So I was doing some research on the highest yielding blue chip dividend stocks on the SGX recently.

And with the help of AI, I managed to compile a list of the Top 20 highest-yield SGX blue-chip stocks per below.

So I wanted to take some time to go through the list, and discuss which of these dividend stocks I would consider buying for my own portfolio today.

Highest-yield SGX blue-chips — ranked (close 18 Jun 2025)

Here’s the full list (in picture form):

And in text form:

| # | Company / SGX code | What it does | Latest indicated yield¹ |

| 1 | Frasers Logistics & Commercial Trust (BUOU) | Industrial & office REIT | 7.6 % |

| 2 | CapitaLand Integrated Commercial Trust (C38U) | Retail & office REIT | 7.5 % |

| 3 | Mapletree Logistics Trust (M44U) | Pan-Asian logistics REIT | 7.0 % |

| 4 | Mapletree Industrial Trust (ME8U) | Data-centre & industrial REIT | 6.9 % |

| 5 | Mapletree Pan Asia Commercial Trust (N2IU) | Retail & office REIT (SG, HK, CN, JP, KR) | 6.8 % |

| 6 | DBS Group (D05) | Bank | **6.8 %**² |

| 7 | Venture Corp (V03) | Electronics manufacturing & design | 6.6 % |

| 8 | Frasers Centrepoint Trust (J69U) | Suburban-mall REIT | 6.3 % |

| 9 | Jardine Cycle & Carriage (C07) | SE-Asian autos & agribusiness | 6.0 % |

| 10 | CapitaLand Ascendas REIT (A17U) | Business-park & hi-tech REIT | 5.9 % |

| 11 | Singapore Airlines (C6L) | Flag-carrier airline | **5.8 %**³ |

| 12 | Genting Singapore (G13) | Resorts World Sentosa | 5.6 % |

| 13 | Hongkong Land (H78) | Premium commercial property | 5.5 % |

| 14 | United Overseas Bank (U11) | Bank | **5.3 %**⁴ |

| 15 | Wilmar International (F34) | Agri-commodities & brands | 5.2 % |

| 16 | OCBC Bank (O39) | Bank | 5.1 % |

| 17 | Thai Beverage (Y92) | Beer & spirits | 5.1 % |

| 18 | Jardine Matheson (J36) | Conglomerate (property, retail, auto) | 5.1 % |

| 19 | Keppel Ltd (BN4) | Infrastructure & asset management | 4.6 % |

| 20 | Singtel (Z74) | Telecoms & data-centres | 4.3 % |

¹ Forward yield unless the issuer has yet to declare a FY-2025 dividend, in which case trailing (TTM) yield is shown.

² Assumes DBS continues the S$0.60 regular + S$0.15 capital-return dividend each quarter through FY-2025.

³ Based on S$0.40 total FY-2025 dividend and S$6.85 spot price.

⁴ UOB’s figure reflects the first 25 ¢ tranche of its 50 ¢ 90th-anniversary special still to be paid in 2H-2025.

Here’s some additional colour from ChatGPT o3 after it helped me crunch the numbers to generate the list:

What the numbers really mean

- Source & basis. Yields are the forward or latest-declared payout divided by the 18 Jun 2025 closing price, pulled from SGX/Yahoo Finance data. I round to one decimal place for clarity.

- One-offs distort bank yields. DBS’s figure includes its new 15 ¢/qtr capital-return dividend; OCBC’s and UOB’s include announced specials tied to excess CET-1. Strip these out and the “core” yields drop 40-80 bp.

- SIA’s 5.8 % is inflated by a 30 ¢ special following the Air India/Vistara merger gain; management hasn’t promised this will repeat.

- Property trusts dominate. Seven of the top ten names are REITs, reflecting the sector’s policy of paying out 90–100 % of distributable cash.

- Yields move daily. A 3 % share-price swing can knock a stock two or three rungs down this list. Always cross-check the ex-date and whether the dividend is recurring before committing capital.

No sugar-coating

- High yield ≠ safe income. REITs are carrying 30–45 % gearing at a time when refinancing still costs 4 %+; any slip in asset values or rental growth bites distributions fast.

- Banks are hostage to rates. If the Fed lops off 100 bp by early-2026, NIM-compression will hit payout ratios unless management chooses to over-distribute.

- Cyclical names (Venture, Jardine C&C, Wilmar) can and do slash dividends in downturns; don’t chase the headline number without stress-testing earnings.

Top 10 highest yield dividend stocks on SGX – Which would I buy? 5% dividend yield minimum?

The way I see it, you can split this list into 3 types:

- REITs

- Singapore Bank Stocks

- Non-real estate, non-bank dividend stocks

Let’s discuss each.

REITs – value given the recent drop in interest rates?

You can see below how of the Top 10 list – 7 out of 10 are REITs.

Yes I know that the numbers for CapitaLand Integrated Commercial Trust are slightly inflated because this is trailing twelve-month numbers (actual yield is closer to 5.5%ish), but let’s stay big picture here.

| # | Company / SGX code | Latest indicated yield¹ |

| 1 | Frasers Logistics & Commercial Trust (BUOU) | 7.6 % |

| 2 | CapitaLand Integrated Commercial Trust (C38U) | 7.5 % |

| 3 | Mapletree Logistics Trust (M44U) | 7.0 % |

| 4 | Mapletree Industrial Trust (ME8U) | 6.9 % |

| 5 | Mapletree Pan Asia Commercial Trust (N2IU) | 6.8 % |

| 6 | DBS Group (D05) | **6.8 %**² |

| 7 | Venture Corp (V03) | 6.6 % |

| 8 | Frasers Centrepoint Trust (J69U) | 6.3 % |

| 9 | Jardine Cycle & Carriage (C07) | 6.0 % |

| 10 | CapitaLand Ascendas REIT (A17U) | 5.9 % |

REITs as the highest dividend paying blue chip stocks? How safe are REITs in this macro climate?

Typically speaking – the price of REITs is inversely correlated with long term interest rates.

If long term interest rates go down, REIT prices should go up.

Now the funny thing is that Singapore 10 year interest rates have plunged from 3.5% a year ago.

To 2.28% today:

By that logic, REITs should be flying.

And yet they are not.

You can see REIT prices plotted against the Singapore 10 year yield (inverted) below.

If the relationship held, REIT prices should be significantly higher.

So what gives?

What is the risk with REITs?

I suppose one way to rationalise it is that the market expects long term interest rates to pick up eventually – driven by Trump’s large budget deficit and inflationary policies.

For example let’s say Trump replaces Jerome Powell with a dovish Fed chair in 2026 – who cuts short term interest rates, bringing inflation up, and sending long term interest rates higher.

That’s not good for REITs.

And perhaps the market is pricing this in, capping the upside for REITs.

What is the flipside?

But the other way to see it, is that yes perhaps that may happen down the road.

But for every day that the Singapore 10 year yield stays at 2.28% – REITs look like a relatively good bargain.

I mean if CICT offered 5.5% yield when 10 year yields are at 3.5%, that’s a 2.0% yield spread vs the risk free.

If 10 year yields are at 2.28% today and CICT still offers a 5.5% yield, that’s a 3.22% yield spread.

Then hey by that logic – REITs are a much better buy today.

And even in the scenario above – a sharp rise in the long end is going to trigger a broad market sell-off, so it is in the interests of the Trump administration to ensure that does not happen for an extended period of time.

So personally I find decent value in REITs today.

I would stick primarily though, with REITs with Singapore high quality real estate, with a strong balance sheet, and good sponsor.

You can see the REITs I am keen on on FH Premium, with my rough price targets.

Singapore Bank Stocks – Attractive dividend, but what about the path forward?

And then of course.

No list of blue-chip dividend stocks is complete without the 3 local bank stocks.

You can see their relative standing below compared to the other dividend stocks.

| # | Company / SGX code | Latest indicated yield¹ |

| 1 | Frasers Logistics & Commercial Trust (BUOU) | 7.6 % |

| 2 | CapitaLand Integrated Commercial Trust (C38U) | 7.5 % |

| 3 | Mapletree Logistics Trust (M44U) | 7.0 % |

| 4 | Mapletree Industrial Trust (ME8U) | 6.9 % |

| 5 | Mapletree Pan Asia Commercial Trust (N2IU) | 6.8 % |

| 6 | DBS Group (D05) | **6.8 %**² |

| 7 | Venture Corp (V03) | 6.6 % |

| 8 | Frasers Centrepoint Trust (J69U) | 6.3 % |

| 9 | Jardine Cycle & Carriage (C07) | 6.0 % |

| 10 | CapitaLand Ascendas REIT (A17U) | 5.9 % |

| 11 | Singapore Airlines (C6L) | **5.8 %**³ |

| 12 | Genting Singapore (G13) | 5.6 % |

| 13 | Hongkong Land (H78) | 5.5 % |

| 14 | United Overseas Bank (U11) | **5.3 %**⁴ |

| 15 | Wilmar International (F34) | 5.2 % |

| 16 | OCBC Bank (O39) | 5.1 % |

| 17 | Thai Beverage (Y92) | 5.1 % |

| 18 | Jardine Matheson (J36) | 5.1 % |

| 19 | Keppel Ltd (BN4) | 4.6 % |

| 20 | Singtel (Z74) | 4.3 % |

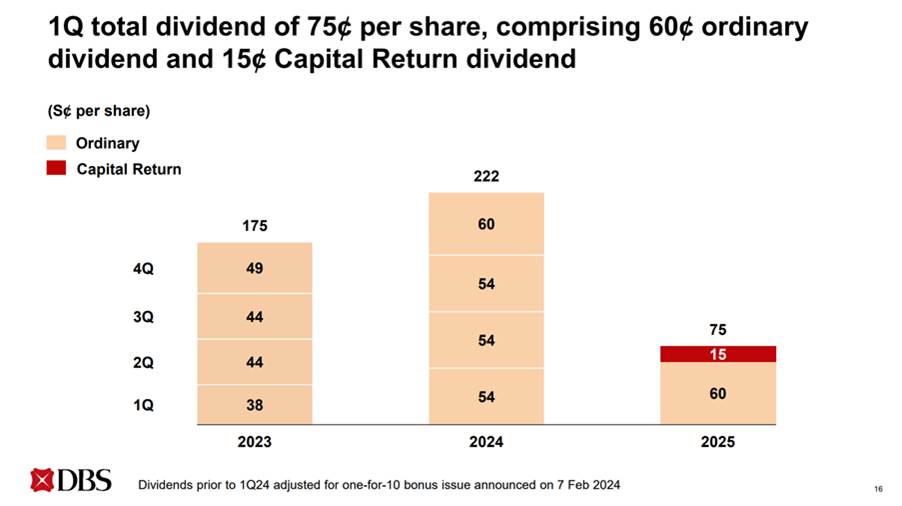

Why is DBS’s dividend yield so much higher than OCBC and UOB Bank?

Now the reason why DBS stands heads and shoulders above OCBC and UOB Bank.

Is largely because their dividend includes a $0.15 “capital return” dividend.

I crunched the numbers in my recent article on DBS:

Using the full S$0.75 per-share distribution, DBS’s latest dividend payout ratio is about 74 % of 1Q 2025 earnings.

On the traditional measure that considers only the ordinary 60-cent dividend, the ratio is roughly 59 %.

In plain English, the additional $0.15 dividend pushes DBS’s dividend payout ratio to quite high levels.

It is sustainable if profits stay high, but if profits come down there is a risk it may get cut.

And OCBC or UOB don’t have a similar “capital return” dividend, hence their dividend yield is much lower.

Interest rates poised to drop? Will this affect bank stocks?

The risk for bank stocks of course, is that if (a) interest rates come down, or (b) economic growth slows, then we may see bank profitability come down.

But there’s a lot of nuance to (a) – because if short term interest rates come down, and long term interest rates go up, that’s a steeper yield curve which could actually be good for bank profitability (since banks borrow short and lend long).

So this is not so straightforward to call as well.

And you can see from the chart below that the share price for the banks has generally stayed flat in most of 2025 (barring the sell-off following the liberation day tariffs).

Personal view – I have exposure to Singapore bank stocks.

But at current prices, I don’t really see a need to go out there and buy a lot more bank stocks today.

But I will hold my positions for now.

Follow Financial Horse to avoid missing any post!

Non-real estate, non-bank dividend stocks – stock picking required, no two are the same

Which brings us to the most interesting section.

Non-real estate, non-bank dividend stocks.

The names are bolded below, and you can see they generally pay about 5%ish dividend yield:

| # | Company / SGX code | Latest indicated yield¹ |

| 1 | Frasers Logistics & Commercial Trust (BUOU) | 7.6 % |

| 2 | CapitaLand Integrated Commercial Trust (C38U) | 7.5 % |

| 3 | Mapletree Logistics Trust (M44U) | 7.0 % |

| 4 | Mapletree Industrial Trust (ME8U) | 6.9 % |

| 5 | Mapletree Pan Asia Commercial Trust (N2IU) | 6.8 % |

| 6 | DBS Group (D05) | **6.8 %**² |

| 7 | Venture Corp (V03) | 6.6 % |

| 8 | Frasers Centrepoint Trust (J69U) | 6.3 % |

| 9 | Jardine Cycle & Carriage (C07) | 6.0 % |

| 10 | CapitaLand Ascendas REIT (A17U) | 5.9 % |

| 11 | Singapore Airlines (C6L) | **5.8 %**³ |

| 12 | Genting Singapore (G13) | 5.6 % |

| 13 | Hongkong Land (H78) | 5.5 % |

| 14 | United Overseas Bank (U11) | **5.3 %**⁴ |

| 15 | Wilmar International (F34) | 5.2 % |

| 16 | OCBC Bank (O39) | 5.1 % |

| 17 | Thai Beverage (Y92) | 5.1 % |

| 18 | Jardine Matheson (J36) | 5.1 % |

| 19 | Keppel Ltd (BN4) | 4.6 % |

| 20 | Singtel (Z74) | 4.3 % |

What does Venture Corp do?

Venture Corp really stood out for me as being heads and shoulders above the other dividend stocks in terms of yield.

A bit more on Venture Corp.

It is an:

End-to-end design-to-manufacturing partner (“ODM/EMS on steroids”) – it co-designs, prototypes, builds and ships complex electronic / electromechanical products for > 100 global customers.

And a high level overview of the stock from ChatGPT o3:

| Metric | FY-2020 | FY-2021 | FY-2022 | FY-2023 | FY-2024 | Comment |

| DPS (S$) | 1.25 | 0.75 | 0.75 | 0.75 | 0.75 | Flat since 2021 after one-off pandemic special in 2020. |

| EPS (S$) | 1.46 | 0.94 | 0.93 | 0.93 | 0.84 | Earnings slipping as customers digest inventory. |

| Payout ratio | 86 % | 80 % | 81 % | 81 % | ≈ 89 % | AGM minutes confirm 89 %. |

| Cash / debt | Net cash, zero borrowings every year since 2014 | Dividend is backed by cash, not leverage. | ||||

| Current yield | ≈ 6.6 % at S$0.75 DPS and S$11.39 closing price on 18 Jun 2025. |

Strengths

- Cash-rich, debt-free balance sheet – gives management room to defend the dividend even in a soft year.

- 25-year record of paying (and rarely cutting) dividends; management publicly states intent to keep DPS “on par or higher”.

- Share-buy-back programme (10 m shares authorised, acceleration approved) adds a second capital-return lever.

Watch-outs

- High payout ratio already close to the ceiling; any further profit slump pushes the dividend above 100 % of earnings.

- Revenue contraction – FY-2024 sales -9.6 % y/y; 1Q-2025 still down. If key customers delay new programmes, earnings will shrink faster than costs can be cut.

- Customer concentration – top five accounts are believed to contribute >50 % of revenue (company does not name them). A lost programme could punch a hole in cash flow.

- No growth in DPS since 2021 – great for income stability, poor for inflation-beating returns.

- EMS cyclicality – margins are healthy today, but historically Venture’s earnings have whipsawed with the tech cap-ex cycle (e.g., 2008-09, 2019 smartphone slump).

As you can see, there’s no free lunch here.

The dividend yield is high yes, but payout ratio at 89% is as high as it gets – suggesting that the dividend yield may not be sustainable if there is a drop in profits.

And also the drop in topline revenue is worrying, not to mention the lack of growth in dividends since 2021.

So the yield is high for a reason here – the market is efficient like that.

Pros and Cons of Non-real estate, non-bank dividend stocks

The benefit I would say with this category of dividend stocks – is diversification.

You cannot have your entire portfolio made up of real estate and bank stocks, from a diversification perspective that is tricky.

And some of the stocks on this list have done very well.

Singtel for example, which I just covered this week in the FH Premium article:

What would I do? If I were building a dividend portfolio today?

That said and done.

To be brutally honest.

If I were building a dividend portfolio today.

I would probably still build the bulk of it using real estate and banks.

And then layer on exposure to specific dividend stocks from the non-real estate and non-banks category.

And then layer on growth exposure – stuff like US stocks, US tech, Bitcoin and so on.

In any case you can see my full portfolio on FH Premium.

Whatever the case, I would love to hear what you think.

Which of these dividend stocks would you consider buying?

This post is written on 20 June 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Good one. But why no analysis for Wilmar, Thai Bev, Jardine Methason ?

Haha, article was already getting too long! I will see if I can cover those in a follow up article.

Hi FH,

Appreciate your weekly write-ups.

Question, why not buy just the STI ETF instead? Its 50% Banks & 20% Reits at least with the other 30% for ‘diversification’ at 5% ylds still i tink with ample liquidity for execution.

Appreciate your thots.

Thank you.

Yeah that’s perfectly fine for an investor who wants to passive index. No issues at all. This analysis is more for investors who want to understand more about what lies under the hood, or try their hand at stock picking.

I was thinking exactly the same thing. The SPDR STI ETF is yielding a bit more than 4% and saves all the stress of stock-picking, which we have to admit is difficult (or almost impossible to get right). Just average in every month and we’ll probably do quite OK.

Yep I think that’s perfectly fine.

Very detailed analysis..good one..please include Wilmar in your next part..

Thanks for the kind words. OK – will do.

If REITs operate on a 5-year financing cycle, then the primary interest rate impact to consider is the refinancing cost—specifically, the spread between the interest rates from five years ago and today. The 60-month moving average of the yield curve offers a useful proxy for this refinancing cost over time.

If this moving average continues to slope upward, it indicates that REITs are still rolling over debt at higher rates compared to their previous financing terms. In that case, it’s likely premature to expect earnings tailwinds from a declining interest rate environment. In my view, this dynamic contributes meaningfully to the sector’s underperformance.

Happy to hear your thoughts on this.

This analysis is broadly correct from an earnings perspective. But REITs are also priced from a yield spread perspective – the spread in yield vs the risk free rate. So if the 10 year rates drop, by that logic the yield spread has gone up which makes REITs more attractive.

The market hasn’t really priced that in for now, suggesting the market thinks that either (a) long rates will go back up, or (b) REIT yields will come down. If you disagree with that view, then REITs could be interesting.

My non-Singaporean thoughts:

1. I expect higher rates over the next 30 years. The west empoverishes – social welfare will implode. BUT(!) as Sg is debt free, she could be the one with low rates in hardest times for others. So I could be wrong to expect some contagion.

2. The US is in this moment bombing Iran. I do not have one asset in US. It is as Nassim Taleb said (I saw him yesterday on SD Bullion) – nobody trusts US anymore. I sold all after the Russian ADR theft some years ago.

3. When a third WW is more or less starting, I am not keen on real estate. When I watch a real estate soap before bedtime (say: Escape to the Country) I wonder how much people are willing to pay for a roof. Yes the builders are down and the REITS are, but reality is not. I do not know if Singapore can be an island – if she is you win! – but I expect lower real estate in rising interest rates AND less income AND dropping currencies (buying power).

-> I go with KLKK Uncle – people will eat and drink. KISS!

Cheers.

btw: FH, could you do an article about SDR? Some have very low volume, my question would be: “Kasikorn BK TH SDR1to1 (TKKD.SI)” had a volume of just 3700, is this of importance or not? Is the price (value) pegged to that in BKK? When I sell, do I sell probably to a buyer in Thailand? I am unsure about the connection. When I order, are SDR born as real stocks go into custody in Thailand? Thanks!

Got it – I will cover those other names as well. Interesting question on SDR though. I have not looked at them in detail thus far, but let me have a look.

On your 3 points, I generally agree. I too expect structurally higher rates, and I think this will be a period of higher geopolitical uncertainty. This makes it vital for investors to start thinking about some of these factors that you raised.

1. nobody knows what’s gonna happen in the next 3 years, let alone the next 30. I’m sure you read about such uncertainty in Nassim Taleb’s Black Swan.

2. wow S&P 500 gained 46% since you sold after the Russian ADR theft. that’s a lot of nobody trusting the US anymore LOL

3. what 3rd WW. think you should stop watching all the doom porn.

Hi,

Can advise the breakdown for FCT Reit 6.3% yield ?

Yield = DPU / 18Jun Px = 0.1228/2.22 = 5.5%

(12.28cts DPU was the Post-acquisition for NorthPt mall ann on 25Mar25)

Thanks

Sorry you are right – 5.5% is the accurate number.