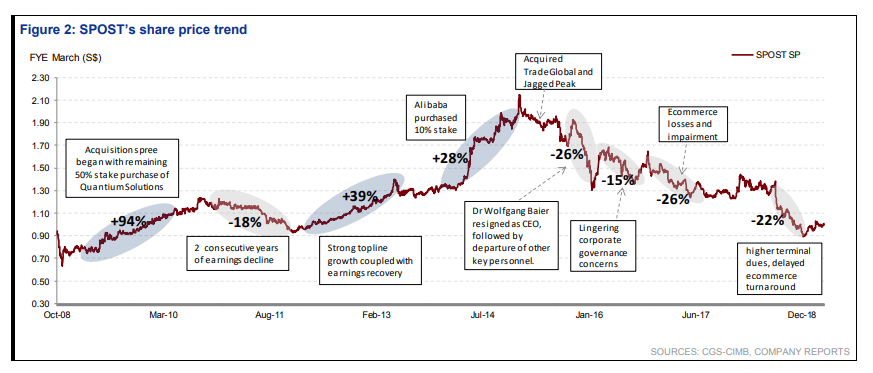

I’ve always been very interested in SingPost. As the only national mail operator in Singapore, coupled with the explosion in eCommerce volumes, and major shareholders being Alibaba and Singtel, you would have thought that SingPost would be the next big thing.

Nothing could be further from the truth. The 10 year share price is set out below, and it’s been a disaster since 2015. What happened though? Could this change in the future?

Basics: SingPost, our national Postman

SingPost organises themselves into four key business segments:

From 1 April 2018, SingPost Group has reclassified the reporting of certain business units into four key business segments, namely Post and Parcel, Logistics, eCommerce and Property (FY2017/18: Postal, Logistics, eCommerce and Property).

♦ Post and Parcel segment comprises the core Postal and Singapore Parcel delivery business of the Group. This includes Domestic mail, International mail, vPost, products and services transacted at the Post Offices, as well as Parcel deliveries in Singapore.

♦ Logistics segment comprises the Logistics businesses of the Group. This includes Quantium Solutions, Couriers Please and Famous Holdings. The comparative period last year had included the Singapore Parcel delivery business SP Parcels, s elf- storage business General Storage Company (“GSC”) and other logistics businesses, which have accordingly been adjusted to Post and Parcel (for SP Parcels) and Property (for GSC).

♦ eCommerce segment comprises the front-end related eCommerce businesses. This includes SP eCommerce in Asia Pacific, as well as our US eCommerce businesses, TradeGlobal and Jagged Peak.

♦ Property segment includes the provision of commercial property rental, as well as the self-storage business of GSC.

To summarise:

- Post and Parcel is the traditional delivery of letters, mail and parcels that we are familiar with. Ecommerce parcels will come under this segment. This is primarily a Singapore based business.

- Logistics is the regional delivery of shipments, so things like freight shipping, shipping of large boxes etc. This is an Asia based business, competing in markets that include Australia, New Zealand and Hong Kong.

- eCommerce is a more recent business SingPost acquired in the US. This segment provides end to end eCommerce services (from order tracking to order fulfilment) in the US. SingPost recently announced that they are going to sell this business segment.

- Property comprises the rental from their mall, SingPost Centre, and the self storage business (General Storage Company) that they run.

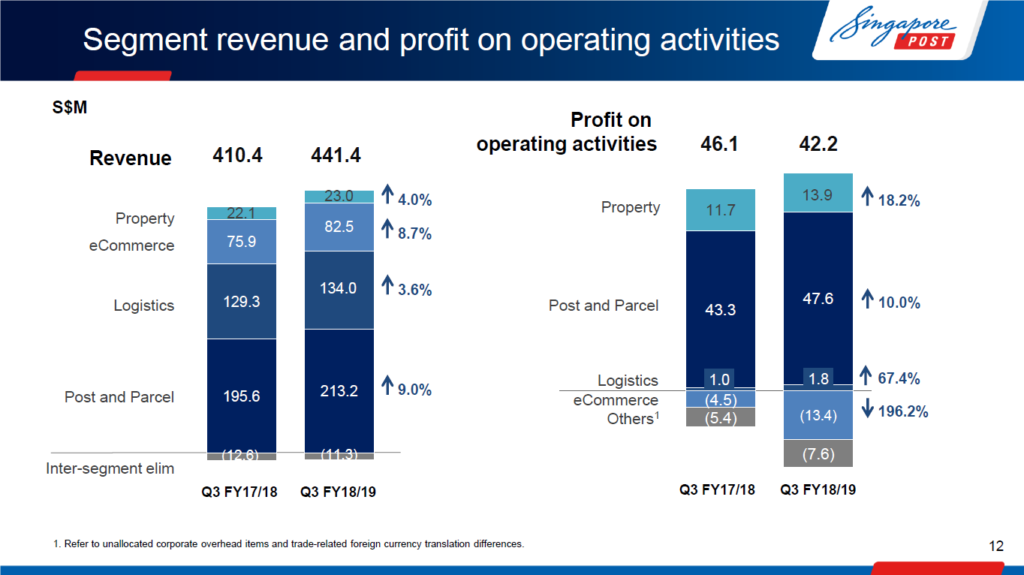

The revenue and profit splits are set out below, and the results are astounding. Post and Parcel is the only segment that turns a good profit (apart from Property). Logistics and eCommerce contribute good revenues, but don’t contribute to profits.

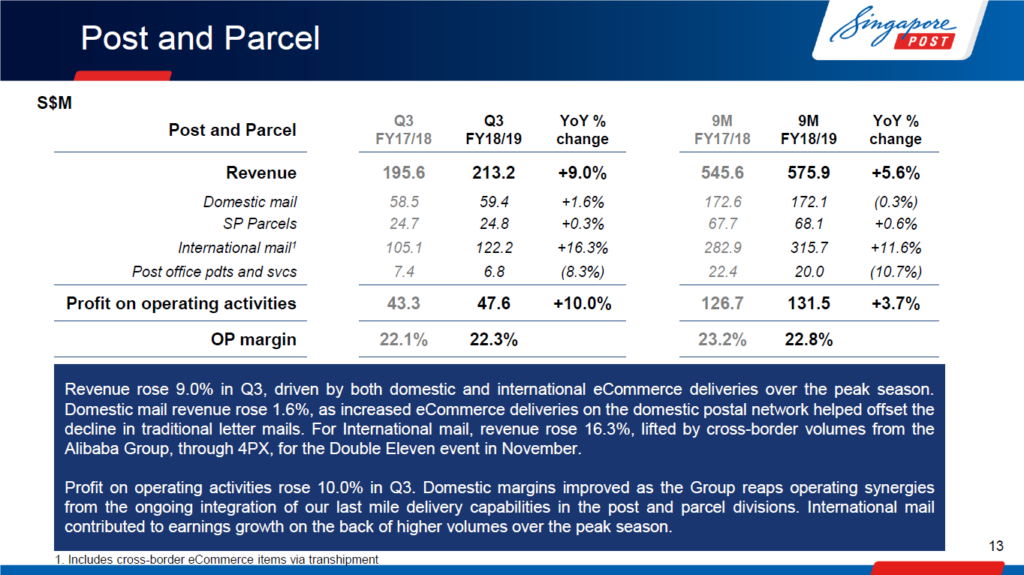

Post and Parcel

Post and Parcel is by far the brightest spot in the company. Year on year revenue and profit numbers are great (5.6% and 3.7% respectively), and the profit margin is a very nice 22.8%.

Personally I expect eCommerce volumes to explode in the next 5 years. eCommerce spending increased 22% year on year in 2019, and is projected to grow at about 15% annually over the next 5 years.

Leaving the numbers aside, the experience for me has been transformational. There was a time when I absolutely had to go to a shop to pick up a new gadget that I wanted, because I didn’t trust internet purchases. Those days are long gone. These days when I want a new Xiaomi phone, I’m going to the shop only to take a look at the phone, and then I’m gone to Lazada, Shopee, Qoo10 etc to check prices and get the cheapest one. And I just don’t see that changing. And as I talk to my friends and relatives, I hear similar stories.

Sure, there are competitors like Ninja Van who are sharing a slice of the pie, but I think it’s going to be a case of a rising tide lifting all boats here. The pie is going to grow so much in the coming years that almost all players in this space will benefit.

One potential problem though, is the poor delivery service standards. It was so poor that SingPost was fined S$100,000 and the CEO had to came out to apologise. The way I see it, SingPost may have taken their eye off this core business in the past few years, and tried to squeeze profits as they focussed on the newer eCommerce and Logistics plays. In some ways it’s similar to what happened with SMRT, where underinvestment resulted in deteriorating service standards. Going forward though, SingPost will need to invest heavily in capital expenditure (new equipment for delivery services), more postmen, and higher postmen pay. This is going to increase costs, and there will be short term pressure on margins.

In the longer term though, I see this as a huge positive. Ecommerce volumes is going to explode whether we like it or not. If SingPost can bring up their service standards to the level of Ninjavan or the other global players, there’s huge room to grab market share here.

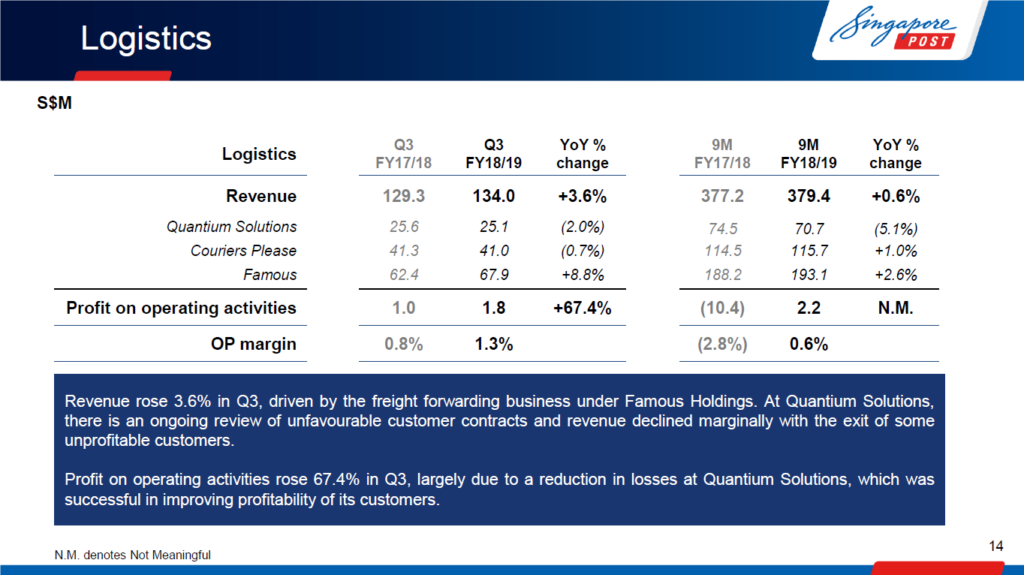

Logistics

I wouldn’t say that Logistics is a disaster, but I would say that it’s one for the future. Revenue growth is in the low single digits, but the profit is non-existent.

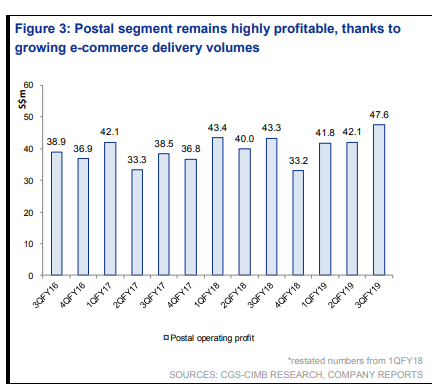

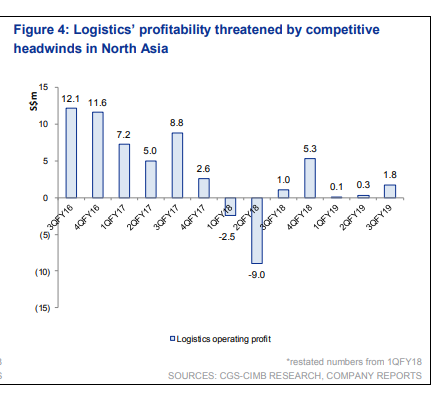

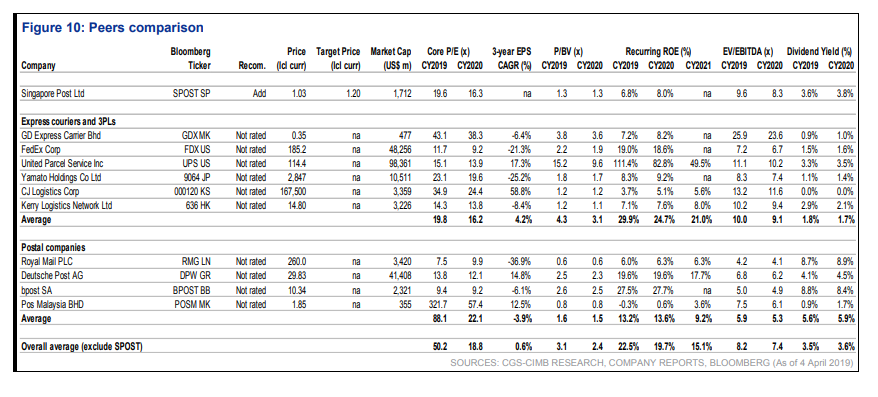

CIMB has a nice chart below that shows how poor the quality of earnings is.

According to SingPost, this is due to heavy competition, and rising costs associated with the transhipment business (eg. higher terminal dues).

I’m not an expert on the logistics industry, but the way I see it, logistics is highly competitive these days. Lots of really big players from Alibaba to Amazon are trying to build up logistics capabilities that will be able to handle their eCommerce volumes in the years to come.

The Post and Parcel business is relatively shielded from international competition because not many players want to come into Singapore and set up extensive delivery operations. The market is so small that it makes more sense to just leverage on existing players to save cost, provided that service standards are acceptable.

In logistics however, because SingPost is running operations in North Asia and Australia, they’re going to be up against the really big boys. And that’s gonna be a tough fight.

You can argue that Alibaba has a large stake in SingPost (14.5%, SingTel holds another 21.8%) so it’s in their interests to help SingPost succeed, but don’t forget that Alibaba also has stakes in 4 of 6 of the large logistics companies in China.

The way I see it, Alibaba spreads its eggs around, building large stakes in many existing logistics players, such that regardless of who succeeds, Alibaba wins.

I think competition in this space is going to heat up further in the coming years, and Alibaba may or may not be willing to inject huge amounts of money to save this business segment.

At best, the outlook here is murky.

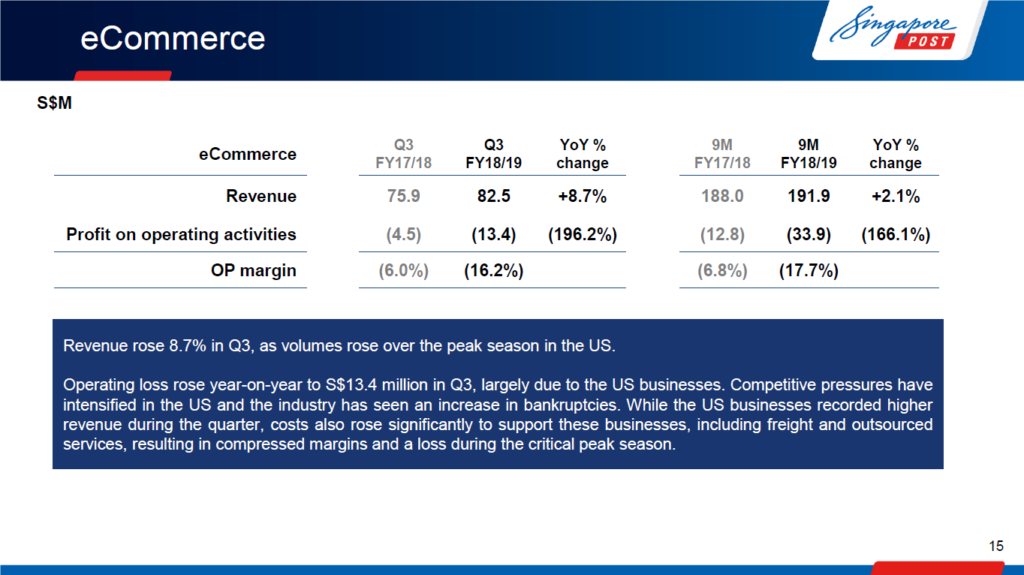

eCommerce

It you wanted to understand the meaning of a disaster, you can take a look at the eCommerce segment. It’s so bad that I’m not even going to go through the numbers, apart from pointing out a 166% increase in losses from 12.8 million to 33.9 million for the first 9 months of FY18/19.

I would launch into a long discussion about why SingPost going into the most competitive eCommerce market around the globe, a market where if your name is not Amazon or Walmart you’re in deep trouble, was an absolute disaster right from the start, and you probably don’t need an MBA from Harvard to understand why, but I feel that’s just flogging the dead horse.

Because SingPost has already announced that they would be selling this entire business segment following a “strategic review”. Gee, I wonder what they saw.

The problem though, is that they seem to have announced a sale of the business, before they even found a buyer for it. In fact, DBS research is of the opinion that SingPost is in the early stages of soliciting buyers.

Now I’m no expert here, but if a business is bleeding cash, and if everybody knows that you have to sell it because it’s bleeding cash and is in an incredibly competitive industry that you’re trying to exit, wouldn’t that make it a lot harder to get a good price for the sale? I see absolutely no reason why SingPost had to announce this sale before they secured a buyer, apart from wanting to boost their share price. And when management does things only to boost share price, that never works out well long term, at least in my view. While I love the fact that they are selling off this horrible loss making business, I would have preferred them to tell us only after they found a buyer and signed the Sale and Purchase agreement, not before. Given how it’s played out, I’m going to be incredibly wary of the price that SingPost will be able to get for this business.

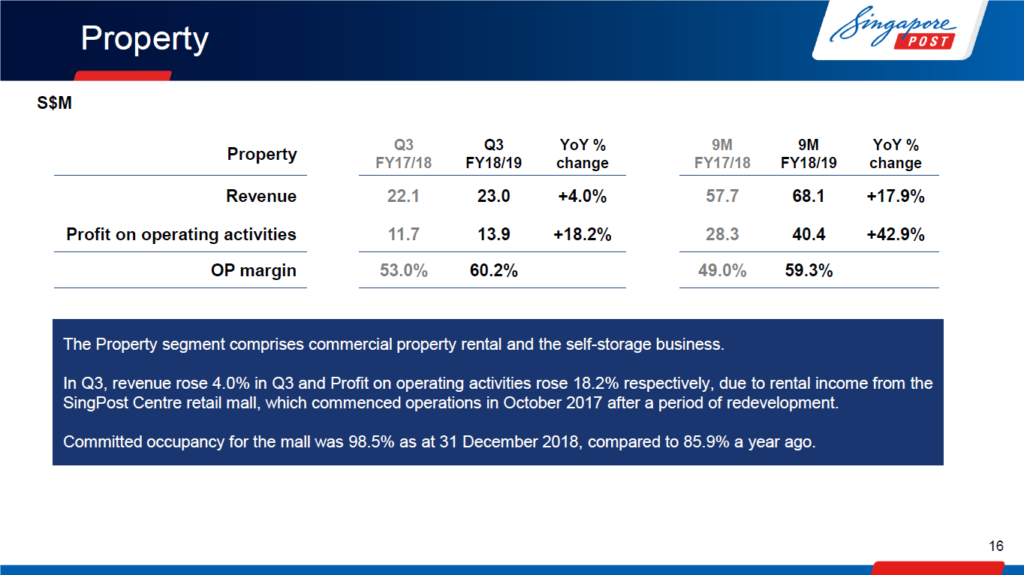

Property

The year on year growth numbers are big because SingPost Centre opened in October 2017, so the FY2017 numbers don’t have the full contribution from the mall.

Going forward though, SingPost’s own outlook is for revenue and profit to stay stable, something I agree with. With committed occupancy for the mall at 98.5% now, there’s not much upside left, but because of its good location and because it’s managed by CapitaLand, I think the downside is limited as well.

When you think about it, it’s pretty amusing that almost every company from SPH to SMRT to SingPost seems to get a decent chunk of earnings from property rental these days.

Dividend

SingPost’s dividend policy had been changed from an absolute amount to one based on a payout ratio ranging from 60% to 80% of underlying net profit for each financial year.

Based on FY2018 numbers, that works out to a trailing dividend yield of 3.3%.

The big question though, is on spending going forward. If SingPost spends heavily to upgrade the Singapore delivery infrastructure (and I would expect them to), the increased costs would affect profits, and consequently the dividend.

Personally though, that’s something I want to see happen. As a shareholder, I would prefer the company to invest heavily in infrastructure, keep customers happy and set the company up for long term growth, than to pay out big dividends and keep shareholders happy in the short term. But it remains to be seen which route SingPost takes.

Valuations

CIMB has a great peer comparison on valuations below:

If we assume a 30% increase in profits after the sale of the eCommerce business, SingPost will trade at a 17 times forward PE. That’s still higher than the P/E ratios of the big global players like FedEx, UPS and Kerry Logistics. It’s also a lot higher the P/E of old school postal companies like Royal Mail and Deutsche Post.

Personally, I think that if we look at the global valuations, SingPost is not cheap.

Macro Outlook

Actually the more interesting question is why the global market as a whole simply isn’t affording logistics stocks a hefty premium. I suspect it’s a two pronged issue: (1) poor global macro outlook, and (2) increased competition from ecommerce players.

On the macro outlook, players like FedEx have come out and reported horrible Q4 2018 and Q1 2019 results, that really dampened global risk appetite for logistic plays. Of course, they’re now saying that they see some small pickup in Q2 2019, so that could improve going forward.

On eCommerce, you either get the Amazon and JD.com approach where they build entire logistics networks inhouse, or you have the Alibaba approach where they take large stakes in other logistics players. Either approach sets the space up for huge competition going forward, which creates uncertainty, and investors don’t like uncertainty.

Afternote:

A reader left a really amazing comment that I felt really added to this discussion. Have extracted it in full below:

Logistics is scalable and growth is through volume but must not offer too much discounts or rebates (cheap pricing). That may be possible if one has control of the end-to-end entire chain, from warehousing to delivery – being cost effective. Singpost has built that capabilities, even the chance to possibly test drive omnichannel model through their property asset (singpost managed retail mall).

Now, the question is to monetize this logistics network. To do this, they need partnership, for instance last mile providers to be part of it. They already did that as well, for example park n parcel also worked with Singpost.

In other words, at this stage, they are building an ecosystem. You, as the ecosystem, call the shots because others may have to depend on your internal resource-based capabilities to stay competitive (e.g. tracking software from warehousing, packing etc…). Partners can have shared margin with Singpost and possible cross-sell opportunities, thereby bringing them deeper into the system. That is cruicial to gain great economies of scale.

Singpost also has the abilities to manage huge volume (their regional distribution ctr manages bulk of Lazada delivery)

If I recall correctly, they are also selling the EDGE software subscription which can bring in more individual players into the ecosystem. It can be a recurring revenue stream for SingPost.

Its in line with their Leap23 transformation strategy – increase global ecommerce flow and to monetize existing internal expertise as mentioned above. Singpost also hired a transformation leader, setting up this unit to spearhead new initiatives as part of this plan. It has already taken shape.

However, the key problem I see here is the senior leadership commitment – communicating this strategy and motivating their next level of management and mid-level Managers to consistently deliver, being empowered to do this and passionate to make an impact. Meaning, culture of the firm. That to me is 50-50 for now, primarily of the fine slapped recently where postmen were disgruntled. Its not a new issue after all yet shows signs of poor culture where folks just run off and others worried of taking the blame.

In short, Singpost has the end-to-end infrastructure network. Its not always you see a regional logistics firm has such capabilities.

If Singpost executes their leap23 transformation strategy well, if they continue be the leader from their ecosystem in the local market and some other nearby markets – then this company will fly.

Its a blessing they announce that both US e-commerce units are put up for sale. Better to bite the bullet first. Then, re-organize internally to concentrate their core business agenda. Lets see how the management perform post sale. I believe AGM this year will give a good peek into their leadership style – yes, its the management that I am most concerned about.

Closing Thoughts: Will I buy SingPost?

SingPost is a really interesting one for me. I think the growth in eCommerce is going to be so strong in the next 5 years that SingPost will benefit greatly. And the more they spend to improve service standards, the more customers will come to trust their service reliability and use their service, so this whole issue about lousy postmen may be a blessing in disguise.

The Ecommerce business will be sold so that removes a huge loss generator, but I’m not optimistic on the price they can get on the sale.

The Logistics business though, is a big question mark. It if pays off, it pays off big. If it doesn’t, it could well turn into another Ecommerce disaster. And looking at management’s track record in building new business segments, I’m going to take a “I will believe it when I see it” approach here. In business, execution in everything, and I’m not entirely convinced on management’s ability to execute in this highly competitive space.

I’m going to stay on the sidelines for this one, but keeping a close eyes on earnings. If Logistics starts turning a good profit and they grow meaningful market share, this could be a really interesting stock. Sure, the stock price would have gone up 20 to 30% by then, but it’s still better being late to the party, than to be early and find out the party is cancelled.

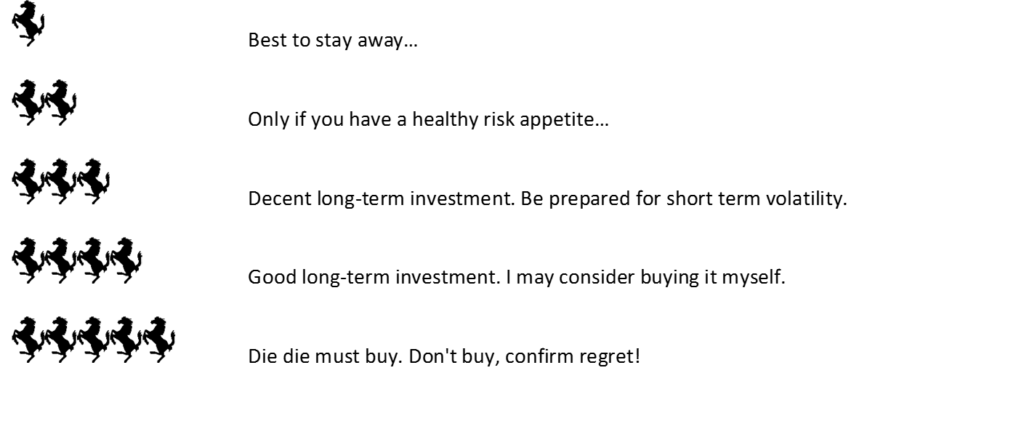

That said, if you are really bullish on the Post and Parcel and Logistics business, I think this could be a pretty decent investment. I’m giving this a 2.5 Financial Horse rating.

SingPost – Financial Horse Rating

![]()

Rating Scale

Till next time, Financial Horse, signing out!

Enjoyed this article? Do consider supporting us and receiving additional exclusive content. Big shoutout to all Patrons for their generous support, and in helping keep this site going!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!