So remember how I wrote an article last week saying that Singapore REITs are pretty overvalued right now? Well, since then, REITs have absolutely exploded in prices.

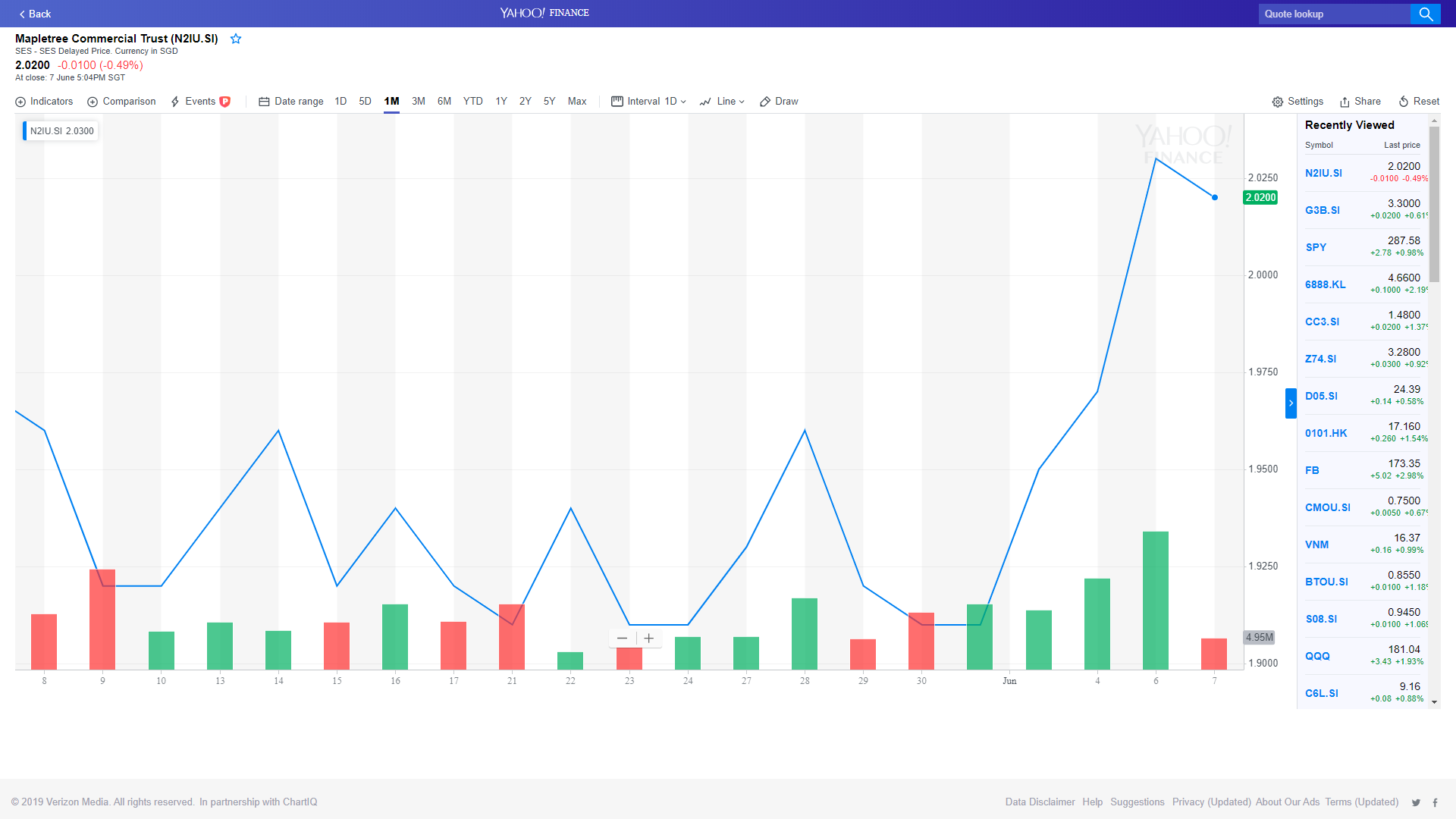

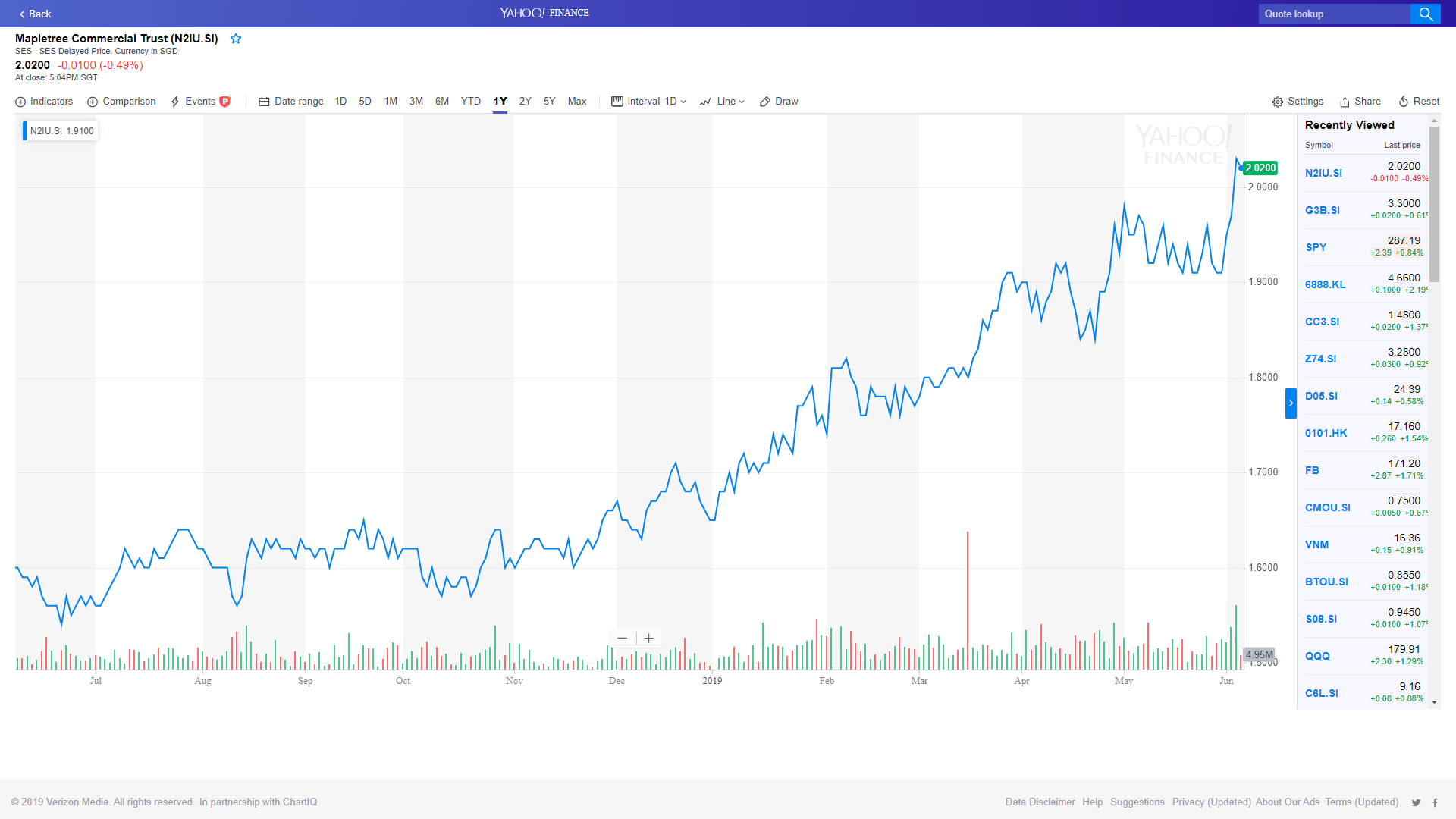

To illustrate – Mapletree Commercial Trust has gone up from 1.91 to 2.02 in the span of a week, a whopping 5.7% increase.

I received a couple of queries from readers on this, that I’ve set out below on an anonymous basis:

Hi FH,

Today I saw a sharp increase in almost all the prices of REITs especially MCT, MLT, CMT and FCT , given the poor economy outlook i was really surprised that the REITs market is booming like this. If possible may I know your opinion on this matter?

Thank you very much.

In other news: Mapletree Commercial just shot up to $2.05, 5 days after you (IMO rightfully) declared it as too expensive at $1.91 ?

I think my retirement REIT portfolio needs a plan B. The questions is whether to leave the units I bought at 1.7x untouched or not (given this portfolio is meant to outlive me). How do you go about yours?

To all of you guys out there, well, I’m wondering the exact same thing myself!

Basics: What happened?

Let’s briefly summarise what has happened the last 12 months. In early 2018, the projection from the Feds was for a total of 4 rate hikes in 2018, and 2 or 3 rate hikes in 2019.

Because of this, there was a huge sell-off in REITs, and it got to a point where just about every article I published on REITs would have a comment saying REITs are a poor investment right now due to the interest rate environment. But don’t just bash the facebook commenters, because I remember many big banks coming out with research reports that said the exact same thing (which just goes to show how much weight you should put on such forecasts).

Fast forward to end 2018, and the market thinking now is that the Fed had erred in hiking interest rates too aggressively, and that 2019 would see no further rate hikes. The Feds insisted this was not the case and that 2019 would see 2 to 3 hikes. Markets freaked out, and this eventually resulted in that huge December selloff.

Eventually in March 2019, the Feds realised the market was right after all, and they announced they would be pausing all rate hikes until further notice. This led to a huge risk-on mode for REITs.

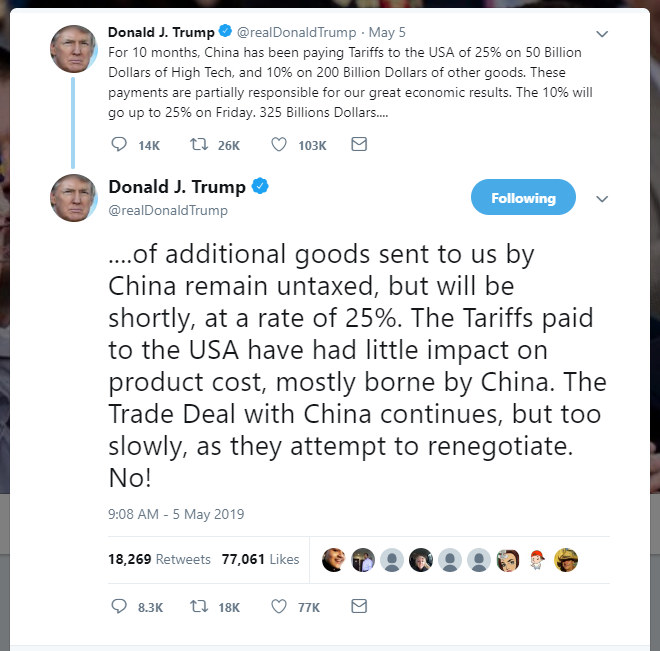

In early May, Trump unleased the one tweet that released shockwaves across global financial markets.

Because of the escalation in the trade war and the uncertainty on global businesses, the Feds came out this past Wednesday to state that they are prepared to cut rates in 2019 if necessary. This was exactly the catalyst the markets needed, and the moment S-REIT trading resumed after Hari Raya, they promptly shot up.

So we’ve basically gone from 4 rate hikes a year, to the Feds talking about rate cuts, in the span of 12 months or less. And that’s one reason why REITs have gone up so much.

Are REITs overvalued right now?

But are REITs actually overvalued right now? There are 2 metrics commonly used to value REITs, the yield spread, and the price to book ratio.

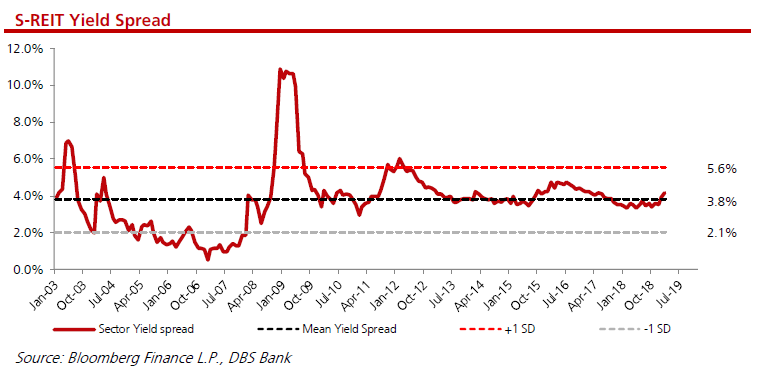

Yield Spread

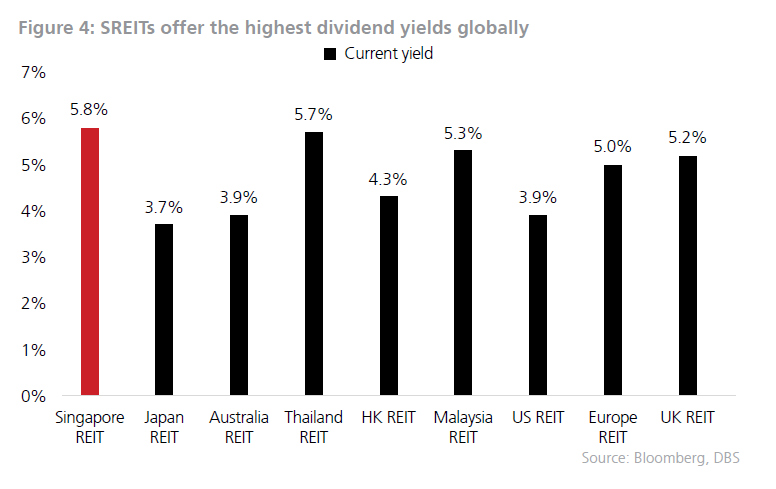

The yield spread is basically the difference in yield for Singapore REITs versus a 10-year Singapore Savings Bonds. The average yield for Singapore REITs is about 5.8%, the 10 year SSB is about 2.2%, which works out to an average yield spread of 3.6%.

The historical range is 2.1% to 5.6%, and the median is 3.8%, so we’re only slightly below the middle, but well within historical norms.

So based on yield spreads, Singapore REITs as an asset class are still looking pretty decently valued.

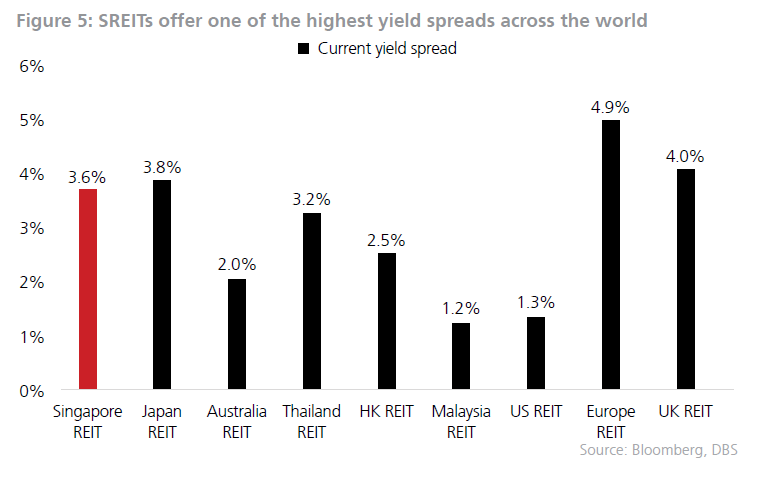

In fact as DBS argues, Singapore REITs still offer the highest dividend yields, and are pretty attractive when compared to other countries.

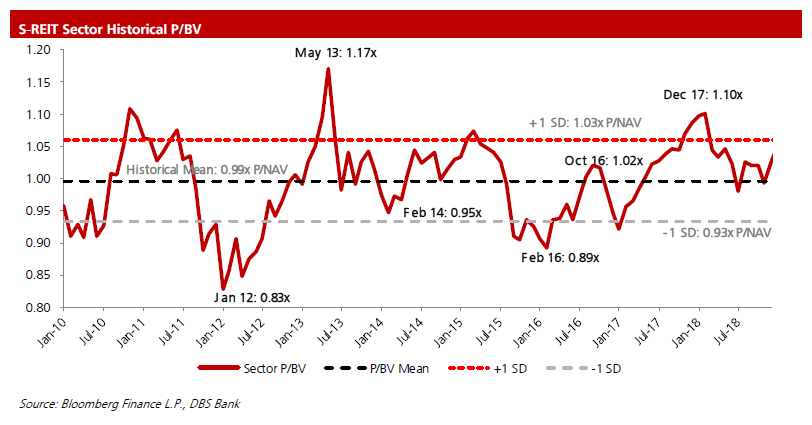

Price to Book Ratio

The current Price to Book ratio for S-REITs is about 1.1 times. The historical range is 1.03 to 0.93. So the Price to Book is on the higher side, but it’s nowhere near the point where it’s bubble territory.

So when you look at Singapore REITs broadly as an asset class, it turns out the yield spread is within historical norms, while the Price to Book is on the high side. But nothing that would come out and scream overvalued.

The problem though, is that average numbers don’t tell you the truth. Like the reader above highlighted, the big REITs, like those from CapitaLand, Mapletree, and Frasers, have gone up much more than the smaller REITs.

MCT in particular is now trading at a 1.26 times book value, and a 4.5% dividend yield (2.3% yield spread). And then you have stuff like Eagle Hospitality Trust, which is at 0.9 times book value and a 8.5% yield (6.3% yield spread). So yeah, average numbers tend not to be so helpful, because you have a situation where the big REITs are very expensive, whie the small REITs are still pretty cheap, so the average numbers look very attractive.

What happens next?

But just because Singapore REITs are slightly pricey, doesn’t mean they can’t get a lot more pricey in the future. Whether REITs are a good investment right now, depends a lot on what happens next.

The big one is going to be the rate cuts, and how the economy responds. The possible scenarios are:

- Rate cut – that results in economic recovery

- Rate cut – that is too late to prevent a recession

- No rate cut – and there is recovery

Rate cuts are big for REITs because they are basically leveraged plays on real estate. When interest rate drops, their interest repayments drop as well, increasing the distribution yield. Their yield also becomes more attractive when you compare it to the alternatives, so more people buy them, and prices go up.

Of course, the reason behind interest rate cuts matter as well. Don’t forget that at the end of the day, the REITs are making money from rental, and some poor guy has to pay these rentals. If you’re an office REIT and the economy is in recession, you can bet that your office tenants are going to want to renegotiate the terms of the lease. And as a responsible landlord you’ll want to give some concessions so they don’t go under. So REITs aren’t immune to the economy as well.

A lot of people expect the next recession to look like 2008. They expect that REITs will drop by 50%, and there will be a fantastic buying opportunity to set them up for the future.

I don’t necessarily agree with that. 2008 was a financial crisis that originated largely from the financial institutions. Financial Institutions bore the brunt of the impact, and this eventually spread to the main economy. REITs in particular were hit incredibly hard because of their inability to refinance, as the bank liquidity absolutely froze up (banks were afraid to lend to each other). So any REIT that couldn’t refinance, needed to tap the equity markets at depressed valuations, and this resulted in huge dilution.

This time round, banks are looking much better capitalised, so I don’t think they will be ground zero for the crisis. By contrast, the companies have had 10 years of near zero interest rates, and they have taken on huge amounts of debt, most of which ended up in share-buybacks, or large M&A deals. So I actually think that in the next crisis, it’s going to be the companies, and not the banks, that will be in trouble.

What does this mean for Singapore REITs?

Financially speaking, the REITs have become a lot more prudent than they were back in 2007. They’ve learned their lessons since 2008, and these days they have well-spaced out debt maturities on fixed rates. When the next crisis comes around, I think they’ll actually be able to manage their refinancing pretty well, especially since the banks are well capitalised. As long as you’re a big REIT with solid assets and a strong sponsor behind you, I don’t think there would be any problems refinancing.

The problem though, is the rental, because when tenants start renegotiating rental terms, or occupancy drops, that’s going to hit the bottom line, and translate into lower yields. But that’s a far more gradual process, as compared to a liquidity scare that could result in insolvency.

Because of this, I suspect that while REIT prices will still fall in the next recession, you may not necessarily be able to get the big blue chip Singapore REITs at the fire sale prices they were back in 2008.

What will the next crisis look like?

The discussion is becoming a bit more technical than I like, but it’s leading somewhere I promise.

Let’s take a step back, and look at the global economy now. What we have, is the European and Japanese economies at 0% interest rates, and the US economy at 2.5%. We are very late stage in the credit cycle, so at some point in the near future this will come to an end.

And that’s actually fine, because business cycles are part and parcel of how the economy works, and they’re vital to keep the economy going. It’s like a forest fire. You can delay the forest fire as much as you want, but eventually it still has to burn to get rid of the fallen trees, otherwise new trees will never grow.

But when you have a recession with most developed nations at 0% interest rates, how are you going to stimulate the economy. The usual method is to slash interest rates, but that no longer works because you’re already at zero. Quantitative easing (QE, or money printing) is helpful, but we’ve already done that the past 10 years and how did that work out for the general economy?

Because of this, I think that in the next recession, we’re going to see a lot of creative new methods coming out of central banks.

And don’t just take it from me, because a lot of really smart people share this view as well.

Ray Dalio in particular, calls this Monetary Policy 3 (Monetary Policy 1 being interest rate cuts, and Monetary Policy 2 being QE). I’ve extracted his take on this below

We think that interest rate cuts and QE will be significantly less effective in the next downturn for reasons we’ve described in depth elsewhere. We also don’t believe that monetary policy is producing adequate trickle-down. QE and interest rate cuts help the top earners more than the bottom (because they help drive up asset prices, helping those who already own a lot of assets). And those levers don’t target the money to the things that would be good investments like education, infrastructure, and R&D.

…

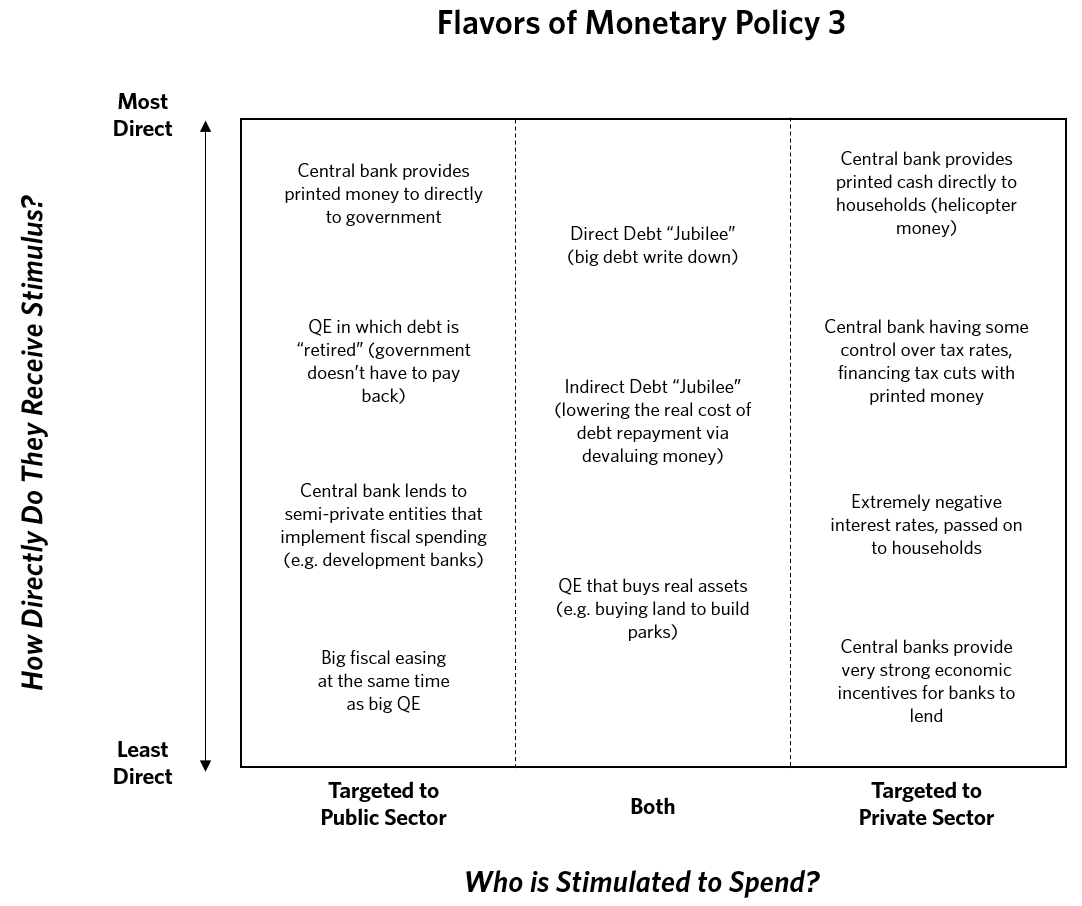

Though most of us haven’t seen it in our lifetimes, it has existed in other lifetimes and other places. MP3 is a continuum of coordinated monetary and fiscal policies that vary who gets the money (private sector versus public sector) and how directly that printed money is provided (directly providing “helicopter money” to spenders versus more indirect means of financing spending). The following diagram maps many of the possible types of MP3 onto that continuum. In general, the more direct policies would be more effective, but also more politically difficult to do. And some of the least direct policies (or variants of them) have recently been used, but not at the scale that would likely be needed in the next significant downturn.

What MP3 Looks Like

So in other words, MP3 basically envisages a situation where interest rates are permanently set to zero, the government incurs huge fiscal spending, and there is widespread helicopter money (think of the SG50 bonus, on a bigger and global scale). Crazier stuff would include things like debt writeoffs – imagine if the US government decided to wipe out half of all student debt, so that students can spend more to save the economy.

It may sound crazy right now, but just look at the kind of talk coming out of the central banks these days. In the next recession, I think they’re going to have no choice but to resort to such options to bail out the economy, much like what was done back in the 1930s.

All very interesting Financial Horse, but what does this mean for REITs?

Imagine a situation where interest rates are zero, and the government floods consumers with extra dollars that need to be spent. What would you want to own in such a situation?

I would want to own gold, and I would want to own real assets, like real estate.

The common trait that both gold and real estate has, is that the supply is finite. No matter how much new cash is created by governments, you cannot create more gold, and you cannot create more land.

Of course, not all land is equal, because you still want real estate that is well located in a major global city, and you want it financed properly so it doesn’t get seized.

And that’s exactly what Singapore REITs do. They’re basically levered plays on income generating real estate, that is located in prime locations in global financial centres.

And if interest rates are going to zero in the next recession, that levered play on real estate starts looking very smart very quickly.

Long story short, I actually get a lot of the reasons why people are buying REITs so heavily, and I think there’s a strong argument to be made for why they will continue to be attractive, at least for the next few years.

A lot of this could be the smart money frontrunning the macro developments, because if we’re going to return to a regime where SSB pays 1% interest rates, a 4.5% yielding MCT suddenly looks a lot more attractive.

Should you still buy Singapore REITs now?

So back to the original reader question. Should you buy REITs now?

I think it depends a lot on your timeframe. If you’re going to buy a blue chip Singapore REIT and hold it for 10 years, I think you’re still going to achieve decent returns.

But if you’re buying it to hold for a 2 to 3 year time period, that could be a lot more volatile, because the next few years will depend a lot on how central banks and governments around the world react.

What about me personally?

Currently about 40% of my investment portfolio consists of Singapore REITs. That’s a large proportion, so I don’t see any pressing need to add to it at the current time.

But do I sell them? Probably not as well, because my investment horizon is 10 to 20 years, and I think in the next recession, blue chip REITs may actually do quite well relative to the other asset classes.

Would I buy more REITs now? Probably not too, unless I find a really compelling REIT I like (like Eagle Hospitality at a 10% yield). The way the markets are trading, I actually like dividend stocks a lot more than REITs. With a choice between DBS at 5% yield and MCT at 4.5% yield, DBS looks a lot more attractive, given that they’re only at a 50% payout ratio (compared to the MCT’s 100%). Sectors that I like include the bank stocks, real estate developers, and telcos (you can check out the FH Stock Watch if you’re keen).

What about you guys? Are you buying or selling Singapore REITs at this time? Share your thoughts in the comments section below! I respond personally to all comments!

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

Thanks for this. Was on my mind as well 🙂 some random thoughts:

1.The Fed Put makes REITs someone of a portfolio diversifier with bond like characteristics.

2.Rentals are affected in a downturn, but some types of reits are less cyclical than others. Malls and healthcare are relatively less cyclical than office, industrials/logistics, and hospitality.

3.Unconventional monetary policy will be a huge boost, but things will have to get really bad for central Bankers to even begin considering this. Hence, if we get a rate cut and recession still, reit prices would take a hit. So maybe worse before better in that scenario.

Thanks for sharing your thoughts! There’s not going to be any right or wrong answer here, but I’ll just share some of my quick thoughts as well:

1 and 2. Like you mentioned, the type of REITs and the structuring actually matter a lot. If it’s something like ParkwayLife REIT, you’re right it could actually function a lot like a bond, without the cyclical tendencies of other asset classes. But I think how bad rentals get for something like Malls or Offices depends on how severe the next downturn is going to be for corporates, and that’s a tough one to predict in advance.

3. Again it’s hard to say for certain, but the way things are, all you need is a mild recession and both the EU and Japan are in deep trouble, because they can no longer slash interest rates any further. Even for the US they typically need to cut interest rates about 5% to restart the business cycle, and they’re only at 2.5% now. So in the next recession, I think unconventional monetary policy could potentially come into play quite early on, simply because there are no other tools.

Good sharing though. I don’t have any easy answers on my end. Time will tell how this will play out. 🙂

5%? Seems so unreal to me! I have only known lower for longer in my entire working life… 1% is massive to me 😛

Haha I meant that central banks need to slash rates by 5% for the market to recover. So with US rates at 2.5%, it needs to go to -2.5%, which means there’s about 2.5% of unorthordox monetary policy in the pipeline. 😉

Hello! Great article!

Just a newbie question: How is the yield spread related to whether a REIT is overvalued or not? If the yield spread is e.g. 0%, does this mean the REIT is over or under valued?

Thanks, have been an avid reader of your posts for quite some time.

Hi, and welcome to Financial Horse! 🙂

The yield spread basically reflects the risk you are taking on for the investment. So if the yield spread is zero, you might as well just buy SSBs because it is completely risk free.

The 10 year average yield spread for SREITs is 3.8%, so anything above would indicate its undervalued, and anything below would be overvalued (very simplisitically of course). As you learn more about REITs, you’ll find that yield spread is just one tool in many when evaluating REITs.

Hope this is helpful! Feel free to reach out if you have any queries. 🙂

[…] previously shared my thoughts in an earlier article but given that it’s been some time since, it’s probably warranted to do an […]