for example:

- What is the value of the property relative to the overall net worth of the investor (big or small)

- What is the risk appetite / age of the investor

- Which property is this, and what is the outlook if held for another few years

- Is the selling price even realistic – given the large amount of supply (over 50 listed for sale), and low transaction volume

And so on.

But let me try to share my views based on what was given to me above.

Why Singapore residential property is unique as an asset class?

Generally speaking the 2 key points that make Singapore residential property an attractive asset class for diversification to me are:

- Tightly controlled demand-supply – such that prices over the longer term should track economic growth, without too much volatility

- Ability to leverage up to 75% LTV to finance the purchase

This to me, means that Singapore residential property has a fairly unique risk-reward profile, that isn’t very much correlated to other asset classes, and has diversification benefits in a portfolio.

What is the thought process I would use to make this decision?

To me, the Singapore residential property is the less volatile, less risky asset class.

US stocks are a much higher volatility, higher risk asset class.

If you sell the lower risk asset class to rotate into the higher risk asset class, there are 2 key points to consider:

- Risk appetite – can you stomach the risk?

- Level of sophistication – do you have what it takes to manage risk / manage the investment?

In some ways they are the same point.

If you are a sophisticated investor with 20 – 30 years trading in markets, and very confident in your abilities to manage risk, then hey maybe US equities is a pretty low risk approach for yourself.

But be honest with yourself.

If you not so sophisticated or familiar with risk management, then US equities could be a pretty volatile and high risk investment, with the potential for significant fluctuations both ways (both on the upside and downside).

In which case you need to be comfortable that you are taking on higher risk with this approach.

And is that something you are comfortable with – only you can answer that for yourself.

Follow Financial Horse to avoid missing any post!

What would I do? If I were in the same situation?

If this were me?

To be absolutely honest I would try to have my cake and eat it.

I would find a way to keep the condo investment – while also investing in US stocks.

Of course whether this is feasible depends very much on how much other assets the investor has beyond this property, and what percentage of his net worth this property comprises.

If it is small, I suppose it’s not really an issue because there will be sufficient assets to do both.

If it is a large proportion (which I suspect it is given the question), then a decision has to be made whether to keep the investment in condo or sell and invest in stocks.

If it were me, and in the latter situation – I think I would still do my best to keep the condo and rent it out, and then invest in US stocks with my spare cash (even though the US stocks investment amount would be smaller in this case).

But of course – you need to crunch your own numbers to decide if this is feasible.

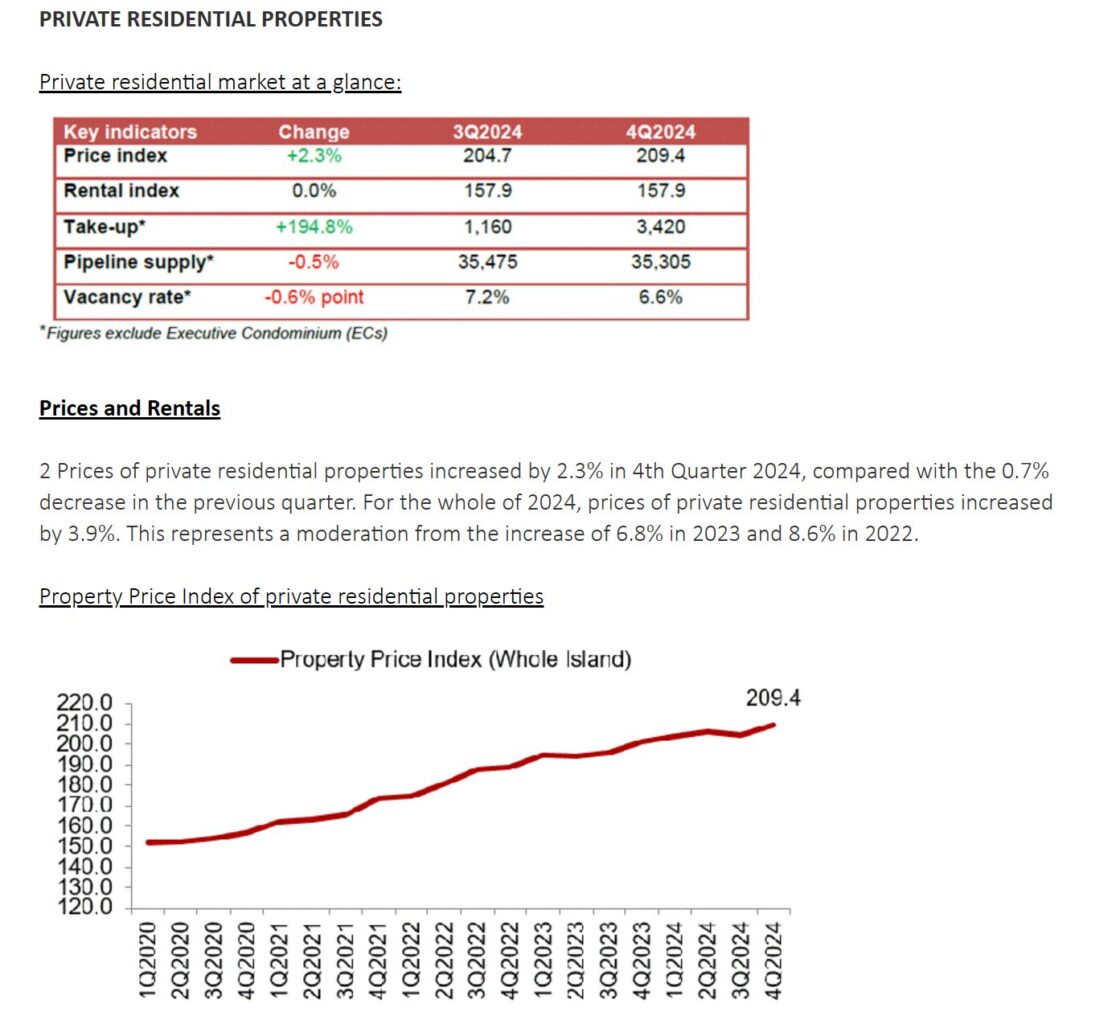

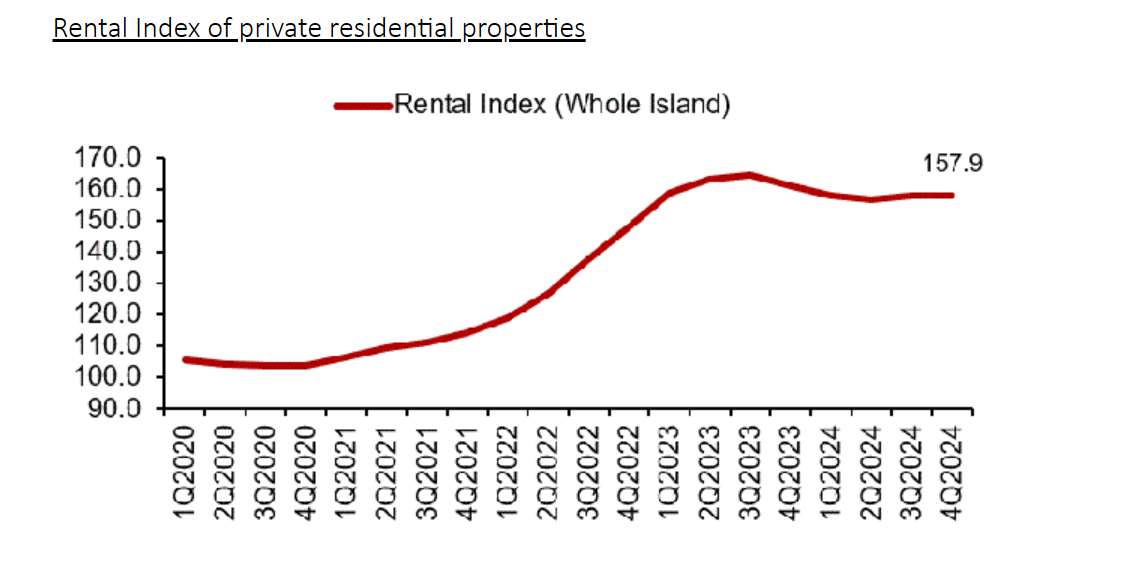

As you can see – rental prices have generally come down since the 2023 peak:

I don’t know I just like the idea of being greedy and having my cake and eat it.

This would also force me not to be lazy, and to find other ways to increase income, to increase the amount I have available to buy US stocks.

But hey frankly there’s no right or wrong here – it really depends on the investor in question.

Some people thrive under the pressure, some people can’t sleep at night with too much pressure – it really depends on who you are as a person.

That’s just how I see it.

Would love to hear what you think though!

Faced with a similar situation, would you sell the property to buy stocks?

This was an FH Premium post written for subscribers only.

I am making this available to all readers in case it may help others out there.

If you find content like this helpful, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

My own personal opinion would be for your first house/flat to viewed purely as a consumption not an investment

Reader should assess once risk profile and not just all in, reader would just end up being in an even worse situation than currently

This is a fair point, generally tend to agree with this.